Global open banking and open finance directory launched

“When I’m talking with people in the open finance community, the most common question I’m asked is whether I can recommend a company offering a certain service in a particular region. This directory is our answer to that need, helping companies connect and building awareness of what they have to offer.”

“When I heard about the new directory, I was very keen to be involved, and we’re delighted to be on the list for the launch. Open banking has come a fantastic distance in the last two years and this will be of huge benefit to anyone seeking to understand the players in the open banking and open finance world,”

“We want to encourage everyone in the sector to share their information and to make use of this free resource. As the directory evolves, we’ll be able to map the ecosystem, add more advanced search functionality and highlight some of the great case studies that are emerging,”

“With the open banking industry now fully emerging worldwide, it is invaluable to have all of the global entities together in a resource such as the Open Future World Directory. This platform will be extremely useful to experts, partners, investors alike and will provide a forward thinking space in which to share ideas and stay up to date.”

It’s worse than that”¦ Jim

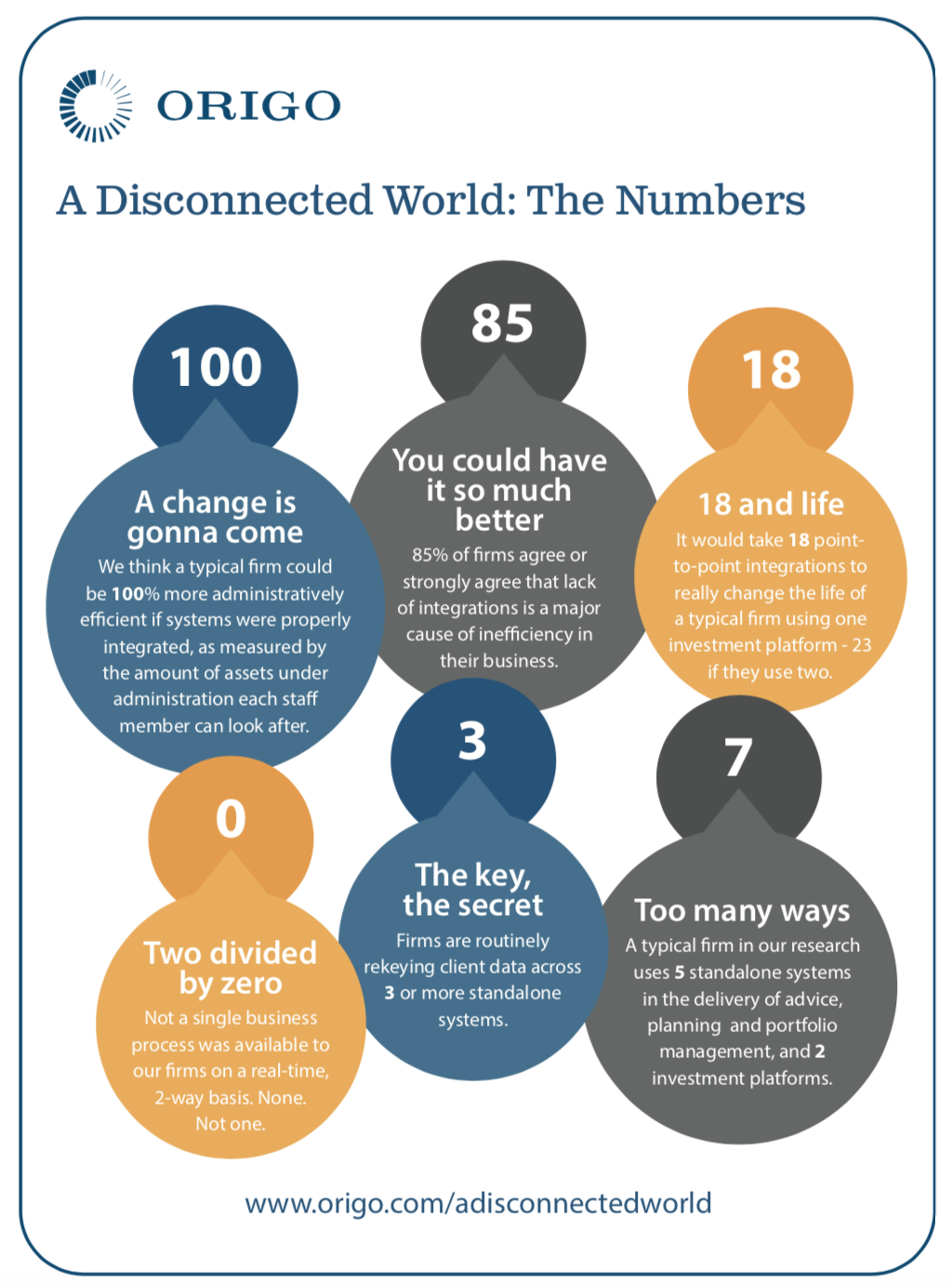

Anthony Rafferty, Managing Director, Origo says recent research into integration between systems in financial adviser firms’ back-office systems reveals a worrying disconnect eating into time, resource and profits of businesses

Origo recently commissioned in-depth research into the integration between systems in the back-offices of financial advice firms, and how this affected the efficiencies and profitability of those firms.

The research was carried out independently by the lang cat, a specialist financial services consultancy based in Edinburgh, and combined hours spent in financial advice firms around the UK mapping processes and analysing how they use the systems they have in place, as well as conducting online research with another 116 financial advice firms.

The conclusion is best summed up by Mark Polson, the MD of the lang cat, who was heavily involved in the research. He says: “We knew things weren’t great before we set out to conduct this research. But even so, we were struck by the impact of these inefficiencies on adviser back offices. Even where integrations do exist, firms aren’t trusting them or using them ”“ with good reason in some cases.”

From closely studying firms’ processes, the research estimates that in a typical financial advice business, staff could be up to 100% more efficient, dealing with twice the assets under administration they currently manage, if the systems they used were properly integrated with one another. In other words, staff could potentially be dealing with up to twice the number of fee paying clients than they are at the moment.

That is both a shocking state of affairs and also one of opportunity ”“ not least for financial advice firms.

To explain what we found: Firms involved in the study on average used five standalone systems in the process of giving advice, building investment and savings portfolios and managing clients; seven when platforms (transaction and administration services) were added; 10 with the addition of more general systems like accounting and office software.

It showed that due to a lack of integration between systems, and trust in those systems, firms are having to plough time and money into otherwise unnecessary manual input and reconciliation. In a typical new business journey, for example, client details were being keyed into systems at least three times!

Key facts from the research can be found on the accompanying infographic.

Currently ”“ and to be fair, despite sterling work by some of the players in the market ”“ advice firms do not benefit from a level of integration that is of real use to them. Integrations are typically point-to-point, with one provider integrating with another for specific purposes, for example for portfolio valuations.

They are also driven by business case, with platforms, CRMs and other system providers naturally prioritising integrations that will bring in higher levels of returns.

On a practical level and worryingly, even where integrations exist, adviser firms said that the lack of consistent and quality data meant they distrusted the output the systems are delivering, the result of which was that they had reverted to inefficient, costly and potentially risk inducing manual processes, because it was a process over which they have more control.

Typically there are 23 point-to-point integrations required within a firm using two investment and savings platforms, without factoring in any systems for protection and mortgage services and general office systems. On a point-to-point basis, that level of integration is never going to happen.

But there is a solution. We identified that if there was a centralised hub, into which platforms, CRMs and adviser software systems and tools could integrate once and then connect to every other player in the market who was also connected to the hub, and which also dealt with making and maintaining the connections, the benefit to the industry could be huge ”“ in particular to the financial adviser firms.

Using a centralised hub would mean any provider new or established could connect with any other provider on the hub, for services pertinent to their operations, no matter the volume of business.

In this way, a centralised integration capability would significantly improve the market’s connectivity, helping advice firms to improve their efficiencies, their profitability and enabling them to deliver faster and better service to their clients, whilst potentially boosting business across the board.

Hence, for the past couple of years we have been building the Origo Integration Hub to help provide that solution.

From a business perspective, for systems and services providers, this hub-and-spoke approach to integration does away with the need for case-by-case decisions and resource restraints incumbent of the point-to-point integration method. Linking to a hub incurs one set of integration costs instead of many, and significantly reduces resource and IT costs, which platforms and system suppliers can better apply elsewhere in their business.

Importantly, it provides the opportunity for all software and service companies, including smaller companies and new entrants, to easily connect with new trading partners if they wish. Also, it enables adviser firms to use the software or service that best suits their business set-up.

Currently, the Integration Hub has 19 companies including some of the big names in investment and savings signed to it, with others in the pipeline.

From a top down perspective it seems illogical that in the 21st century systems do not talk to one another in an efficient manner. However, this is a legacy issue which Origo with its remit to help improve the efficiencies and cost effectiveness of the industry and deliver better outcomes for consumers, is in a position to help resolve.

Read more about Origo here

Scotland’s fintechs can unlock the power of open banking

There are over one hundred fintech companies thriving in Scotland’s fintech community with a range of new start-ups, existing firms developing their fintech offers and tech-driven firms re-locating north of the border. The launch of open banking last year has played a key role in fuelling the growth of this sector and the UK as a whole is now recognised as a world leader in open banking innovation.

So far, much progress in open banking has been made in the small business environment where innovative products and services are already in the marketplace such as tools for monitoring cash flow and accessing finance. An important contribution to this innovation was the first Open Up Challenge in 2017 and 2018 ”“ spearheaded by the Competition and Markets Authority (CMA) and run independently by Nesta Challenges. The Challenge was part of the CMA’s package of measures introduced to stimulate competition in the financial sector and help small businesses save time and money, find better services, reduce stress and discover the intelligence in their financial data. Winners included fast-growing fintech brands such as Swoop, Funding Options and Coconut whose products are frequently used by freelancers and small businesses across Scotland. However, as important as it is, the small business space is just the start of the open banking revolution.

When we consider the consumer market, while there are products that are already in use it’s fair to say that take-up has not yet been widespread – especially in light of research showing UK consumers stand to gain £12bn a year from open banking-enabled services[i]. Awareness of open banking is still low, with new research from Nesta Challenges showing that 55% of people in Scotland have not heard of it.

On the other hand, 46% of Scottish people say that they want to feel more in control of their finances and 33% want personalised information and guidance to help them manage their finances. For people in Scotland the two biggest benefits of using an open banking enabled product are seen to be: saving money and finding better deals. These findings present big opportunities for those fintech companies and start-ups in Scotland developing open banking-enabled innovations for consumers.

That’s why Nesta Challenges, in partnership with Open Banking Ltd, has launched the Open Up Challenge 2020 – a £1.5m prize fund to encourage fintech innovators to create solutions that will help people to make more of their money.

With Open Up 2020 we want to attract breakthrough innovations designed to support hundreds of thousands of people ”“ particularly the most vulnerable. We’re looking for fintech innovators that can unlock open banking’s potential to change the way that the UK manages its money ”“ especially for the 15.2 million who regularly run out of money each month.

Open banking represents a genuinely new way of empowering people with their data ”“ it is a key milestone on the journey to a digital economy, and the Open Up Challenge has an important part to play in encouraging people to make their data work for them. Open Up 2020 will not only help people better manage their money and take control of their data, but it will also support Scotland’s growing and thriving fintech sector by fast-tracking innovative new products and services. Applications for Open Up 2020 are open until October 2nd2019 and guidance on how to apply can be found at https://openup.challenges.org/apply/. In addition, the Open Up 2020 team will be holding office hours at Codebase, Edinburgh on Thursday 12thSeptember ”“ book your slot hereto benefit from tailored application support from the Open Up Entrepreneur-in-Residence Sarah Tierney.

[i]Consumer Priorities for Open Banking 2019

Income Verification: The Next Stage in Open Banking

As I’ve iterated more times than I can remember over the last two years, the implementation of Open Banking has changed the face of finance for ever.

To my eye, most financial institutions have now reached base camp’ with Open Banking, that is to say, the development of account aggregation within mobile apps. This is nice, and I’m sure consumers are enjoying having access to all their accounts in one place.

The next stage will be for banks and financial institutions to begin deriving value from its use. Within the next year I fully expect to see new services being launched by banks and FinTech’s that will allow financial institutions as well as consumers to reap the rewards from Open Banking.

To that end, we here at The ID Co. have been working with banks and lenders over the last year to bring a new proposition to market.

The ID Co.’s Income Verification solution offers banks and lenders the opportunity to capitalise on the Open Banking opportunity.

We work with numerous banks and lenders. On top of that we’ve spoken to many more over the course of the last year, both in the UK and Europe, and across the globe.

As such, I have a fairly good idea in my head of some of the challenges that are witnessed in the banking sector. One of the biggest that we’ve witnessed is the need to cut operating costs in order to stay competitive.

It’s no secret that the sector is far more crowded than it was just 10 years ago. And some of the Challenger banks now boast healthy customer acquisition, impressive UX across their apps and the web, and innovative new services.

Banks and lenders therefore have the dual pressures of bringing to market new services that will make their core offerings stickier’, while also attempting to streamline back office solutions.

It’s for this reason that I’d suggest exploring an income verification solution.

Verifying income is vitally important for banks and lenders, ensuring they have an accurate view of applicant’s financial income prior to awarding credit in order to ensure they are lending responsibly and offsetting any future risk of bad debt.

Operational Costs

Having an applicant’s income calculated within seconds of them making an application for a loan or credit totally negates the need for paper-based bank statements. The savings in time and resource here are enormous. It could take a few weeks for an applicant to submit their bank statements. And in that time, there’s plenty of opportunity for them to decide not to proceed, or to find an alternative.

We’re sympathetic to the hurdles that banks and lenders need to jump through in order to grant a loan. As well as AML and KYC checks, there are new rules on affordability to consider. For these reasons and more, it is vital that a sound lending decision is made, and not only that, be able to demonstrate why it was a sound decision.

Income verification allows you to do just that. With a solution such as ours, banks and lenders can know an applicant’s income exactly and can then calculate their monthly disposable income accordingly.

Thin Credit Files

Many of us will have friends and colleagues who are not British by birth. It feels a long time since I made the long journey from Canada to Scotland, but it is one that I remember well.

With individuals moving homes and countries with such frequency why is it that when beginning life in a new country, you also start with a blank credit file? Those with a thin credit file, perhaps because they’ve just moved into the country, can now illustrate their earnings and therefore capacity for credit through income verification.

Credit Risk

It’s a difficult challenge because most people aren’t paid monthly, or consistently. With the gig economy, students, retired, and others, those that get paid monthly are in the minority. To make a decision around credit risk, Underwriters or others need some context on which to base a lending decision. We need to understand what kind of income applicant have ”“ frequency, recency and more are all critical factors.

And this works both ways. While those with thin credit files can demonstrate why they might be right for a loan, it also gives the creditor more protection as they can protect themselves from applicants unable to practically make repayments or those that pose a bad credit risk.

Fraudulent Applications

When we were conducting research into loan applications and how Open Banking could support banks and lenders, I was struck by the volume of fraudulent activity that financial institutions needed to filter out in order to service genuine applications. Open Banking removes any opportunity for fraud as through APIs, direct access is made with an applicant’s bank account. Our Income Verification solution then looks back over many months to calculate income, not just the last one or two.

Conclusion

Income verification is the first of the services that will allow banks and lenders to derive value from Open Banking. The savings in time, cost and resource through its use are enormous and as its such reception from those who have trialled it use has been universally positive.

Reducing fraud, servicing customers with a thin credit file, widening prospect pools of potential customers, and illustrating good governance are all vitally important to lenders in 2019. We think that the introduction of our Income Verification solution will give financial institutions the answers to these questions.

Pensions Dashboards ”“ a positive step forward for the nation’s financial wellbeing

By Anthony Rafferty, MD of Edinburgh-based Fintech, Origo

Improving the overall wellbeing of citizens is becoming and ever more important focus of government, an important element of which is financial wellbeing ”“ the vision being a society where people make the most of their money and pensions through being more financially aware and equipped.

Technology has an important part to play in this, notably in respect of the implementation of the Pensions Dashboards. Primarily, dashboards are about enabling individuals to find and view all their pensions in one place, thereby increasing engagement with their long term savings and retirement planning.

Last week the DWP published its Pensions Dashboards paper, which is the Government’s response to the consultation that ended in December 2018. It sets out the practical steps necessary to implement Dashboards, starting with the establishment of an industry delivery group by the end of the summer under the new Money and Pensions Service (MPAS).

Some initial commentator reaction to the paper suggested the project wasn’t being moved on fast enough, but the paper is what we expected at this stage in the project and we see it as a positive step forward. In the paper, government clearly stated its intention to introduce Dashboards as quickly as possible’.

The four key elements necessary to make the Pensions Dashboards a reality are governance, compulsion to provide data, state pension and digital architecture. Next steps for all of these elements have been addressed in the paper, which we see as good news.

What’s more, through the consultation, government was able to test its proposals with the industry, consumer groups and other interested parties. Some 125 organisations gave feedback and the paper says the vast majority’ of them agreed with the suggested approach.

This approach includes establishing a single Pension Finder Service ”“ the core architecture that orchestrates an individual’s search for their pension data across all pensions companies and which displays their data on the dashboard they have chosen to use.

Origo has taken a leading role in the project from the start, quickly demonstrating how the technology could meet the government’s policy intent and objectives. We have built and scale-tested the central components to more than handle the 15 million and more potential requests the service could receive. Furthermore, we believe that the digital architecture can be deployed quickly to meet the stated timescales.

Through the DWP paper, government has given dashboards the green light. The task now is for the industry to help MAPS and the delivery group take the project forward to launch. It is a most exciting challenge and one that can have a significant positive effect on the wellbeing of this nation’s retirement savers.

The Global Open Finance Centre of Excellence project hits a new milestone

The Scottish bid for the development of The Global Open Finance Centre of Excellence (GOFCOE) has received very good feedback from the Strength in Places Fund assessors and moves to the second stage as announced todayby the UK Research and Innovation organisation

In October 2018 a Scottish consortium decided to come together behind the ambitious project of launching the Global Open Finance Centre of Excellence in Edinburgh and apply for funding from the Strength in Places fund.

The University of Edinburgh, FinTech Scotland, Scottish Enterprise and the Financial Data And Technology Association (FDATA) joined forces to produce a very strong application.

Open Banking, and its impending evolutions into open finance more generally, is the biggest global trend in financial services, for people and for businesses.

A centre of excellence would be a world first, providing leadership, coordination, research and capability to support this rapidly expanding and evolving phenomenon.

The GOFCOE is one of twenty-four ambitious projects, from pharmaceuticals to aerospace, and transport to the creative economy, that have received early-stage funding to develop full-stage bids that could lead to significant economic growth in places.

The GOFCOE project will receive early-stage funding, which will allow for the development of full-stage bids.

Ultimately, eight of the strongest bids are set to receive additional funding to carry out projects designed to drive substantial economic growth.

Announced in the modern Industrial Strategy in November 2017, the Strength in Places Fund will benefit all nations and regions of the UK by enabling them to tap into the world-class research and innovation capability that is spread right across the country. The fund brings together research organisations, businesses, and local leadership on projects that will lead to significant economic impact, high-value job creation and regional growth.

Chief Executive of UK Research and Innovation, Professor Sir Mark Walport, said:

Our clear vision is to ensure we benefit everyone through knowledge, talent and ideas. Significant support through the Strength in Places Fund will further catalyse economic potential across the country by bringing researchers, industry and regional leadership together to drive sustained growth through world-class research and innovation.’

The Government confirmed in the 2018 Budget that the Strength in Places Fund is to receive a further £120m to bring the fund budget for the period up to 2021/22 to £236m.

Stephen Ingledew, Chief Executive at FinTech Scotland said:

“The Global Open Finance Centre of Excellence builds on Scotland’s heritage of financial services and enviable entrepreneurial track record combined with an enlightened and progressive culture which aligns the social and economic benefits of innovation. Going forward the Centre of Excellence focused on data driven innovation will support the inclusive growth objectives of Scotland, leveraging the ongoing role of international collaboration across Europe and globally with the private sector, consumer groups, academia, regulators, governments”

Jarmo Eskelinen, Director of the Data-Driven Innovation initiative at the University of Edinburgh said:

“The University of Edinburgh is delighted to support the Global Open Finance Centre of Excellence [GOFCOE] and to be developing this exciting project in partnership with FinTech Scotland, FData Global, Industry and Academia across the central belt of Scotland. The success of the Strength In Places Fund [SIPF] bid is confirmation of the importance of innovation for industrial strategy in the UK and we look forward to engaging with the consortium to develop the GOFCOE in the coming months. As a partner in the Edinburgh and South East Scotland City Region Deal, this project exemplifies all we are aiming to achieve through our Data-Driven Innovation initiative; attracting talent and investment to the region; linking world-class researchers and data analytics expertise with industry and innovating to drive new products and services.”

Danny Cusick, Director Multi Sectors at Scottish Enterprise said:

“We’re excited to be developing this project with our partners as it has the potential to bring substantial economic benefits through increased innovation and inclusive growth to firmly establish Scotland’s reputation as a world leader in Open Finance. Scotland already has exceptional capabilities in fintech and data and the Centre of Excellence demonstrates what we can achieve through collaboration to create competitive advantage for Scotland.”

Open Banking: Bringing Product Diversification & Consumer Choice

In a major vote of confidence in the future of Open Banking, Clydesdale Bank has integrated the DirectID Open Banking Platform from The ID Co. into its B mobile banking app. B analyses user data to make informed suggestions about spending and saving habits. Use of the platform will allow customers to see their account details and balances from all major banks and building societies in one location.

PSD2

Following the passage of the second Payment Services Directive in January, the nine biggest UK banks have been opening their data to approved FCA companies such as The ID Co. and other Payment Initiation Services Providers (PISP).

We have been extremely vocal in our support for Open Banking, bringing about, as it does, a tremendous opportunity for banks and customers. In the case of Clydesdale Bank customers, they can now import banking data from a range of UK banks including: Barclays, HSBC, Lloyds Group, Santander, RBS and Nationwide, as well as digital banks such as Starling and Monzo.

Future Developments

This is an excellent start for legislation that has only been in place for eight months. For both the industry, and consumers, the future is even more exciting.

The introduction of Open Banking and PSD2 are set to revolutionise the banking sector, as new players and smaller disruptor banks can level the playing field and compete with the established players. This in turn will lead to an upsurge in the volume of innovative products that are on offer to banking consumers, which will ultimately transform the sector.

Tech Innovation

Through the use of APIs, we expect to see further innovation and growth amongst new businesses in the financial technology space, as well as within banks directly. This is in part being driven by customer expectation. Consumers in the main continue to bank with the five largest banks (Lloyds, HSBC, Barclays, RBS & Santander), but due to their size and scope and lack of direct competition, services have not matured in line with technological innovation. Savvy consumers demanding innovative products are being offered more opportunity than ever to tailor the services that they are offered by financial providers.

“Clydesdale’s adoption of Open Banking is an exciting step forward in how Open Banking enabled propositions are helping customers securely move, manage and make more of their money.”

Imran Gulamhuseinwala OBE, Trustee of the Open Banking Implementation Entity.

Moving forward, we are confident that account integration will be viewed as the starting point for Open Banking. Companies, including the ID Co., are building products and services that will address such diverse issues as income verification, affordability, credit risk, and Know Your Customer (KYC).

These, individually and collectively, will impact upon major issues across the globe such as financial inclusion and servicing the unbanked, allow access to credit for those with thin credit histories, and drive down the cost of lending for consumers.

Digital Banks

The view amongst industry experts is that there is now a defined movement away from viewing banks as focusing solely on money, and towards banks becoming connected spaces for digital services. How banks react and take up this mantle could be key to their success in this new era of Open Banking. We have already witnessed banks such as Starling, Monzo and Atom Bank that have developed their proposition based on the ability to provide a “marketplace” of additional features to their customers ”“ albeit not based on Open Banking – and it is now up to the larger banks to respond.

Closing Thoughts

Open Banking has ultimately been brought about through the will of Government in order to offer consumers more choice and range in their financial products. Now that Open Banking is here and is happening, the response of the major banks will be closely monitored.

We are delighted that Clydesdale & Yorkshire Bank have understood the need to explore and implement functionality brought about through Open Banking, and we look forward to working closely with them. As more services and products are brought to market through fintech companies, challenger banks and the established players, we look forward to understanding their impact upon the industry, and ultimately the consumer.

Author

James Varga, CEO, The ID Co.

James founded The ID Co. in 2011 with a mission to create convenience””to allow us to sign up to new products and services in seconds.

The ID Co. builds products based on (open) bank data that helps businesses like online lenders to onboard their customers efficiently by solving pains such as affordability and credit risk.

Our DirectID business products help lenders to onboard their customers by removing friction caused during the application process by the current challenges of risk, compliance, fraud, and regulation.

The products we provide solve business pains such as assessing a customer’s affordability, verifying their account information, and thereby offsetting credit risk.

James is active in a number of local and global efforts to help people do more online, including the Fintech Delivery Panel (FDP), FDATA, Open Banking Excellence | Edinburgh, and Trust In Digital Life (TDL), whose mission is to create a trusted ecosystem that protects the data and assets of citizens and enterprises across Europe.

Open banking: Catalyst for collaboration and partnership

Open Banking – the challenge

Opening Banking was a popular theme at the annual Scottish Fintech conference and it was analysed from numerous angles e.g. likely changes in the market landscape that might be triggered by Open Banking, how banks are losing the control over the purchasing process of financial products, and PS2D regulation.

During the conference, Phill Gillespie from Money Dashboard and I had the opportunity to host a workshop about Open Banking and the API ecosystem in the FS industry.

The underlying challenge we face in the FS industry is plain and simple”¦for most people FINANCES ARE BORING! But it is also true that without financial products we would not be able to protect ourselves and our families, we would not be able to sustain our lifestyle or achieve our personal goals. We do not think how cool buying a insurance is and we certainly do not brag with our friends about our pension plan, but we need these products because we want to travel safely and enjoy our retirement.

The power to re-organise the industry

At Inbest.ai, we think that Open Banking will allow companies to place FS products and services where they belong, co-piloting our lives and checking that we are taking the right decisions to protect our families, maintain our lifestyles or make our hard-earned salaries go further.

FS companies must be humble and flexible to seamlessly embed their propositions into the products and services we use throughout our lives i.e. banking should be a mean to improve our lives, not a goal on its own. To deliver this strategy, FS companies should understand intimately customers’ needs and behaviours as well as collaborate with companies in other industries to distribute their products and services. If FS companies keep working in isolation, non-financial players with large Balance Sheets will be more than happy to fill this market gap, as Bill Gates famously stated, “Banking is necessary, banks are not”.

Another alternative will be reducing their front-line exposure and focusing on a core part of the banking stack e.g. trading, foreign exchange, settlement. To succeed in this strategy, these specialised banking services should be easy to consume by companies that are downstream in the value chain.

All in all, regardless of the strategic route, partnering and collaborating should be a core foundation on the way modern FS providers operate, and APIs are the technological framework that makes this possible. FS providers should embrace the use of APIs across their different teams and divisions as well as with their suppliers and customers.

Want to find out more?

Inbest.ai is on a mission to automate, simplify and personalise long-term financial planning to make financial advice & guidance accessible and affordable. APIs are the backbone of our company and we use them not only to build, market and sell our Financial Planning platform but also to manage our business.