Fintech ”“ never an overnight success

By Anthony Rafferty, CEO, Origo

At the beginning of 2022 everyone was breathing a sigh of relief as the worst of the two year pandemic appeared to be behind us. We looked ahead to 2022 as a year when we could get back to normal’ again.

A year on and the world is looking at a global recession, we have a war in Europe and in the UK, high inflation, rising interest rates, falling GDP and an austerity budget which will see many people and businesses pay more tax.

With the Bank of England’s warning of a two year recession ringing in our ears, there is plenty of negativity in the atmosphere.

Which is why I believe every company every year should look back on their achievements and celebrate their successes.

The tenets of success, certainly as I have found them in my many years in the financial services industry, are that it takes a lot of hard work and it takes time. “Overnight successes” are rarely ever that, but the cumulation of many hours of hard graft by a dedicated group of people, propelled by a vision, a passion for what they do and a resilience to make it work.

This is no better evidenced than in Fintech.

Origo has a long history of working collaboratively with the industry to deliver ground breaking technology. This includes the Origo Transfers Service, our current work to establish the pensions dashboard central digital architecture and our Origo Dashboard Connector, as well as Unipass Identity, Unipass Mailock, Unipass Letter of Authority and the Origo Integration Hub.

Every one of these are developments offering industry-wide benefits, helping to make the industry more streamlined and efficient, helping companies to achieve their ESG goals, as well as delivering better service to the end consumer.

Yet, despite the considerable efficiencies, cost savings and other benefits they bring to the industry, none of them have been overnight successes.

If we take the Origo Integration Hub as an example, it was launched in 2016 as a service for products providers, platforms and software houses in the savings and investment market.

We had spotted that we could help these participants achieve considerable efficiencies, cost, time and resource savings by doing away with the need to undertake resource heavy, time consuming and costly point-to-point integrations with the companies with which they needed to exchange data. Instead we built a centralised hub to which they could link once and then connect to any other user of the hub for key services such as investment valuations, bulk valuations, account opening, remuneration, transfer tracking and bulk transaction history.

It is a common-sense strategy for the industry, fulfilling the very real need for companies to be able to integrate with each other as quickly and as easily as possible. In addition, it meant the industry could become more efficient and competitive, as integrations did not depend on having deep pockets or a significant business case.

Genius, right? Everyone told us so and yet by August 2020, only 21 firms had joined the Hub.

There were plenty of good reasons for it, not least the incredible drain on resources, time and money caused at the start of the pandemic.

But having been in the market for 30+ years we were not fazed by this, as we know with projects of this kind it can take time for momentum to build. You often need your early adopters to demonstrate the benefits before the rest of the industry will come on board.

And this is what happened. As we go into early 2023, we will be looking at over 50 companies, including top industry names, who will be using the Origo Integration Hub, with others in the pipeline.

To achieve success, we have learned that along with the hours of hard graft, dedicated people, a vision, passion and resilience, it also helps to have a little patience.

So, as we head towards the end of the year, we are celebrating our successes, bit by bit and no matter how long they take to come to fruition. I recommend you do the same.

Increasing industry use of encrypted email to combat cybercrime

Recognition amongst financial services businesses of the need to safeguard emails is increasing in the face of financial cybercrime and they are taking action. Origo’s Unipass Mailock recently marked its one millionth email sent though the encrypted system.

Industry providers such as Aegon and Royal London are using military-grade encryption email services to protect their email exchanges with financial advice firms, and other providers are also realising email protection is now essential.

Cyber criminals hack vulnerable email systems and employ sniffer programs which identify valuable emails and take copies of them, which the criminals can then exploit. For example, in just one email in which a client sends their personal and asset details to their financial adviser, there would be enough detail to help criminals commit fraud.

Putting in place a secure, military-grade encrypted email system, one which protects emails in transit, and ensures that only the intended recipient can access the email, as well as providing an audit trail for compliance purposes, now needs to be thought of as base-level security for product providers and financial advice firms, and without a doubt where confidential and transactional data is being sent.

It is also another way for providers and firms to demonstrate value to their respective customers in the precautions they are taking to safeguard their data.

Origo’s Unipass Mailock system has now surpassed one million emails through the system. Looking at industry benefits, not only has this protected over a million communications between providers, advisers and their clients, but we calculate that this equates to £1.9m saved in print, packaging and postage costs, as well as climate related savings of 459 tonnes of CO2 and 154,000 tonnes of water.

The risk to businesses is not just potentially having to compensate clients for losses, and meeting fines imposed by the Information Commissioner’s Office (ICO), but the effect on client trust and the reputation of the business.

As we move to a more digital advice experience, we expect to see companies of all sizes look to protect this potential point of vulnerability and employ encrypted email as a matter of course.

Standard security protocols advice firms can follow

Some general basic actions businesses can take to help protect their businesses against cybercrime, include:

- Having in place standard items of internet hygiene including firewalls, anti-virus software and a virtual private network (VPN) for off-site working.

- Identifying where the risks to the business lie ”“ are they with providers or are they in unsecured communications with the end client?

- Implementing formal processes and procedures, and staff training, to raise awareness of the potential dangers, and how to protect the business against them.

- Having formal cybercrime processes written into a firm’s policy documents, including written instructions for staff to follow where, for example, fraud is detected.

- Having in place appropriate controls for inward and outward communications ”“ such as encrypted email.

- Letting your customers know the potential dangers and what you are doing to protect them.

Photo by Markus Spiske from Pexels

Why Origo is supporting the Research and Innovation Roadmap

Origo has been delivering technology solutions for the UK financial services market for over 30 years. We are proud of that history and also proud to be an Edinburgh-based company, contributing to the economies of both Scotland and the UK.

“With the technological innovations happening in the world today, and the opportunities they offer, this is probably the most exciting time in our history.

“Open Finance Data, which is one of the four themes of the Roadmap ”“ the others are climate finance; payments and transactions; and financial regulation ”“ is one example of the innovation taking place in financial services. Amongst other things, it will enable people and businesses to have more control over their finances by making it easier for them to access their financial information.

We see the value of this type of access every day at Origo. Our technology enables the industry providers to access pension and investment information and by evolving through Open Finance we can use this capability to enable individuals to directly access their information.

To this end, we are partnered with Capgemini to supply the central digital architecture for the Pensions Dashboards Programme, which will enable pension holders to easily access all their pension details in one place ”“ action that is vital for individuals planning for the future and for retirement.

But technological innovation is not restrained by geographical boundaries, so it is important that UK FinTech continues to innovate and push the boundaries, within the highly regulated environment in which we work.

This is about the future of finance, the way people engage with money, their savings and investments. The FinTech Scotland Research and Innovation Roadmap will help enable industry-led collaboration to provide a practical pathway to accelerate the development of FinTech and open up opportunities across the financial services industry as well as the broader economy in Scotland and the UK.

We are proud to be part of this forward-thinking and practical initiative.

Origo – Four of our proudest achievements in 2021

Antony Rafferty, CEO of Origo, reflects on four of the Edinburgh-based FinTech’s key achievements over the past year.

While 2021 has been another year that most people are probably glad to see the back of, as this time of year is traditional a period when we take a step back and reflect, I feel as a company we should take the time to consider what we have achieved.

Origo has a 30-year history of delivering technology solutions that make a difference to the financial services industry and to the consumers buying its products and services. Our expertise is in identifying the pain points for the providers, platforms, software companies, and financial advisers in the market and delivering a utility solution that solves the issue and whicheveryone can buy into.

We are proudly based in Edinburgh, but we work collaboratively with companies from the UK and overseas in delivering our industry solutions.

This year there are four areas I would like to highlight where, despite the pandemic, we have been able to help the industry become more efficient, more cost effective and as a result, help deliver better outcomes for consumers.

1. Being selected to build and run the core architecture of the UK Pensions Dashboards.

This year Origo was delighted to be able to announce that Capgemini and Origo had been appointed to supply the central digital architecture for the Pensions Dashboards Programme (PDP).

Pensions Dashboards will enable pension holders to identify and see displayed their pension policy data, which will help them make more informed decisions around their retirement planning.

This is a project we feel particularly passionate about and Origo was fully committed to progressing pensions dashboards from the day the project was announced. We see it as a major milestone in helping UK citizens to prepare for their futures.

PDP stated that the Capgemini/Origo bid was successful “due to its quality and value for money, plus the credibility and expertise of both parties to deliver the contract.”

2. Driving integration between systems and software.

One of the bugbears of our industry is that systems and software needed to run financial services businesses do not talk to one another and so force the re-keying or manual transfer of data and information between them. Not only does that increase risk to businesses but it makes for inefficient, overly time consuming and so costly operations. The solution is to integrate between companies and systems. In the past that has meant point-to-point integration between individual companies, which is expensive, resource heavy and requires ongoing maintenance and updating as rules, regulation and legislation changes.

As an industry solution, we launched the Origo Integration Hub, which enables participants to integrate once with the Hub and then operate with any other user. Currently, these arefor key operations, such as valuations, account opening, remuneration, transfer tracking and bulk transaction history, and further developments are in hand.

The Hub also helps drive competition and innovation, by levelling the playing field for all players, no matter how deep their pockets.

In 2021 signings to the Hub doubled and we now have over 40 companies integrated, from large providers to innovative new joiners to the market.

3. Doing away with inefficient paper-based systems.

Given we are in the 21st century, it is surprising that paper is still used to the extent that it is in our industry. While tackling operational inefficiencies has not been top of the priority list for financial services firms during the pandemic, for obvious reasons, this is now beginning to receive renewed focus amongst providers as they see it as a means to reduce costs and create operational differentiation in the market.

The Letter of Authority process, which is the way financial advisers notify providers that they are authorised to work with new clients, is a case in point. Currently, advisers have to manually fill in forms and have them signed by the client and then email, or in some cases fax them, to providers. Origo is making a dent in this with our Unipass Letter of Authorityservice, a way for providers to help simplify the current ad hoc way Letters of Authority are processed, creating a utility that delivers greater efficiencies for providers and adviser firms alike.

4. Keeping communications secure.

Cyber security has definitely risen up the priority list for financial services firms in 2021. As an industry we are handling huge amounts of personal and confidential information about individuals, which, if it falls into the hands of criminals, can be used to scam them or steal their identities. This can lead to devastating consequences for individuals as well as fines and reputational damage for the companies involved.

One of the most commonly used ways to communicate, i.e. email, is often the most vulnerable. This vulnerability is why we launched Unipass Mailock as a centralised industry utility to help businesses of all sizes secure their communications.

It encrypts email to keep the contents safe, combined with dual factor authentication, so the sender knows only the intended recipient can open it, and an audit trail is created for compliance purposes.

Two of the industry’s larger providers ”“ Aegon and Royal London ”“ started using Unipass Mailock in the past year to protect their communications with intermediaries and their clients and other companies are in the pipeline to go live.

These are four of our achievements over the past year. We arenot a large company and all that we have achieved is because of the dedication and expertise of our people, who, working together, physically and virtually, have done great things despite the pandemic.

If you haven’t done it already, I highly recommend taking a step back and contemplating your achievements this year. 2021 may not have provided the best environment for success but I will bet you will find you’ve achieved more than you think you have.

Big win for Scottish Fintech Origo

Origo is delighted that Capgemini and Origo have been appointed to supply the central digital architecture for the Pensions Dashboards Programme and will be working with the PDP to help deliver the service for the benefit of UK pensions holders.

Announced by the Pensions Dashboards Programme and the Money and Pensions Service (MaPS) on 6 September 2021, the contract was awarded to Capgemini, who will partner with Origo to deliver the specified elements of the central digital architecture, namely the pensions finder service, consent and authorisation service and governance register, which will form a key part of the pensions dashboard ecosystem.

Origo has been fully committed to progressing pensions dashboards from the day the project was announced. Our 30-year history has been about delivering ground-breaking technology to make financial services more efficient and cost effective, and improve outcomes for savers and investors.

PDP stated that the Capgemini/Origo bid was successful “due to its quality and value for money, plus the credibility and expertise of both parties to deliver the contract.”

The procurement process

The procurement followed an extensive period of engagement by the PDP, with both the pensions industry and potential suppliers, which shaped the development of the technical requirements. This included several market engagement exercises and webinars to explain how the digital architecture will work and the policy background to the programme.

The five-month procurement started with the invitation to tender in April this year. The open and transparent process, used Lot 4a (Programmes and large projects ”“ covering Government official security classification) of the Crown Commercial Service Technology Services 2 framework agreement. This approach complies with all necessary government spend controls and provided a speedy, effective method to procure the digital architecture.

The successful conclusion to the procurement marks the end of the first phase of the Pensions Dashboards Programme, and is a major step towards bringing pensions dashboards to life. The programme now moves into its develop and test phase, as indicated on the PDP programme timeline. The focus now shifts to building the software elements that will make pensions dashboards work and testing the ecosystem, with the volunteer organisations that have signed up to be part of the testing phases.

Richard James, Programme Director of the Pensions Dashboards Programme at MaPS, commented on the day of the announcement: “Today’s announcement of a digital technology supplier marks the moment when dashboards move off the drawing board, and become real. I’m delighted to partner with Capgemini and Origo, who really impressed us with the quality of their bid; and whose deep pensions industry expertise coupled with extensive experience of delivering major programmes makes them superb partners for the programme. PDP now formally moves into its delivery phase, and I am looking forward to working with our new supplier, and across the industry, to make a success of pensions dashboards, and enable individuals to take control of their retirement planning.

Paul Margetts, Managing Director of Capgemini in the UK echoed our own delight “to have been chosen as the digital technology partner to build the core architecture and support the significant milestone of bringing pensions dashboards to life.” He added: “We believe our success is founded not only upon our expertise and deep capabilities but also through our strategic collaboration with Origo, who is dedicated to improving the financial services industry’s operating efficiencies. We are looking forward to working with the Pensions Dashboards Programme to support them in delivering a seamless service that will allow UK pension holders the control and visibility to take action and plan for the future.”

Concept to reality

Guy Opperman, Minister for Pensions, said that the announcement was “a crucial milestone for the dashboards programme, taking things to the next phase, where the concept starts to become a reality.

He added: “We’ve already put in place the primary legislation needed to pave the way for pensions dashboards. Now the programme, in partnership with Capgemini and Origo, can start to implement the technical elements, bringing the delivery of the first functioning dashboards even closer.

“I have previously urged pension schemes to get their data ready for dashboards. My message remains ”“ schemes should be improving their data quality as part of their preparations for participating. The clock is ticking and this achievement is yet another reminder that schemes must be getting ready to connect.”

Anyone interested in keeping up to date with programme updates and future call for inputs can sign up to receive the monthly Pensions Dashboards Programme (PDP) newsletter, and following PDP on Twitter and LinkedIn.

Origo ”“ what are we working for?

Written by Anthony Rafferty, Managing Director, Origo

The other day a member of the team wrote this in an email to us all: “It’s so exciting how highly anticipated this service is ”“ we’re really doing the right thing for people in the industry.”

She was referring to a brand new service Origo had launched in the financial services (pensions, investment and savings) market, with which we had set out to tackle one of the most frustrating issues for the administrators, paraplanners (think para-legals for the financial planning market), financial advisers as well as the product providers and platforms in our industry. This is conveying the authorisation required from the client of the financial advice firms by the providers and platforms, stating that they are authorising the advice firm to act on and transact on their behalf; termed the Letter of Authority (LoA).

On the face of it you’d expect this to be a simple process and hardly an issue for an industry that transact billions of pounds every year. Right?

The actual situation is this: A myriad range of requirements and different pieces of information being required by providers and platforms; paper-based systems; pieces of paper having to be posted or faxed(!) to every individual provider/platform; no way of tracking the process, so no way of knowing if it is being dealt with or how long it will take. You can imagine the resource and cost implications all along the process chain.

Here’s a quote from someone on the front line:

“We offer an outsourced administration support, alongside our paraplanning services, and our administrators spend a lot of time finding out how a provider wants to receive the LoA (not everyone accepts emails and some still insist on seeing the wet signature, and these requirements seem to vary all the time), making sure the LoA actually got to the team which is supposed to be dealing with it and establishing current turnaround times, and finally chasing for information, often spending hours on hold each week only to be told there’s currently a backlog. Providers must also spend a lot of time answering these calls.”*

If you want to read further of the frustrations this is causing those dealing with this administrative burden, read this article on LinkedIn [ https://www.linkedin.com/pulse/sending-letters-authority-2020-debbie-condon/ ].

It’s written by Debbie Condon, founder of Intuitive Support Services, an outsourced administration firm for this market. She tells how she has had to put together a spreadsheet of 100 companies (there are many more in the industry) for her team of administrators laying out what each company needs and in what format and to which department the information should go. Needless to say, we asked Debbie to be one of the testers for our new service.

Hopefully, this gives a flavour of the issues and frustrations being experienced.

So, how have we tackled this. First, we did one of the things we do best, having identified the issue, we brought together a range of different industry participants to ascertain what they would need to create a common, efficient digital process that would meet the requirements of the industry and they would all be happy using.

From these working groups we developed the Unipass Letter of Authority service. Unipass is one of our brands ”“ 8 in 10 financial advisers use Unipass Identity for example to safely connect to the websites of the various providers and platforms they use on a daily basis.

In a nutshell, Unipass Letter of Authority enables the person in the financial advice firm to enter all the client’s details in a common format and for that information to be sent to all providers and platforms on the system. No laborious form filling for the advice firm and no postage cost.

Also, by securely digitising the process, Unipass Letter of Authority enables advice firms to know where they are in the onboarding process, so they can keep up-to-date with progress and keep the client informed, helping to improve their customer service.

This is a service that the industry tells us it has been crying out for and we are delighted to have been able to work collaboratively with participants in developing it. To accelerate the use of the service and the benefits it can bring to the industry, we are making it free to use until July 2021, allowing advice firms, providers and platforms to experience first-hand how the service will work for them.

I’m going to end with a quote from Debbie Condon: “What we need is for providers to sign up to this system as soon as possible. The more companies that are on board, the faster, easier and cheaper this process will become for the industry and the better the quality of service adviser businesses will be able to give to their clients.”*

Having this kind of impact on the efficiencies and for the people in our industry is what inspires everyone at Origo to be the best they can be in their jobs. The new Unipass Letter of Authority is just one of several innovative services we provide for our part of the industry and I am extremely proud of what we do as a FinTech to help address these issues.

An Edinburgh company doing its best to change the industry for the better.

Unipass Letter of Authority launches on 23 November 2020.

* Quotes from articles published by Professional Paraplanner magazine.

https://professionalparaplanner.co.uk/new-letter-of-authority-service-could-be-game-changer/

Two means to help protect against cybercrime

Firms need a combination of robust policies/procedures and technology to help protect against themselves against cybercrime, says Anthony Rafferty, Managing Director, Origo

It seems hardly a week goes by without news of the vast sums of money which has been scammed or otherwise stolen by criminals through cybercrime.

The extent to which cybercrime is prevalent within pensions and financial advice services ”“ two of Origo’s principal areas of focus ”“ has been brought home during the Covid-19 crisis as criminals have ramped up their attempts to trick individuals and businesses into giving away personal and financial details to enable fraudulent transactions.

Recent reports have highlighted that the Financial conduct Authority (FCA) has been investigating more than 150 Coronavirus-related scams since the outbreak began (1) and spent over £300,000 on fighting fraud online in the first six months of the year (2).

The industry’s compliance consultancies have been warning financial advice firms on scams and email hacking. Paradigm Consulting recently warned advice firms about fake email surveys purporting to be from the Regulator (FCA) on the impact of Covid-19 (3), while ATEB Consulting warned on fraudsters hacking personal email accounts and impersonating clients to encash investments (4).

Alongside this are reports of company owners and directors receiving highly realistic scam emails from trusted organisations, including banks, requesting usernames, passwords, and bank details.

This increase in reports and news stories serves to illustrate that the threat to financial services businesses from cybercriminals cannot be ignored by any company.

Data published by the Information Commissioner’s Office (ICO) has revealed that phishing’ by cybercriminals was the second highest reported incidence of the inappropriate disclosure of data’ by company staff (5).

However, the most common incidence of data breach reported to the ICO was information being emailed to the incorrect recipient. That suggests a breakdown or lack of internal procedures.

Clearly, whether dealing with cybercrime or staff error, having a well-documented policy, robust procedures and monitoring of processes, can go a long way to preventing potentially costly data breaches.

Education is another area where firms can help protect themselves from external threat and internal error, including regular cybercrime awareness sessions and training of staff.

Implementing technology ”“ such as employing military-grade encrypted email, particularly when exchanging personal and sensitive information with clients or between organisations ”“ should become standard every-day practice. Encrypted email secures against hacking, enables authentication to ensure the right person has accessed the information, and provides an audit trail for security and regulatory purposes.

We are operating in a world where disclosure of information is a threat on many levels and putting in place preventative measures is essential for any size of firm within our industry.

(1)The data was obtained under the Freedom of Information (FOI) Act by the Parliament Street think tank’s cyber research team.

(2) https://www.ftadviser.com/regulation/2020/09/03/fca-spends-300k-to-fight-fraud/

(3) ttps://www.moneymarketing.co.uk/news/scammers-posing-as-fca-send-out-advisers-covid19-impact-survey/

(4) http://www.atebconsulting.co.uk/news/beware-email-hacking-scam/

(5) https://ico.org.uk/action-weve-taken/data-security-incident-trends/

Time to secure our emails

In February I wrote about the growing awareness of cybercrime targeting the financial services and the industry’s need ”“ and I would say duty ”“ to help protect consumers and businesses against this invidious problem which has been growing year-on-year. Little did we know at that point what was coming down the line.

The current crisis in which we find ourselves ”“ with the public fearful of the pandemic and businesses having to enable staff to work from home ”“ have made both even more vulnerable to cybercrime. Cybercriminals are playing on not only people’s fears around the Covid-19 pandemic but also the unprecedented need for staff to work from home, stretching companies’ communications channels and security systems.

Regulators, including the Financial Conduct Authority (FCA) and The Pensions Regulator (TPR), have issued warning statements on cybercrime and scams, a clear indicator of the seriousness with which they take this issue and the extent to which it is a problem ”“ see FCA: https://www.fca.org.uk/news/news-stories/avoid-coronavirus-scams/.

Incidences of scams, like phishing and smishing’ ”“ i.e. when criminals use emails or text messages to impersonate individuals or organisations to trick people into giving away their personal and financial information or money ”“ are reported to have increased notably over the past few weeks as the Coronavirus has taken hold.

At the same time, the need for data and information, including that of a personal and confidential nature, to move outside of companies’ security systems, has increased the risks for businesses, including that their communications will be intercepted.

For the financial services industry, this risk has been exacerbated by the end of the tax year and the need to meet tax and investment planning deadlines, which has meant advice firms have needed to get client requests and information to platforms and providers in the most expedient way.

As you might expect, most communications are by email, particularly between adviser and client, because that is the most familiar, fastest and easiest channel to use.

As mentioned in my article in February, working with leading cyber security specialist Beyond Encryption, we have developed and launched a new encrypted email solution for the financial services industry, in particular aimed at protecting the communications between product providers, platforms, advisers and end clients.

So, to help financial advisers secure their email communications during the crisis, we’re providing two months free use of the Unipass Mailock premium service for our Unipass identity service users in advice firms. To take advantage of this, users simply enter a voucher code (2monthsfree’ via www.unipassmailock.com/) to get access and there is no automatic renewal and no payment information required to get started.

It is our way of helping the industry to tackle this particular issue which has been magnified by the current unprecedented crisis we are all experiencing.

I would add that in an industry where transmission of data is key, and emails are the primary communication channel and will remain so for the foreseeable future, now, more than ever, it is time to secure our emails.

Cybercrime ”“ protecting the weakest links

Blog written by Anthony Rafferty, Managing Director at Origo

“The FBI say that cyber criminals are deliberately targeting financial services firms. They reckon that has increased by over 100% in the last year. Given that these criminals are operating all over the world, if you think they are only going to target the US, then you need to think again.”

This was the opening statement from Ian McKenna, Managing Director of the Financial Technology & Research Centre (FT&RC) for a session on cybercrime at the centre’s recent Empowering Advice Through Technology 2020 event in London.

The size of people’s pension pots and investment portfolios make pension providers, savings and investment companies and platforms, and financial advice firms ”“ amongst others ”“ prime targets for criminals’ tactics, such as Identity Substitution Theft.

Ian pointed out that over 60% of the FCA’s business plan for 2020 was focussed on cybercrime. Likewise, the Information Commissioners Office (ICO) is focussing on firms where “significant risk” exists, “which is going to be within financial services firms.”

Ian was introducing a panel session including myself and Paul Holland, CEO and founder of Beyond Encryption, to talk about the dangers of cybercrime for the financial services sector, in particular, that section of the sector relating to provision of financial advice and planning.

Cybercrime has been raised as one of the top concerns for financial advice businesses in 2020. Keeping client data safe within a firm is not the problem. It is the passing of information, invariably personal and confidential in nature, between client, adviser, platforms and providers, i.e. where the information moves outside of a company’s security systems, which invariably is the weak point that cyber criminals exploit.

Emails are a case in point. Quite often sensitive information is emailed within the body of an email or in an attachment. Yet sending an email is like sending a postcard through the post ”“ it can be easily read and altered. We hear too many stories about emails being intercepted and data stolen and then used to commit cybercrime. Personal data accessed in this way can be used to scam payments and commit identity fraud, sending of false invoices, requests for passwords and carrying out malware attacks being just a few examples.

Paul Holland flagged the example where conveyancing solicitors’ emails asking clients for final payment on property sales have been intercepted and the bank account details changed. The client’s money is sent but never received because it has been syphoned off by the criminals.

The risks to businesses can be huge. Not only could they be subject to public censure, fines and costs but it can be highly damaging to consumer trust in the business.

We recognise that financial services companies are becoming more aware of their regulatory and compliance obligations, particularly under GDPR, MIFID II and the recently introduced Senior Managers and Certification Regime (SM&CR) legislation, which make the individual accountable for decisions in the firm. In this regulatory environment, deploying email security into any organisation is vital to reduce business and senior management risk as well as to build and maintain trust with clients.

The same applies for B2B companies. Would you prefer to do business with a company where its emails are secured or one with non-secured emails? Which would give you more confidence that they are handling your data and that of your clients’ in a secure and responsible manner?

With firms able to be fined heavily for data breaches, and as cybercriminals become ever more sophisticated in their methods, we believe protecting client data will be an even greater focus for financial services companies in 2020, with businesses of all sizes looking to greater protect their email communications.

Origo has worked with Beyond Encryption to launch a new secure email messaging system, Unipass Mailock, for financial advisers, investment and savings platforms, providers and consumers. It enables users to securely communicate sensitive personal, financial, medical or policy information to their clients efficiently and securely ”“ using military-grade encryption and unique identity authentication capabilities ”“ safe in the knowledge that only the intended recipient can read and reply to the message.

We are making the solution available to over 45,000 financial advisers already using the Unipass Identity service, as well as millions of consumers. By de-risking the industry’s communications our aim is to help protect consumer data as well as business reputations.I’m also delighted to say that Unipass Mailock picked up the Best in Class’ award at the FT&RC technology conference.

It’s worse than that”¦ Jim

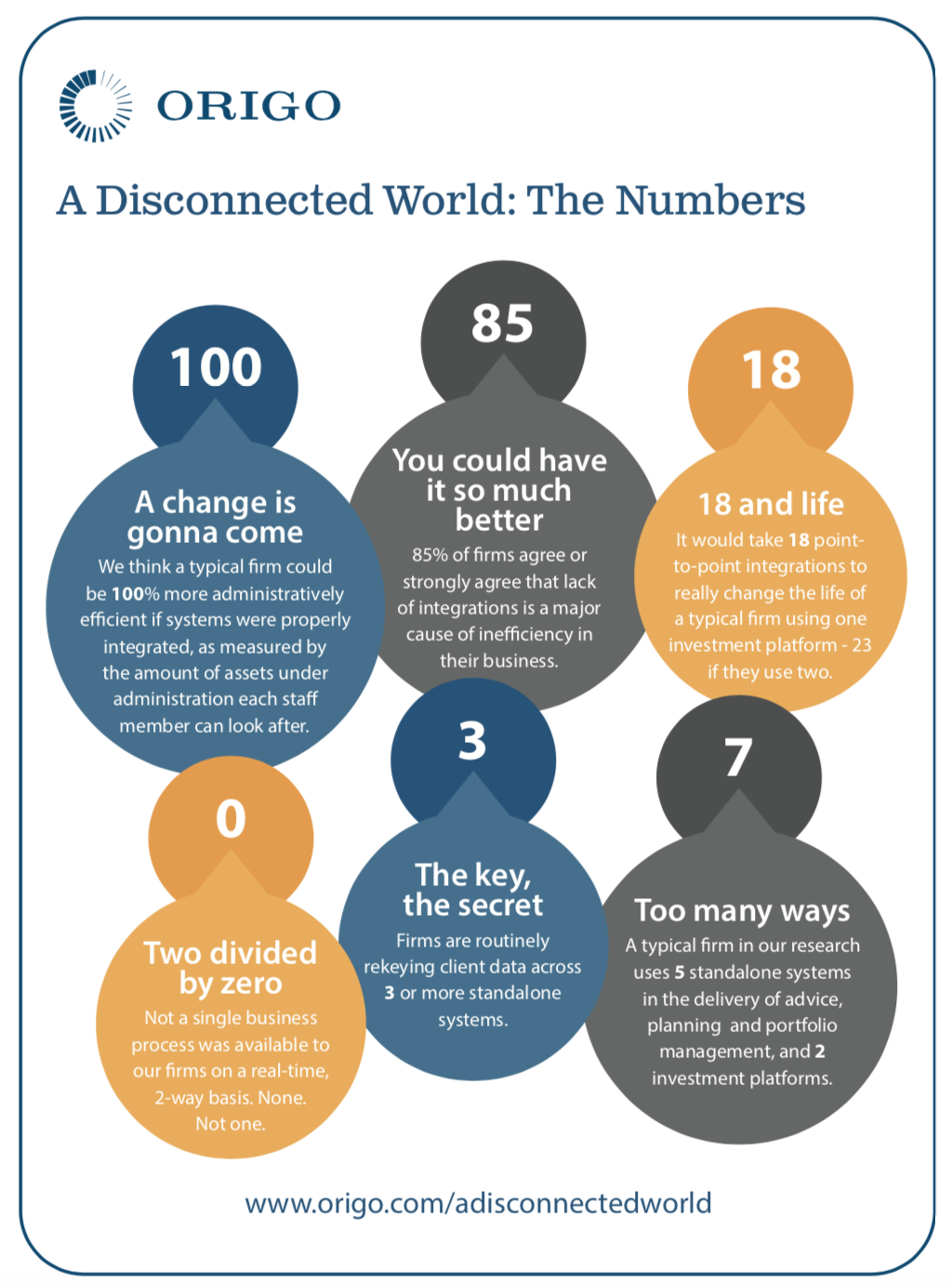

Anthony Rafferty, Managing Director, Origo says recent research into integration between systems in financial adviser firms’ back-office systems reveals a worrying disconnect eating into time, resource and profits of businesses

Origo recently commissioned in-depth research into the integration between systems in the back-offices of financial advice firms, and how this affected the efficiencies and profitability of those firms.

The research was carried out independently by the lang cat, a specialist financial services consultancy based in Edinburgh, and combined hours spent in financial advice firms around the UK mapping processes and analysing how they use the systems they have in place, as well as conducting online research with another 116 financial advice firms.

The conclusion is best summed up by Mark Polson, the MD of the lang cat, who was heavily involved in the research. He says: “We knew things weren’t great before we set out to conduct this research. But even so, we were struck by the impact of these inefficiencies on adviser back offices. Even where integrations do exist, firms aren’t trusting them or using them ”“ with good reason in some cases.”

From closely studying firms’ processes, the research estimates that in a typical financial advice business, staff could be up to 100% more efficient, dealing with twice the assets under administration they currently manage, if the systems they used were properly integrated with one another. In other words, staff could potentially be dealing with up to twice the number of fee paying clients than they are at the moment.

That is both a shocking state of affairs and also one of opportunity ”“ not least for financial advice firms.

To explain what we found: Firms involved in the study on average used five standalone systems in the process of giving advice, building investment and savings portfolios and managing clients; seven when platforms (transaction and administration services) were added; 10 with the addition of more general systems like accounting and office software.

It showed that due to a lack of integration between systems, and trust in those systems, firms are having to plough time and money into otherwise unnecessary manual input and reconciliation. In a typical new business journey, for example, client details were being keyed into systems at least three times!

Key facts from the research can be found on the accompanying infographic.

Currently ”“ and to be fair, despite sterling work by some of the players in the market ”“ advice firms do not benefit from a level of integration that is of real use to them. Integrations are typically point-to-point, with one provider integrating with another for specific purposes, for example for portfolio valuations.

They are also driven by business case, with platforms, CRMs and other system providers naturally prioritising integrations that will bring in higher levels of returns.

On a practical level and worryingly, even where integrations exist, adviser firms said that the lack of consistent and quality data meant they distrusted the output the systems are delivering, the result of which was that they had reverted to inefficient, costly and potentially risk inducing manual processes, because it was a process over which they have more control.

Typically there are 23 point-to-point integrations required within a firm using two investment and savings platforms, without factoring in any systems for protection and mortgage services and general office systems. On a point-to-point basis, that level of integration is never going to happen.

But there is a solution. We identified that if there was a centralised hub, into which platforms, CRMs and adviser software systems and tools could integrate once and then connect to every other player in the market who was also connected to the hub, and which also dealt with making and maintaining the connections, the benefit to the industry could be huge ”“ in particular to the financial adviser firms.

Using a centralised hub would mean any provider new or established could connect with any other provider on the hub, for services pertinent to their operations, no matter the volume of business.

In this way, a centralised integration capability would significantly improve the market’s connectivity, helping advice firms to improve their efficiencies, their profitability and enabling them to deliver faster and better service to their clients, whilst potentially boosting business across the board.

Hence, for the past couple of years we have been building the Origo Integration Hub to help provide that solution.

From a business perspective, for systems and services providers, this hub-and-spoke approach to integration does away with the need for case-by-case decisions and resource restraints incumbent of the point-to-point integration method. Linking to a hub incurs one set of integration costs instead of many, and significantly reduces resource and IT costs, which platforms and system suppliers can better apply elsewhere in their business.

Importantly, it provides the opportunity for all software and service companies, including smaller companies and new entrants, to easily connect with new trading partners if they wish. Also, it enables adviser firms to use the software or service that best suits their business set-up.

Currently, the Integration Hub has 19 companies including some of the big names in investment and savings signed to it, with others in the pipeline.

From a top down perspective it seems illogical that in the 21st century systems do not talk to one another in an efficient manner. However, this is a legacy issue which Origo with its remit to help improve the efficiencies and cost effectiveness of the industry and deliver better outcomes for consumers, is in a position to help resolve.

Read more about Origo here