Where Banking Is Heading: From Vision to Execution in London this May

Banking Transformation Summit | 19–20 May | Tobacco Dock, London

The Banking Transformation Summit is the definitive gathering for senior executives driving real change inside Europe’s leading banks and building societies to shape what’s next in banking. Returning to London on 19–20 May, a verified audience of 1,000 decision-makers will convene at Tobacco Dock; a first-class venue delivering premium hospitality for all attendees, and located a convenient distance from London’s financial districts and major transport links for ease of travel.

What to expect: agenda and themes

Carefully curated to ensure high-value connection and strategic clarity, the two-day agenda addresses the decisions, technologies and leadership challenges actively reshaping banking today. Day One focuses on vision and where banking is heading, exploring what’s changing across the industry, the forces shaping the future of financial services, and what leaders need to be thinking about next as regulation, technology, and customer expectations continue to evolve. Day Two turns vision into execution, examining how ideas translate into action inside complex banking environments, what actually works in practice, and how teams move forward with confidence and clarity.

Across the two days, 150 world-class speakers will share practical, battle-tested insights and honest perspectives on what’s working today and what’s coming next, providing actionable, take-home learnings to apply to your own strategies. Through keynotes, panels, roundtables, lightning talks and demos, they’ll divulge exclusive case studies across six core themes, reflecting the most important challenges and opportunities banks are facing:

- The AI Frontier: Explore how generative AI, machine learning, and predictive analytics are transforming customer engagement, fraud detection, risk management, and operations.

- Intelligent Infrastructure: Learn how banks are simplifying legacy environments, improving resilience, and building the foundations for AI-powered transformation.

- Money in Motion: Discover how the flow of money is changing, with real-time payments, instant settlement, digital identity, and the platforms powering embedded finance.

- Trust in the System: Explore how banks are strengthening defences, improving detection and response, and protecting customers while still enabling innovation.

- Power to the People: Dive into how banks are redesigning services that are faster, simpler, and more relevant while meeting rising expectations and Consumer Duty.

- Human & Machine Leadership: Learn how banks adapt their culture, operating models, and ways of working as automation and AI reshape roles, teams, and decision-making.

Networking, audience and how to attend

Every detail has been centred around connection, from the event app with messaging and meeting booking functionality, to networking breaks and more informal drinks receptions – ensuring you network and connect with the transformation leaders driving real change. With 62% of attendees at VP-level and above, and more than 120 banks and building societies in attendance, you’re 5x more likely to meet a bank than at other European Fintech conferences.

This year, to protect the experience, attendance is capped at just 750 complimentary tickets for banks and building societies, and limited sponsorship opportunities are available on a first-come first-served basis.

Visit the links below to learn more.

Banks & Building Societies Apply to Attend for Free: https://hubs.ly/Q03_lXt10

Sponsorship Enquiries: https://hubs.ly/Q03_lYm90

Why Upskilling can’t wait: Building Smarter Skills for a Smarter Financial Future

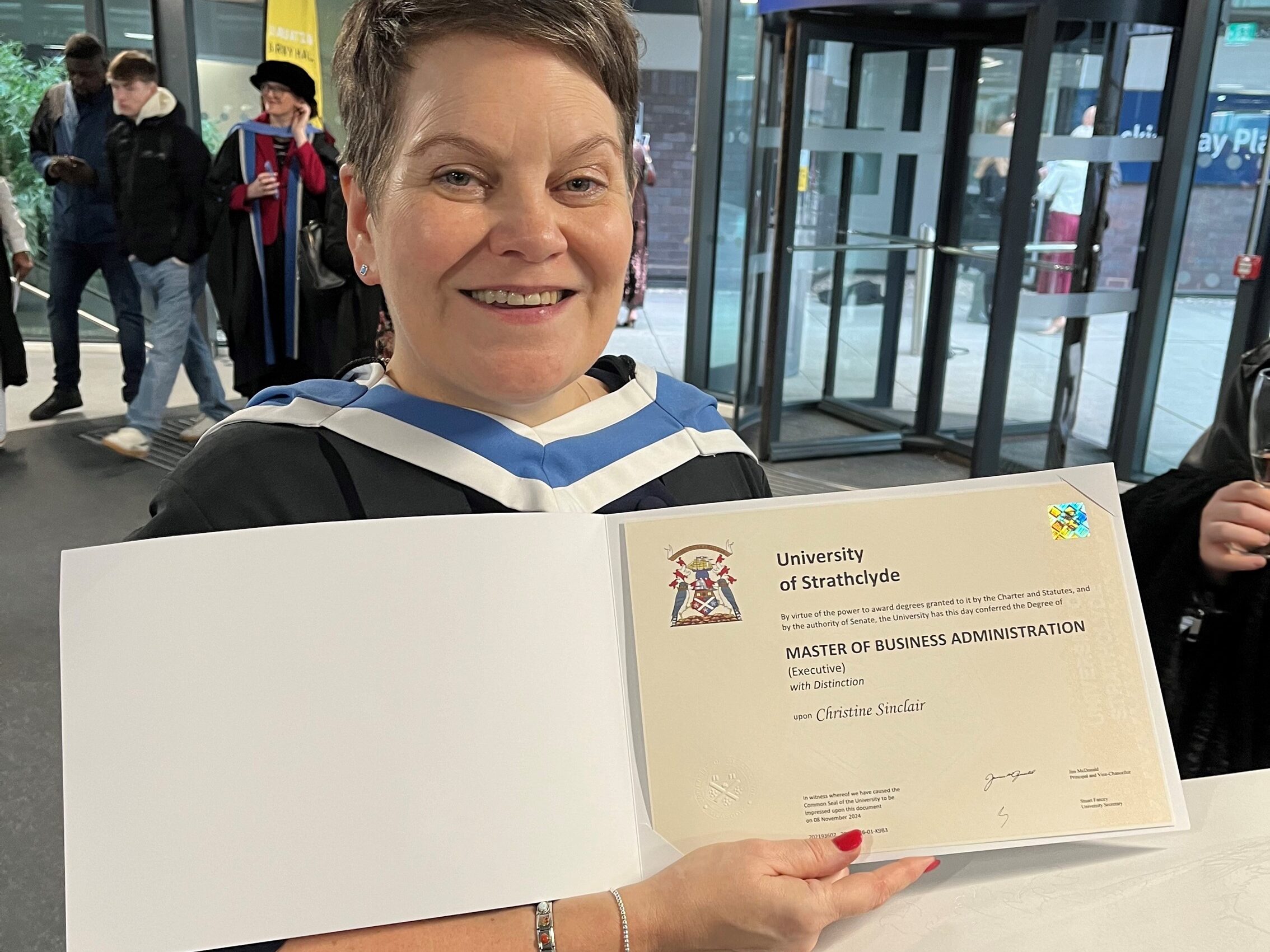

Q&A With Christine Sinclair

Programme Director, Financial Regulation Innovation Lab (FRIL), University of Strathclyde

Financial services is undergoing one of the most significant periods of change in decades. Technology is advancing at pace, new regulations are emerging, and organisations of every size are wrestling with the skills needed to keep up. The Financial Regulation Innovation Lab (FRIL) was created as a catalyst to help the sector respond, to support better outcomes for consumers, strengthen the industry, and enable fintech entrepreneurs to innovate with confidence.

Central to this mission is a progressive skills development programme delivered in partnership with the University of Strathclyde and the University of Glasgow. Together, they’re building a portfolio of Microcredentials (which gain academic credits), short courses and executive education that help people across financial services understand, adopt and apply new technologies responsibly and effectively.

Christine Sinclair, Programme Director, FRIL, University of Strathclyde

Here, Christine Sinclair, Programme Director for FRIL, explains why this work matters, and why now is the time to invest in the future skills of the sector.

Q 1 – Hello Christine, let’s start with the big questions first… what challenge are you addressing here, and why does this matter?

A 1- When you look across financial services, the message is the same everywhere: the pace of technological change is relentless, and people and industry need to keep up. The biggest example right now is generative AI. There’s a real desire to understand it, but also a lot of uncertainty.

When you look at the evidence around AI adoption, the barriers are strikingly consistent. Many organisations hold back because they don’t have the skills or confidence to implement it safely. They don’t fully understand the risks, or they’re concerned about data management and governance. A lot of this is driven by the hype cycle, which can be overwhelming.

So the challenge we’re addressing is simple but vital: helping people develop the skills they need to adopt new technologies responsibly, whether that’s AI, data, digital transformation or ESG reporting. And what we’re doing is demand-led, we’re not creating courses and hoping people want them. We’re listening closely to what financial services and fintechs tell us they need.

Interestingly, the needs differ. Fintechs tend to be highly technical but often need more support with leadership, negotiation and change management. Larger financial institutions have deep organisational knowledge, but they often need help with the technical understanding. So it’s about supporting both sides, and helping both work together…

…and it’s all really important because with the speed of change, the biggest risk is to do nothing.

Q 2 – Who are the courses for?

A 2 – They’re for anyone in financial services, from credit unions to fintechs and large institutions to board-level executives.

A lot of participants join because they want to refresh their own skills. Others are sent by employers who know they need to build capability quickly. And we’re seeing more early-career professionals who want to understand the fundamentals of digital transformation or AI as they move into new roles.

What’s important is that the courses meet people where they are. You don’t need a technical background. You just need curiosity and a willingness to learn.

As a result of the success of the programmes developed for financial services, we’ve also welcomed people from energy and health sectors where the challenges are very similar.

Q 3 – What’s unique about this particular skills offering?

A 3 – The comprehensiveness. There are plenty of short “how to prompt engineer” or “what is GenAI” sessions out there, but they tend to cover only one slice of the picture. FRIL’s courses build from fundamentals all the way through to practical application in financial services.

For example, our AI microcredentials are designed to allow learners to understand and engage with AI in a structured and progressive manner. Focussing on core concepts and techniques, such as machine learning and large language models, but also, cover risk, governance and data science, and communication skills, whilst including real industry use cases which demonstrate practical application. For executives, we even include topics such as decision-making through AI driving business insights in the boardroom, AI Governance and compliance, as well as AI in Enterprise Risk Management and developing strategies to implement and scale GenAI.

Everything is designed to be flexible and accessible. You can learn in your own time, supported by lecturers who track your engagement and are available when you need help. It’s comprehensive without being overwhelming.

Q 4 – What kind of courses are currently being offered?

A 5 – We’ve developed microcredentials in Digital Transformation, ESG for Executives, and a full AI literacy suite, from beginner to advanced, plus an executive-level course. And there are programmes in AI & RegTech, and ESG Leadership.

We originally planned to deliver two microcredentials. We’ve delivered ten due to demand. Seven at Strathclyde, two at Glasgow, and one short course through the UK Government’s Help to Grow programme at Strathclyde. Our microcredentials are accredited and can stack towards a postgraduate qualification, so learners build credits over time.

For those who don’t wish to earn credits, we are now looking at awarding digital badges so learners can showcase their acquired skills on LinkedIn or their CV.

Q 5 – What format do the courses take?

A 5 – In general, course delivery is blended. Each week, participants complete short online lectures, which are no more than 15 minutes each. This, along with reading and other practical activities helps them apply what they’ve learned and typically brings the total up to around two to three hours per week.

We run online inductions, drop-in webinars and a final in-person consolidation session on campus. That’s where the learning community really comes together. Everyone arrives with the same foundation and can share what’s worked in their own organisations.

Our blended delivery provides a safe space to learn at your own pace and without judgement.

Q 6 – Can you share a story of someone who’s been on a course, and the impact it’s had?

A 6 – One participant told us he’d never been to college or university. He came straight into work and never had the opportunity to study formally. He was the first person in his family to ever take a university course, and it was our Digital Transformation programme.

Something clicked for him. After completing the course, he asked what else he could do. He’s now enrolled on a graduate apprenticeship degree. Another participant has gone on to apply for an MBA. So these short courses aren’t just about skills, they can genuinely spark lifelong learning.

Short courses are powerful…they can change the course of someone’s career.

Q 7 – How does FRIL create the ‘engine’ that drives these skills programmes?

A 7 – Our skills work is tightly linked to the Research and Innovation strands of FRIL. The research teams produce white papers, and we analyse common themes. We attend FRIL’s Innovation Calls, listening to pitches from fintechs proposing solutions to challenges highlighted by industry partners. That’s where you hear the real issues, things like: AI, data, legacy systems, regulatory change.

We also have a skills subgroup with finance industry representatives who act as a sounding board and help us to shape course priorities. Everything is demand-led, grounded in industry conversations, networking and skills gap analysis. We’re supporting a sector that contributes hugely to Scotland’s economy, and we want to get this right.

We’re not just creating courses, we’re listening to what the sector is telling us it needs.

Q 8 – How can what we’re doing here influence learnings across other sectors?

A 8 – While the focus here is financial services, the content isn’t always sector-specific, which means we can swap out case studies to fit different industries. We’re already seeing learners from energy and health joining our courses. Because the pace of change is constant everywhere, the need for digital and AI literacy applies just as much outside financial services.

And the short video-based model means we can keep content fresh. If something changes in AI, which it does daily, we can re-record a section quickly.

Q 9 – While this might be our final question today, this really is just the beginning. What might we expect to come?

A 9 Visibility is a big focus. We’re launching the FRIL Skills Academy, which brings everything together including upskilling, reskilling, executive education, and early-career engagement. It will guide people through learning pathways based on their needs, offer microcredentials, and connect with the student FinTech societies across Strathclyde and Glasgow. There will also be the opportunity to engage with either University to gain support for projects, knowledge transfer partnerships and PhD@Work.

Longer term, we want to work more closely with colleges to support talent pipelines, widen access and create opportunities for people who wouldn’t normally enter higher education. We’re also exploring mentoring programmes, internships guest lectures and masterclasses.

This is about us all embracing the future together. When you engage with the universities through FRIL you’re part of a learning community for the long term.

What next?

If you’d like to find out more about FRIL’s skills programmes, please visit:

- Financial Regulation Innovation Lab (FRIL) – Skills development.

- 10‑credit Online Microcredentials from the University of Glasgow.

The FRIL Skills Academy will be launched at the end of January 2026.

About FRIL

Creating Fairer Financial Futures

Advice Guidance Boundary Review Innovation Call

The Financial Regulation Innovation Lab (FRIL) launched its latest Innovation Call last week, which addresses one of the most important regulatory shifts in financial services and could reshape how millions of people access financial support.

The call is all about finding new ways to help consumers make informed financial decisions, delivering more accessible and tailored support while staying within evolving regulatory expectations.

The call focusses on the FCA’s Advice Guidance Boundary Review – a technical name for a very human issue: how to make financial help clearer, fairer and available to far more people.

To understand what all this means – and how it connects to creating a fairer financial future – we spoke with Kostas Oikonomakos, Programme Manager at the Financial Regulation Innovation Lab (FRIL), ahead of last week’s launch of the Innovation Call.

In Conversation with Kostas Oikonomakos

Hi Kostas!

Q: OK, let’s start with what is the Advice Guidance Boundary Review, and why does it matter?

Kostas: The AGBR is a really important development for the financial services industry. Right now, millions of people in the UK don’t receive any financial advice at all. Advice exists, of course, but it’s often too expensive for most people. The Review aims to make sure those people can finally get some form of support to help them make important decisions about their money.

Just 9% of UK adults took financial advice in the year leading up to 2022. While 64% hadn’t in five years. This highlights an ‘advice gap’ affecting an estimated 12 million people identified as non-advised but with need or potential.

*Stats from FCA’s 2022 Financial Lives Survey and the Financial Services Scheme.

It’s also good for firms. It gives them new ways to deliver support that is practical and can scale. And it brings clarity. Today, there are grey areas where a firm thinks they’re offering guidance, but the FCA might say it’s actually advice. AGBR will help define what is advice, what is guidance, and how new services like ‘targeted support’ and ‘simplified advice’ fit in. That clarity will help the whole financial system work better for everyone.

Q: Why does this matter to our everyday lives?

Kostas: The gap is real. The wealthy can afford advice, but millions of people don’t receive any support at all, so they have to navigate pensions, savings, and long-term planning by themselves. New types of guided support can help close that gap and improve confidence and outcomes for people who’ve never had access to anything before.

Q: At what points in our lives would we feel the difference created by AGBR, and how would it change the way we access advice or guidance?

Kostas: You’d notice it would make financial decisions easier. For example, when you’re getting close to retirement and need to understand your pension options, but you can’t afford full advice. With developments from AGBR, you could use a digital service that gives you targeted support based on the information you share, helping you make decisions with much more confidence. The same applies if you have a few small pension pots from different employers and don’t know how they fit together. Guided tools can help you navigate that without needing a one-to-one adviser.

You’d also see the difference much earlier in life. Let’s say you have a small amount of savings and you’re trying to work out how to make it grow, or you’re deciding whether to pay off debt or put money into a pension. Right now, most people in that situation get no support at all. New ‘advice-lite’ services would give clearer, personalised guidance at a price people can actually access. And in time, as open finance develops, firms could safely build a fuller picture of your financial situation and offer even more accurate guidance without you having to pull everything together yourself.

Q: What is the main challenge that the FCA is trying to address?

Kostas: The main challenge the FCA and HM Treasury are trying to solve through the AGBR is that too few people are getting the financial support they need. There are lots of people who could really benefit from help but don’t get it – that is the advice gap. Part of the problem is that firms aren’t always sure where the line sits between regulated advice and general guidance. The Review should clear up that uncertainty and create space for new, more affordable ways to help people, like Targeted Support and Simplified Advice, so that many more consumers can get the right help at the right time.

Q: What is the difference between advice and guidance?

Kostas: Advice is the traditional, regulated service where an adviser understands your full financial picture and gives you a personalised recommendation. It’s tailored to you and your long-term goals, and the firm takes responsibility for that recommendation. Guidance is different. It doesn’t look at your whole situation and it doesn’t tell you exactly what to do. Instead, it helps point you in the right direction based on the information you choose to share. It supports your decision, but it’s not a personalised recommendation.

Q: Why is FRIL taking on this topic right now, and what does it hope to achieve?

Kostas: The timing is ideal because the AGBR framework is still being developed. Final rules are expected by the end of 2025, with firms able to apply for the new targeted-support regime from Spring 2026. That means there’s still an opportunity to feed in insights before anything becomes enforceable.

This creates a safe space for firms to share challenges and explore potential solutions without regulatory pressure. Through this work, we can generate early evidence and practical ideas to help shape how the new regime operates in practice.

The kinds of ideas we expect to explore include digital tools for targeted support, simpler ‘advice-lite’ journeys, interactive disclosures, and even early work on open finance so firms can safely access a fuller picture of a customer’s finances. The goal is to produce practical, testable solutions that show how AGBR could work in the real world, to prepare for tomorrow and to improve outcomes for people who currently receive no support at all.

Q: Why is FRIL a good environment to help shape developments?

Kostas: More broadly, what FRIL wants to achieve is genuine collaboration around real problems. Large firms get early sight of new technologies and ideas that could help them support customers at scale. Fintechs get a clear understanding of what those firms actually need, and they can adjust or sharpen their solutions accordingly. The FCA is part of those conversations too, which is helpful for any fintech that might want to become regulated in future. And our academic partners bring research and analytical thinking that helps everyone look at these issues from different angles.

Q: OK quick summary – how does this help create a fairer financial future?

Kostas: By widening access. More people get the right kind of help, firms can serve broader audiences, and the rules are clearer. That combination improves confidence, access to financial advice and guidance, and ultimately, better outcomes for everyone.

Explaining the terminology

The Advice Guidance Boundary Review. Just what does it mean? A brief glossary:

- Advice: A regulated service where a financial adviser looks at your full financial situation and gives you a personalised recommendation.

- Guidance: Support that points you in the right direction based on limited information you share, without telling you exactly what to do.

- Boundary: The line that separates advice from guidance, defining how much information is needed and what a firm can or can’t recommend.

- Review: The FCA’s process of consulting industry and consumers, and government to create clear new rules that will shape how these services work in future.

What next?

Over the coming weeks, FRIL will be exploring new technologies, fresh thinking and real-world challenges with partners across the ecosystem. Watch this space for insights and thought leadership content from across the call – there’s much more to come.

Email the team at FRIL@fintechscotland.com if you’d like more information about our Innovation Calls.

About FRIL

Financial Regulation Innovation Lab (FRIL) Responsible Innovation Case Study: Encompass

FRIL: Accelerating the Fight Against Financial Crime

Financial crime might sound distant, something that happens behind the scenes in big institutions, but its impact is personal. It can touch anyone. From identity theft to money laundering, these crimes erode trust and cost billions every year.

That’s why FRIL launched its Financial Crime Innovation Call: a challenge designed to find, fund, and fast-track groundbreaking technology that helps financial institutions stay ahead of criminals.

For Encompass, an international company with roots in Glasgow, this was more than just a competition. It was an opportunity to showcase their expertise, build new partnerships, and accelerate innovation.

By taking part, Encompass gained direct access to global tier-one banks, opened up new commercial opportunities, and fast-tracked the development of new product capabilities. For a company already at the forefront of financial crime prevention, FRIL’s challenge acted as a powerful accelerator, connecting ambition with action.

The Challenge: Fighting Financial Crime Head-On

Fraud and financial crime affect everyone: individuals, businesses, and entire economies. Criminals find new ways to exploit the system every day, while financial institutions face the ongoing challenge of keeping up. The stakes are high: in 2023 alone, global banks were fined billions for failing to prevent fraudulent activity.

Complying with regulations is essential, but it comes at a cost: around £38 billion in the UK that same year. And as technology evolves, so do the tools of both criminals and those working to stop them.

One of the biggest hurdles? Disconnected data.

When information is trapped in separate systems (within or between organisations), it becomes harder to spot suspicious behaviour and act quickly.

Why tackling this challenge matters:

| For Industry | For Consumers |

| Preventing financial crime isn’t just about avoiding fines – it’s about protecting customers, building trust, and reducing operational and regulatory risks. | Strong financial crime prevention means safer transactions, fewer victims, and the confidence that their personal data and money are secure. |

When the system works better, everyone benefits.

FRIL’s Approach: Innovation in Action

To tackle this complex problem, FRIL’s Financial Crime Innovation Call set out five specific challenges. Each focused on a critical question:

- How can technology and data help us understand and detect financial crime faster?

- How can we make identity verification more secure and efficient?

- Could smarter data sharing between institutions improve outcomes?

- How can we enhance fraud response systems in real time?

- And what can we do to future-proof these systems against new risks?

Rather than solving these questions in isolation, FRIL brought together innovators, major financial institutions, regulators, and data experts to collaborate directly.

This unique setup, combining early-stage funding with direct access to decision-makers, gave companies like Encompass the chance to test, refine, and rapidly advance their solutions in a real-world environment.

The Case Study – Encompass

Encompass, a global company headquartered in Glasgow is celebrating ten years in the city. The corporate digital identity firm continues to expand in Glasgow, and has recently signed a ten-year lease on a new premises. Encompass joined FRIL’s Innovation Call on Financial Crime in January 2025. This is their story of their experience with FRIL.

“What we’ve ended up with in three months, is three real commercial opportunities that would have easily taken us twice or three times that long if we had not had the backing of FRIL and that structure”.

— Howard Wimpory, Director of Transformation, Encompass.

“FRIL has been an exceptional support and catalyst in helping Encompass expand our network and presence in Glasgow. We have benefited from valuable insights and interactions from the market that will fuel our ongoing innovation”.

— Alex Ford, Chief Revenue Officer, Encompass.

About Encompass

Encompass has been fighting financial crime since 2011. Founded in response to a personal experience with fraud, Encompass helps the largest global financial institutions understand exactly who they’re doing business with by revealing the true owners and controllers behind corporate clients.

Watch the video to see how EC360, Encompass’s Corporate Digital Identity (CDI) platform, works in practice.

“The reason that we do this is to identify whether they’ve ever been sanctioned for crime, so that those bad actors are excluded from running companies and accessing the world’s commercial financial institutions”.

— explains Howard.

“Our solution creates a consistent and reliable outcome every time, and we do it in a faster way than any human can do. So for a human to do the job that our platform does could take three or four days – what we could do in ten minutes”.

— adds Howard about the Encompass solution.

Encompass stats

| Sector | Fintech |

| Employees | 130 (46 in Glasgow) |

| Turnover | UK, US, Netherlands |

| Location | Glasgow / London |

The Ambition – Growth and Vision

Encompass joined the Financial Crime Innovation Call because they wanted to explore how their existing corporate identity platform could develop to benefit financial institutions.

“Glasgow offers a collaborative ecosystem of fintechs, financial institutions and tech talent emerging from leading universities”.

— explains Alex.

There were two key specific areas the Innovation Call helped Encompass explore that were key to the company’s growth and vision:

| To work directly with industry to hone products and services | To build relationships with clients, and others in the financial ecosystem |

| In this case, Encompass were interested in developing their future ambitions around ‘Know Your Customer’ processes, which are mandatory processes to verify the identity of clients to prevent financial crime and comply with regulations. | The collaboration brought Encompass closer to potential new clients while also offering an opportunity to build confidence within industry in the value of buying from trusted FinTechs who offer tried and tested solutions. |

The Outcomes – Impact

For Encompass, FRIL’s challenge wasn’t just a networking exercise: it was a catalyst. The collaboration helped them build stronger industry connections, speed up product development, and unlock commercial opportunities with global banks.

For FRIL, it was proof that innovation and regulation can move faster together, creating real progress in the fight against financial crime. Because when data connects, people are protected. And when innovators are empowered, financial systems become safer for all.

“We’ve made direct new commercial relationships with at least two Scottish based financial services firms. And we’ve got involved with a parallel organisation based in the West Midlands focused on legal

firms. Through the backing of FRIL, we achieved in three months what would normally take 18 months”.

— explains Howard.

Impact summary

- New commercial relationships developed.

- Expanded network.

- Acceleration of average ‘contact to client’ development time reduced from average of 18 months to three.

- Relationships developed with other members, leading to events in New York and London, expanding connections and brand.

Next steps – Watch this space for:

- Emerging deals with interested clients.

- Accelerated product development to support financial institutions in tackling financial crime.

“We’re excited to continue our journey in Glasgow, and look forward to leveraging this well-connected community to fuel our growth globally”.

— concludes Alex.

Download the Encompass case study.

About FRIL

MoneyMatix to Curate First-Ever “Money Village” at Ideal Home Show Scotland 2026

Financial education will be one of the key themes at next year’s Ideal Home Show Scotland thanks to an exciting new initiative led by Scottish fintech MoneyMatix.

In May 2026, the consumer show (now in its 74th year), will launch a dedicated “Money Village”, designed to give thousands of visitors the financial tools, knowledge, and advice they’ve been asking for.

Demand for practical, trustworthy financial guidance has never been greater. Visitors to the show have repeatedly highlighted the need for more help navigating the ongoing cost-of-living crisis, from everyday budgeting through to pensions, investing and planning.

MoneyMatix Advice Stage, curated and hosted by MoneyMatix, will bring together Scotland’s leading financial voices alongside top UK experts. Across the four-day event, attendees will be able to take part in engaging talks, masterclasses and fireside discussions covering the full spectrum of money matters (planning and tax to savings, mortgages, insurance, pensions and family finances

Tynah Matembe, founder at MoneyMatix said:

“Our mission has always been to make financial education accessible and engaging,” Tynah said. “The Money Village will give thousands of people the chance to learn, ask questions, and leave the show with actionable knowledge that can make a real difference in their lives.”

With over 31,000 attendees expected at the Ideal Home Show Scotland, the Money Village also offers a powerful new platform for the financial services industry to connect directly with consumers. Exhibitors will benefit from a carefully curated environment with limited competition per category, as well as the opportunity to book one-to-one consultations with visitors.

The Ideal Home Show Scotland 2026 takes place between 22–25 May 2026 at the SEC, Glasgow.

Scottish Fintech Guiide Launch of First-of-its-Kind Retirement Support Tool

A new solution is helping people take greater control of their retirement planning and it has Scottish fintech innovation at its heart.

Pathlines, in collaboration with Scottish fintech Guiide and global investment firm Invesco, has launched a first-of-its-kind tool offering guided support for non-advised defined contribution (DC) pension savers. The new self-service platform allows users to manage their pension drawdowns with greater confidence, building on Guiide’s holistic planning technology that has already been helping individuals navigate complex retirement decisions for over three years.

Initially available to anyone over 50 who is not yet drawing their pension, the tool enables savers to create a sustainable plan within Guiide, consolidate their pots with Pathlines, and link their cashflow projections to real pension accounts. The system then allows them to review and adjust their plan each year, offering an intuitive and dynamic way to stay on track with their long-term financial goals.

The partnership demonstrates the power of collaboration between fintech innovators and established financial institutions to deliver solutions that bridge the gap between advice and guidance, a key focus of ongoing regulatory and industry discussions.

Christine Hallett, CEO at Pathlines Pensions, said:

“Pathlines is centred on helping individuals take control of their financial future by empowering them to shape their own path to retirement. We’re proud to partner with Guiide and Invesco to deliver this innovative solution for those at the very beginning of their retirement journey.”

Guiide Chairman, Ruston Smith, added:

“Our goal is to make sustainable retirement plans a reality as simply as possible for the non-advised. We hope this new tool will help reduce the risks of drawdown for many savers.”

Georgina Taylor, Invesco’s EMEA Head of Client Investment Solutions, noted that decumulation — the process of managing and drawing down pension savings — is a core strategic priority for the firm, adding:

“Cashflow planning tools such as Guiide play a critical role in ensuring there’s a robust retirement platform for everyone, regardless of how they choose to access their savings.”

Supporting Innovation in Financial Guidance

This launch comes as FinTech Scotland, through the Financial Regulation Innovation Lab (FRIL), recently announced a UK-wide innovation challenge on the Advice-Guidance Boundary Review in partnership with leading financial institutions. The initiative invites fintech innovators to co-create next-generation solutions that make it easier for consumers to access the right kind of support at the right time, exactly the kind of practical innovation exemplified by Guiide and its partners.

Addressing tomorrow’s pressing challenges, today: Operational Resilience Innovation Call launches

“We expect to be able to withdraw cash from the cash machine. We expect to be able to see that our salaries have hit our bank account – to have things available in the palm of our hands.”

But what happens when known or unknown threats – such as wars, climate change or cyber attacks – challenge the delivery of our financial services?

That is why Operational Resilience continues to be a top regulatory priority for the financial and professional services sector.

It’s also why the subject is the focus of Financial Regulation Innovation Lab (FRIL)’s most recent Innovation Call, launched last month. Bringing together leading minds from across the fintech and financial services sectors, regulators and academia, we are tackling some of the most pressing challenges to create solutions for the future.

Pioneering solutions for customers and financial services

“It’s about getting ahead of the game. The big thing about operational resilience is that it asks organisations to think beyond what they’ve experienced before and try to design for how they might respond to scenarios that they haven’t already planned for.”

Rob Mossop, Chief Operating Officer, Sword Group

This Innovation Call sees 15 cutting-edge fintech businesses selected to collaborate directly with leading financial institutions, professional services firms, and academics to design practical solutions that build resilience across the sector.

“It’s about partnering and working closely together to develop outcomes and solutions that work for the best for those banks or investment managers.”

Simba Mamboininga, CEO and founder of Devlin Mambo

This is our fifth Innovation Call and will address challenges affecting the sector including:

- strengthening supply chain monitoring

- improving data quality

- addressing cross-border compliance

- advancing scenario planning

- fostering resilient cultures

- managing risks across cloud and hybrid environments.

“Creating those solutions, bringing deep knowledge and pouring thinking into products and services which can help firms deal with issues around resilience.”

Shriparna Kosh, partner at EY.

Launch and Next Steps

The programme officially launched on 26 August at Sword’s Glasgow offices, where the fintechs met with industry leaders and academic experts to kick-start their collaborative journeys.

View the kick‑off event brochure.

Watch the recording from the day below.

Over the coming weeks, participants will take part in workshops and deep dive insight sessions designed to refine their solutions and align them with real-world industry needs. The most promising ideas may also receive grants of up to £50,000 to accelerate development.

Who is involved?

The Operational Resilience Call is hosted by the Financial Regulation Innovation Lab in partnership with SuperTech West Midlands.

We are proud to be working with 12 strategic partners – Sword Group, Tesco Bank, Unity Trust Bank, EY, Aberdeen, Morgan Stanley, Pinsent Masons, Dudley Building Society, Tipton Building Society, KPMG, M&G, and NatWest – alongside academic partners at the University of Strathclyde and the University of Glasgow. Their combined expertise ensures that innovation is rooted in both cutting-edge research and real-world regulatory priorities.

“I really relished the opportunity to work alongside industry partners in FRIL, because there was this opportunity to take real life use cases and put academic research around them.”

Steve Owens, Knowledge Exchange Fellow at the University of Strathclyde.

Our 15 successful Fintechs include:

- Argus Pro: Aegis 9™ and NexEdge™ use AI to assess compliance frameworks and detect regulatory gaps.

- Blankstate: Its Consensus AI model and Intention Blended Framework (IBF) reimagine operational excellence by understanding intent, nuance, and context.

- BR-DGE: An independent payments technology hub that boosts resilience by giving merchants and institutions more control over global payment connections.

- Continuity2: A trusted resilience partner for over 20 years, providing SaaS software for business continuity and operational resilience.

- Devlin Mambo: Scalable software that automates supplier governance, compliance monitoring, and reporting.

- DORA.report: A platform built to help firms and providers meet EU DORA reporting obligations.

- FinTrack & FinPay: Secure cash logistics and a unified resilience platform for crisis simulations, dependency mapping, and regulator-ready evidence.

- HAELO: IO® uses AI to map requirements to obligations and controls, helping firms simulate and act on operational risks.

- ICEFLO: A ServiceNow-native runbook management platform for rehearsing and executing complex recovery scenarios.

- Ionburst: Unified secure hybrid-Cloud solutions that deliver compliance-ready, auditable data protection

- Jellifysh: Application security platform tackling software supply chain vulnerabilities.

- Lupovis: Real-time cyber threat intelligence powered by network decoys.

- Profylr: Information Genetics® engine that connects regulatory requirements to data, creating transparent compliance blueprints.

- SENGUARD: Shifts resilience strategies from reactive to preventive with threat intelligence.

- TEXpert AI: GenAI-powered risk extraction from unstructured data to surface hidden risks in portfolios and supply chains.

What next?

If you’ve liked what you’ve read, follow us on LinkedIn for the latest updates. For more information about getting involved in future innovation calls, email FRIL@fintechscotland.com