AutoRek and Glasgow Chamber of Commerce come together for free International Business Development working lunch

AutoRek, a global financial controls, regulatory reporting and data management platform, have announced that they’ll be hosting an International Business Development working lunch in collaboration with Glasgow Chamber of Commerce next month.

The aim of the event is to bring together a number of business leaders from Glasgow’s SME community to discuss the International Business challenges they face and will provide them with an opportunity to work together to overcome such challenges. As a business with roots in Glasgow, AutoRek is keen to offer advice to these businesses, as well as give them the chance to collaborate with like-minded professionals and tackle issues head-on.

Headquartered in Glasgow, with offices in London, Edinburgh and New York, AutoRek’s solutions are deployed globally. They deliver a range of financial, operational and regulatory reporting control solutions. They have supported implementations in many leading organisations with projects including high volume data migrations, elimination of spreadsheets and manual processing, regulatory reporting, mitigation of operational and regulatory risk, and reduction in fast close processes. This makes AutoRek well placed in their collaboration with Glasgow Chamber of Commerce to assist these businesses in combating the challenges they face, Lyn Canavan (Head of Marketing) said:

“We have teamed up Glasgow Chamber of Commerce to host our first in a series of International Business Development working lunches. We believe that it presents a great opportunity for local business leaders to collaborate together sharing ideas and common challenges. We already have a good relationship with Glasgow Chamber of Commerce and we are looking to build upon this partnership and expand globally.”

The event will be held between 11:30 and 14:00 on the 5th of March in AutoRek’s offices at the Garment Factory on Montrose Street. A huge plus for these businesses is that the event will be totally free to attend, offering an excellent opportunity to network with other Glasgow-based business professionals and SMEs looking to work on these common issues and expand internationally. With Brexit on the horizon, the impact of it on SMEs has been and is a growing concern. Recently, Barclays has announced that it will be hosting Brexit clinics’ in Scotland from March to support SMEs through Brexit, and, last week, Scotland’s finance secretary Derek Mackay told MSPs that the Scottish economy faces being pushed into a recession “worse than the 2008 financial crash” under a no-deal Brexit. With the loss of multi-million pounds worth of global trade contracts in such an event, it’s no surprise that Scottish SMEs are keen to prepare ahead of it.

AutoRek’s offices are located in the heart of Glasgow’s City Centre, just off of George Square and will be easily accessible for all attendees; just a 10-minute walk from Glasgow Central Station.

Are you interested in attending the International Business Development working lunch? You can sign up for the event on AutoRek’s website:

https://www.autorek.com/events/international-business-development-working-lunch/

Orca launches Innovative ISA to help investors access multiple P2P platforms

Orca, the Scottish fintech, announced today the launch of its Innovative Finance ISA (IFISA). It will enable investors to invest across multiple peer-to-peer lenders (P2P) by taking down

Until now, investors were only allowed to one P2P platform in an IFISA each tax year. Should they want to invest in an ISA from different platforms, they had to go through a painful process of creating separate accounts with each P2P platform.

One interesting stat given by Orca is that in order to achieve the same level of diversification enabled through Orca’s IFSA, it would have taken five years as opposed to minutes now. They can now invest in 5 leading P2P platforms at once.

Iain Niblock says: “The Orca ISA is an innovation that can make investing in P2P far more accessible to the wider investing public. It gives them a diversified, highly attractive alternative to Cash and Stocks and Shares ISAs.

“Investor funds are automatically spread across many of the UK’s leading P2P platforms. This reduces exposure to any one platform and distributes investment across a much broader range of asset classes and risks.

UK Ranks #2 for Startups in Europe. How Does Scotland Compare?

Photo by rawpixel.com from Pexels

Article written by Erin Yurday at NimbleFins

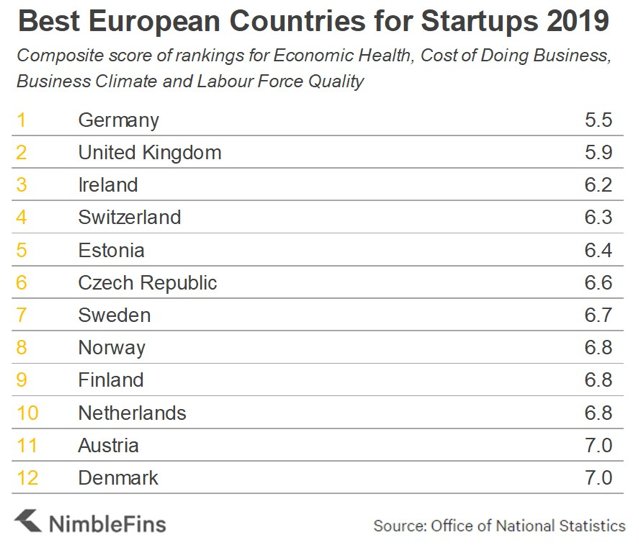

A recent study by NimbleFins showed that the United Kingdom ranked #2 in a study of the best countries in Europe for startups. Germany finished first, in part due to stronger economic health and a better business climate than in the UK. Scotland certainly had a hand in the UK’s second place finish, for instance pulling up the UK’s GDP growth estimates.

In order to compare the 50 European countries in the study, NimbleFins analysed data from the World Bank, the World Economic Forum, the OECD and UNESCO to arrive at their rankings, using metrics related to economic health, the cost of doing business, business climate and labour quality.

Strengths and Weaknesses in the UK

The UK’s #2 overall ranking is driven primarily by a strong showing in the Cost of Doing Business category, where they ranked third behind the Czech Republic and Estonia. Lower-than-average costs of living and salary expectations mean that a new company in the UK should benefit from lower expenses than in many other European countries.

A plan for decreasing corporate taxes will only serve to make the UK even more attractive to new startups, from a financial perspective.

The UK was held back by weaker economic health and, perhaps surprisingly, less trust in the justice system than in most other top 12 countries. While educational attainment levels were lower in the UK than many other European countries, the UK ranked 4thout of the top 12 for offering specialized training services””enabling startups to help develop their employees’ skills and individuals to advance their skills in order to apply for new jobs and improve their marketability.

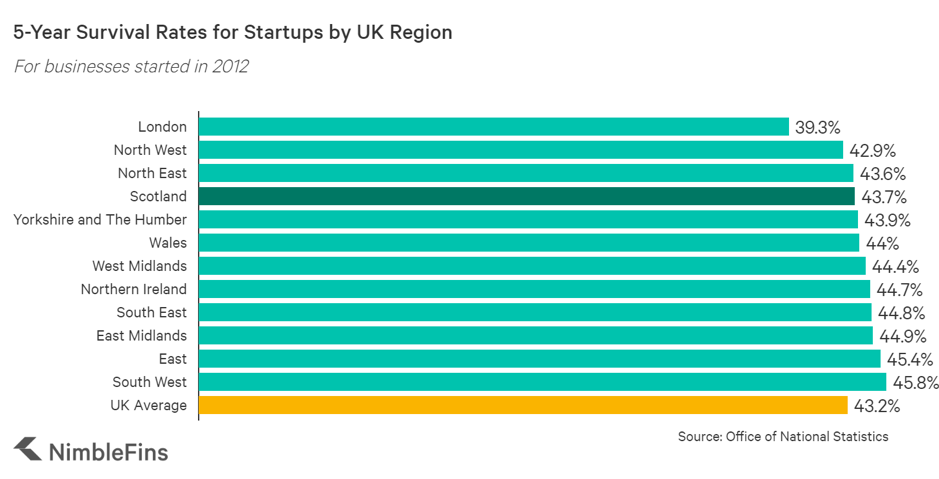

How Scotland Compares: Survival Rates

While most of the data used in the study was not available for Scotland specifically, the Office of National Statistics (ONS) produces other data that lets us see how startups in Scotland fare compared to the rest of the UK.

Using the ONS’s Business Demography study data, we can see that startups in Scotland have slightly higher survival rates after 5 years than the UK average (43.7% vs. 43.2%) and noticeably higher survival rates than those based in London, the startup capital of Europe (43.7% vs. 39.3%).

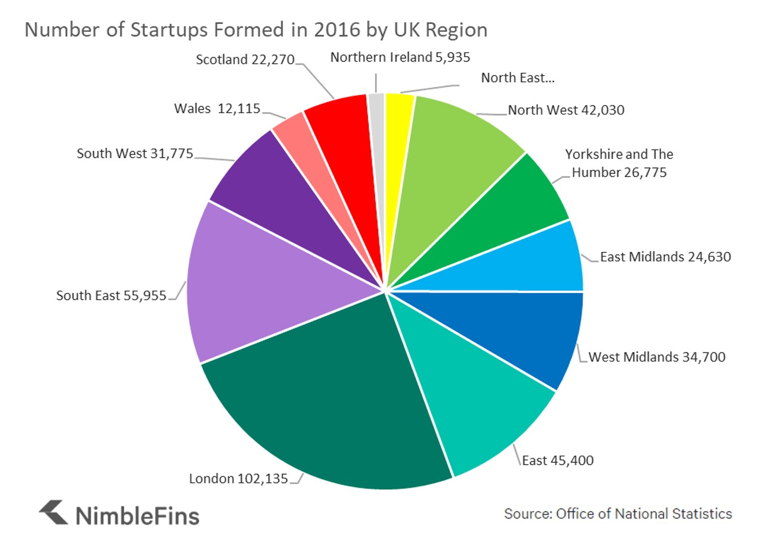

How Scotland Compares: Startup Births

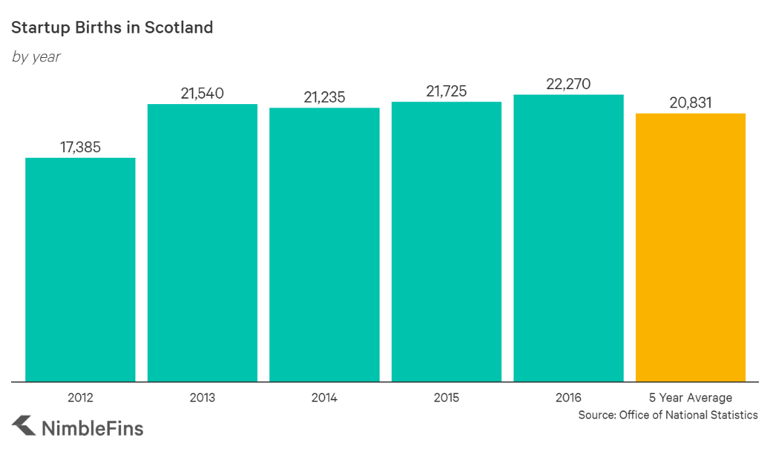

Around 5% of the UK’s startups are located in Scotland. In 2016, the most recent ONS data available, entrepreneurs began 22,270 new companies in Scotland.

Over the five years between 2012 and 2016 the annual birth rate of Scottish startups rose from 17,385 to 22,270, an increase of 4,885 startups per year representing 28% growth over the five years””proving that the Scottish startup scene is active and growing.

On top of this solid growth, the active community of entrepreneurs, support networks and development programmes in Scotland (e.g., The Data Lab’s MSc. Placement Programme) surely contributed to Scotland helping the UK achieve the #2 spot for Best Countries in Europe for Startups.

Fortnightly FinTech Fuse ”“ Spreading The FinTech Network Far and Wide

This last couple of weeks has reinforced to me once again the enormous value in developing the fintech network far and wide.

I’ve believed from the outset that developing a broader and deeper network will enable the community of fintech SME enterprises to thrive and grow as well establish Scotland a significant global fintech cluster.

Therefore, it was a real privilege to share this philosophy at the Scottish Business Network (SBN) event on Tuesday evening in London

Scottish Business Network

The SBN team is by far the exemplar role model in how to bring a diverse group of business leaders together to establish a dynamic network of people sharing a mutual interest in enterprise and innovation.

The event on Tuesday evening very much demonstrated this, organized expertly by Christine Esson and hosted by Alex Threipland and the Silicon Valley Bank team

It was wonderful to hear from Jo Halliday of Talking Medicines and Isobel Brown from Internet of Equals share their stories on their terrific enterprises

I very much appreciated the opportunity to share with the full house of SBN members and guests the role of Fintech Scotland in leveraging the Scottish fintech network to establish a global centre of excellence.

Big thank you to the inspiring host of the evening, Russell Dalgleish, who for a number of years now has provided me with valuable counsel, encouragement and insight.

The SBN event was of real value in further building the Scottish fintech network in London but also on a broader global level.

This is something SBN team is extremely well versed in doing with its community of global scots around the world and something the fintech community will be able to leverage going forward.

Global Network

Building visibility of the fintech developments on an international level is something we are seeing the benefits from in this early part of 2019.

My time in London coincided with a visit from by Avi Karani, the founder and CEO of Alice Financial, the market leading New York fintech firm.

Great to catch up and looking forward to welcoming Avi and his CTO Paul to Scotland very soon.

Earlier in the day I enjoyed meeting up with Miten Amin of VendEx Solutions, a new exciting fintech enterprise platform which we are looking to collaborate with to develop the global network connections for Scottish firms.

Following the recent trade mission to Switzerland I was introduced to Shantanu Bhagwat of the Department of International Trade Venture Capital Unit, who I met in London on Tuesday.

Great conversation with Shantanu on how we can leverage their global network of investors to connect with the innovative fintech enterprises in Scotland.

There will be opportunities to expand on this in late April with Fintech Week and it was useful to catch up with Peter Cunane of Innovate Finance to discuss working together on their Global Summit in London

Looking forward to working with Charlotte and the Innovate Finance team along with Julian Wells of FinTech North on demonstrating the value from an extensive global fintech network.

There are also plans for major global conferences in Scotland which will certainly expand the fintech network.

For example, very much appreciate the great introduction by the wonderful Amanda Fergusson of Marketing Edinburgh to the ESOMAR team regarding their global data conference

This will provide great opportunities to demonstrate data driven fintech innovation from Scotland and looking forward to working with seeing Angela, Neda and Rhiannon on this.

Then also brilliant working with Professor Emilios Avgouleas, Paul Mosson from Law Society of Scotland, Gordon Dow from the University of Edinburgh and Laura Henry from Marketing Edinburgh on the proposed International Law Conference coming to Edinburgh.

Global events such as this reinforce the innovation taking place in Scotland and help build the international connections for Scottish fintech enterprises

A super example of this is the Well Being Alliance, a global movement with firm roots in Scotland in which fintech can play a major role. Thanks to Una Bartley and Jock Encombe, another wonderful long standing network connection, for involving me in this great initiative.

Very much enjoyed the inaugural meeting at the Scottish Parliament with excellent presentation from Dr Katherine Trebeck, Peter Kelly of Poverty Alliance and Andrew Cave of Baillie Gifford

It was great to be there with some of the larger financial institutions such as Aberdeen Standard, RBS and Baillie Gifford collaborating in this valuable network as well as meeting new network contacts such as Charlotte Millar from New Economy

Collaboration Network

There are an increasing number of examples of larger organisations recognizing the value of the Scottish fintech network and looking to play a more active role.

For example, useful to catch up with Robert McKillop and Ross Hayter at Aberdeen Standard Investments on Thursday to discuss mutual fintech innovation opportunities in the asset management sector.

Then also to meet up with Mark Napier of JP Morgan on how to give greater visibility to the exciting developments in Glasgow across fintech enterprises and large organizations.

This was discussed further with the inspiring Michael Young and Rob Huggins of MBN Solutions, who already do so much in amplifying the data driven innovation and talent being developed across Scotland

I’ve also been encouraged by the new interest in the Scottish fintech network and cluster from large organizations hearing about the developments for the first time.

For example, I enjoyed meeting Laura Mason, chief executive of L&G Retirement to talk through mutual areas to explore on innovation

Alongside this the FinTech Scotland strategic partners play a crucial role in the expanding network.

It was valuable to catch up with Simon Pink and Mairi Cairney of IBM to plan joint initiatives and then while in London meet with the Equifax executive team to talk through collaboration progress.

Thank you, Neil Stephenson and Robert McKechnie for hosting me, I very valued the conversation with Equifax colleagues Suzanne Brown, Rhona Parry, Jorge Hernandez, John Power and the breadth of their strategic engagement with Fintech Scotland.

HSBC was at the forefront in creating FinTech Scotland just over a year ago through Colin Halpin’s leadership, and it was fantastic to catch up with Marc Ellis, Paul Macdonald and KC (Kwok Ching Tsui) on the areas we can progress

Excited about connecting more Scottish fintech community into the HSBC innovation sandpit’ and developing fintech collaboration opportunities with the University of Edinburgh

We’ll be progressing this in a couple of weeks when Frank Tong, KC will have an opportunity to meet some of the Scottish fintech community in Edinburgh.

Thank you to Ahmed El Rayis from the University’s School of Informatics for arranging this exciting session which will be a great opportunity to showcase the expertise of the Scottish fintech network in action.

Expert Network

The expertise of the Scottish universities in the fintech network is a significant component of the innovation and entrepreneur activity.

Very evident this week, with the launch by Daniel Broby and his team at University of Strathclyde of a new fintech enterprise Listings Ledger.

Hugely exciting and another example of how fintech activity in Glasgow is thriving in so many ways

This was something which was high on the agenda a meeting with Charlie and Billy from HPE with Adrian, Olga and Tim from University of Strathclyde a couple of weeks ago.

Later that day, it was fantastic to meet up with the newly formed Strathclyde University Student Fintech Society who are going to be another fabulous active addition to the Glasgow fintech network.

The meeting with students wanting to be involved in the fintech network is always very motivating and I was delighted to join Louise of Common Purpose to support the Heriot Watt students on their innovation task.

The role of students, amongst a host of other areas related to the fintech network, was also a key part of the conversation with Gail Boag, David Potter and Brian Windram of Edinburgh Napier University recently.

Excited about working with the team to embrace the academic and student expertise in the coming months.

Similarly, with the initiatives at the University of Edinburgh such as the setting up of the new European Digital Office focused on fintech in the Bayes Centre.

Great to catch up with Morgan Gillies, Gbenga Ibikunle and Damien McGarrigle on this and sharing this fantastic opportunity with the fintech network across Scotland.

Another initiative which is progressing in putting resource in place to take forward is the global open finance centre of excellence.

Thank you Damien for the updates and coordinating the support from the University, Scottish Enterprise and FDATA.

The Open Banking Excellence meet up on Monday evening gave me the opportunity to share the latest developments on the Centre of Excellence with people from across the network.

Thank you to the terrific Dave Jennings and The ID Co team for hosting the session and to the always insightful Stephen Hart for his impromptu session on open banking evolution.

Communication Network

The various meet ups across the Scottish network are hugely valuable in engaging the broad range of participants, I just wish I had more hours in the day to participate!!

Therefore, I always find it valuable to catch up with communication leaders who support the fintech network such as Andy McIver from Message Matters.

Thanks, Andy, for your ongoing support and looking forward to pushing forward on building the Scottish fintech communication channels even further, especially with open banking.

This week it was also an absolute pleasure to meet up with Mandy Rhodes of Holyrood Communications and share our mutual objectives and plans.

Very much look forward to working with Mandy and the team, especially with the exciting emerging developments in respect of fintech, GovTech and CivTech.

The Scottish Enterprise team have always played a leading role in working with FinTech Scotland in developing the network

So, it was valuable to catch up with John Booth when I was in Glasgow to talk through the collaboration opportunities to amplify the substantive examples of positive innovation.

Running Network

My running network is almost as dynamic and diverse as the Scottish fintech network!!

Everything from Strava to Garmin to Good Run Guide to Facebook running groups and more!

My latest running race adventures took me to South Lanarkshire and the town of Strathaven for the Run with the Wind half marathon’.

The reality was it was more of a run against the gales and hailstorms whilst climbing several hundred feet!! It was a great tester and the warm Scotch broth at the end was most welcome.

Next up is the Meadows Half Marathon a week on Sunday, involving nine laps of Edinburgh Meadows!

Before then, there is lots more network connecting to be done around the streets of Scotland and beyond. Until next time

Mi Rewards: the first card-linked, city-wide loyalty scheme. Here’s how it works

In 2018 we launched Mi Rewards, the cardless, city-wide loyalty scheme, in Perth. It’s the first UK scheme to offer rewards that can be earned and spent across a town or city.

Mi Rewards is unique: consumers don’t need a loyalty card or app. They link their payment cards to the programme and, when they spend in participating businesses, they are automatically rewarded.

Over 2600 consumers and 60+ businesses have signed up. So how and why did we develop Mi Rewards?

Miconexhave nearly a decade of experience working with UK towns and cities on digital communication and local currency programmes. We manage a successful Gift Card programme with Perth & Kinross Counciland we’ve helped nearly 30 other cities and regionsto replicate this model.

Next we wanted to add a town/city rewards scheme, to:

- encourage shopping in the city;

- stimulate additional spend;

- better understand and communicate with customers;

- develop new consumer communication channels;

- measure the impact of events, marketing and planning decisions.

The main issue with traditional town and city loyalty programmes is that the consumer has needed to identify themselves at the point of sale. This means that either all staff in all the businesses require training or that additional hardware/software is required (expensive and unwelcome). We had to remove this friction.

Following extensive research, we concluded that payment-card-linked technology would remove the barriers. We partnered with Stampfeet, Perth and Kinross Council’s City Centre Management Team and a steering group of Perth businesses.

“Stampfeet has vast experience with card-linking technology, and our flexible loyalty platform supports the requirements of a city-wide scheme. We were excited about delivering an excellent product with a great vision.”

Asaf Rozin, Stampfeet CEO

Our proposition provides a frictionless solution:

- Automatically rewardsparticipating customers;

- No joining fee;

- No staff training, additional hardware/software;

- Cost to business is 1% of qualifying transactions;

- Points are converted into Perth Gift Cards.

This is highly attractive for consumers and businesses. Once they have registered for the programme the rest of it works automatically. We reward our customers just as Tesco and Nectar do ”“ but without a loyalty card. Mi Rewards and the businesses benefit from data insights into consumer behaviour; we are essentially creating a “single view” of a consumer across a whole network of businesses.

“Mi Rewards allows Place Managers to better understand how people engage with towns and cities and how we can adapt to satisfy evolving consumer preferences. We can improve residents’ experiences and the local economy.”

Leigh Brown, Chair of the Association of Town and City Management and City Centre Manager at Perth & Kinross Council“I love that Mi Rewards encourages people to shop locally. And it doesn’t pitch one business against another but rewards customers for shopping with us all.”

Dawn Cotton Fuge, owner of Precious Sparkle

We now have 2600 Mi Rewards users (1400 of those have linked at least one payment card). We’ve tracked over £100,000 of local spend to date, gaining powerful insights into retail trends. To engage customers further, we introduced “Points, Perks & Prizes”, where they earn points, win prizes or get perks, e.g. exclusive discounts and offers.

How it works

Because Mi Rewards is cardless and requires no additional software, hardware or training, it’s easy to use. Consumers register at Mi Rewardsand link their payment card(s). Businesses register at Mi Rewards Business. Shoppers are rewarded with pre-loaded credit cards (e.g. a Miconex Gift Card) to spend in registered businesses.

Moving forward

We’ve recently partnered with Stagecoach Group to offer Mi Rewards to bus users. We will also shortly introduce mobility tracking apps which will reward people for walking/cycling into the city centre.

Mi Rewardsallows us to communicate more effectively with consumers, gain insights, reward loyalty and encourage healthier living. We’re in discussions with many towns and cities about the UK/Ireland programme rollout. We believe that Mi Rewardsis the future of town/city loyalty.

Contact

Colin Munro, Managing Director, Miconex

01738 444376

colin@mi-cnx.com

Engage Invest Exploit

Scotland has long been recognised as a nation with an established financial cluster and a reputation for innovation – we even invented the Bank of England! By bringing together entrepreneurs, the established financial sector, public sector, government, accelerators and universities, Fintech Scotland has facilitated collaborative innovation across the fintech ecosystem and the momentum behind it has been palpable.

The talent pools in Scotland in financial services and technology have ensured that in the past year alone the number of fintech companies in Scotland has grown threefold. In addition to the growing international fintech companies taking advantage of the reduced capital cost of salaries and office accommodation in Scotland, innovative new homebuilt businesses are creating disruptive and exciting fintech ideas; ensuring that Scotland is building firm foundations to support its aspiration to become one of the top five fintech hubs in the world.

It’s little wonder, then, that within the data driven sectors to be represented on 24thApril in Edinburgh at Engage Invest Exploit(EIE), fintech make up almost a third of the 50+ companies taking part. Now in its 11th year, Engage Invest Exploit draws a global audience of investors and connects them with some of the most ambitious and innovative data-driven companies.

EIE, powered by Informatics Ventures,was at the genesis of the tech ecosystem in Scotland and currently occupies pole position as an International thought leader at the cutting edge of data centric innovation. From its humble beginnings within Appleton Towers at University of Edinburgh, Engage Invest Exploit (EIE) has grown exponentially to become Scotland’s premier tech investor showcase.

Informatics Ventures, located at the heart of the University of Edinburgh, part of the School of Informatics and nestled within the new Bayes Centre (the first of the City Deal Data Driven Innovation hubs designed to foster collaboration and drive the ambition to establish Scotland as the Data Capital of Europe) provides an eclectic mix of practitioner-led entrepreneurship, education, networking and an intense investor ready programme to ensure the participating companies are pitch-fit for the event.

EIE fintech alumni include companies such as Float”“ an intuitive visual cash flow forecasting business ”“ which has drawn on the wealth of tech talent located in Edinburgh. The investor readiness programme developed by Informatics Ventures allowed us to refine and hone the Float pitch for investors and potential customers’ CEO Colin Hewitt commented. From the founding team who pitched way back in the early days of EIE, Float continues to grow beyond its current team of 20and expand its customer base to create a revenue generating, sustainable business with ambitions beyond the 40 countries it already operates in.

Companies taking part in previous EIE events have gone on to attract over £650Million from seed through series A and follow on funding. Last year’s cohort has already secured investment in excess of £4.8Million.

On 24thApril, at McEwan Hall in Edinburgh, more than fifty new and returning businesses will take to the stage to pitch to the investor audience, hoping to stand out from the crowd. Amongst them are the 14 fintech and cybersecurity’ ventures, includingAllatus Unity(creating a powerful regulatory reporting and data governance tech solution),Amiqus (fast secure anti-money laundering identity and compliance checks) and Squarebook(addressing the capital raising needs of high growth companies and introducing a new approach to the IPO process).

EIE attracts around 1000 attendees ”“ international investors, young companies and a high-calibre business audience. It’s the must attend tech investor event in Scotland. The advanced saver discount is available until 31stMarchfor ticket and table sales. Keynote speakers at this year’s event will include Nagraj Kashyap, Corporate Vice President of M12, previously Microsoft Ventures.

Jane Kennedy is Product and Community Manager of TalentSpark, powered by Eden Scott. TalentSpark is a gold sponsor of EIE and Jane is seconded to the Informatics Ventures team to help deliver EIE.

The dangers of cashless and how to design for a digital economy

Blog written by Sergei Miller-Pomphrey – analyst, designer, full-time finch nerd – @goforsergei on twitter and medium

Many have recently spoken about the dramatic cashless uptake by consumers. June 2018 was a big month with the breaking news that UK debit card transactions had overtaken cash transactions for the first time (13.2bn transactions compared to 13.1bn)”Š”””Šreported in various media, examples here, hereand here”Š”””Šand contactless transactions (5.6bn) had grown dramatically, also.

In terms of debit cards, the uptake is an outcome of many factors like fewer branches and cash machines, but probably most prominent is the general cultural shift toward using cash less frequently and leveraging the efficiencies that card transactions bring.

As for contactless, this has been made possible in part by the enhancements made to UK bank cards”Š”””Šall new cards printed in the last several years have generally been contactless-enabled, barring a few slow off-the-mark legacy banks, with the earliest contactless adopters going back a decade (and longer if you’re a real pedant).

Contactless debit cards coupled with smartphone ubiquity, the rise of smartwatches, and Apple, Google and Samsung Pay enabled on almost every device, has made paying by some form of cashless payment easier.

Not to mention the meteoric rise of internet shopping, which now goes beyond buying books and small electronics, with everything available online from food and clothing to holidays and cars.

Also, Direct Debits are now so standard it’s hard to imagine that there ever was a time when you got a physical bill from a supplier and you went to the Post Office to pay it!

(Many) Users are obviously embracing contactless and a cashless economy.

But none of this could have been made possible without merchants evolving to accepting cashless payments as a standard, also.

Your local coffee shop these days is as likely to have a sign that says “No Cash” as it was a decade ago that the sign read “Cash Only”.

The challenge

Let’s cut to the chase”Š”””Ša cashless economy requires democratised, stable and secure infrastructure.

Users need the ability to engage in a cashless economy, which means they need bank accounts to get debit cards and smart-enabled devices to pay for things cashlessly.

Getting a bank account means you need proof of identification and a fixed physical location to call a home.

Even mobile numbers and email addresses are mandatory in many instances these days when applying for a bank account, which means you need a home landline or mobile phone contract and some form of internet access.

And all of that is just for the consumers”Š”””Šbusinesses that rely on cash and cheque need to invest in business bank accounts that generally charge the business a monthly fee and additional fees for transactions, payments, deposits, withdrawals.

Businesses need EPoS machines (electronic point of sale”Š”””Šcard readers) to take payments. In order for card readers to work, they need internet. EPoS vendors can charge monthly fees, flat percentage fees on transactions, or varying tiers depending on value or number of transactions.

Then comes the underlying payments network infrastructure. Mastercard and Visa, the two biggest players in the game”Š”””Šcheck your bank cards, their logos are likely on them! (With American Express being another biggie.)

Last year, in June, the Visa network went downall across Europe. It was a pretty crazy day.

Then, a month later, Mastercard went down.

With the growth in cashless payments, these down times were felt by consumers hard ”“ people were rushing to cash machines to withdraw funds to pay for dinner, buy shopping, go out, or even just manage to make it home safe from wherever they were.

It exposed just how reliant we are, now, more than ever, on systems rather than people. When working in hospitality. If you’re working in a café and your till system goes down, you just have to use a piece of paper, a pen, and a calculator, and you take cash only.

There was no alternative here for those that didn’t already have cash on them or who couldn’t get to a cash machine.

In the grand scheme of things, a few hours of payment processing being down is manageable”Š”””Šthink about how we manage power cuts and bus replacement services, we just need a back-up infrastructure.

At the moment, that backup infrastructure is cash. But this may not always be.

Cash and cashless

Cash

One of the huge benefits of cash and the physical economy is that it is democratised for, of and by the people ”“ you don’t needa bank account for cash, you don’t need a home, you don’t need a driving license, Council Tax bill, phone number, email address or passport.

While some may have more or less money than others, nobody (practically) owns money or the cash economy itself”Š”””Šregardless of who prints the money.

Another huge benefit is that you don’t need a technical infrastructure”Š”””Šcash is good old brain and brawn (counting and moving).

If there’s an issue with a register, EPoS machine or calculator, you can always just figure it out yourself.

Cashless

In essence, many of the benefits of cashless are just the negative points of cash”Š”””Šlike all good evolving innovations, cashless is finding and fixing the weak(er) points of its predecessor.

Cash is physical, so it’s SUPER dirty”Š”””Šit’s pretty disgusting when you think about it.

Cash is physical, so it’s fragile”Š”””Šthe number of times I washed my last fiver while in school makes me want to cry just thinking about it. Or that ripped £20 that you taped back together so you could top up the leccie card and keep the lights on!

Cash is physical, so it goes missing”Š”””Šremember looking all over the house for the tenner that fell out when you emptied your pockets that night?

Cash is physical, so it takes up space”Š”””Šall those times you walked down the street with your pockets sounding like the unmistakable jingle jangle of a high-school janitor!

Holding cash can bring risk.

You could be mugged in the street for the contents of your wallet, if you’re lucky, or sustain injuries or worse if you’re unlucky that day.

Your business could be burgled, losing a day or week’s or month’s takings depending on how often you get to the bank.

One big point about digital however, is that it is every bit as susceptible to theft as hard cash.

The difference being that we now put even more of that burden of protection on the organisations that hold our cash, in exactly the same way that we did when banks first started operating.

The pros of cashless essentially boil down to three things, efficiency, security and convenience.

The bigger issue

System infrastructure is one thing, but socio-economic infrastructure is another, much more difficult issue altogether.

There has been a lot of discussion about two main things to do with the negative effects of a cashless economy (with, of course, many other issues and nuances, also):

- Inherently denying access; and

- Hurting businesses that rely on cash

Let’s take them in turn.

Access

The first part of the infrastructure outline above should act as a warning bell to every one of you reading this”Š”””Šhow do the homeless, those who can’t prove their identity, those without access to internet, the unbanked and the underbanked gain access to the cashless economy?

Access to the cashless economy is a privilege.

Cashless is inherently baking additional privilege in to the world’s economies.

This additional privilege thereby adds more disadvantage those who are already hugely disadvantaged and deprived in our societies to start.

With cashless adoption growing, there’s less need for a physical infrastructure such as bank branches or cash machines (though, of course, more reliance on an network of card readers).

This has negative effectson those who rely on those services, which invariably includes the poor, the elderly, the not-digitally-enabled, the un- and under-banked, and those who just don’t know how to manage their finances, digitally, or engage in the system.

There are many, many, manyarticles to read on the subject.

Business

The second part is about how micro and small enterprises can survive in a cashless economy.

Part of the reason for this struggle is due to cash flow.

Businesses that rely heavily on cash and cheque transactions are able to manage their cash flow more easily against low turnover.

For example, if a cheque takes a few days to clear, then they can write the cheque on the Friday but use the takings from the weekend to pay for the cheque come Tuesday.

Other issues include the additional overheads that businesses need to absorb in order to engage in a cashless economy”Š”””Šphone line, card reader rental, fees on transactions, all of that needs to either come off the business’s bottom line or be put on to the consumer.

The future of cash

Cash will die. Eventually.

Just like the horse-and-cart are no longer the primary mode of logistics and transportation, and the quill is no longer the prevalent form of writing implement”Š”””Šcashless is the evolutionof cash.

It is inevitable.

Now, it may not happen tomorrow or in the next decade. Cash still has some fight in it yet, but that isn’t necessarily down to any inherent traits in the benefits of cash.

The necessity of holding on to cash actually comes from the sheer scale of the culture change required and our failures in being able to adapt quickly enough to build for a cashless economy that was peaking over the horizon for the last decade.

Let us re-frame and reverse a position above”Š”””Šcashless does notinherentlydeny access to the economy.

Cashless doesn’t think. It’s not a thing or a person. It’s a concept. It’s a culture. And it’s a culture born out of the real world and how people interact.

And those that are denied access to the cashless economy is not because of those that are engaging with it, but because financial institutions have not solved access to the economy for those people.

For those that don’t have access to internet, this is due to government and big telcom not having solved issues of access as a right for the populace.

The last one is more difficult”Š”””Šfinancial literacy and awareness, in being consciously able to adapt and embrace a cashless / digital economy. That’s huge culture change and the government and banks and all financial institutions should be working together provide access to information and knowledge that can help these people engage.

And businesses, how do we help them?

Well, part of this isn’t cashless’s fault, again. High-streets all across the UK are being squeezed because of online shopping and changing demand.

Cashless is only one part of a larger trend for businesses and they need to adapt their business models regardless of whether they take card or not.

But they must know that if the trend is leaning towards cashless payments, then they risk losing customers if they can’t accept this payment.

And as for managing suppliers and cash flow, there are ways to re-set yourself there, too”Š”””Šbusinesses need to recalibrate to be able to hold cash for future payments, not pay yesterday with today.

So, what..?

Well, we need to do something about it.

And by we’, I don’t mean consumers. I don’t mean that they need to shop local, ignore online retailers, and hoard cash under their mattresses.

Consumer trends are consumers voting with their feet and the economy needs to react to them, not attempt to control them.

The worry here is that government may impede progress by placing regressive policies on consumers or businesses, instead of acknowledging that change is needed and pushing onwards.

It’s always better to fix forward instead of policing back.

We need to have some form digital economy design council that coordinates and aligns financial institutions, businesses, consumers, and most importantly, government.

We need to agree that access to the digital economy is a right, not a privilege.

If we agree that access is a right and not a privilege, it changes how we frame the issue.

It becomes a social imperative to provide access, just like health, education, security, and infrastructure, rather than putting the blame on consumers and changing habits.

Then we can begin designing forward, finding ways to include individuals that are excluded or at risk of exclusion by the many criteria out there.

Maybe we could increase and speed up government incentives for telcoms to provide internet and cellular infrastructure to those in remote or rural areas?

Maybe financial institutions could leverage their Corporate Social Responsibility policies to provide low-cost starter’ smart-enabled devices to allow those without a mobile phone, a computer, internet, or even a branch to access their bank account?

Maybe financial institutions could provide starter’ bank accounts for immigrants, vagrants, and transients?

Maybe government can create a basic account associated to your national insurance number so that every single citizen has basic access to some form of bank account?

Maybe that could be provided in collaboration with a challenger bank like Starling, who have an infrastructure built for the modern economy?

Maybe.

Maybe.

Maybe.

None of these issues are easily solved, but the conversation needs to be had to start trying to solve them.

Thinking forward instead of back is the key to how we can solve this and build for the inevitable digital economy.

But the first step is to think at all.

Why ”˜adopt’ a MSc Data Lab Student?

Article written by Bethany Rodgers-Rintoul, Delivery Lead at the MBN Academy part of MBN Solutions. MBN are one of the UK’s leading Recruitment/Talent Solutions organisations with a focus on the Data space.

If you follow MBN or The Data Lab, you’ve probably heard a lot of noise recently about The Data Lab’s MSc. Placement Programme ”¦but what really is this Programme? Why do companies take part? And most importantly, how will it benefit my organisation?

What is this Programme?

Essentially, The Data Lab’s MSc. Placement Programmeis a 10-12-week paid internship where current MSc. Data students are paired with companies across several industries and locations in Scotland. This year, we are tasked with placing around 100 students who come from 11 Universities from Aberdeen to Glasgow and everywhere in-between. These students are all funded by the Data Lab and are roughly ¾ of the way through their post graduate studies. They have the full support of the Data Lab and their University and can utilise resources from both.

How it’s organised

MBN, the Data Lab’s official delivery partners for the Programme, train all funded students in Employability skills, work with organisations to promote understanding of the Programme, help shape a suitable Project and match the most appropriate students to. MBN have been delivering the Programme for 3 years.

5 reasons to get involved:

- Address The Data Skills Gap in Scotland

The potential Data opportunity in Scotland is huge and the skills needed to take advantage of this are in great demand, but unfortunately in short supply. This Programme aims to create a steady pipeline of talented data individuals who are perfectly equipped with the relevant skills needed to help them build their professional data capability. The Data Lab MSc Programme differs from most other academic courses as it is focused on building applicable domain and soft skills expertise in addition to theoretical understanding. By developing both technical skills and industry gained “non-technical” skills that are essential to becoming a successful data scientist, we hope that these students obtain the perfect balance of hard and soft skills to ensure success in industry.

- Inclusion and Diversity

Diversity in approach, background and thought is a key driver within most organisations. A student can bring a world of fresh, diverse, new ideas to your company. They can see things from a different point of view, can help to influence decisions from a different perspective and can add value with a wider technological lens. This, along with the added research and support that they have access to, both from their University and the Data Lab, could massively help the development of your company. Often, a fresh set of eyes is all that is needed to solve problems and add innovate insight to your company.

- Gain technology knowledge

Upskilling staff through professional development/ refresher courses is often a time consuming as well as an expensive exercise. University students have been exposed to the latest technologies and tend to be very tech savvy and up to date with the latest trends. As these students are completing an MSc, they often have the added advantage of maturity which can be used to benefit an organisation. When you add “exposure to the latest tools and technologies” to “grounded maturity” you have a powerful combination. This shared knowledge can help you stay ahead of the curve and beat the competition.

- A set of helping hands

We’ve all been in this situation before, 1 million things to do and hardly any time to compete any of them. In brief, these students can help reduce the workplace pressure and “get things done”. Even with minimal commercial expertise, an extra set of hands can make all the difference. Also, with so many things to do and so little time, projects which are not high-priority’ are often put out on the back burner and forgotten about. A student can help with these projects, which in turn lightens the workload for others and can produce very interesting results.

- A chance to give back

These students are at the start of their data careers, this internship will mark the commencement of their practical’ experience. This is a huge and sometimes daunting step for these students, so helping them to establish themselves in the working world of data is a huge deal! We are all where we are today because of people who have coached and mentored us. Now, is it time to repay the favour? When you create an opportunity for a student, you are helping to prepare the next wave of Scotland’s Data Talent.

If this sounds like something that could interest you – please get in touch by dropping me a line at:

I’d be happy to talk you through this amazing initiative!

Bringing Open Banking into 2019 with DirectID Insights

We’ve heard a lot over the last 12 months over the potential that Open Banking can bring, to business and consumers alike. For sure, there has been doubters, but for the most part any criticism has focused on the lack of uptake around Open Banking.

We at The ID Co. are never one to shirk a challenge. We were one of the first UK companies to advocate for the introduction of Open Banking, and we’ve now had over eight years’ experience working with bank data. Last year we delivered on the consumer facing side with the introduction of our app, NoMo, and now we feel we’ve delivered a first with our latest product, DirectID Insights.

To say we’re a little excited about what DirectID Insights can deliver is an understatement. We’re confident that DirectID Insights has the ability to re-shape the way that consumers apply for credit, and will change the way that those applications are then actioned.

As a first, DirectID Insights utilisesOpen Banking technology to deliver bank data into the hands of Credit Risk Officers, Underwriters and Fraud Analysts in seconds.

We all know the way that the traditional application takes place. While some of the basic information is entered online, financial institutions then all-too-often require bank statements to be physically posted in.

The repercussions surrounding this are obvious. The drop-out rate is high. The time between initial contact and the time banks can then start selling in products and services is extended. And worst of all, Underwriters and Risk Officers have to spend hours, potentially even days, manually evaluating bank statements to determine income, outgoings and everything in-between.

Now imagine if there was a way to deliver this information, electronically, in seconds, with all the information extrapolated out into a visual dashboard.

How much time, effort and resource could this potentially save financial institutions?

Think of the customer also. Rather than waiting around at home waiting for the post to know whether their loan request has been granted or denied, they can find out in minutes. It’s a win-win for everyone.

Well, this is exactly what DirectID provides. And it’s all provided courtesy of Open Banking.

For customer’s Open Banking is as easy as logging into their Online Banking. For lenders it offers all the bank data that they could need to make to grant or deny a loan. As an added boon, without the customer sending in bank statements, the ability to make fraudulent applications, or make applications based on spurious details, is seriously curtailed.

With zero integration, DirectID Insights offers a host of options that are critical for Underwriters and Credit Risk Officers, including Account summary to see an overview of each account; Deposits and outgoings analytics; End of day balances; Loan servicing; Gambling analytics and; Transaction Reporting. DirectID Insights offers up to twelve months of bank data for each individual or business which is categorisedand classified.

We’re confident that DirectID Insights will prove to be a major success for The ID Co. As I said at the top of the article, the min criticism with Open Banking has been the lack of uptake. We firmly believe that this new product is a business-critical tool that will prove to be essential for anyone working in Credit Risk or Underwriting, and we have Open Banking to thank for its creation.

Fortnightly FinTech Fuse ”“ Developing the Global FinTech Fellowship

This past two weeks has involved a range of international activities which have further contributed to Scotland being recognized as a global fintech centre.

The time has never been so important to empahsise our global collaboration and inclusive international mindset with all corners of the world, especially Europe.

Importantly, the positive engagement from the international community to fintech developments in Scotland has been hugely encouraging, very much reflected in last week’s trade mission to Switzerland.

European Fellowship

Last week it was a privilege to join seven Scottish fintech firms on the trade mission to Zurich to meet with a range of financial institutions and stakeholders from Switzerland.

Each of the senior leaders from the seven firms delivered compelling presentations on their business propositions to a very engaged European audience.

Congratulations to Jason Forsyth from Agenor Iceflo, David Waddington from Asura Financial, Wayne Johnson from Encompass, David Smith from Renovite, Dave Jennings form The ID Co and Tom Butcher from Trakz Labs for fantastic engagement and showing fintech innovation at its very best.

Massive thanks must go to the brilliant Pat Kunz of Scottish Development International, Noel McEvoy, Marie Gow and James Penn of the Department for International Trade who engineered the delivery of such a constructive trade mission.

We were hosted by the wonderful Sabrina Schenardi at the excellent SIX Group offices for the mission which was chaired by the awesome Manuela Andalora who acted as the magnificent master of ceremony throughout the event.

It was a terrific to join an esteemed panel of Gavin Littlejohn, Katharina Bart, Keith Phillips of the Investment Association and Michael Coletta of London Stock Exchange to share thoughts how fintech can really change the financial services landscape for good.

Later in the day it was great to hear from major influencers, Catherine McGuiness of the City of London Corporation, Maria Leistner of UBS, David Bundi of PWC, Angela Yore of SkyParlour and Petra Arends-Paltzer on driving creating diversity through fintech initiatives.

On the Thursday evening, I was given the opportunity to host a Scotland dinner to bring together the fintech firms with a range of key influencers, investors and senior executives.

This gave me the opportunity to share Scotland’s international mindset based on community, collaboration and a progressive culture.

This was then brought alive even further by the inspiring Gavin Littlejohn who shared the emerging developments of a Global Open Finance Centre of Excellence in Scotland

I must also thank Catherine McGuiness who shared so eloquently her thoughts on the close collaboration between the City of London and Scotland in supporting shared objectives.

The visit to Switzerland also gave the opportunity to catch up with some of the Avaloq team including the innovative Anders Christensen and Philippe Meyer.

Avaloq are certainly a “Rolls Royce’ fintech enterprise making great strides and it is a real privilege that they are one of FinTech Scotland’s founding partners, further demonstrating their strategic leadership credentials

The links with Switzerland are growing stronger and it was wonderful to meet Caroline Rosenberger and Mike Johnson from the Chamber of Commerce team who are doing so much to build on this

Our European engagements have also extended to France this last two weeks and Mickael Paris has been at the Paris FinTech Forum, where once again we were given a very warm welcome and support.

Developing the European fintech collaboration and fellowship opportunities will continue to be an important focus for FinTech Scotland in 2019.

London Fellowship

The Switzerland trade mission also gave me the opportunity to meet and listen to some exciting London based fintech enterprises such as Rebecca Peche from Smart Pension, Sean Hunter from Oak North and Justin Farr-Jones from Creditscript.

I’m hoping they will all make a visit to the fintech community in Scotland soon.

This week saw many of the Scottish financial services and fintech leaders in London for the official launch of Scotland’s financial services prospectus at the Mansion House in the City.

It was a wonderful Burns night occasion hosted by the City of London Mayor which was brought alive by an inspiring speech by the First Minister of Scotland, Nicola Sturgeon and then followed by an awesome Address to a Haggis’ by Steve Ewing of Informatic Ventures.

The evening was a special fellowship opportunity to catch up with many of the inspiring leaders in Scotland such as Gillian Docherty, Russell Dalgleish and Jamie Coleman as well as make new friends such as Anyi Hobson of Commerzbank.

Big congratulations to Clare Carswell and Bronwyn Torrie from Scottish Financial Enterprise for a wonderful evening and for bringing alive Scotland Is Now’ with the prospectus.

The next morning it was along to the London Stock Exchange for the launch of Elite Scotland, the investment funding programme to support high growth companies such as Encompass.

Terrific to listen to Gordon McArthur of Beeks Financial on their impressive journey as well as hear from many of the leading figures from the Scottish investor community such as Sarah Hardy of Archangel Investors, Fraser Lusty of Equity Gap and Jackie Waring of Investing Women.

Supporting fintech firms in accessing funding options is a key priority and it was valuable to have a session recently with a range of investors on progressing this.

Many thanks to Andrew Coleman of Equity gap, Ian Mitchelmore of British Business Bank, Thomas Brock of BE Group, Michiel Smith of Apollo, Aidan Macmillan of Par Equity and Andrew Sloane of ADV for a very constructive session with actions we will follow up on.

The time in London gave me the opportunity meet up with Vishal Patel of Anthemis Group to discuss how we may work together in connecting with fintech investment opportunities in Scotland.

Very much looking forward to welcoming Vishal to Scotland in April to introduce to some of the exciting fintech firms developing a national and global presence.

Global Fellowship

The global connections are a key part in building Scotland’s fintech reputation for international development as well as inward investment.

Fantastic news last week to hear that the Hong Kong based fintech Actelligent will be developing their exciting enterprise in Scotland. Great leadership by Graham Hatton, David Leven and the SDI team.

We are delighted to welcome Charmaine Lo and the team to the Scotland fintech community and support the next stage of their journey along with many other exciting international fintech firms.

There is an opportunity to develop Scottish fintech opportunities with Hong Kong with the opening of the Bridge Pilot Programme. Thank you to Thorsten Terweiden for this.

It was great to share Scotland’s international fintech ambitions with the Global Scot community last week as well and give examples of how we are progressing to be a major fintech centre

Huge thanks to Collette Hughes from SDI for setting up the double webinar to cover all quarters of the world, it was really useful to share the plans of fintech in Scotland

Very much encouraged by the follow up feedback from the Global Scot community from around the world and the offers to support firms as they progress their international plans.

Collaborating to develop the international opportunities is a key part of our partnership with the fantastic team at Deloitte and it was really useful to catch up with Kent Mackenzie and Chris Brown on the areas to focus on for 2019.

The brilliant insights and support from the Deloitte team is a valuable asset for FinTech Scotland.

The global opportunities were also very much on the agenda for the meeting in London with Tom Helm and Sameer Gulati at the Department of International Trade as we discussed the opportunities for leveraging international opportunities.

Very much looking forward to progressing the important work of DIT FinTech Board with Tom and Sameer as well as collaborating for the FinTech Week in Spring of this year along with Graham Hatton and the SDI team.

The FinTech Week showcase event will be the Innovate Finance Global Summit and it was very helpful to catch up with Charlotte Croswell and Rolf Merchant this week in London to develop joint plans.

We’ll also be working with the Fintech North team on this and it was great to catch up with Julian Wells to hear about the terrific work he has been leading in developing the various new initiatives.

I’m very much looking forward to taking up Julian’s offer to speak at the forthcoming FinTech North events in the cities of Manchester and Leeds in the Spring.

Then we’ll be reciprocating by supporting Julian and the team with an event as part of the Fintech Festival in September which will take place across Scotland’s cities.

City Fellowship

Scotland’s cities are further enhancing their reputations as major fintech areas of activity and none more so than Glasgow.

On this it was great to meet up with Graham Smith of Glasgow City Council as well as Paul Hughes, Graeme Rennison, Jamie Rankin and Jacqui Cosgrove of Scottish Enterprise on how we can amplify the great activity to a higher level.

From the exciting developments at the University of Strathclyde through to ongoing progress of firms such as market leading Castlight Financial and Previse, there is much to share with the wider world.

Many congratulations to Previse and Edinburgh based LendingCrowd for being selected for the Tech Nation Upscale programme, well deserved recognition of their high growth potential.

I had the opportunity on Thursday to share these and other examples of the exciting fintech developments with the Edinburgh Chamber of Commerce members including Niki McKenzie from the highly respected Archangel Investors and the leading academic Professor Joe Goldblatt of Queen Margaret University.

Many thanks to Liz McArevey, Alexia Haramis and Rebecca Neish for inviting me to the meeting which was unfortunately cut short by the firm alarm on the coldest day of the year!

I hope we can reconvene for part two’ of the session to share how the fintech developments in the City are relevant to all sectors and businesses

The close collaboration with the Financial Conduct Authority is a key enabler which further demonstrate the value of fintech fellowship.

In this respect I found it very helpful to catch up with Ed Smith of the FCA in London earlier in the week at the Stratford HQ and highlight some of the valuable work Nicola Anderson is leading for FinTech Scotland whilst on secondment to us.

Then yesterday it was fantastic to see so many of the fintech community and the wider financial services sector come along to the FCA Project Innovate event on Thursday afternoon.

A very big thank you to Maggie Craig for her inspiring leadership and to the engaging Steven McWhirter, Molly Benjamin, Katherine Brown, Laura Royle and Thomas Ward for a valuable event

Many thanks to the other contributors to the discussions, including David Mcllwaine from our strategic partner Pinsent Masons, Fiona Kinsler from the exciting Cyber Security firm EncompassIT and the brilliant Nilixa Devlukia from the Open Banking Team

The collaboration being developed across Scotland between fintech firms, established financial services businesses, Scottish Enterprise, the FCA and the Scottish universities is very powerful and is attracting a lot of interest.

It has been really useful to progress these plans with our strategic partners Craig Wilson and Colin Carmichael of Sopra Steria as well as Neil Cunningham and Robert McKechnie of Equifax especially in connection with university collaboration.

Also great to catch up this week with Anneli Ritari-Stewart and Steve Farquhar from our strategic partner Dentsu Aegis on how we can amplify some of the collaborative innovation taking place across our cities.

There have been other fantastic examples over this last few weeks of collaborative fellowship to support the development of fintech opportunities

For example, wonderful to hear about the successful Fife FinTech Skills Academy pilot which completed this week and the plans to build on the success and take to the next stage

Magnificent example of collaboration between innovative fintech firms such as Renovite and Ingenico along with Fife College and Fife Council. So inspiring.

Running Fellowship

My running is often a solo activity, so it was fantastic to have the opportunity to go on a run with fellow runner Pat Kunz of SDI on arrival in Zurich last week.

When Pat said he was going to show me the beautiful sights of Zurich I did not expect this to be a three mile run upwards into the sky above the City.

However, with Pat’s encouragement we made it to the top and the FIFA HQ before enjoying a more leisurely run downhill for three miles.

This all did me a power of good because on Saturday I ran my best Parkrun time for over a year so I guess hills (or should I say mountains) are good for me!!

Thanks Pat, next time it is race around Arthurs Seat when you come over to Edinburgh

My next race is the Strathaven half marathon in a couple of week’s times which I know will involve a few more hills and some wind!! Until next time.