Forging the Future of Financial Services: TSB Spotlight Innovation in Open Banking

Three fintech innovators, Sikoia, Credit Canary and Aperidata, have been named winners of the 2024 TSB Innovation Labs programme, a partnership between TSB and FinTech Scotland. This is a collaborative effort to shape the future of financial services through responsible use of data and technology.

Now in its fourth year, the Innovation Labs programme offers early-stage fintech firms a platform to explore real-world applications of their technology. With access to expert mentorship at TSB’s Technology Hub in Edinburgh, the cohort has worked over the last year to develop propositions that aim to improve customer experiences across banking.

The focus of this year’s winners is very much Open Banking technology to simplifies and accelerates customer support.

Sikoia is working to streamline finance applications, potentially reducing barriers for new customers. Meanwhile, Credit Canary and Aperidata are exploring solutions to improve credit scoring and accelerate lending decisions. All three firms will now develop proof of concepts in partnership with TSB, testing how their solutions might translate into practical improvements for customers.

The TSB Labs programme has previously seen success with fintechs such as Lightning Reach, which helps users access benefits and financial support through a single portal. Since its implementation, TSB customers have accessed over £160,000 (£500 per customer) in grants. Another alumnus, ApTap, has supported customers in saving more than £65,000 (£150 per customer) on broadband bills by helping them switch to better deals.

Speaking on the latest announcement, Nicola Anderson, CEO at FinTech Scotland, said:

“We are delighted to witness the success of Sikoia, Credit Canary and Aperidata through the TSB Labs programme. These innovative fintech companies show how data and AI can be harnessed to deliver real impact for people and communities. At FinTech Scotland, we believe meaningful collaborations are the key to unlocking innovation and this partnership with TSB demonstrates the powerful outcomes that can be achieved when new innovative firms and progressive established companies work together to shape the future of financial services.”

Adam Betteridge, FinTech & Open Banking Lead at TSB said:

“We are incredibly proud of the progress made by these three innovative fintechs during the TSB Labs programme. Over the last 12 months, Sikoia, Credit Canary and Aperidata have demonstrated exceptional potential to help TSB customers get support more quickly. Their innovative solutions use data and technology in new creative ways to help provide an even better experience for TSB customers. We’re looking forward to what comes next.”

The programme reflects wider themes highlighted in the FinTech Research & Innovation Roadmap 2022–2031, developed by FinTech Scotland. Central to that vision is the role of Open Finance and collaborative innovation in addressing societal, economic and environmental needs. The roadmap points to a future where fintech drives financial inclusion, better consumer outcomes and a more sustainable economy.

Sword Group Expands Cybersecurity and AI Capabilities with Acquisition of Edinburgh-based iDelta

Sword Group, a FinTech Scotland’s strategic partners, has announced its acquisition of Edinburgh-based fintech iDelta Ltd, a specialist firm focused on customised data solutions, cybersecurity monitoring, AI automation, and fraud analytics.

Founded in Scotland’s thriving tech ecosystem, iDelta has developed a strong reputation for its bespoke solutions in infrastructure and application monitoring, particularly within financial services. Its specialist consultants have created innovative tools for managing Open Banking data APIs and have developed extensions available on the popular Splunk marketplace. These solutions streamline the integration process with third-party technologies, enabling customers to effectively harness their data assets.

Kevin Moreton, CEO of Sword UK, described the move as a strategic step towards enhancing Sword’s capabilities in cybersecurity and artificial intelligence, particularly within the financial services sector.

“We’re pleased to welcome iDelta into Sword Group. This acquisition is well-aligned with our strategic vision for 2028 and significantly strengthens our cybersecurity strategy. Combining our expertise will enable us to deliver even greater value to our customers,” Moreton said.

Stuart Robertson from iDelta also welcomed the acquisition, noting the shared commitment between both companies towards innovation and technical excellence.

“Joining Sword opens exciting new opportunities for growth and collaboration. Our strong partnerships with Splunk and Cisco, combined with Sword’s extensive resources, mean we’re perfectly positioned to expand our offerings and accelerate our capabilities,” Robertson said.

Sword Group, known for providing business technology solutions across energy, public, commercial, and financial sectors, currently employs over 600 staff across its UK locations, including Aberdeen, Glasgow, Teesside, and London.

The acquisition underlines Sword Group’s strategic approach to bolstering its technical expertise in critical domains like cybersecurity and AI, reflecting broader industry trends towards greater digital resilience and smarter data utilisation.

Open Finance and Carbon Neutral Banking

Recent industry insights show that banks still face significant constraints in measuring indirect Green House Gas (GHG) emissions owing to data limitations and a lack of harmonised methodologies.

At the same time, banks and other financial institutions hold large volumes of consumer data that can be leveraged to estimate GHG emissions albeit financial transaction data are privately owned with restricted access. This paper discusses how an open finance framework can be used to aggregate consumer transaction data across multiple financial products to compute carbon footprints.

It highlights a step-by-step approach to carbon footprint estimation and discusses the consideration for using microdata for emission computation.

Open Finance – What’s next?

Season 4, episode 10

Listen to the full episode here.

Open Finance is set to unlock a new level of transparency, accessibility, and control for consumers, businesses, and financial institutions. But what does this mean for the future of the financial ecosystem, and how will key players navigate the opportunities and challenges that come with it? We discuss what Open Finance really means, the progress made so far, and what the future holds for consumers, fintechs, and traditional banks alike.

Guests:

Ezechi Britton – CEO at the Centre for Finance, Innovation and Technology (CFIT)

Jen Lothian – Founder at MyArk

Space-Comm Expo Scotland 2024: How Can Fintech and SpaceTech Come Together?

The inaugural Space-Comm Expo Scotland will be the largest space industry event ever held in Scotland and will take place at the SEC Glasgow from September 11-12, 2024. Hosted by Will Whitehorn, the former President of Virgin Galactic and current Chancellor of Edinburgh Napier University, this event promises a fantastic lineup of keynote speakers from various sectors, including government, aerospace, defence, and academia. Among the speakers, Nicola Anderson, CEO of FinTech Scotland, will offer her reflection on the growing intersection between space technology and financial technology.

A Showcase of Scotland’s Space Industry Prowess

Space-Comm Expo Scotland is set to shine a spotlight on the nation’s dynamic space sector, which has become one of the fastest-growing in Europe. With over 150 space companies and 80 aerospace companies, Scotland supports nearly one-fifth of all UK space sector jobs and builds more small satellites than anywhere else in the world, second only to California. The event will feature more than 100 exhibitors and is expected to attract over 3,000 attendees, including representatives from government, industry clusters, academia, and commercial enterprises.

Keynote Speakers and Industry Leaders

The Expo’s impressive roster of speakers includes notable figures such as Dr. Paul Bate, CEO of the UK Space Agency; David Parker, Space Exploration Director at the European Space Agency; and Professor Malcolm Macdonald, Chair of Applied Space Technology at the University of Strathclyde. The opening address will be delivered by the Lord Provost of Glasgow City Council, Jacqueline McLaren.

Nicola Anderson’s presence is particularly noteworthy for the fintech cluster. As CEO of FinTech Scotland, Anderson has been driving innovation and collaboration within Scotland’s financial technology sector. Her participation shows the critical role fintech plays in supporting and enhancing space technology ventures. A previous initiative between FinTech Scotland and Space Scotland highlighted how data from satellites can be used to enhance propositions in the financial sector such as supply chain management, measuring carbon impact of various assets or better handling of insurance claim management to name a few.

Exploring the New Commercial Space Age

The speaker programme at Space-Comm Expo Scotland will cover a wide range of topics, including spaceports, launch capabilities, satellite manufacturing, downstream data, AI, cyber security, space law, investment, skills development, and space sustainability. These discussions come at a pivotal time in the commercial space age, highlighting both the opportunities and challenges the industry faces.

Anticipated Outcomes and Collaborations

Kevin Scullion, International Trade Specialist at Scottish Enterprise, expressed high hopes for the event, anticipating further collaboration between Scottish, UK, and international partners. The Expo is expected to foster discussions on trade opportunities and strengthen ties within the global space community.

Supported by key organisations such as the UK Space Agency, Scottish Enterprise, and FinTech Scotland, the Space-Comm Expo Scotland will be an unmissable event for anyone involved or interested in the space industry. With a world-class programme of content, product demonstrations, panel sessions, and 1-2-1 networking opportunities, it offers a comprehensive platform for knowledge exchange and business development.

Space-Comm Expo Scotland will be held from September 11-12, 2024, at the SEC in Glasgow. Registration is free, and those interested in attending can sign up at space-comm-scotland.co.uk. For information on exhibiting, email spacecomm@hubexhibitions.co.uk.

Transforming wealth management: Trends from the Banking Transformation Summit

Advances in cloud computing, data analytics, and artificial intelligence (AI) are driving significant transformation in wealth management; reshaping how firms manage and serve their clients. Such is the scale and potential of these advances; wealth management firms face an abundance of both challenges and opportunities.

This blog explores some of the most pressing challenges firms must face and how they can overcome them to leverage this technological innovation effectively. It’s a journey that promises to enhance customer experience, operational efficiency, and competitive advantage, offering a bright future for wealth management.

Balancing existing clients and new client bases

Wealth management firms face the challenge of catering to existing clients who prefer a more traditional approach and a new breed of younger, digitally savvy clients.

Whereas more established clients value a human-facing service, younger generations expect and indeed favour seamless digital interactions. To effectively engage this younger demographic, firms must be able to complement professional validation with diverse communication channels beyond email.

Firms must remove barriers to attract and retain these clients by creating accessible, digital-first experiences, offering incentives, and increasing marketing budgets to encourage interest.

Personalisation and mass customisation

Rather than simply a feature, personalisation is the essence of effective wealth management. Whether delivered on a per-client basis or by using a more segmented approach, it fulfils the essential role of making each client feel uniquely important.

Next-generation AI enables this mass customisation, allowing firms to provide tailored advice at scale and reinforcing the value of each client’s individuality. For example, wealth managers can offer timely, relevant advice to enhance client engagement and satisfaction by leveraging data from various life events and triggers. However, handling customer data sensitively and tailoring services explicitly for client benefit is critical to the success of this approach.

New digital products and AI integration

Investment platforms and open banking tools, like Moneyhub and Moneyinfo, simplify financial management by allowing clients to aggregate data in one place. Meanwhile, AI provides opportunities to enhance these platforms by automating manual tasks, such as capturing meeting notes and client conversations and ensuring regulatory compliance.

AI’s role in wealth management goes beyond improving efficiency and accuracy – it also plays a crucial role in protecting clients. For example, AI can flag if a client appears to misunderstand a piece of advice that would not be picked up from word transcripts alone, ensuring that clients are well-informed and protected.

Speed, accessibility, and presentation

Today’s clients expect quick, online access to their financial information, slick data presentation, and the option to speak to a professional when needed. Speed and accessibility across hybrid channels are paramount.

Wealth managers must invest in intuitive, visually appealing interfaces that make complex information easy to understand. Customer expectations on the ability to interact with services seamlessly are now generalised across financial services, set by advances such as Open Banking. They require robust authentication and providing immediate access to professional advice when necessary.

Regulatory demands and data quality

An increasingly demanding regulatory ecosystem requires wealth managers to enhance their data completeness, quality, and accuracy. The FCA’s 2023 Dear CEO’ letter stressed the importance of tackling financial crime and putting customer needs first by meeting high standards underpinned with strong data governance.

If wealth management firms are to meet these standards and lay the foundation for compliant product innovation, investment in technology is needed. For example, AI systems can assist in identifying regulatory triggers, such as testing customer understanding and vulnerabilities to ensure compliance. Nonetheless, firms must remember their duty to the customer and ensure AI ethical policies are established from the outset.

Customer journey and operational efficiency

Building customer journey-based services while delivering operational efficiencies to provide a holistic client experience involves a coordinated approach across financial services and insurance. This approach is crucial for ensuring client retention and satisfaction. Data analytics can then optimise internal services, such as risk and compliance, further reducing costs and improving service delivery.

Firms need to start with a well-defined customer journey and build out services across all relevant areas. Taking this approach helps remove barriers to entry for the younger demographic, to prepare for the ‘great wealth transfer’ where trillions are anticipated to be handed down to future generations in the coming years.

In Summary

Integrating cloud, data, and AI is revolutionising the wealth management industry. Firms embracing these technologies can enhance personalisation, improve operational efficiency, meet regulatory demands, and engage and protect a new generation of clients. Those who delay moves towards modernisation risk losing out to the competition.

Article written by Orla Parry, Head of Private Sector Business Development at BJSS

BJSS is a leading partner to the financial services industry. Over the past 30 years, we’ve helped multiple wealth and asset managers to innovate at scale.

Talk to us about your transformation goals and find out how we can help you leverage cutting-edge technology and stay ahead in a wealth management industry undergoing unprecedented evolution.

This is not a sponsored article and no commercial agreement exists between BJSS and FinTech Scotland.

EY Launches First Scottish Fintech Lab with Space Agency Partnership

EY has launched its first Scottish fintech lab in Edinburgh. The innovative space is designed to foster collaboration, experimentation, and rapid prototyping among start-up and scale-up companies in the fintech sector.

Purpose and Vision

The Edinburgh fintech lab brings together fintechs, investors, clients, regulators, and other partners, the lab will facilitate the development of real-world solutions that enhance market and customer service. The focus will be on creating innovative solutions to key financial challenges, particularly in sustainable finance.

First Cohort and Space Collaboration

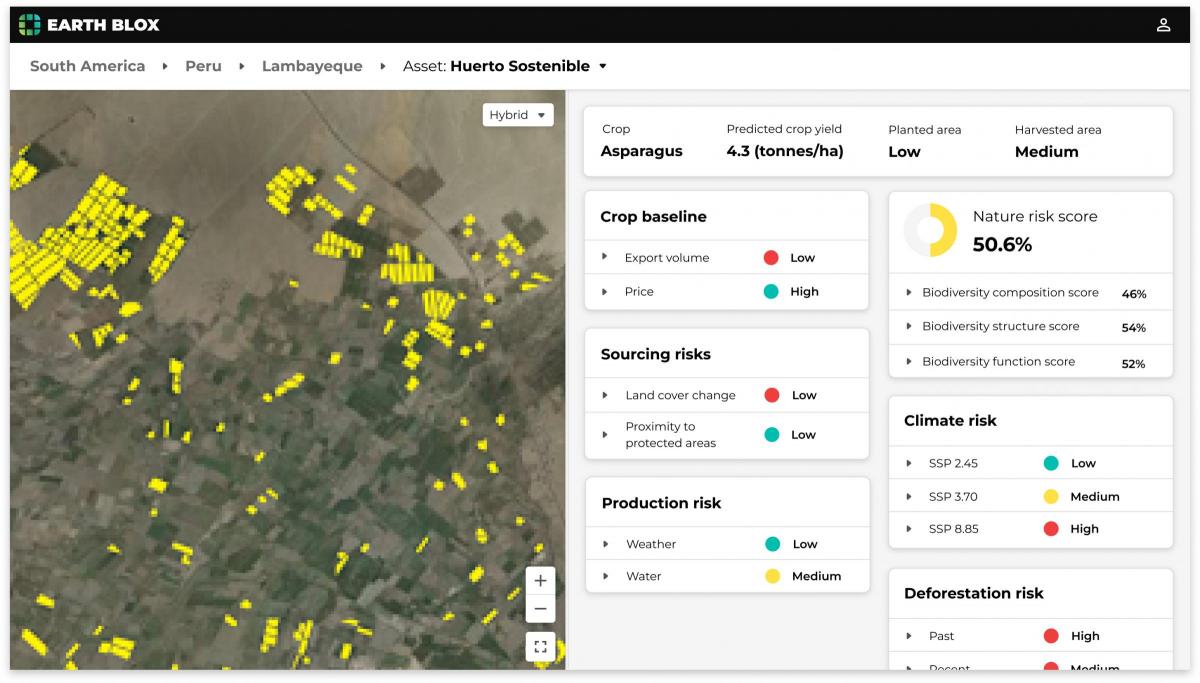

The lab’s first cohort explored the intersection of space science data and finance. In partnership with FinTech Scotland, Space Scotland, and supported by the UK Space Agency (UKSA), the program aims to deepen the understanding between financial services and the space industry. A notable project by Environment Systems and Earth Blox utilised spatial data to optimise agricultural commodity production while ensuring compliance with environmental regulations.

Leadership Insights

Sue Dawe, EY Scotland’s financial services managing partner, highlighted the importance of sustainable finance and the lab’s role in fostering innovation within Scotland’s fintech sector. Nicola Anderson, CEO of FinTech Scotland, and Hina Khan, Executive Director of Space Scotland, emphasised the collaborative efforts to drive positive economic and social change.

For more information, visit EY Fintech Lab.

Scotland Fintech Festival – Episode 4 – Smart Data Foundry

Season 3, episode 13

Listen to the full episode here.

During this special episode of Fintech Scotland’s Podcast we recorded live from the Fintech Summit, the opening event of Scotland Fintech Festival that took place between the 21st of September and the 12th of October 2023.

In this episode we spoke to Bryn Coulthard, Chief Product and Technology officer at Smart Data Foundry.

We discussed the role of data as an enabler for collaboration between fintech firms and established financial firms. More specifically we looked at synthetic data to innovate in a safe and efficient way.

Unlocking Financial Innovation with Digital identities and Open Finance

Open banking data is hugely valuable as it allows us to address the lack of trust that innately exists in a digital-first financial services engagement. In actuality, it is our bank accounts that best reflect us as physical people, spending money every day and creating a footprint of data. By using open banking data we can leverage the identity and data we already have with our banks, so that third parties (like lenders) can understand us just as well as our bank understands us.

James Varga, Founder of DirectID, is passionate about Open Banking and the opportunities it provides to redefine the credit and risk industry. In 2011 he founded DirectID with a mission to leverage the identity and data that users have with their bank accounts, helping them prove their identity, financial health, and credit risk in seconds.

“One of my core fundamental beliefs is this idea that we should be able to manage our own individual data,” says Varga. “In the very near future, I think we’re going to start to hit that challenge around the sharing of identities and related standards, which will push us towards a consumer-centric data sharing model, where consumers are empowered to manage their varying sources of data and share them with third parties. But we’re not quite ready for it yet.“

Over the past few years, he notes that the industry has started to view digital identities as an enabler and opportunity, largely because we need to rely on a trusted exchange of information to make decisions. In a centralised view of the consumer-centric data sharing model, identities are treated as a utility with control over identifiers as a result. However, it is extremely difficult to maintain control within this centralised system due to the sheer scale of data relationships that exist. The decentralised model, meanwhile, places the consumer at the middle. This model recognises that value is found, not from controlling the identifiers, but from within the data and services related to that data. There are examples of decentralised models that we can draw on, for example, the domain name network and mobile phone numbers. Such a decentralised model won’t come without challenges: a framework and methodology still need to be ironed out, but prior to this Varga believes that the first big industry challenge is to realise that we shouldn’t own people’s identity and give up ownership over that.

As we move into a world where consumers have an increasing amount of access and control in managing their data, we move from open banking to open finance, which can incorporate all sorts of data occurring over a person’s lifespan. Once the decentralised framework of identity sharing is agreed on, issues around security, compliance and tech standards can then also be agreed upon. “This isn’t a technical problem,” says Varga. “What we want is for people to use multiple identities, and give that control back to the individual to help them to understand who sees your data, who is accessing it, and who is sharing it. And even, ideally, here is the money that you can make from enabling or the benefit that you can get from enabling.”

The Evolution from Open Banking to Open Finance

Bryn Coulthard is the Chief Product and Technology Officer at Smart Data Foundry, coming originally from a background in banking technology and product. The goal of the Smart Data Foundry is to safely unlock the power of financial data to provide huge benefits to society and inspire innovation by delivering economic, social and environmental benefits for everyone.​

As the UK’s journey progresses from Open Banking to Open Finance, Coulthard stands by the need for the development and evolution of standards. Whilst the UK mandated that providers deliver against API standards, Europe’s PSD2 approach decreed that banks needed to provide APIs but did not prescribe what these should look like. Today, as a result, we can see the level of adoption of Open Banking in the UK is much higher as opposed to Europe, due to the EU’s large array of differing standards. Such a myriad of standards means both fintechs and aggregators have to now build and develop complicated solutions to handle these multiple APIs.

With ever-increasing complexity in the global Open Finance standards landscape, Smart Data Foundry maintains a Standards Library to help financial institutions and innovators quickly and easily assess technical standards adopted by a geography or financial system. “We look at Open Banking and Open Finance standards across the globe, and we maintain and update those standards as they evolve,” explains Coulthard.

Coulthard is firmly of the view that standards need to be enhanced to be much more prescriptive about how APIs perform in terms of performance and availability. While in the past the UK was certainly a leader in this space, we’re now starting to see other countries learning from and building upon what’s been achieved in the UK. For example, Australia is more advanced in driving wider value through their core Consumer Data Right standards, Brazil has begun to really embrace Open Finance, and some Middle Eastern countries are beginning to push some quite strong Open Banking standards. “What we’re seeing internationally is that people have gone beyond the UK’s position and are now looking at ways to build on what we did and bring things to the next level. We need to learn from that as well,” he emphasises.

Coulthard strongly believes that Open Finance provides an opportunity to help people through their journey by demystifying finance so that people will make better informed decisions. It can help people retire, build new debt management, provide SMEs with better access to finance, or gig economy workers with savings or pensions programmes. “Open Banking has been around for the past six years, and it has been a real success. I just think it took time to get going,” he says. He warns against people getting too excited, however, about Open Banking or Open Finance as they are simply a means to an end. People should actually get excited about the value that increases the type of propositions and offerings.”