Blockchain, a key driver for economic growth

Article written by Maciej Zurawski, Founder and CEO, Musemantik

We all know technological innovations are a key driver of economic growth. Innovation is so essential to increase the productivity and efficiency of value creation that economists attribute a staggering 85% of the economic progress in the Twentieth century was to technological innovations. For those of you keeping score, that’s a little over five of every six dollars that the world economy grew by in the last hundred years can be directly credited to technological advancement. What may surprise you is just how much developing Blockchain technology can further this trend towards prosperity.

Blockchain is a novel development in computer science that can escalate economic growth radically through personal value creation. Fundamentally, it is a technology of distributed data and digital assets that are spread across a global, decentralised computer network. New data is chronologically recorded in blocks that are cryptographically in a permanent chain of synchronised information. This information shared is public and does not rely on any centralised actor for it to operate and consequently cannot be manipulated by corrupting information on a central server. Data contained within the blockchain is completely secure and trustworthy allowing for applied use of data in new and valuable ways. In the same way that instant communication revolutionised the economy, totally secure communication offers incredible economic, social, and societal benefits. We at Musemantik believe that the Scottish economy is particularly poised to adopt Blockchain and to take advantage of the myriad benefits adoption will bring.

In brief, we estimate a £2.46 billion contribution to Scotland’s GDP by 2030 as a consequence of information transparency, £1.1 billion in efficiency savings, and a £4.48 billion general increase in GDP as a consequence of adoption. [I] We encourage general implementation of blockchain solutions to capitalize on their benefits to create value for Scottish society. By encouraging socially responsible supply chain activities, implementing user-friendly health care systems, and reducing the costs of data transactions or financial intermediaries this have the potential to increase the national wealth substantially.

[i] The calculations are based on the figures in the “Time for trust” report of PWC (2020) and on the share of Scottish GDP from the total GDP of the UK.

Photo by RODNAE Productions: https://www.pexels.com/photo/silver-and-gold-round-coins-8370389/

A conversation about art and NFT with Trevor Jones

Season 2, episode 4

Listen to the full episode here.

The NFT movement seems to have taken the world by storm. For most people it came out of nowhere and when most people are grappling with the idea of digital currencies, they now have to deal with non-Fungible-tokens. Digital currencies are changing everything and not just the way we deal with money. However, it’s not just about coins anymore. Today, in the episode we’re speaking about how it’s affecting one of the oldest disciplines in the world. Art. And just like appetite for cryptocurrencies is going up and down (down at the minute) so might NFTs. However, one thing is for sure is that they are here to stay. On this episode we welcome on of the top 10 NFT artists in the world according to most NFT specialists, Trevor Jones. Trevor is Canadian but has chosen bonny Scotland to establish himself and his art. With him we’ll discuss his incredible story and his vision on this new world. This podcast will also be an opportunity to showcase the Stirling Castle Party.

Trevor Jones – a story of art and NFTs

I never planned on or expected to be an artist. Although I took art classes in high school in Canada (as I had a natural talent) it wasn’t until my early 30s that everything changed. I left my home country in my mid-20s with a backpack to explore the world, working mostly in hospitality to get around and ended up in Scotland a few years later on a UK ancestry visa. After making some bad decisions I spiralled into depression, and I hit an important crossroads in life. For some strange reason, I decided that art would save me’.

Proving one’s never too old to follow one’s dreams, I enrolled in a foundation course at a small school in Edinburgh and the following year I was accepted into Edinburgh University and Edinburgh College of Art for the 5 year MA Fine Art programme. Thankfully, I managed to escape the dark depths of depression by the time I graduated; however, I now found myself at 38 years of age, broke and armed with very little but a huge student loan and an art degree.

Moreover, after two moderately successful commercial gallery solo exhibitions, I came to the conclusion that it was near impossible to make a living as an artist. So, there I was, working two jobs; managing a small art charity and teaching part time whilst running an Airbnb year round at my flat, to make ends meet all while spending every other spare moment painting.

I realised that if I were to make my art career dream viable that I would need to somehow differentiate myself from all the other artists exhibiting in Scotland, which led me to exploring and integrating new technologies with my work. In 2011 I was investigating QR code oil paintings and by early 2013 I was employing augmented reality as one of the first professional painters in the world to use AR.

I was more than excited when it came to exploring art and tech innovation but unfortunately it appeared the Scottish art world felt almost the exact opposite to me. As constant rejection of my artworks continued to fuel my frustration with the institutions was mounting, I decided to troll the legacy artworld with various tech inspired stunts.

For example, after my AR painting was rejected once again from the annual Royal Scottish Academy open exhibition, I snuck into the RSA building the day before the opening to photograph all the works on display. That night I augmented over 60 paintings and digitally replaced’ them with my pieces. I counterfeited 25 invitations and turned up to the posh opening night with a bunch of friends with smartphones and tablets and my AR app turning the event into the Trevor Jones solo exhibition. Some of the old guard’ weren’t too happy with me after this stunt but at the same time I also managed to build a little excitement and momentum around my artwork.

Fast forward to 2017 and for once I had a bit of money in the bank after a successful AR solo exhibition ”“ one that I’d organised myself as commercial galleries were no longer interested in showing my paintings. I invested in Bitcoin and very quickly became consumed with the world of crypto. I began coordinating my next solo show, which was titled Crypto Disruption: The Art of Blockchain. Almost all the paintings sold to crypto enthusiasts internationally via bitcoin and eth (which completely boggled my mind at that time!) and it was by far my most successful exhibition.

Near the end of 2019 I dropped my first NFT, a collaboration with the late, great Alotta Money, which broke all previous NFT sales records and really put me on the cryptoart map. I think I was a bit of an anomaly, as an academically trained painter coming into this space filled with almost entirely digital artists; which again, likely helped to differentiate me from the rest.

Things have continued to go from strength to strength with the last couple years being quite literally life changing both creatively and financially. Along with my record breaking Bitcoin Angel open edition drop on Niftygateway, seven figure sales collaborations with Pak, Metacask and the legend Ice Cube, and hiring Stirling Castle in July to throw an exclusive party for 300 of my angel collectors, I’m now working on a commission which will be a gift for a very high profile individual who makes electric cars and rockets.

My dad always used to say to me, “Son, life’s a funny thing” and he wasn’t wrong. I guess I’ll now add to his words with, “Work hard, persevere, focus on being different and you never know where you may end up.”

Why early payments could be the key to strengthening supply chains

Why early payments could be the key to strengthening your supply chain

Having a strong supply chain is one of the most powerful tools you can have in your arsenal. Creating a solid network of all the organisations involved in delivering your product or service to your end customer ”“ from vendors to producers, warehouses to retailers ”“ is critical to keeping things running smoothly. In fact, it can make or break your success.

But if there’s one factor that can help boost and strengthen supply chains, across all sectors and industries, that often gets overlooked, it’s the power of early payments.

Here’s why they could be the key to making your supply chain even stronger.

Building confidence and trust

It might sound simple, but don’t under-estimate the importance of having confidence in and being able to trust each and every member of your supply chain. Early payments can help build this confidence ”“ for both suppliers and customers alike.

If you’re a buyer, offering to pay early (for example in return for a small discount), signifies that you’ve got the cash ready and waiting, and are considerate of the fact that your supplier might benefit from a boost to their cash flow before the date their invoice is due.

For suppliers, being able to incentivise your customers to pay early by offering a small discount signals sound financial wellbeing. If you’re able to offer your services or products at a beneficial cost, it implies you’re not stretched to the last penny ”“ which gives customers confidence and reassurance that you’re not at risk and they’ll be able to keep buying from you.

Access to better deals

It goes without saying that, if early payment benefits both buyer and supplier, there could be great deals attached to paying up early. When either side is empowered to use early payment as a tool for negotiation ”“ whether that’s a reduction in price, a speedier delivery, or another mutually agreed benefit ”“ it can help move things along exponentially, and might even lead to longer term process changes in your supply chain that keep things really efficient and effective.

Reputation builder

If you’re a buyer that’s offering to pay early, you’re going one step further than avoiding a reputation as a nightmare customer that your supplier has to keep chasing: you’ll become a preferred choice.

When suppliers are stretched or at capacity, they’ll be in a position to choose who they work with. Customers or buyers with good reputations for paying on time (or, even better, early) are much more likely to make their way up the food chain of preference ”“ and might even attract more suppliers looking to work with them, as a result of word of mouth, too.

Growth on both sides

It’s no secret that, for the SMEs and start-ups that form a bulk of the UK’s suppliers, cash is king. Offering early payment can be a real cash injection that helps SMEs out with their cashflow. And good cashflow means more money to invest and grow.

But the benefits aren’t one sided. If you’re a buyer that’s looking to grow, you’ll need your suppliers to be able to keep up with your ambitions ”“ which will likely lead to an increased demand for goods or services. By paying them early and helping them grow, you’ll be helping them to help you grow, when the time comes.

Only as strong as your weakest link

When it comes down to it, your supply chain is only as strong as its weakest link ”“ and late payment has a habit of breaking the bonds that the chain relies on. In fact, according to a recent survey of 500 UK decision makers, 86% agreed that one single late payment affects everyone in the supply chain. And, out of the 31% of businesses that admitted paying a supplier late, almost half say it was due to a late or failed payment from their customer.

So, if late payment has a knock-on, negative impact on everyone in a supply chain, imagine the knock-on, positive impact that early payment could have, if things were reversed?

How Early Pay can help

If reading this has convinced you that building early payment into your supply chain is something you should be looking at, you’re in the right place.

Our CEO, Anthony Persse, thinks it’s time to turn the conversation about late payment on its head: “By shifting towards a more positive conversation about early payment’, we will do much more than simply improve payment performance. We will help create more jobs, deliver greater levels of investment and generate deeper social value with long-term sustainability at a time when the country needs it most.”

If you’d like more information visit saltare.io, or please get in touch with the team at Info@saltare.io and we’ll be happy to help.

The Identity Tooling Needed for Institutional Adoption of DeFi

Blog written by Kai Jun Eer, founder of fintech Onboard ID

In the past year, the term Web3 has become an increasingly used buzzword. The growth in different blockchain protocols and metaverse projects seem to have shed a light on how the new Web3 might look like. We are on the forefront of technology innovation, and we are really excited about it. Yet, it is important to remember that Web3 is not just about crypto and metaverse, but how we define a more user-centric internet. Behind every shining DeFi protocol or NFT project, there is an infrastructural layer supporting them.

Most of the current decentralised finance (DeFi) protocols are pseudonymous in nature (meaning each user is tied to an identifier but not to its real world identity). As these protocols start to grow into institutional adoption, inevitably they will need to comply with certain institutional regulations. One example being some of the users might now need to undergo the Know-Your-Customer (KYC) verification in order to continue interacting with these institutions through the DeFi protocols. I envision that as DeFi matures, the underlying protocol that facilitates the settlement / transactions would be fully decentralised and trustless, while specific use cases can be built on top of the protocol where some might introduce regulations.

A concrete example is Aave, one of the largest DeFi protocols deployed on multiple blockchains such as Ethereum and Avalanche. Aave first started out as a decentralised lending and borrowing protocol. Earlier this year, Aave launched a permissioned protocol (Aave Arc) that targets institutional adoption. The benefits that a blockchain can bring to speed up efficiency of financial settlements do not have to be limited to a fully decentralised setting. However, users that interact with Aave Arc have to undergo KYC in order to meet regulatory requirements.

As more DeFi protocols are becoming more regulated to expand their markets to financial institutions, does that mean that as an end user, each time I want to access a different protocol, I have to undergo a KYC verification again and again? Other than not user-friendly, it makes an already high barrier to entry in DeFi even less accessible.

A digital identity might help. Imagine if an end user only has to undergo the KYC process once, where it receives a digital identity which can be subsequently presented to the different DeFi protocols. With increasing awareness of data privacy and data ownership, users want to be in control of their own data. As an end user, I no longer want to delegate my identity data to a centralised data custodian (think Google ID), especially sensitive data such as what financial services I am accessing. There is a need for a privacy-preserving identity solution, which provides convenience yet still user-centric.

At Onboard ID, we are building the next generation identity tooling, where users are always in control of their own data. Once a user has undergone the usual KYC verification, it receives a cryptographic digital credential which contains the user’s verified identity data. The identity data is only stored in the user’s mobile phone and not in any central databases. An identifier of the credential is recorded on a public permissionless blockchain, such that when the user presents its credential, it is verifiable that the identity data in the credential comes from the trusted KYC provider. The reason our solution is user-centric is that during KYC reverification, data transfer only happens between the user and the verifier without passing through any third parties, not even us as the infrastructure provider. Therefore, users are always in control of how they want to share these data and with whom.

We are currently in beta testing. If your organisation is looking to get an edge in streamlining KYC reverifications, whether it’s in the fintech sector, looking to get into DeFi, or other more specific use cases, please get in touch at kaijuneer@gmail.com! Our vision is to contribute towards building a more user-centric internet, and we hope you could come onboard with us.

Payments & Transactions, the fintech opportunity

is discussing the key outputs in a series of blogs. This blog focuses on Payments & Transactions, which is one of the four key strategic priority themes.

is discussing the key outputs in a series of blogs. This blog focuses on Payments & Transactions, which is one of the four key strategic priority themes.

The way we pay for things is changing. Throughout the development of the Research & Innovation Roadmap, payments and transactions were referred to in the broad context of the transfer of value (either money, goods, or assets) in exchange for goods and services.

The Roadmap pinpoints the significant move from physical exchanges to digital transactions, and identifies several significant trends that could mean payments will change significantly in years to come. These changes will have a significant impact on the economy, and could also have a substantial impact on citizens and businesses, which is why the future of payments is one of the four priority themes identified.

The importance of Payments & Transactions

The pandemic accelerated the move from physical to digital in many aspects of our lives, including how we make transactions. Customers’ digital expectations and a shift towards more instant electronic payments are having a significant impact on our economy, and a new digital economy is emerging strongly, with major implications for consumers and SMEs alike.

Across the development of the Roadmap, when looking at the theme of the future payments we considered the topic of digital currencies and crypto currencies. These innovations present new ways for value to be stored and exchanged. It is clear there is a still a lot to learn about the potential, the impact, and the implications of cryptocurrencies as a method for mainstream payments. Stablecoin is a form of cryptocurrency that is linked to an asset that is stable in value, and stablecoins are generating significant interest for future payments and value exchange.

The UK Government has established a crypto assets taskforce, and the UK regulators are considering the benefits and risks on a range of issues connected to this topic, including a separate digital currency backed by a central bank. Since the publication of the Roadmap, HM Treasury has confirmed its commitment to the development of appropriate regulation for crypto.

As we further explored the payments theme, we identified technologies of particular interest, such as AI, blockchain and distributed ledger tools. Industry expressed interest about how these technologies could offer a completely different way to organise and manage payment systems, providing a route to real-time, cross-border payments worldwide. These developments pave the way for a potentially very different future of value exchange. According to the World Economic Forum, up to 10% of global GDP could be stored on blockchains by 2025.

Embedded payments is one of the hottest topics in FinTech in 2022, and was another area of particular focus. Technology is advancing the methods to embed payments in everyday experiences and allow customers and businesses to pay for purchases without entering bank details, credit, or debit card information.

Historically, the payments process has lived at the edges of experience for businesses. Payments were either taken in cash, or offline, with no real lasting insights into the customer and the goods or services they purchased. Technology businesses are now fully embedding software that enables a change to this experience, creating more choice and allowing businesses to have a deeper connection with customers. In addition to high profile examples such as Uber, many embedded payment innovations are emerging, such as in-car payments, smart fridges and connected homes.

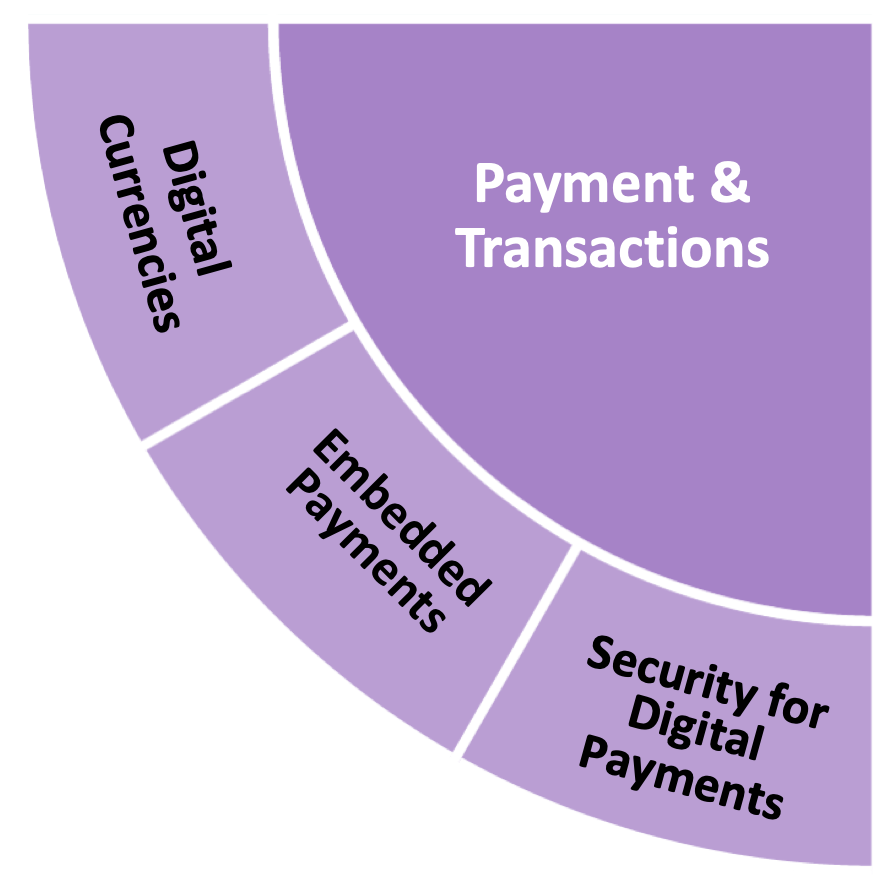

Priority areas in Payments & Transactions

The industry contributors to this roadmap offered a view that the future looks set for significantly more change. Our analysis highlighted three topics of interest:

Digital currencies

- Cryptocurrencies and stablecoins

- Distributed ledger technology

Embedded payments

- SME market

- Retail consumers

Security for digital payments

- Cyber security

- Biometrics

Roadmap next steps: Payments & Transactions

A range of proposed next steps are laid out in the published Roadmap, which specifically identifies 10 actions relating to Payments & Transactions, and categorises each into one of three phases over the next 10 years. These actions are illustrated in the graphic below. The report also references 23 different stakeholders who can support the implementation of these actions, which are broken down into research projects and innovation calls.

More information about FinTech Scotland’s Research & Innovation Roadmap can be found here, where the full Roadmap can also be downloaded.

The FinTech Research and Innovation Roadmap

Season 2, episode 1

Listen to the full episode here.

In March 2022, FinTech Scotland released its 10-year Fintech Research & Innovation Roadmap for the UK.

In collaboration with leading universities, large financial institutions, fintech businesses, citizens, industry experts and senior officials this report explores the opportunities that will help the UK maintain its fintech leadership globally.

In this episode we explore what this roadmap means for Scotland and what the next steps are to deliver on the roadmap recommendations.

Fraud Academy ”“ Cryptocurrency: Opportunity vs Threat

Fraud Academy ”“ Cryptocurrency: Opportunity vs Threat.

Are you familiar with the legislation and rules that pertain to cryptocurrencies in the United Kingdom? What can be done to prevent crime involving cryptocurrency, where could fraudsters go from here, and how do we begin to investigate this?

PwC are hosting a highly informative virtual event and will explore these questions, and more.

Date: Wednesday 9th February 2022

Time: 13:00 – 14:15 (GMT)

Location: Virtual / Webcast

Within the first nine months of 2021, cryptocurrency related fraud is estimated to have cost the UK over £146 million; a figure already 30% higher than that noted for the whole of 2020. Over 7,100 reports of fraud involving cryptocurrency have been made to the UK’s national reporting centre for fraud. More than half of victims were aged between 18 ”“ 45.

Cryptocurrency will only become a bigger part of how we do business, presenting both an opportunity and a threat; yet how ready are we to make the most of the opportunity and to deal with the threat?

Are you aware of the legislation and rules which exist in relation to cryptocurrencies in the UK? What can be done to prevent crime using cryptocurrency, where could fraudsters go from here and how do we start to investigate it?

At this highly informative virtual event, we will explore these questions, and more with a panel of deep subject matter experts.

We are delighted to be joined by Jim Robertson (DCI, Police Scotland), who will give an overview of the current lay of the land’ from a policing perspective in relation to cryptocurrency and discuss how law enforcement is dealing with the challenges of an increase in this crime type.

Jim will be joined by Craig Kennedy (Partner, Dentons), who will discuss the legal powers available in relation to cryptocurrency in the UK and the potential risks and benefits of using cryptocurrency.

We will also be joined by Haydn Jones (Senior Blockchain Market Specialist – PwC) who will share his own opinions and thoughts on the opportunities and threats presented by the rise in cryptocurrencies from his own experiences investigating and providing expert witness testimony on cases involving cryptocurrency.

Attendees will also have the opportunity to put questions to our speakers during a Q&A session.

We look forward to welcoming you to our event on Wednesday 9 February 2022 at 1:00pm.

If you have any questions about this event, or have any issues registering for this event, please contact the team via uk_fraud_academy_scotland@pwc.com or uk_ni_fraud_academy@pwc.com.

PRESS RELEASE: Automation the key to growth and data management for banking and payments sector, finds new report

A new report from leaders in reconciliation and finance automation software, AutoRek, has found widespread concerns around the ability of businesses to grow amidst scalability and regulatory pressures over the next three years, affecting 92% of professionals surveyed.

The report ”“ Banking and Payments in 2022: Digital transformation and trends in financial technology ”“ was designed to provide an insightful view of the key challenges and solutions that will face the financial industry as it enters 2022.

AutoRek gathered insights from senior professionals across the banking and payments industry on the barriers they face surrounding the handling of payments data, compliance and growth, and new technologies in use or consideration.

Automation was found to be a key source of hope for enabling growth and regaining competitive advantage. Other key findings include:

- Manual processes form the biggest roadblock to achieving automation, cited by 46% of firms, followed by legacy systems (42%), poor interoperability (40%) and regulatory requirements (38%).

- In-house IT solutions are the most common for data handling across payment operations, used by 44% of firms ”“ a higher reliance on in-house systems than in most other sectors.

- Almost one-third of firms consider their jurisdiction’s regulatory body audit and control around regulatory reporting infrastructure somewhat or far too strict, while 22% consider it somewhat or far too lax. Just under half consider it appropriate. Financial institutions in central and south America were considerably more likely to view their regulators as lax than their European and Asia-Pacific counterparts.

- When selecting a solution to handle payments data, almost 80% of respondents consider its ability to integrate easily with existing infrastructure a key factor.

- Over half of respondents (56%) either already have or are in the process of deploying modern technologies such as artificial intelligence (AI), machine learning (ML) and application programming interfaces (APIs) to help monitor and streamline their data management processes. One-third had onboarding planned in the next 12-24 months. Only 12% reported having no plans to apply technology to improve data management processes.

Firms slow to adopt emerging technologies should be aware that they are now falling behind in an increasingly automated and competitive landscape, according to Nick Botha, Banking Lead at AutoRek.

Commenting on the findings of the report, Nick Botha continued: “While automating data flow has been a priority for some years now, this survey makes clear how many inefficiencies continue to plague firm’s day-to-day operations when it comes to data processing and reconciliation. Legacy banks in particular are grappling with often more than 20 disparate systems written in varying generations of software, none of which are designed to interact with one another.”

“While a decade ago that might have flown under the radar, the last few years have seen control of the payments space shift from banks into the hands of Payment Service Providers (PSPs), whose ability to deliver totally user-native customer service is forcing the whole industry to step up.”

“Beyond competing for market share, it’s a question of compliance. The costs associated with non-compliance are substantial both from a financial and reputational perspective, and regulators are increasingly less forgiving, as we have witnessed in the last few months with significant fines incurred by some of the world’s largest banks.”

“New technologies like AI, ML and APIs can be used to create greater interoperability and remove or significantly reduce manual interventions and use of spreadsheets. Investing in these capabilities today will enable firms to address evolving customer preferences, mitigate risk and achieve regulatory compliance down the road ”“ essential elements for remaining competitive in the payments landscape of today.”

Rise, created by Barclays, launches new Insights report that decrypts crypto

Rise Insights report lead, Colin DeLarso (Assistant Vice President ”“ Innovation, Barclays) shares some highlights

The latest edition of the Rise Insights report, “Decrypting crypto”, reviews the new world of digital assets in financial services. It demystifies some of the most pertinent and often complex concepts, explores what the innovations might mean to FinTechs and institutions, and examines ways they can both benefit ”“ from subjects as diverse as regulation, efficiencies in payment systems, rolling out Central Bank Digital Currencies and what it means to bring about universal participation in the crypto-economy.

The FinTech ecsosystem is leading the charge in this blockchain-driven space, designing the platforms on which crypto-assets are created, stored and exchanged, and developing the decentralised apps (dapps’) that support some extremely new use cases. The pace of change is so fast, and market interest is so high, that now everyone is taking notice – even large banks.

Charlotte Kanagasabapathy, Global FinTech Platform Director in Barclays Innovation, makes the point that:

Charlotte Kanagasabapathy, Global FinTech Platform Director in Barclays Innovation, makes the point that:

“it’s only a matter of time before technological limitations such as scalability and interoperability are overcome. Beyond that point, a financial system built on blockchain may be unrecognisable by today’s standards.”

In the report, Shreepad Shukla, Enterprise Architect in Barclays’ Chief Technology Office, makes the case for deep and collaborative enterprise engagement.

“Turning crypto-use cases into workable solutions will require organisations to innovate alongside FinTechs, central banks, regulators and even competitors,” writes Shreepad.

Digital assets are being implemented by traditional financial institutions. Compared with the wildfire of FinTech disruption, it’s been a slow burn for larger enterprises, but they’re definitely accelerating their adoption of blockchain technology. Here’s a survey of some of the work taking place and the considerations many enterprises face. Read more about these subjects in the report.

Corporate infrastructure meets blockchain

Alisa DiCaprio, Head of Trade at R3, explains why implementing Distributed Ledger Technology (DLT) is such a huge task for any enterprise financial services firm, and how they can keep up to date. This involves both DLT interoperability and, unsurprisingly, careful consideration of legacy systems.

Enterprise-ready security opens the crypto-economy to institutions

Financial institutions will be one of the biggest contributors to growth of the crypto-economy. The signs are that this is more than a research project for them. They’re investing in crypto in record volumes, say Coinbase’s Brett Tejpaul, Head of Institutional Sales, and Greg Tusar, Head of Institutional Product. While security remains a concern for larger organisations, infrastructure is being created that allows crypto-trading to become a reality for them.

STOs and smart contracts are reinventing securities

Security Token Offerings (STOs) have built-in restrictions to make them more compliant with securities regulations. STOs combined with smart contracts are allowing companies to formulate new financial propositions, save costs and simplify processes. Chris Housser, Interim CEO of Polymath, leads us through these concepts and suggests ways for traditional financial institutions to adapt to and take part in new forms of investing.

DLT innovations at Barclays

Barclays’ Chief Technology Office (CTO) is at the cutting edge of Distributed Ledger Technology (DLT) and has a long history of innovation. Shreepad Shukla, Enterprise Architect in the CTO, describe the work he’s been doing on two crypto-projects: digital fiat currencies and wholesale payments. The key to success with both innovations is close collaboration with governments, regulators and FinTechs.

FinTechs featured in the report

Contributors to this edition of the Insights report include:

- Chainalysis is an alumnus of the 2015 New York Barclays Accelerator, powered by Techstars, and provides data, software, services and research to government and law-enforcement agencies, exchanges, financial institutions and cybersecurity companies in over 50 countries, helping them to ensure cryptocurrency compliance

- R3 delivers trust technology for multi-party applications, connected networks and ecosystems, and regulated markets expertise. R3 is the creator of Corda, a permissioned blockchain platform allowing businesses to build networks so they can transact directly and privately using Distributed Ledger Technology (DLT)

- Coinbase operates the largest cryptocurrency exchange in the United States by trading volume[1] and is enabling universal participation in the crypto-economy for institutions and corporations

- Solana is a decentralised, permissionless blockchain built to enable scalable, user-friendly apps for the world. The project is Open Source and has an extensive ecosystem of developers and validators (who validate transactions added to the blockchain ledger)

- Polymath has an Ethereum-based solution for securities trading using security tokens. Polymath’s Polymesh platform supports confidentiality, identity, governance and cross-jurisdiction execution

- Arch is an alumnus of the 2015 New York Barclays Accelerator, powered by Techstars. Arch (formerly Smash) untangles DeFi, allowing investors to buy into diversified strategies at the crypto frontier

- Andrea Maria Cosentino is Co-Founder of Licas Ventures and Global Business Strategy & Development Manager at Bloomberg. He has extensive corporate and startup experience in financial markets and technology

Get involved

“I’m a big believer in the ability of blockchain technology to effect fundamental change in the infrastructure of the financial service industry.” ”“ Bob Greifeld, CEO of NASDAQ

- Download the Rise Insights report to learn more about how digital assets are impacting financial services, and for more on the FinTech companies mentioned here

- Listen to the latest episode of the Rise FinTech Podcast

- Contact the Rise team in London or New York to meet any of the companies featured in the report or in the Rise ecosystem of over 100 FinTech startups