Scotland is Tomorrow: Developing Responsible Investing in Scotland with rTech?

Scottish Fintech has been a key highlight of Scotland’s modern economic rotation. A more sustainable, inclusive and progressive ecosystem. It is helping to change the shape and face of Scottish e-commerce and finance but has it always been changing it to be more responsible?

Despite the COVID-19 lockdown, the delayed COP26 presents a unique opportunity to reinforce Scotland’s position as a global centre for responsible investing. In doing so Scotland competes with every other country to drive leadership and achieve United Nation Sustainable Development Goals (SDGs). Like Scottish Fintech and the formation of the Scottish National Investment Bank, developing and growing Scotland’s responsible investing landscape is a powerful way to move Scotland’s economy to something more purposeful. The key is collaboration, which stimulates innovation, which encourages inward investment, which produces change in Scotland and overseas.

May 2020 saw the launch of Ethical Finance Hub’s new report, Mapping the Responsible Investing Landscape in Scotland’, which examines the responsible investment market in Scotland, looking at:

- History: the history of responsible investing with a focus on Scotland;

- Ecosystem: the composition of the Scottish responsible investment market, and the linkages between different participants;

- Taxonomy: the terms used by Scottish fund managers to describe their approaches to responsible investment; and

- Market Size: The size of the responsible investing market in Scotland, and how it compares to Ireland and the rest of the UK.

The motivation behind the report was to raise awareness and support the growth of the responsible investing market in Scotland. Having engaged with a number of stakeholders, as well as undertaken internal desk-based research, it was apparent that, whilst data on the sector exists for the UK as a whole, there was little or nothing specific to Scotland available. A link to the report can be found here: https://www.ethicalfinancehub.org/investingscotland2020/.

The report sets out the following call to action:

“Across the globe individuals, organisations and governments are starting to move from talk to collective action as we strive to achieve inclusive economic growth without depleting natural resources. It is now widely recognised that the financial services sector has a fundamental role to play in delivering universally supported targets such as the Paris Agreement and the SDGs. However, despite its potential, the current financial system can be a cause of, rather than a solution to, some of the pressing challenges our planet and its people currently face. In trying to address this predicament Scotland is reflecting on its heritage and seeking to emerge as a leading centre for a new financial paradigm that looks beyond profit and shareholder value to deliver social, economic or environmental impact as well as financial returns.”

In parallel Scottish Fintech can now boast over 120 Fintechs, connected with 15 universities, 16 tech spaces, accelerators and incubators. The conditions are fertile for cross pollination between responsible investing initiatives and Fintech. Yet Scottish Fintech and Scottish Asset Management are, at best, acquaintances rather than partners driving true innovation in responsible investment. Only by linking the success and innovation of Scottish Fintech with the opportunity in responsible investing can Scotland truly compete and succeed as a global leader. Bluntly put, Scottish asset managers and asset owners are missing a step in utilising the talent within Scottish Fintech.

Indeed a key observation in the report was the lack of collaboration between Scottish Fintech and Scottish asset managers in creating new solutions to expand investment, improve data and clarify the taxonomy (the universe of terminology). This is totally in keeping with what I set out as a New Fund Order’, the enablement and transformation of asset management through Fintech.

Stephen Ingledew, Chief Executive at FinTech Scotland said:

“Fintech innovation in asset management and capital markets is a fast emerging trend with a growing number of fintechs in Scotland developing innovative propositions to help the sector be more efficient and deliver better outcomes to investors. THis is being boosted by Scotland attracting many international fintech firms for example Agrud from Singapore and Actelligent from Hong Kong, who are attracted to Scotland because of university research capabilities and highly qualified students and professionals.”

The Scottish Asset Management Market

With £8 trillion AUM (as at end of 2019) the UK is currently the second largest global centre for asset management after the United States. Within the UK, Scotland is the second largest financial services centre after London, and includes the headquarters of Aberdeen Standard Investments – the largest active manager in the UK with a total AUM of £525 billion as of June 2019. Scotland is also a growing centre for fund administration (also referred to as asset servicing’), with strong corporate links with firms based in London and overseas.

Today, asset managers in Scotland include: Aberdeen Standard Investments, Aberforth Partners, Amati Global Investors, Ardstone Capital, Baillie Gifford, Blue Planet Investment Management, Cadence Investment Partners, Cameron Hume, Castlebay Investment Partners, Circularity Capital, Cornelian Asset Managers, Dalmore Capital, Dundas Global Partners, Edinburgh Partners, Kames Capital, Martin Currie, Panoramic Growth Equity, Pentech, Revera Asset Management, RM funds, Saracen Fund Managers, Stewart Investors, SVM Asset Management, Walter Scott & Partners and Valu-Trac. The following are now subsidiaries of larger asset managers based elsewhere: Kames Capital (Aegon Asset Management), Martin Currie (Legg Mason/Franklin Templeton), Edinburgh Partners (Franklin Templeton) and Walter Scott & Partners (BNY Mellon). Firms originally founded in Scotland, like Newton (also part of BNY), still retain a Scottish presence.

In addition, a number of asset managers headquartered elsewhere have branch offices in Scotland including: Liontrust Asset Management, Investec, Janus Henderson Asset Management, Franklin Templeton, BlackRock and Barclays. Lastly there are a number of smaller boutique firms, many of which straddle fund management and financial advice such as; Alan Steel Asset Management, Balmoral Asset Management, Charlotte Square Investment Managers, KPW Investments, Murray Asset Management, Odysseus Capital Management, Par Equity, Rossie House Investment Management, Rutherford Asset Management, Social Investment Scotland, TCAM and Trafford. Together these asset managers manage a mixture of open-end, mandates and closed-end funds for domestic and overseas investors, across a broad gamut of asset classes. The vast majority noted above (if not all) are categorised as active managers’ (that is, they do not track an index). Currently there are no Exchange Traded Fund (ETF) or passive’ (index tracking) providers based in Scotland.

Fintech Innovation is Happening but not Everywhere

We see more innovation in the asset servicing part of the market but again could grow significantly from here. Currently Scotland does not have any investment exchanges upon which to trade assets. Currencies are traded without a centralised location, rather the FOREX market is an electronic network of banks, brokers, institutions, and individual traders (mostly trading through brokers or banks). Scotland has no central clearing companies; for asset managers, the main firms that serve the UK are Euroclear, Clearstream, LCH Clearnet and Calastone. All are based in London or overseas. Similarly all of the large global custodians like State Street, RBC, BNY and Blackrock (that control >90% of the market) centralise their custody operations outside of Scotland. Scottish stock brokers include Redmayne Bentley, Speirs and Jeffries (acquired by Rathbones in 2018) and StockTrade. However the majority of brokerage is controlled by large investment banks like Morgan Stanley, JP Morgan and Goldman Sachs outside of Scotland.

Meanwhile smaller providers like Valu-Trac, based in Inverness, and Multrees Investment Services, based in Edinburgh, offer a range of fund management, administration, custody and back office services. A number of asset managers (e.g. JP Morgan, Morgan Stanley, Blackrock) also base their asset servicing and technology operations in Edinburgh and Glasgow. Computershare is a global leader in financial services and data management, working with around 16,000 global clients and their 125 million customers and having an established operation in Scotland providing relationship management and registry services to around 150 listed companies in Scotland and beyond.

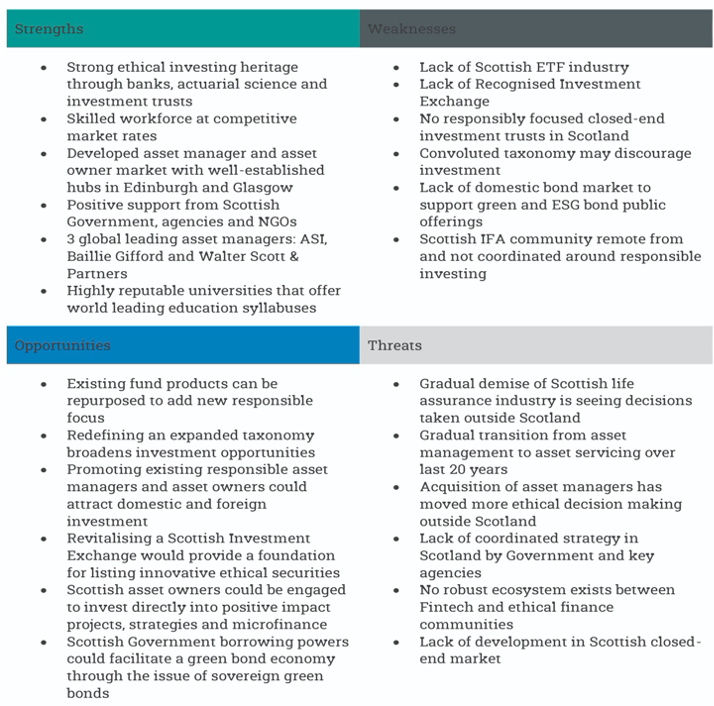

The analysis of the Scottish responsible investing market can be summarised in the following table of strengths, weaknesses, opportunities and threats.

Fig. Extract Mapping the Responsible Investing Landscape in Scotland’.

Page 55: SWOT Analysis’:

Conclusion: A Missed Opportunity

This innovation is not being replicated in the front and mid office of asset managers or asset owners and here the opportunity arises. Scotland lacks many of the traditional levers to stimulate responsible investment. This stymies the size the market could grow to. It also presents as a missed opportunity for Scottish Fintech. The goal is encouraging external investment into Scotland through asset management and asset owners. In doing so to become a global headquarters for responsible investment. Developing technology solutions and platforms to transplant these deficiencies calls on Fintech investment. The dawn of rTech’, responsible and sustainable Technology, with it the New Fund Order’ is set to becoming increasingly Green.

JB Beckett, Consultant, Ethical Finance Hub, Global Ethical Finance Initiative #GEFI #newfundorder #fintechscotland #scotlandisnow #scotlandistomorrow

Co-Author Mapping the Responsible Investing Landscape in Scotland’

Author New Fund Order 2.0 A Digital Resurrection’

Co-Author: The WealthTec Book’, AI Book’ and Paytech Book’

Photo by Karolina Grabowska from Pexels

Scotland’s Fintech: A Tale of Two Cities or Two Towers? Part 2

“The old world will burn in the fires of industry. The forests will fall. A new order will rise. We will drive the machine of war with the sword and the spear and the iron fist”

JR Tolkien, The Two Towers, Lord of the Rings

Scotland’s Finance is enjoying a renaissance, a digital economy, should then history dictate tomorrow’s Fintech? In re-imagining Edinburgh versus London, the Two Towers, can Scotland compete as a viable alternative hub on grounds other than simply cost? In this Part 2, of the article, we explore the UK hub economy as it exists, versus regional ecosystems outside of London and the role education has to play? This then is no history lesson..

Old paradigms, new challenges

Our focus for Fintech naturally gravitates towards Edinburgh and its historical ties with London (the City’)? London and Edinburgh make a fine pair, Tolkien’s Minas Morgul and Orthanc, his Two Towers’. Indeed Edinburgh has served its London master well as an affordable outsourcing location and profited from it. In Part 1 we highlighted the operational leverage of outsourcing jobs from London to Edinburgh.

Whilst cheap has always been attractive; lower paid roles can become quickly commoditised. The first indication of the danger was global-sourcing to the likes of India. Here executives were exploring new lower cost locations. Just as our industry was coming to terms with globalisation it got hit by the Great Financial Crisis. The sense of being at the brink’ changed the long term strategies of many boards and many roles have been targeted by Digitalisation sooner. If you hear agile working’ at work then buckle up.

Unsurprisingly decision-makers and executives tend to be a little shy when it comes to their own synthesis. That will come later. The near-term problem is when those attractively valued skills become superfluous to automation. Fewer roles become a negative feedback leading to emigration, fewer graduate roles, resulting in brain drain, making the country less attractive to investment.

The fintech opportunity

Is then Fintech threat or opportunity? It is a question I am sure that my friend Professor Chris Sier asked himself when he became a champion for the Northern PowerHouse’ and establishment of its Fintech hub (Fintech North’). The reality is that over the last 50 years the UK has moved from manufacturing to a service-based economy and with it the North of England lost its economic leverage in the investment and political apparatus within UK Plc.

Meanwhile Scotland (specifically Edinburgh) benefitted from that industry rotation just as the North, Birmingham and other parts of Scotland suffered. Why? Today UK Plc, unlike say Germany, operates a single hub economy that has gravitated wealth and investment around London, the South of England and Edinburgh. London, itself as a global city, a metropolis of both finance, commerce and politics. It enjoys the multiplier effect that stems from such agglomeration, greater GDP per capita and tax receipts, just as other parts of the UK suffer flat or falling GDP, wage disinflation and stagnant productivity.

Technology then can be THE great enabler, a means to rebalance the economic hot spots of the UK. However it is vulnerable to policy error, inward and external investment naturally gravitating towards London, as new Technology companies seek to target Finance firms from Old Street across to Finsbury Square and into the heart of EC2 and Threadneedle. In doing so they set up shop close by.

Dickens or Tolkien?

The sheer gravity of London cannot be underestimated and it leaves the other centres vying for the scraps. How then should Edinburgh and Scotland respond? Coordination. Either Scotland (Edinburgh) seeks to pursue Dickens’ tale of two cities’, competing directly and openly with London, or are we left in a somewhat Tolkien-esque the Two Towers’ scenario, un-separable and subservient? Do we continue to operate as a satellite of the UK capital or increasingly compete for innovation and inward and external investment? This is the key question I pose to Fintech Scotland, under the stewardship of my friend and ex colleague Stephen Ingledew.

After all, Edinburgh (as the de facto main financial centre of Scotland) has effectively defined itself as much by its relationship to the City of London as it has through its own trading status. This link has been further reinforced as US banks set up front office operations in London and back office in Scotland, extending the tendrils between the two. Yet that relationship looks far less secure in a digitalised world for two reasons.

Firstly traditional Finance is in long-run demise and disintermediation, with it relationships between firms are changing from partner to competitor, as the value chain compresses. In the race for operational supremacy, insourcing becomes outsourcing in a capital lite’ world as employees are unceremoniously morphed into the Gig economy. You just need to count full time employees (FTE) v contractor heads in any of today’s big Finance firms to smell the coffee.

Secondly the requirement for affordable moderately skilled administrative staff, as an outsource centre for London, will become less attractive. Workforces in traditional roles will reduce simply as an effect of Digitalisation. We need only examine the realities of the once Scottish Insurance and Banking leviathans; now ostensibly under the control of firms South of the border or overseas. Workforces are rarely preserved on grounds of nostalgia or political intervention. Competitiveness, tax breaks, public-private partnership and or some other economic or political incentives are needed.

London, “the precious”?

The shifting political landscape, North-South divide, rise of Labour populism and Brexit paranoia appears to have drawn out a more inclusive tone in the Government’s latest strategy thinking.

“It is also a strategy that recognises and respects the devolution settlements of Scotland, Wales and Northern Ireland. With many of the policies that can drive productivity being devolved, it

is a strategy that necessarily brings our work together with that of the devolved administrations as we work in partnership to get the best possible outcome for every part of the UK.”

IS the One-Britain-One-Fintech a dangerous game to play?

Outwardly it is clear the UK Government is battling hard to maintain its balance (see chart) of foreign inward investment post Brexit. Inwardly it seeks to appease the industry outside of London that it is doing all that it can to build better commute links back into the Capital. This policy is not about evenly spreading investment but enhancing the City’s global standing as a hub, which the Conservatives still laud since the Big Bang’.

Why Edinburgh shouldn’t be the new London

The challenge then for Scotland is to compete but also to not replicate the single-hub flaw of the UK model. We should invest and promote Fintech across Scotland’s centres not simply hub its focus around Edinburgh. It is very attractive to run your winners but we need to think about the shape of Scotland’s economy in 25 years from now, not just the next 5 years. Fintech like other modern industries should be an opportunity to replace the old primary and secondary industries lost over the last 50 years, the main driver of unemployment, low wage growth, migration and low productivity in the regions.

Our close neighbours at Fintech North’ are well aware of the challenge. As Chris Sier noted: “There is a deep vein of skills, resources and opportunity in the Northern Powerhouse, but for its potential to be realised it is important that we build a strong FinTech community, which means the public and private sectors coming together and enlisting the support of key stakeholders such as our universities.. Over the last year there have been many positive developments in building the FinTech economy in the UK outside of London, including the FCA’s regional sandbox, the impending launch of Nexus at Leeds University and a number of other initiatives. Events like FinTech North help build the regional FinTech community, and supporting them is therefore very important to grow the regional and national FinTech economy.”

It is important then to have a consistent voice in London and overseas. Fintech Scotland, Scottish Financial Enterprise and Scottish Development International (SDI) can provide this, a voice that represents the Scottish Fintech industry as a whole. Outwardly we should seek to partner firms in London while competing where possible for; investment, for students, for intellectual and entrepreneurial capital. After all to create a self-sustaining Fintech ecosystem requires; initial capital + intellectual capital + workforce + start up ventures + ongoing external investment. Just as Chris Sier realised, inwardly we need to encourage competition but also collegiate working across the different Fintech hubs and incubators in Scotland; Edinburgh, Glasgow, Dundee, Aberdeen, Stirling and others.

New paradigms, new opportunities

Whilst history in Finance carries little utility anymore; Scotland can still leverage its rich and long pedigree of learning and quality tertiary centres to bridge the old economy to the new. For example if we look at the current Fintech courses available in Scotland today then we can see they are distributed across the major centres not just Edinburgh. A quick google search of UK Fintech courses lists the new prestigious Oxford and Imperial courses as the top results.

However it was the University of Strathclyde that offered the first Fintech Masters course in the UK, Stirling followed shortly after with its new Masters course ready for the 2018 intake. Meanwhile Edinburgh University, in the now classical Oxbridge model, created Fintech Innovations’ and, in conjunction with the Scottish Government and private sector, to form Fintech Scotland.

The locality is understandable but the focus must extend far beyond auld reekie and just one university. . We should remember that our own Universities are in direct competition for research, overseas students and, within their own walls, competition between faculties for funding exists. We need to short-circuit these frictional fiefdoms. In learning Finance and Fintech will become interchangeable.

The mission of Fintech Scotland is “FinTech Scotland aims to promote sustainable economic growth through innovation, collaboration and inclusion.” It is the last word that is so critical. I was encouraged by Stephen’s first update as CEO, which promises an inclusive approach to embrace collegiate investment and partnerships and meetings both in and outside of Edinburgh.

So step forth Fintech Scotland. My advice to Stephen Ingledew is to be bold when competing with London but to not repeat the mistake of London. After all we are only five million people and geographically and digitally just next door to one another. Put another way we number significantly less than the London metropolis. Our infrastructure links (bar the far North and South) are far more able to support our population than the road-jammed, high-rise, tube squeezed malaise of London.

Let us create a sustainable, multi-centre, ecosystem to share Fintech skills, build synergies, foster accessible learning and opportunities both inside and outside of the University system. In doing so Scotland galvanises itself as a centre of technological advancement on the global stage, to attract students and investors and from that catalyse start-up hubs around those centres. A nice example could be linking Strathclyde University with Stirling University courses, cross-over projects between Finance and Fintech syllabus and tapping into the gaming industry in Dundee.

The idea of exploring Gamification in Fintech would be pretty obvious in California yet not here. Strange. By building creative and collegiate links, between learning centres, Scottish Fintech becomes a vibrant multi-hub success, fully leveraging the talents across Scotland and not localised around one centre. Otherwise we risk Fintech becoming little more than a defensive strategy to protect the current industry rather than something altogether more ambitious and progressive. Recall I posed whether Scotland’s Fintech should resemble Two Towers’ or Two Cities’? What would Dickens think; what indeed would Gandalf the Grey?

The future of Scottish Fintech is neither. It is something new, not something set in the past. Stephen has the most amazing and challenging role ahead of him to achieve that.

Scotland’s Fintech: A Tale of Two Cities or Two Towers? Part 1

By JB Beckett. In re-imagining Scotland’s new vibrant digital economy, should the history of today’s Finance dictate tomorrow’s Fintech (Financial Technology) map of Scotland? Is Scotland’s Finance and its Fintech tied to London or somehow distinct? Yes or no. In this first of a 2-part article, we explore the dichotomy of enjoying and suffering being a satellite to a hub economy, as Edinburgh is to London. This then is no history lesson..

Historical ties

In the UK when we talk Finance, two cities are quickly mentioned. London and Edinburgh. As most know, Edinburgh’s illustrious financial services history dates back centuries, to the establishment of The Bank of Scotland in 1695 to support the growth of Scottish business, RBS in 1696, the banks placed Scotland on the financial map of the UK despite competition from London. They later bank-rolled the City of London. It saw the introduction of paper money in Scotland; it opened up the opportunity for trade south of the border and the renaissance of a geometric-Anglo city for the modern Georgian world: the Edinburgh New Town.

However should our focus for Fintech revolve around solely Edinburgh and its historical ties with London (the City’)? Standing as the two key financial centres of UK Finance, London and Edinburgh make a fine pair, what Tolkien might have named Minas Morgul and Orthanc, his Two Towers’. Unassailable in their power share. However as Dickens wrote in a Tale of Two Cities’, the opportunity is also a threat:

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to Heaven, we were all going direct the other way””in short, the period was so far like the present period, that some of its noisiest authorities insisted on its being received, for good or for evil, in the superlative degree of comparison only.”

Scotland’s financial sector

“Through the centuries,” said Graeme Jones, Chief Executive of Scottish Financial Enterprise, to a reporter “our financial scene has played a huge part in the fabric and prosperity of Scotland as a whole”. He’s right of course, the addition to banking, the increase of international trade during the 1700s led to marine insurance. Then a growing demand for life insurance during the Napoleonic Wars: families of soldiers paying premiums in anticipation of the worst. Scottish Widows was established in 1815 to service those war widows and remains today in name (albeit a subsidiary of Lloyd’s Bank).

Meanwhile Scotland’s rich tapestry in asset management can trace roots back to Robert Fleming and the first ever investment trust in 1873. In Dundee, Robert saw the massive profits being made by the owners of Dundee’s jute industry and realised they needed to invest it somewhere. It was a model that would be copied across the rest of the UK. Then with every new development in Scottish financial services, so grew the legal profession, the accountancy and Actuarial profession, academic institutions, mathematics, economics, in Edinburgh.

“It’s clear to see,” says Graeme, “that the origins of the Scottish financial services industry aren’t predated anywhere in the UK. As we started to export and import, our home-grown economy started to grow.” Edinburgh thus stands aloft proudly on its heritage; even if millennials today might as easily interpret heritage as old’. Don’t forget that Amazon was only created in 1994 yet millennials cannot remember BA (Before Amazon) and that Jeff Bezos has a balance sheet larger than the entire Scottish Finance industry in totality.

Scotland, using experience to prepare the future

Today, Scotland’s Finance employs around 100,000 people directly and a similar amount again in support services. Scotland’s financial services sector is a vast economy compared to the size of its total populous. In a post-industrial, post-manufacturing age it is one of the country’s biggest sectors, generating around £8 billion for the home economy per annum.

Consequently Scotland is becoming an attractive base for the Fintech entrepreneurs and Edinburgh (the UK’s largest financial hub outside of London) lies at the heart of it all.

Unreservedly, Edinburgh has prospered both through Retail Banking, Insurance, Life Assurance, Wealth Management, Fund Management and Asset servicing on behalf of UK and global institutions. While Edinburgh’s own financial exchange (the smoker’) is long gone; Scottish-based employees have continued to provide expertise in securities servicing, investment accounting, performance measurement, trustee and depositary services and treasury services since London’s Big Bang’ in 86 and before.

Post 2009, Edinburgh has again helped mitigate the recessional pressures across the rest of Scotland for the better part of a decade. That and devolution being a defining feature versus the North of England. Yes, Edinburgh has enjoyed a long history in Finance and its links with the City remain as strong ever since the Scottish Banks capitalised and founded the Bank of England. Scotland’s Economic and Actuarial sciences have been the very DNA of Finance ever since.

However the role of Edinburgh is not assured simply by history, the brand names that still occupy it or by virtue of attractive postcards on Princes Street. Edinburgh is a fantastic city to work in, often wet but full of fresh air that someone in Shoreditch could only dream as they knock elbows for space, tabbing through green space images on social media as they sip their tenner’s worth of artisan flat white.

Scotland, a fintech capital

As effectively ground zero’, then, after 200 years of shaping the modern (old) Anglo-Saxon finance industry, Scotland’s commutation to Financial-Technology (fintech’) or Finance 2.0 asks probing questions about our collective will to transform. It is about new skills but also a new persona of what Scotland’s Finance will look like, how it will be shared and shaped by Fintech. This has far reaching social, economic and political questions that reach deep into our collective psyche, ambitions, collegiate working practices, start-up investment, regional disparities and culture.

How does Scotland become a true global Fintech centre to rival London, Berlin, New York or the Bay area? As Dylan sang times are a changing’. Once the actuaries of Edinburgh and Glasgow held court for the industry, but those days are fading fast. The mutual giants demutualised then quickly became owned by non Scottish conglomerates. As the older actuaries retire they leave behind over 70% of members of the Institute and Faculty of Actuaries under the age of 40 and over 50% of members being non qualified students. Actuaries are already somewhat redundant in terms of predictive modelling but eek sufficient living from changes in longevity rates, cash flow matching and quasi investment analysis. They face an uncertain future as adaptive intelligence and self-learning synthesises, assimilates and optimises 200 years of Actuarial rules in the blink of an eye.

Moreover, in excess of 35,000 people work in Edinburgh’s financial and insurance quarter while more than 90% of all Scottish fund managers (like Baillie Gifford) are based in the city region. Many firms represented host asset servicing teams, client management but fairly minimal front office except for home-grown firms like Baillie Gifford, Scottish Value Management and Kames. The city is home to Europe’s second largest asset fund manager, Standard Life Aberdeen, as well as retail and challenger banks, platforms, Actuarial consultancies and ethical finance providers. In many cases the majority of the staff can be typified as support function or middle Office’ just as the majority of Glasgow’s workforce might be described as back office’ or more politely operational support’.

An urgent need to change gear

All of these roles will be reduced in some way, as companies shift CapEx from people to technology. Even without Brexit, in 10 years we only see 10% of those current roles left in their current form. Some will disappear, others change. Those decisions will be made in London, Paris or New York not Edinburgh. If that’s true then the productivity enjoyed by Edinburgh from London today will deteriorate.

That leaves a hole in the Scottish economy that Fintech must aim to fill. Only slightly less gloomy, a 2017 report by the Centre of Financial Regulation and Innovation by Strathclyde Business School in Glasgow revealed that Scotland could, in a worst-case scenario, lose over 14,063 jobs (14%) in its financial services sector over a 10-year period, the worst-case prediction seeing a loss of £597m in taxable salaries. Conversely in a best-case scenario, investing in Fintech could inversely “lead to the creation of an additional 14,959 jobs in the Scottish banking industry” adding £1.1bn back to Scotland’s taxable income. The report’s co-author, Daniel Broby, told the Herald Scotland that the two outcomes call for a streamlined and coordinated’ approach for the development and adoption of Fintech.