Scotland invests £3.18m to fast‑track fintech growth, jobs and collaborative innovation

Funding backs a Scottish programme turning strengths into real‑world impact

The Financial Regulation Innovation Lab (FRIL), the UK’s centre of excellence for innovation in technology to efficiently meet financial regulation requirements, has secured £3.18 million from Scottish Enterprise to deliver three years of the award-winning programme. The funding will deepen collaboration amongst academia, industry and regulators, and further accelerate the adoption of responsible technology-driven innovation in financial services, supporting the sector’s competitiveness and that of the economy.

Led by FinTech Scotland in partnership with the University of Strathclyde, FRIL will accelerate the adoption of new solutions enabling fairer financial futures and supporting technology innovators to scale their businesses.

The types of industry regulatory challenges that FRIL will address include:

- ensuring AI is adopted by providers in a way that is responsible and explainable to ensure fair financial outcomes for businesses and consumers;

- finding solutions that strengthen the effectiveness, integrity and efficiency of financial crime controls.

Agile prioritisation during the programme will address industry needs and emerging regulations around the use of AI, open data and digital assets. By uniting industry, academia, technology innovators, government and regulators, FRIL will turn shared insight into products, partnerships, investment and real‑world adoption.

To date, FRIL has successfully supported 120 fintech SMEs to accelerate solutions, enabled £28 million in committed private investment and delivered a projected 6:1 economic return on investment for every £1 of public funding.

Jane Martin, Managing Director Innovation and Investment, Scottish Enterprise, said: “FRIL is a shining example of how collaboration between industry, academia and regulators can make a real impact, utilising the development of advanced technologies to create high‑value jobs and attract private investment.

This funding underscores our commitment to fintech innovation and our support for innovative businesses, helping them to scale with confidence and build the global competitiveness of Scotland’s financial services sector.”

Aleks Tomczyk, Chief Executive, FinTech Scotland, added: “The opportunity from the current and forecast future growth of fintech is huge. We are proud of FRIL’s impact to date. FRIL’s success evidences the strategic value of innovation to the economy and the strength of our fintech cluster in simultaneously delivering growth and better outcomes for consumers. Scottish Enterprise’s investment will use FinTech Scotland’s proven Innovation Labs model to accelerate innovation in large companies and speed growth in fintechs.”

Professor Eleanor Shaw, University of Strathclyde, stated:“We are delighted to be a partner again in delivery of FRIL phase 3. Continuing our triple helix partnership approach ensures we can deliver on our mission to drive positive impact through useful research, learning, and innovation. This approach has so far demonstrated its success in delivering for Glasgow City Region, and we are excited about supporting this to become a national programme.”

Derek Shanks, Technology Platform Lead, Lloyds Banking Group, commented: “We’ve supported three FRIL innovation calls as a challenge partner and have seen first-hand the value of this model. It brings together the right mix of expertise, technology and challenge to turn ideas into real solutions. We welcome Scottish Enterprise’s investment and look forward to building on this partnership over the next three years.”

Calum Murray, CEO and Founder, Amiqus, noted:“The potential impact delivered by FRIL over the next three years to the broader Ecosystem is enormous. Thanks to a previous FRIL financial crime innovation call, we were able to build, pilot and take to production new capability to directly support Virgin Money with their new business onboarding journeys.

This three-year commitment effectively sets the stage for collaborative and rapid progress across both financial services developing new capabilities with the support of a wide range of fintechs going forward. It’s a win win on all accounts.”

Benefits reliance rising in every region of Great Britain, new financial data shows

Smart Data Foundry launches new Benefits Reliance Indicator using transactional data from 5 million bank accounts

Smart Data Foundry has launched a new data indicator designed to help policymakers, local authorities and researchers better understand where people may be coming under increasing financial pressure.

The new Benefits Reliance Indicator, available through their map-based Economic Wellbeing Explorer uses aggregated anonymised transactional data from NatWest. This data covers five million consumer current accounts across Great Britain and highlights areas where benefits from Universal Credit, Housing Credit and Tax Credits constitute 20% or more of people’s incomes.

The launch comes at a time of continued cost-of-living pressure, with the Food and Drink Federation forecasting food inflation could reach up to 10% by the end of 2026 and the energy price cap expected to rise again this summer, local authorities face growing pressure to target support effectively. At the same time. Department for Work and Pensions statistics show that more than a third of people (32%) receiving Universal Credit are in work, underlining the growing role benefits play in supplementing low or variable incomes.

Unlike traditional survey-based datasets, the Benefits Reliance Indicator provides a near-real-time view of how people’s income composition changes month-to-month. The indicator measures the proportion of people in a local area for whom means-tested benefits account for 20% or more of total income. This threshold was developed in consultation with local authority stakeholders as a meaningful signal of financial vulnerability.

The data combines income from Universal Credit, Housing Credit and Tax Credit with earnings, pensions and other income sources to provide a fuller picture of financial wellbeing – and where communities may be more exposed to labour market changes and welfare policy reforms.

Data to 29 March 2026 reveals:

- A rising proportion of people across England, Scotland and Wales relying on benefits for at least 20% of their income. This has been rising for the last two years. Scotland has seen the biggest increase, at 1.83% over the past 2 years, with benefits reliance in Wales increasing by 1.7% and in England by 1.25%.

- There are strong regional variations within England, Scotland and Wales:

- Wales has the overall highest rate of benefits reliance, with South East Wales at 9.36% – an increase of 2.11 percentage points over the last two years. Whilst North Wales has the lowest proportion at 6.64%, it has also seen a rise in benefits reliance over the last 2 years, as has Mid and South-West Wales – rising from 6.05% in March 2024 to 7.59% in March 2026.

- In Scotland, overall reliance is lower than in Wales and whilst there is an upward trend, it is much less steep. However, in recent months Eastern Scotland has seen a rise of 4.82 percentage points to 7.37% of our sample in that region with incomes consisting of 20% or more from Universal Credit, Housing Credit and Tax Credit. West Central Scotland has seen a similar rise, with a 2.42 percentage pointincrease over two years and 8.38% of our sample now showing benefits reliance. North East Central and the Highlands and Islands have shown the smallest increases, both under 1 percentage point.

- In the North of England, the area with the highest rate of benefits reliance is North East England, at 9.49% of our sample. North East England is also the region with the biggest growth (1.6 percentage points), followed by Yorkshire and the Humber (1.51 percentage points and North West England (1.42 percentage points).

- In the South of England, benefits reliance becomes less prevalent; the South East has the lowest proportion at 4.85%, but similarly to Scotland and Wales all English regions are seeing a growing reliance on benefits. London is an outlier in the south, with 7.75% of our sample showing benefits reliance.

The new indicator has been developed to help organisations identify emerging hardship earlier, target support more effectively and monitor the impact of welfare reforms, labour market changes and wider economic shocks. It will be updated monthly, and can also be filtered by age group and income range.

Dougie Robb, DEO of Smart Data Foundry added “Too often, financial hardship only becomes visible once people reach crisis point. By showing where people’s incomes are supplemented by means-tested benefits in near real time, we can better understand the role these benefits play in supporting people’s living standards – and where financial vulnerability is building.

“That means organisations can better understand changing economic conditions and target support where it may be needed most, as well as evaluate policy changes much more quickly.”

The Benefits Reliance Indicator is available to all users of the Economic Wellbeing Explorer, alongside a companion aggregated research dataset in Smart Data Foundry’s secure research environment, MyFoundry. The Economic Wellbeing Explorer is free to access at national and regional level, with local-level data available on subscription. Organisations interested in understanding benefits reliance within their own local authority area can request a personalised walkthrough of the data and platform.

To support the launch, Smart Data Foundry will host a webinar on 26 May 2026 exploring the new indicator, emerging trends and practical applications for targeting interventions and tackling poverty.

NatWest becomes first UK bank to launch home-buying guidance in ChatGPT

Users can now explore buying or re-mortgaging options within one of the world’s most used AI platforms.

On 30 April, NatWest Group has announced that it has become the first UK bank to offer an app in ChatGPT, providing NatWest-specific home-buying and re-mortgage guidance. This marks a new way for consumers to access trusted information and begin their home-buying journey and is an important step as NatWest continues to invest in technology and AI to meet customers’ evolving needs.

NatWest now appears in the ChatGPT app store alongside well-known platforms such as Rightmove and MoneySuperMarket. This means customers and non-customers can add and tag the bank in a query to receive NatWest‑specific mortgage and home‑buying guidance without having to leave the platform. Users will then be signposted to NatWest-owned channels to take the next steps, including to access specialist advice, appointments for colleague support or digital mortgage applications.

Consumers can explore their mortgage options and support decision-making in a more personalised way, with ChatGPT drawing on publicly available NatWest APIs to calculate how much they could borrow, test affordability and deposit scenarios, and receive tailored mortgage rates. By sharing details such as their income and monthly outgoings, users can receive responses grounded in real numbers, returning to the conversation later as their circumstances or questions evolve.

Conversations within the app are clearly branded as NatWest, so customers understand when they are receiving responses from the bank.

Solange Chamberlain, Retail CEO, NatWest Group said: “As technology and AI open up new ways for people to access information and think about their finances, NatWest is focused on meeting customer needs by showing up in the right places at the right time.

Buying a home is a major financial decision, and we want to support those early mortgage planning conversations wherever they may take place. By bringing trusted NatWest mortgage guidance directly into ChatGPT, we’re giving consumers more choice in how they explore their options in a more personalised and accessible way.”

NatWest continues to transform the digital mortgage experience and currently leads the market with the largest flow of digital new business. This builds on its recent partnership and integration with Rightmove, that sees Natwest provide home buyers with an instant fully digital NatWest mortgage decision in principle when applying through Rightmove, enabling customers to then complete their full application online.

Modulr and Sardine partner to bring real-time, AI-enabled fraud detection to automated payments

Sardine, the leading agentic risk platform to fight financial crime, today announced a partnership with Modulr, the payments automation platform built to scale. Through the partnership, Sardine will support Modulr with a suite of integrated fraud and anti-money laundering (AML) solutions.

The integration, as part of Modulr’s broader investment in financial crime and risk management capabilities, enables Modulr to leverage Sardine’s platform to detect and stop financial crime across card and real-time payment rails, while strengthening AML compliance and operational controls as the business scales. It is integrated into Modulr’s Risk & Compliance Hub – a connected set of tools and infrastructure that spans the entire customer lifecycle and is built to protect customers, reduce friction, and prevent financial crime.

Businesses are increasingly expected to move money instantly, yet many fraud and AML systems were built for slower settlement cycles and manual investigation workflows. By integrating Sardine’s risk platform directly into its payment infrastructure, Modulr is able to leverage the latest technology to prevent and manage financial crime.

“Real-time payments fundamentally change how fraud and AML needs to be managed,” said Soups Ranjan, CEO and Co-Founder of Sardine. “When funds move instantly, risk decisions need to happen just as quickly. Modulr’s platform delivers critical capability for automated payments, and we’re excited to help ensure those payment flows remain secure as they scale.”

“For Modulr to provide our customers with the ability to run mission-critical finance operations accurately and at scale, we need strong compliance that gives peace of mind without adding friction – which is why we are partnering with tools like Sardine, and building a Risk & Compliance Hub that monitors every step of the customer journey to prevent financial crime,” said Ben Taylor, Chief Operating Officer at Modulr. “For our customers, that translates to streamlined and low-friction onboarding, a better money movement experience, and crime prevention infrastructure that keeps pace as their business grows.”

Modulr’s payments automation platform streamlines money movement with greater accuracy, control and reliability – built to scale and powering use cases across payroll, supplier payments, lending, and travel. Sardine backs that network with a track record of protecting over $1T in transaction volume across a global customer base of enterprises and financial institutions. Sardine also operates the fastest growing fraud data consortium, spanning more than 5.5 billion devices, 670 million consumers, and 2.8 million businesses. By protecting funds across some of the highest risk industries in financial services, Sardine gains early visibility into emerging fraud patterns. That intelligence helps Modulr’s customers stay ahead of evolving threats.

Glimzer x Sprint Enterprise: a live data feed for UK financial advice firms

By Glimzer and Sprint Enterprise Technology

Every UK financial advice firm faces the same problem. Client information sits in one system, while plan and valuation data sits in another. Keeping them in sync leads to manual data entry, duplicated work, and advisers switching between logins to find what they need.

We’ve teamed up to address this.

From today, Glimzer and Sprint Enterprise are connected by a live data feed via Sprint’s FINIO data hub. Financial advice firms can stop entering the same information twice, stop switching between systems for current valuations, and work from a single, up-to-date view of each client plan, with far less manual reconciliation.

The problem we’re tackling together

Ask any practice manager where their time goes and manual admin will be near the top. Plan valuations entered into spreadsheets. Provider data keyed into the CRM by hand. The same client details entered multiple times because different systems require them. Advisers logging into one tool to check a figure, then pasting it into another.

None of this is new. And none of it is really an adviser’s job. It’s what happens when systems that weren’t built to connect are expected to share client data.

The fix is simple in principle: connect the systems, let the data flow, and remove the need for manual workarounds. In practice, it requires two teams committed to building it properly. That’s what this partnership delivers.

What the integration does

FINIO is a data hub that provides a single integration point, covering multiple investment platforms – with data normalised, reconciled and enriched and acts as a conduit between software providers and financial advice firms. With this integration, that data now flows directly into Glimzer.

Advice firms can access the data they need without logging into another system, without relying on spreadsheets, and without uncertainty about whether the data is current.

Why we’re building this way

Glimzer’s approach to integrations is focused. We prioritise a small number of integrations that work well with high-quality partners, rather than building a long list that only partially works. The teams we integrate with need to share our focus on reliability, responsible data handling, clear support, and delivering real value to UK financial advice firms.

Sprint Enterprise Technology, the team behind FINIO, fits that approach. Their data hub is widely used across the UK advice market, and a data feed like this requires a partner who will build and support it properly. Working with Gary, Emma, and the wider Sprint team has been straightforward from the outset.

A bit about FINIO

FINIO is built by Sprint Enterprise Technology. It sits between UK investment platforms and the tools financial advice firms use, consolidating plan and valuation data from multiple providers into a single feed. Firms using FINIO benefit from one source of data that is normalised, reconciled and enriched that would otherwise need to be gathered from each platform separately.

A bit about Glimzer

Glimzer is a CRM and practice management platform built specifically for UK financial advice firms. The aim is simple: give firms their time back. Less admin, more time with clients. It’s built in the UK and designed around how advice firms actually work.

What Tom says

“Manual admin is one of the biggest time drains in any UK financial advice firm. Duplicate data entry, switching between systems to find a single number, and maintaining records manually all add up. Every hour spent on this is an hour not spent with clients. Partnering with FINIO was an obvious step. Dan, Gary, Emma, and the wider Sprint team have been great to work with and made the build process smooth.”

Tom Matthieson, Founder, Glimzer

What Gary says

“We’re pleased to welcome Glimzer into the FINIO ecosystem. We focus on working with partners who are building well-designed, practical tools for UK financial advice firms, and Glimzer fits that well. By connecting to FINIO, firms can access reliable, up-to-date investment data within their CRM, helping reduce manual work and improving day-to-day efficiency.”

Gary Shepherd, Business Development Director, Sprint Enterprise Technology

How to switch it on

If you’re a Glimzer customer already using FINIO, get in touch and they’ll guide you through enabling the feed for your firm.

If you’re a financial advice firm reviewing CRM options and want to see how Glimzer works, book a 30-minute call and they’ll walk you through it.

Building societies face growing “Digital Delivery Gap” as member expectations outpace communication infrastructure

New research from Legado highlights structural challenges in communication infrastructure despite rising digital expectations from members

Building societies are facing a growing “Digital Delivery Gap” as member expectations for simple, digital communication continue to rise, while underlying systems and processes struggle to keep pace.

New research from UK fintech Legado highlights a structural challenge across the mutual sector. The Building Society Insight Report 2026 finds that 91% of building societies say their communication systems are not fully integrated with core member platforms, while 73% rely on three or more systems to manage communications.

At the same time, 82% of organisations continue to send more than a quarter of communications by post, and only 18% say members can complete most key actions fully online.

This gap is emerging as member behaviour shifts. 72% of members already use digital platforms to manage their accounts, and 80% would be willing to sign documents digitally if available.

Founder and CEO Josif Grace said:

“Building societies have made strong progress in digital banking, but communication has not evolved at the same pace.

The challenge is no longer digital adoption. It is how communication is delivered. The opportunity now is to simplify that experience and make it consistent for members.”

The research also highlights the impact on member experience. 22% of members say they have been unsure whether their building society received or processed a document they sent, reflecting a lack of visibility across communication journeys.

Legado will be sharing findings from the report at the Building Societies Association Annual Conference, taking place at the EICC in Edinburgh on 28–29 April, where the team will be available at stand 22.

The Building Society Insight Report 2026 is intended to support a wider industry conversation around how the mutual sector can modernise communication while maintaining the trust and accessibility that define the model.

The full report is available here.

Legado, headquartered in Edinburgh, supports financial institutions in delivering secure digital communications, document management and signing workflows. Its clients include FNZ, Quilter, Scottish Building Society, Moneyhub and Co-op Legal Services.

University of Glasgow and Lloyds Banking Group announce groundbreaking agentic AI research programme

- The University of Glasgow and Lloyds Banking Group have launched a four‑year research partnership to explore how AI can support software and data engineering.

- The project will help Lloyds Banking Group implement agentic AI at scale within their software engineering practice, while giving University researchers a unique opportunity to study large‑scale engineering transformation in a real‑world setting.

- The partnership will create a PhD, a Masters of Research and a post‑doctoral role.

- The project’s findings will guide how Lloyds Group scales the use of agentic AI across wider data and engineering teams and contribute to the development of best practice, national policy and industry standards.

A new research partnership between the University of Glasgow and Lloyds Banking Group is setting out to explore the potential of AI to support software and data engineering.

Over the next four years, the partners will explore how large language model-based coding tools called agentic AIs could support and enhance the work of software and data engineers at Lloyds Banking Group.

Agentic AIs are software tools which act as semi-autonomous ‘agents’ to complete tasks of varying complexity. In software and data engineering, they are already being used to write and debug code, solve technical problems, and perform a variety of project management tasks.

As the UK’s largest digital bank, Lloyds Banking Group is investing significantly in developing new digital software and services, alongside training and new skills for colleagues, to support its 28 million customers.

The University’s research team and Lloyds Banking Group will work together to design experiments that test the efficacy of agentic AI for high priority activities in individual software teams. The team will use a variety of empirical software engineering research techniques to gather evidence, such as data mining.

The project will help Lloyds Banking Group implement an agentic AI approach to software and data engineering and measure the impact across their organisation. At the same time, it will provide software engineering researchers at the University with a rare opportunity to study and contribute to a large-scale transformation to software and data engineering practice.

The collaboration will create a PhD and a Masters of Research position at the University, along with a post-doctoral research associate post to work with Lloyds’ software engineering teams.

Dr Tim Storer, of the University of Glasgow’s School of Computing Science, will lead the University’s side of the partnership along with colleague Dr Peggy Gregory.

Dr Storer said: “Agentic-driven software engineering is a fast-developing sector with the potential to enable human engineers to work more efficiently by automating some tasks and allowing them to focus their skills on higher-level work.

“However, there has been relatively little research in industry on how integrating agentic AI into software engineering practices can be done effectively in large-scale organisations.

“We’re delighted to be partnering with Lloyds Banking Group on this groundbreaking project. Together, we will enable the Group’s plans to increase their software development capacity, produce high-quality research for the benefit of all, and influence national policy and industry standards.”

Lloyds Banking Group’s contribution will be led by Dr Shane Montague, Head of Research Engineering, with executive sponsorship from Professor Andrew McDonald, Enterprise Data Provisioning, Technology Platform Lead.

Dr Shane Montague said: “Lloyds Banking Group’s mission to Help Britain Prosper means leading innovation that genuinely improves how engineering gets done, with a focus on delivering enhanced digital services for our customers.

Each quarter, the partnership will task Lloyds Banking Group’s software and data engineers in Bristol, Manchester and Hyderabad to work with their agentic AI counterparts on a different type of task with the aim to measure the impact on quality and speed of delivery.

As the partnership continues, the Group will develop and improve their understanding of how to harness the benefits of agentic AI. Successful projects will be rolled out across the Group’s wider data teams, and eventually to all software and data engineering teams.

At the same time, Glasgow researchers will work alongside the teams to gather evidence on each project’s impact on efficiency, workflow and the day-to-day work of the teams.

Together, the partners will publish regular research papers documenting their work and develop best-practice documents to help organisations of all scales integrate AI into their software and data product development processes.

Finance and Health Lab National Conference

On 19 March, FinTech Scotland hosted the Finance and Health Lab (FHL) National Conference at the Edinburgh Futures Institute, marking the completion of Phase 1 of this programme. The event brought together leaders from financial services, fintech, academia, government, healthcare, and the third sector to share learning from academia, industry, and from the Lab’s first Innovation Stimulation Open Call and to explore the future of financial wellbeing in an ageing society.

The Finance and Health Lab was established to address a growing reality: as populations age, financial health and physical health become increasingly interconnected. Changes in income, housing, care needs, cognitive capacity, and social circumstances create complex challenges that sit across multiple systems. No single sector can address these alone. FHL was designed to catalyse collaboration, evidence-led innovation, and practical experimentation to improve outcomes for people in later life.

Setting the Context

The conference opened with reflections on the programme’s purpose and progress to date. Discussions on the implications of demographic change highlighted both the scale of the challenge and the opportunity for innovation. An ageing society is not simply a policy issue. It reshapes how financial services must operate, how products are designed, and how support is delivered across the life course.

A research showcase featuring leading academics explored the evolving relationship between health and wealth in later life. The evidence underscores that financial insecurity and poor health often reinforce one another, yet services are rarely designed with this interplay in mind. Bringing rigorous research into direct dialogue with industry practitioners is a core objective of the Lab.

Designing Future-Ready Services

An industry panel examined what it will take to build financial services that remain effective as customers age. Trust, accessibility, and long-term resilience emerged as central themes.

Participants highlighted the need to move beyond reactive support models toward proactive approaches that anticipate vulnerability and support people through major life transitions.

Importantly, the discussion recognised that innovation in this space must balance commercial sustainability with public benefit. Aligning these objectives is challenging but essential if solutions are to scale.

Showcasing Innovation

The afternoon sessions highlighted solutions developed through the Innovation Stimulation Open Call. Participating startups delivered rapid demonstrations of tools and platforms addressing issues such as financial vulnerability, planning for later life, support for carers, and accessible digital services. Follow-up discussions allowed founders to engage directly with industry stakeholders and policymakers.

A session led by Smart Data Foundry demonstrated how responsibly governed data can generate new insights into the links between financial behaviour and broader social determinants of wellbeing. This work illustrates the potential for data to support more targeted interventions while maintaining public trust.

Collaboration in Practice

Throughout the day, one message was clear: progress in this space depends on sustained collaboration. The Lab has created a structured environment for organisations that do not typically work together to share expertise, test ideas, and identify barriers to implementation.

Beyond the formal sessions, the conference enabled valuable informal engagement among senior leaders across sectors. These conversations are critical for building the partnerships required to translate early innovation into real-world impact.

Key Insights from Phase 1

The closing discussion reflected on what the programme has demonstrated so far:

- Financial health in later life is a systemic issue requiring cross-sector solutions

- Evidence, lived experience, and innovation must be integrated from the outset

- Trust, accessibility, and dignity are foundational design principles

- Data can unlock new approaches when used responsibly

- There is strong appetite across industry and public services to continue this work

Phase 1 has shown that structured collaboration can move beyond dialogue to tangible experimentation and learning.

Looking Forward

The National Conference marked an important milestone, but not an endpoint. The insights, partnerships, and prototypes developed through the Finance and Health Lab provide a foundation for future phases of activity.

FinTech Scotland remains committed to working with partners to advance solutions that support healthier, more financially secure lives as people age. The challenges are significant, but so is the opportunity to redesign systems around real human needs.

Phase 1 has demonstrated what is possible when diverse sectors come together with a shared purpose. The next stage will focus on deepening this work and translating innovation into scalable impact.

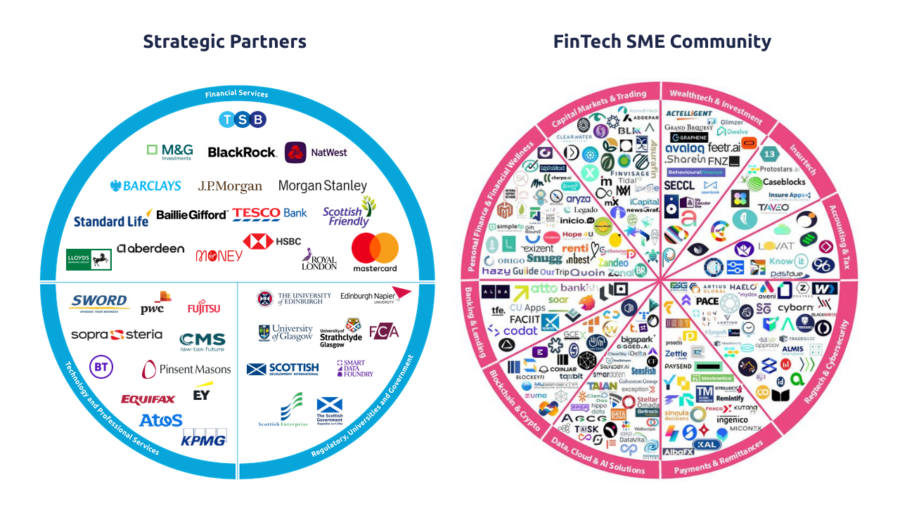

Atos UK&I joins FinTech Scotland as Strategic Partner to accelerate AI‑led fintech innovation and growth

FinTech Scotland today announced that Atos, a global leader of AI-powered digital transformation, has joined the Scottish fintech cluster as a Technology Strategic Partner, strengthening the cluster’s ability to drive collaborative innovation and growth.

Atos brings global scale with a strong UK presence to help create the conditions for faster innovation, secure scaling and economic impact across Scotland’s fintech community. Experts in Agentic AI, digital sovereignty and cybersecurity with a 60,000‑strong team worldwide, Atos provides end‑to‑end digital expertise across consulting, infrastructure, operations and optimisation, as well as integrated services across cloud, application services, smart platforms and the digital workplace.

This partnership strengthens the cluster’s momentum and the shared commitment to collaborative innovation that will shape the future of next-generation financial services. It takes our network to 37 Strategic Partners, building a world-class environment for fintech innovation and regional growth, at a time when Scotland’s fintech cluster has more than doubled in five years, from just over 120 firms in 2020 to more than 260 today, reinforcing its position as one of Europe’s most dynamic and collaborative fintech clusters.

Aleks Tomczyk, Chief Executive at FinTech Scotland, said: “This partnership with Atos strengthens our shared commitment to fostering innovation, collaboration and growth across Scotland’s fintech cluster. By bringing deep expertise in AI, data, secure cloud and digital platforms, alongside a strong global presence, Atos will enhance the support available to fintechs as they develop new solutions and build resilience, contributing to Scotland’s economic and societal progress.”

Simon Chandler, Head of Financial Services and Insurance, UK & Ireland at Atos said: “Atos is delighted to join FinTech Scotland to cement our investment in Financial Services in Scotland. We are excited to work in collaboration with the; FinTech SME community, Financial Services organisations, regulators, universities, and government by leveraging our leading Sovereign Agentic AI, Data, cloud and digital global expertise, underpinned by our unique Sustainability and Social Value commitments. We aim to drive Shared Value success for every part of this community to the betterment of this community and Scotland as a whole.”

The Tipton selects docStribute® to modernise member communications

docStribute® and the Tipton & Coseley Building Society partner to improve the firm’s communications and strengthen member engagement

docStribute®, a UK RegTech company specialising in regulated customer communications, today announces a strategic partnership with the Tipton & Coseley Building Society.

The partnership reflects the Tipton’s continued focus on personalised service, deepening member engagement and meeting the requirements of the Financial Conduct Authority’s (FCA) Consumer Duty.

A key priority for the Tipton is accelerating digital transformation, with the partnership forming part of a multi-year change programme to expand online services, enhance systems and create better retail and working environments.

Through the docStribute® platform, the Society wants to move towards an electronic-first approach for both regulated and general communications. It aims to reduce delivery costs, process important documents more quickly, and use less paper, thereby lowering the associated carbon emissions.

Beyond cost, efficiency and environmental gains, the partnership will help the Tipton in repositioning its regulated documents, so they are not just a compliance requirement, but an opportunity to engage with members.

By presenting information in a clearer, more accessible digital format for those who want it, the Tipton can build greater awareness and understanding within its membership. This in turn supports well informed financial decisions, in line with Consumer Duty expectations.

docStribute® enables the delivery of timely, relevant communications which are easier to access, read, and navigate. The result is improved engagement and measurable insight into how members interact with information, allowing the Tipton to continuously improve clarity and outcomes.

Central to this approach is docStribute’s AIDA, the Artificial Intelligent Document Assistant. Developed through docStribute’s participation in FinTech Scotland’s Financial Regulation Innovation Lab (FRIL), it enables recipients to interact with regulated documents in a conversational way, helping them navigate complex information, ask questions, and receive clear explanations in real time.

The platform can also incorporate supportive formats such as short video and enhanced visual layers to aid accessibility and comprehension. Together, these tools support financial literacy and stronger understanding, while ensuring communications remain compliant and appropriately governed.

The platform uses Distributed Ledger Technology to protect the integrity of customer documents and create a verifiable record of what information was sent and when. This ensures communications remain secure, accessible, and compliant with the FCA’s Durable Medium requirements, while providing the sender with greater visibility of engagement and understanding.

Chris Ansara, CEO of docStribute®, said:

“We are pleased to be working with The Tipton & Coseley Building Society. Building societies have always been rooted in trust and community. Our role is to help turn regulated communications into moments that strengthen that trust by making important information clearer and easier to engage with.

“With AIDA, and enhanced formats such as video, we are adding another layer that actively supports member understanding, not just delivery. This partnership brings our total building society partners to four and highlights the sector’s continued emphasis on improving customer understanding through stronger engagement.”

Richard Groom, Chief Customer Officer at the Tipton, added:

“We are focused on increasing the proportion of compliant digital communications we send as this brings multiple benefits to our business and members alike. Adopting an electronic-first approach, in line with members’ preferences, is another step towards modernising our Society and will improve the overall standard of service we offer.”