Atos UK&I joins FinTech Scotland as Strategic Partner to accelerate AI‑led fintech innovation and growth

FinTech Scotland today announced that Atos, a global leader of AI-powered digital transformation, has joined the Scottish fintech cluster as a Technology Strategic Partner, strengthening the cluster’s ability to drive collaborative innovation and growth.

Atos brings global scale with a strong UK presence to help create the conditions for faster innovation, secure scaling and economic impact across Scotland’s fintech community. Experts in Agentic AI, digital sovereignty and cybersecurity with a 60,000‑strong team worldwide, Atos provides end‑to‑end digital expertise across consulting, infrastructure, operations and optimisation, as well as integrated services across cloud, application services, smart platforms and the digital workplace.

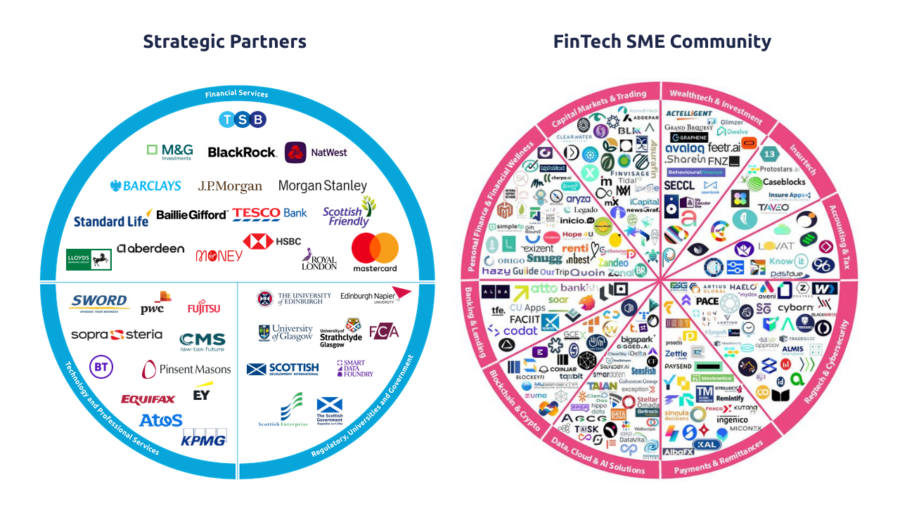

This partnership strengthens the cluster’s momentum and the shared commitment to collaborative innovation that will shape the future of next-generation financial services. It takes our network to 37 Strategic Partners, building a world-class environment for fintech innovation and regional growth, at a time when Scotland’s fintech cluster has more than doubled in five years, from just over 120 firms in 2020 to more than 260 today, reinforcing its position as one of Europe’s most dynamic and collaborative fintech clusters.

Aleks Tomczyk, Chief Executive at FinTech Scotland, said: “This partnership with Atos strengthens our shared commitment to fostering innovation, collaboration and growth across Scotland’s fintech cluster. By bringing deep expertise in AI, data, secure cloud and digital platforms, alongside a strong global presence, Atos will enhance the support available to fintechs as they develop new solutions and build resilience, contributing to Scotland’s economic and societal progress.”

Simon Chandler, Head of Financial Services and Insurance, UK & Ireland at Atos said: “Atos is delighted to join FinTech Scotland to cement our investment in Financial Services in Scotland. We are excited to work in collaboration with the; FinTech SME community, Financial Services organisations, regulators, universities, and government by leveraging our leading Sovereign Agentic AI, Data, cloud and digital global expertise, underpinned by our unique Sustainability and Social Value commitments. We aim to drive Shared Value success for every part of this community to the betterment of this community and Scotland as a whole.”

Every Life Moment Is a Money Moment

By Dia Banerji, Founder and CEO, Cherpa.ai

Separation. Redundancy. Having a baby. Losing a parent. Caring for an ageing relative. Retiring.

Every one of these moments comes with money questions. And for most people, those questions arrive at exactly the wrong time, when you are stressed, stretched, and trying to hold the rest of life together.

In some ways, I have been trying to make money simpler for people my whole career. I spent over 20 years in financial services, building products, shaping propositions, and working with customers at scale. I saw the best of what our industry can do, and I also saw a pattern that kept repeating.

The people who need help most are often the least likely to get it.

Not because they are not capable. Not because they are not trying. But because the industry still expects people to work out what they need, hunt it down across multiple sources, and then stitch it together for themselves, translating generic education into decisions that make sense for their own lives, often in the very moments they have the least capacity to do so.

The problem is not knowledge, it is design

Financial services impact everyone and it should work for everyone.

Yet the experience most people have is fragmented and exhausting. One app for budgeting. Another for savings. Another for pensions. Another for benefits. Another for insurance. Each tool does something useful in isolation, but real life does not arrive in neat categories.

If you are going through a separation, you might need to rethink your mortgage, update your pension beneficiary, understand what help exists for short term bills, and decide what to tackle first. Those are connected questions, but our tools split them into separate journeys, leaving the person to join the dots. We assume information equals empowerment. Too often it is just cognitive load, and when life is already full, it becomes disengagement rather than better decisions.

The same is true for financial education. The industry has invested heavily in it, and rightly so, but it is usually delivered at a distance from real life, generic, broad, and rarely anchored to the moment someone is actually living through. It tells you what people like you should think about, not what it means for you, right now, in your specific situation.

And if the choice is between a webinar on pension consolidation and the next season of Bridgerton, I know which one I am choosing, and I have worked in pension!

People do not need more content. They need clarity.

The advice gap, and the missing middle

There is another layer to this. Regulated advice is essential for big, complex decisions. But most everyday money questions are not asking for a product recommendation. They are asking for direction, options, and reassurance.

People want to know things like:

- What support can I access right now

- What should I change first

- What am I missing

- What is the “obvious” thing that everyone else seems to know

Often the most valuable intervention is not a recommendation. It is connecting the dots.

Before we built anything, we surveyed people about money confidence. Nine in ten told us they could improve. Many said they feel anxious just thinking about their finances. A meaningful number said they do not seek help from anyone at all. And the words people used stuck with me:

“I don’t need a PhD in financial products. Just tell me what’s relevant to me.”

“My budgeting app shames me for buying a coffee. Too many apps, too little help.”

“Make me feel safe asking stupid questions.”

That last line matters more than it seems. Because the real barrier is often emotional. Shame, fear of getting it wrong, fear of being judged, fear of being sold to, fear of admitting you do not understand.

What should the future feel like

I believe we are entering a new era of financial support. One where the default experience is not search, not generic content, and not a cold handoff into a process designed for specialists.

The future should feel more like this:

One front door. A conversation. Your life context. The options that matter to you.

Not to replace regulated advice, and not to turn every question into a product journey. Instead, to help people navigate the messy, human moments where money is involved, which is most moments.

To do that well, three things have to change.

First, we have to start from life moments, not financial categories. Life is the organising system. The tools should follow.

Second, we have to make information genuinely usable. That means connecting it, prioritising it, and presenting it in plain language, with next steps that feel doable.

Third, we have to treat trust and privacy as design requirements, not legal footnotes. Many people are understandably reluctant to share bank data with a new app.

Building a new front door to financial support

Cherpa exists to meet people right where they are. When life changes, money questions do not arrive neatly labelled. They arrive tangled, emotional, and urgent, and yet we still ask people to navigate a maze of tools, terminology, and generic content.

So we are taking a different approach. We start where real life starts, with the moment, not the product. One conversation that helps someone orient quickly, join the dots across the areas that matter, and move from noise to a clear set of options and next steps. The ambition is to create a trusted front door, a place people can begin, without needing to hand over more data than they are comfortable sharing.

That shift, from fear to agency, is the outcome I care about.

Why this is personal

I lost my dad when I was fourteen. I watched my mum try to navigate a financial system that gave her no useful answers during the hardest moment of her life. That memory has never left me.

It is one thing to know, intellectually, that help exists. It is another to live the reality of not being able to find it, understand it, or know what applies to you.

That is why I keep coming back to this belief.

Every life moment is a money moment. And nobody should have to face them alone.

Dia Banerji is the Founder and CEO of Cherpa.ai, based in Edinburgh.

Behind the Scenes at the Skills Academy

“When you look across financial services, the message is the same everywhere: the pace of technological change is relentless, and people and industry need to keep up,” explains Christine Sinclair, Programme Director for FRIL.

And that is exactly what sits behind the FRIL Skills Academy – a pioneering, demand-led, skills and education platform created by the Financial Regulation Innovation Lab (FRIL).

“With the speed of change, the biggest risk is to do nothing,” adds Christine.

The Academy is delivered in partnership between Fintech Scotland and the University of Strathclyde and the University of Glasgow. It is a practical response to real skills gaps identified across the sector from work within FRIL’s Innovation Calls and research.

The academy, which launched officially in January, brings together a portfolio of short courses, microcredentials (which gain academic credits), and executive education that help people across financial services and beyond to understand, adopt and apply new technologies responsibly and effectively.

So, that’s the context. But what are people actually learning at the Academy, and what difference does it make?

Here, we explore the stories of several participants to find out:

Closing the gap, accelerating progress

Professor Mick O’Connor started his working life as an apprentice welder in the Clyde shipyards and is now a serial entrepreneur, academic and managing director of multiple high‑tech businesses spanning regtech, spaceports and drones. When Mick’s regulatory technology firm Haelo won one of FRIL’s first Innovation Calls, he was already building AI-enabled solutions. But as we often find, the more we learn, the more we realise we need to learn.

“I’d never been formally taught AI,” he says. “I’m not a coder. I had an enthusiastic amateur understanding, but I owed it to myself and the business to understand more.”

So, he enrolled in the AI and Regulatory Technology in Financial Compliance microcredential at the University of Glasgow.

“I still wouldn’t describe myself as an AI expert,” he explains. “But I can now talk comfortably with people who are. I can translate the customer problem into user stories, and then into technical requirements.”

And this has helped Mick bring together the business and technical teams required to make the Haelo magic happen.

“We talked different languages. This has helped close that gap,” he explains.

And while the gap may have narrowed, Haelo’s trajectory has accelerated.

“As a direct consequence of FRIL, I developed a technology roadmap. I didn’t have that before. I started with the problems then understood the technology I needed to solve them.”

Haelo is now preparing to launch its first product, designed to be sector-agnostic, capable of pivoting across highly regulated industries including pharma, rail, nuclear, space and aviation.

“I’ve said to FinTech Scotland that this is such a great story,” he reflects. “I can demonstrate that the whole genesis of that product and building the business has been seeded by FRIL.”

Joining the dots between rockets and regulation

“My job is business development,” says Derek Harris. “I need to understand what my clients are doing, especially around satellite launching. These courses helped me have that conversation.”

Derek is Director of Business Development and Communications at Skyrora, which builds small launch vehicles for launching satellites into space.

You might not associate the FRIL Sklls Academy as an enabler for the Space industry but the sectors intersect in surprising ways.

Satellites may orbit the earth, but their impact is grounded in everyday systems: encryption, cybersecurity, data protection, which is also the invisible infrastructure behind banking and digital security.

And similarly, Derek’s career has bridged those two worlds. Before rockets, he spent 15 years in financial services.”

“When it comes to Space and Finance, we have one of the biggest finance areas outside London and Frankfurt. But we also now have a fully forming space industry where the two can work hand in hand.

“So, if we can identify what data is required by financial institutions, these courses can help turn wish lists into actual products,” he explains.

Micro-credentials in AI Implementation and Financial Crime Prevention gave him a structured understanding of how space-enabled data connects with financial regulation and risk.

“These courses helped me fill in the dots,” explains Derek.

And it wasn’t just what was being taught that was helpful, it was the way it was being taught too.

For someone who is dyslexic, the flexible online format was crucial.

“I could go back, relook, learn at my own pace, even while on the go and in between flights. I could jump online and do 30 minutes. That made a huge difference,” explains Derek.

And his biggest surprise about the Academy? “It’s not as well-known as it should be,” says Derek.

“If all the banks were doing this, it would be a game changer. And it’s the customers who would win at the end of the day.”

Confidence to challenge and connect

“The Digital Transformation course brought learning to life with real-world examples, group work and problem-solving,” says Joanne Seagrave, founder of Norwood Risk and Compliance, who offers yet another perspective on the Academy’s impact.

“As a result, I felt empowered to grow my scope within the fintech community, which inspired me to develop my role as a board advisor to start-ups.”

With 25 years in financial services and experience supporting fintechs through FRIL as an industry partner, she joined the course not out of necessity, but curiosity.

“I wanted to take my understanding to a more in-depth level,” she says.

The micro-credentials allowed her to explore business strategy through a technology-led lens, from generative AI to distributed ledger technology, grounding innovation in commercial and regulatory realities.

“The course gave me confidence to be curious,” she explains. “Whether that means challenging compliance teams to use technology more effectively or factoring risk in at the early stages of a project.”

What surprised her most was the diversity of the cohort.

“I’ve worked in financial services for over 25 years, but the community included people from charities, engineering, life sciences, public sector and software development, which made for some interesting discussions and led to diversity of thought,” she explains.

Shaping the future… and your future

So that’s a glimpse behind the scenes of the Academy and the programmes on offer. But let’s leave the final word around its impact to Christine:

“There are so many inspiring stories from people who’ve been through these programmes,” she says. “One participant told us he’d never been to college or university. He went straight into work and never had the opportunity to study formally. He was the first person in his family to take a university course, and it was our Digital Transformation programme.”

“Something clicked for him. After completing the course, he asked what else he could do. He’s now enrolled on a graduate apprenticeship degree. Another participant has gone on to apply for an MBA. So, these short courses aren’t just about skills, they can genuinely spark lifelong learning.”

“Short courses are powerful,” she adds. “They can change the course of someone’s career.”

If you’ve liked what you’ve read and would like to change the course of your career, then please check out the FRIL Skills Academy webpage. Or contact the Skills Team for more information at sbs-fril@strath.ac.uk. They are waiting to hear from you.

About FRIL

Research in Action – How Financial Regulation Innovation Lab (FRIL) Is Turning Insight into Impact for Industry and Consumers

FRIL is turning collaborative research into real-world solutions for the future of financial services – and, in turn, for all of us.

“There’s hardly an organisation you can talk to that isn’t interested in artificial intelligence and cyber security – the opportunities created and the challenges they might face,” explains Professor Eleanor Shaw OBE, Associate Principal External Engagement and Partnerships at the University of Strathclyde.

“As researchers, it’s really important that we use our expertise to explore those challenges with our external partners and find solutions. That’s how we drive impact.”

And the impact Eleanor describes isn’t just for industry; it’s for all of us, in our everyday financial lives.

“Imagine a world where, regardless of your postcode, you can access good-value, high-quality financial products: mortgages, insurance, advice and guidance. That’s the world we’re working towards at FRIL,” adds Eleanor.

Speak to almost anyone in financial services right now – just like many sectors – and you’ll hear the same underlying tension: the future is arriving faster than most organisations can comfortably absorb.

Technology and consumers. Opportunity and risk. Acceleration and anxiety. The list of modern paradoxes keeps growing. It’s enough to raise the pulse slightly.

That’s why addressing those challenges is at the core of the research undertaken by FRIL. This research is not theory alone. It is applied, fast-moving, tested, and shaped alongside industry and regulators – with real-world consequences in mind. Consequences that mean faster solutions for consumers, greater innovation capacity for banks, and new skills development programmes designed for the next generation of financial services.

“There’s a magic formula at the heart of FRIL, which is why we see the results we do. Actionable research is one of four key ingredients. The others are our Innovation Calls, Knowledge Exchange and Skills and Education programmes. Together, they drive impact and get solutions out into industry quickly,” explains Clare Reid, Strategic Innovation Director at FinTech Scotland. “Our partnerships with the Universities of Glasgow and Strathclyde are really important in driving research that shapes positive outcomes.”

Preparing for the future now

So, how does this actionable research actually work? Mark Cummins, Professor of Financial Technology and Lead Investigator at the University of Strathclyde, explains:

“At the University of Strathclyde translation of research has always been a key focus. We work in fundamental research and publications are critical – they build credibility, but we also work hard to translate that research into impact.

“At the University of Strathclyde, for example, we use cluster mechanisms to coordinate expertise across different areas. I lead our FinTech cluster, and those clusters are a key way of translating research for real-world impact.

“What FRIL brings is a mechanism for bringing all the stakeholders into one room: financial services, professional services, fintechs, regulators and others. That coordination gives us a reach that can be difficult to replicate in other ways.”

And that connection to industry and regulators is key:

“We draw on our academic knowledge to deliver applied research set by companies and regulators, and connect that directly to skills development and real industry challenges,” adds John Finch, Professor of Marketing at the Adam Smith Business School at the University of Glasgow and another Lead Investigator for FRIL.

FRIL research starts with real, live problems ranging from consumer vulnerability to operational resilience. The research activities bring banks, fintechs, regulators, and technology firms together to turn those challenges into direct, applied research built for a rapidly moving environment and evolving consumer needs. And it is a model that is appealing to action orientated academics.

“One of the key reasons I came back to academia was the chance to work on these white papers with industry,” says Steve Owens, a knowledge exchange fellow at the University of Strathclyde, and an engineer by trade. “We take real use cases and put academic research around them, then get that knowledge back out quickly. The focus is on getting useful insight into industry hands as quickly as possible.”

That research is increasingly boundary-pushing, and spans explainable AI, multi-modal generative AI, earth intelligence using satellite data, and agentic systems, but always tied back to regulatory and market needs.

The FRIL research model blends open and applied innovation. White papers are published openly so the wider sector can benefit.

Meeting needs

For banks, this means the research environment that FRIL offers becomes a home for strategic insights.

“We’re an insight-led team,” explains Nicole Alston, Programmes and Community Engagement Manager from Natwest. “FRIL gives us visibility across disruptive technologies and emerging sectors. We know we can’t build everything internally and that this is a two-way exchange.”

And that two-way exchange is critical, because at the centre of this high-tech research, is a clear purpose to tackle very human needs.

“If we apply technology correctly in financial services, we can drive greater inclusion and economic prosperity,” Eleanor reminds us.

Consumer vulnerability and consumer duty are recurring themes across FRIL research, but all of these areas are deeply nuanced where ‘one-size-fits-all’ solutions won’t cater for the needs of all those in society. John helps explain:

“Vulnerability isn’t always permanent; it can be linked to life stage and personal circumstances. Insights from firms who see this day to day often reshape how and where we focus our research.”

Those insights are increasingly being translated into practical tools, and Advanced AI research is being applied directly to consumer outcomes.

But what does all of that actually mean? Well, just a few of those examples include identifying potential discrimination in financial decision-making, bringing financial advice and guidance to the masses rather than the few, and building voice-led digital interfaces that help people with reading or learning difficulties access support more easily. This is work that matters for everyday people.

And for technology partners, the value lies in bringing together the academic rigour with market urgency.

“We take hypotheses from industry challenges and shape them into structured research with academic partners,” says John Donoghue, Chief Technology Officer at Sopra Steria, a major tech firm with over 50,000 employees worldwide.

Students are embedded too – through live projects, dissertations, and industry-defined challenges, with the aim of building future skills alongside present solutions

“Students and researchers test and explore the challenges through projects and dissertations, then play findings back to us. We feed that directly into our product and strategy thinking,” adds John.

“This matters because we want to stay at the front edge of the industry,” he explains. “Working on challenges alongside – or ahead of – our clients helps us respond proactively and differentiate.”

People and collaboration

Across every voice we speak to, there is one theme that repeats: collaboration is essential – critical, even:

“Actionable research is crucial,” adds Kal Bukovski, Head of Academia and Research at Sopra Steria. “We bring together regulators, firms and technical practitioners so everyone takes something practical away. It’s about answering the what, why and how, not just describing the problem.”

With such a focus on technology, it may be surprising that what really drives FRIL’s research environment is a community of people who place a strong emphasis on meaningful and productive relationships. Mark explains:

“Our research, skills and education activities are all built on relationships. FRIL gives us a unique environment to build those and to translate research into real use.”

Research with purpose

This is research that doesn’t sit still. It moves quickly into white papers, innovation calls, student projects, product strategy, workforce upskilling and regulatory thinking. Kate Blatchford- Hick is Head of Consumer Investments Policy and Market Analysis at the Financial Conduct Authority and explains how the work drives impact for the regulators:

“FRIL’s research is really valuable as part of the market analysis, horizon scanning and insight work that we do. The work on AI and open finance, for example, helps deepen the evidence base around how emerging technologies are shaping consumer decision-making, both now and in the future. That, in turn, strengthens the FCA’s ability to anticipate market behaviours, risks and innovation, and helps us prioritise policy work that responds to both the opportunities and the potential risks.”

And while insights from FRIL are actively informing regulation and policy, they are also shaping a new generation of skills programmes designed for a rapidly changing sector. Earlier this year, FRIL launched the FRIL Skills Academy. The academy is a first-of-its-kind skills and education platform created to address capability gaps and support career development across financial and professional services and the wider fintech community.

Delivered with academic partners at the University of Strathclyde and the University of Glasgow, the Skills Academy responds directly to the accelerating pace of technological change, particularly in areas such as AI, data quality, and regulatory compliance, where talent shortages continue to slow innovation and increase recruitment costs.

FRIL research has highlighted persistent skills gaps across the sector, reinforcing the need for sustained, strategic investment in workforce development to maintain the UK’s global competitiveness.

“This is a new benchmark for how academia and industry partner at pace,” says Clare Reid, Strategic Innovation Director at FinTech Scotland.

And this point leads us to the nub of FRIL research. This research doesn’t just help us understand change, it informs how we shape it. That’s what makes this model so distinctive.

“I believe in this research because it’s about doing good quickly, we’re not just producing journal outputs, but creating real industry impact and addressing real consumer needs, right here and right now,” concludes Mark.

At the centre of FRIL’s research is a common theme – in a world of rapid change, we need to think differently and act boldly. That same mindset runs through the fintech world, where pushing boundaries, breaking ground, and creating new ways forward are part of the DNA.

As Kal puts it: “Fintech is a kind of art: you have to think beyond the limits and create something new that genuinely serves the right purpose.”

And that is FRIL research.

‘Innovation in financial regulation’ might not sound like the catchiest tagline, but it is at the heart of making the world better for all of us – today, tomorrow and in the decades that come.

What next?

Interested in the research generated by FRIL? Then check out our White Papers across a range of subjects.

If you’re interested in the work of FRIL more generally and would like to contact a member of the team email: FRIL@fintechscotland.com.

About FRIL

The Tipton selects docStribute® to modernise member communications

docStribute® and the Tipton & Coseley Building Society partner to improve the firm’s communications and strengthen member engagement

docStribute®, a UK RegTech company specialising in regulated customer communications, today announces a strategic partnership with the Tipton & Coseley Building Society.

The partnership reflects the Tipton’s continued focus on personalised service, deepening member engagement and meeting the requirements of the Financial Conduct Authority’s (FCA) Consumer Duty.

A key priority for the Tipton is accelerating digital transformation, with the partnership forming part of a multi-year change programme to expand online services, enhance systems and create better retail and working environments.

Through the docStribute® platform, the Society wants to move towards an electronic-first approach for both regulated and general communications. It aims to reduce delivery costs, process important documents more quickly, and use less paper, thereby lowering the associated carbon emissions.

Beyond cost, efficiency and environmental gains, the partnership will help the Tipton in repositioning its regulated documents, so they are not just a compliance requirement, but an opportunity to engage with members.

By presenting information in a clearer, more accessible digital format for those who want it, the Tipton can build greater awareness and understanding within its membership. This in turn supports well informed financial decisions, in line with Consumer Duty expectations.

docStribute® enables the delivery of timely, relevant communications which are easier to access, read, and navigate. The result is improved engagement and measurable insight into how members interact with information, allowing the Tipton to continuously improve clarity and outcomes.

Central to this approach is docStribute’s AIDA, the Artificial Intelligent Document Assistant. Developed through docStribute’s participation in FinTech Scotland’s Financial Regulation Innovation Lab (FRIL), it enables recipients to interact with regulated documents in a conversational way, helping them navigate complex information, ask questions, and receive clear explanations in real time.

The platform can also incorporate supportive formats such as short video and enhanced visual layers to aid accessibility and comprehension. Together, these tools support financial literacy and stronger understanding, while ensuring communications remain compliant and appropriately governed.

The platform uses Distributed Ledger Technology to protect the integrity of customer documents and create a verifiable record of what information was sent and when. This ensures communications remain secure, accessible, and compliant with the FCA’s Durable Medium requirements, while providing the sender with greater visibility of engagement and understanding.

Chris Ansara, CEO of docStribute®, said:

“We are pleased to be working with The Tipton & Coseley Building Society. Building societies have always been rooted in trust and community. Our role is to help turn regulated communications into moments that strengthen that trust by making important information clearer and easier to engage with.

“With AIDA, and enhanced formats such as video, we are adding another layer that actively supports member understanding, not just delivery. This partnership brings our total building society partners to four and highlights the sector’s continued emphasis on improving customer understanding through stronger engagement.”

Richard Groom, Chief Customer Officer at the Tipton, added:

“We are focused on increasing the proportion of compliant digital communications we send as this brings multiple benefits to our business and members alike. Adopting an electronic-first approach, in line with members’ preferences, is another step towards modernising our Society and will improve the overall standard of service we offer.”

The real constraint in advice firms is capacity

Insights from Tom Matthieson, Founder & Director, Glimzer

Capacity, not regulation

When people talk about the challenges facing financial advice firms, regulation is usually the first thing mentioned.

But in conversations with advisers, operations teams and firm leaders, a different constraint comes up far more consistently: capacity.

Not a lack of demand. Not a lack of intent to do the right thing for clients. Simply a lack of time and headroom in the day‑to‑day running of the business.

Advisers want to spend time with clients. Firms want to serve more people, improve consistency and grow sustainably. What gets in the way is the volume of administrative work required to keep everything moving. Manual updates. Duplicated data entry. Chasing information across systems. Maintaining spreadsheets alongside core platforms just to get a clear picture of what’s going on.

None of this work improves client outcomes. But it quietly consumes hours every week.

What’s striking is how normal this has become. Many firms accept admin drag as the cost of doing business, even though it directly limits how many clients they can realistically support. As teams grow, the problem often gets worse. More people means more handoffs, more checks and more effort spent reconciling information rather than using it.

Tools built for records, not delivery

A big part of this comes down to the tools firms rely on. Much of the infrastructure used in advice today was designed primarily to store records, not to support how advice is actually delivered in practice. Over time, firms adapt around these systems, building workarounds and manual processes to keep things running. The result is friction that feels unavoidable, but isn’t.

Small fixes that unlock capacity

At Glimzer, we’ve been spending time listening closely to how advice firms actually work day to day. What becomes clear very quickly is that small improvements in how information flows through a business can unlock meaningful capacity. Capturing data once instead of multiple times. Making workflows clearer. Giving teams visibility without having to build reports by hand.

This isn’t about changing the role of the adviser or introducing more complexity. It’s about removing unnecessary work so firms can use the capability they already have more effectively.

Collaboration matters

Being part of the FinTech Scotland community matters to us because these problems aren’t solved in isolation. They sit at the intersection of advice delivery, operations and technology, and they benefit from a shared perspective and honest discussion.

Our aim at Glimzer

We’re building in this space with a simple aim: to reduce friction, give advice firms back time and help them serve more clients without stretching their teams thinner. We’re keen to learn from others who are thinking about the same challenges, and to contribute to a broader conversation about how better infrastructure can support the future of advice.

Galveston Group

Glimzer

Protostars

Finance and Health Lab National Conference to convene cross-sector leaders at The Edinburgh Futures Institute

FinTech Scotland today announced the Finance and Health Lab National Conference, on 19 March 2026, an invite-only national event bringing together leaders from financial services, health, academia, government and the innovation ecosystem to explore how Scotland can lead the next wave of progress at the intersection of health and financial wellbeing.

Hosted at the University of Edinburgh’s Futures Institute, the conference will showcase practical insights, emerging innovation, and opportunities for collaboration focused on challenges that matter in later life and beyond — including inclusive service design, strengthening financial resilience, and building trusted approaches to data.

The Finance and Health Lab is designed to accelerate collaboration across sectors, connecting partners to test ideas, generate evidence, and support innovations to move from insight to impact. The conference will share what’s been learned so far and set out the next steps for continued ecosystem action.

What to expect on the day

The one-day programme (10:00–16:00, arrival from 09:30) includes:

- A keynote and guided discussion on the future of financial health in an ageing society

- A research insight showcase on health–wealth dynamics in later life

- An industry panel on designing future-ready, inclusive financial services

- A startup showcase and demonstrator session featuring ventures from the innovation call

- A data proposition session exploring trusted, ethical pathways for financial-health data use

- A closing conversation on scaling innovation through collaboration and national impact

Registration is invite-only, with a register interest option available via the event page.

Aleks Tomczyk, Chief Executive, FinTech Scotland, said: “Scotland has a unique opportunity to lead in innovation that connects financial resilience with healthier outcomes. The Finance and Health Lab National Conference brings partners together to share evidence, spotlight innovation, and build practical routes to collaboration and scale.”

Dr Andrea Taylor, Chief Executive Officer of Edinburgh Innovations, said: “This is an opportunity to align research, practice and policy and focus collective effort on innovations that can make a measurable difference for people as they age.”

Register interest

This event is by invitation only. Register your interest on the Finance and Health Lab National Conference page to receive further details.