How fintechs are driving financial inclusion

In this guest blog, Magdalena Krön, Rise Global FinTech Platform Director, Barclays Ventures, takes a look some of the work that the global fintech community is doing to address one of the biggest blights in society ”“ financial exclusion. This blog is based on the latest Rise FinTech Insights, a regular publication from Rise, created by Barclays.

One thing that COVID-19 teaches us, if we needed reminding, is how many people across the world remain disadvantaged by not having access to basic financial services. Although efforts to improve financial inclusion have come a long way in a relatively short period of time, there is still much more to achieve, especially for the 1.7 billion individuals who are currently unbanked(1). The work being done in the fintech space to address this issue, intended to open doors for individuals and families in a way that many of us take for granted, has seen entrepreneurs deploy everything from cryptocurrency to Open Banking and APIs in efforts to find new ways to support the financially vulnerable.

Chris Britt, Co-Founder and CEO of Chime ”“ a leader in the US challenger banking segment that offers internet-based, fee-free services ”“ says, “There is a huge segment of America that has a lot of anxiety around their money and day-to-day finances.” Helping them achieve “financial peace of mind”, he says, starts with providing a banking relationship that doesn’t rely on fees. “As many as 70% of Americans live paycheck to paycheck ”“ we offer free services such as early access to paychecks and overdraft protection.”

Innovative fintech thinking has come to the aid of another swathe of US society: the 2.5 million newcomers to the country on long-term visas who are, for the most part, unable to access credit. Collin Galster, Head of Business Development at Nova Credit, identified a solution to this problem facing the US’s foreign-born population, which is set to rise to 50 million by 2030. The company, a cross-border credit bureau, transfers individuals’ financial histories from one country to another, remedying the issue of lenders not being able to access enough financial information to feel comfortable lending, and therefore enabling immigrants to start funding their futures.

The need to tackle financial exclusion is felt even more acutely elsewhere. In India, for example, almost 11% of the adult population is unbanked. The report highlights a number of successful government initiatives, including Jan Dhan Yojana and Aadhaar Pay, that are spearheading more accessible paperless Know Your Customer (KYC) identification processes and biometric-based identity payment systems. This is a tactic that saw the number of people holding bank accounts increase by just over 50% between 2014 and 2017. Manish Khera, Founder and CEO of HAPPY ”“ a digital lending app targeting a multi-billion-dollar credit gap in India’s micro businesses ”“ emphasises how the internet now plays a vital role in facilitating and widening this access, citing the fact that India currently has 520 million mobile internet users.

Alternative banking solutions are springing up elsewhere, too. In east Africa, for example, Anisha Kothapa, Fintech Analyst at CB Insights, says cryptocurrency is being “adopted widely” ”“ offering a new way for the unbanked to save money and complete transactions without needing an account or credit card. One firm leading the way is Kenya’s BitPesa, a digital currency payments platform that “allows users to accept bitcoin payments, exchange bitcoin for local currency, and deposit bitcoin into accounts or mobile money wallets.”

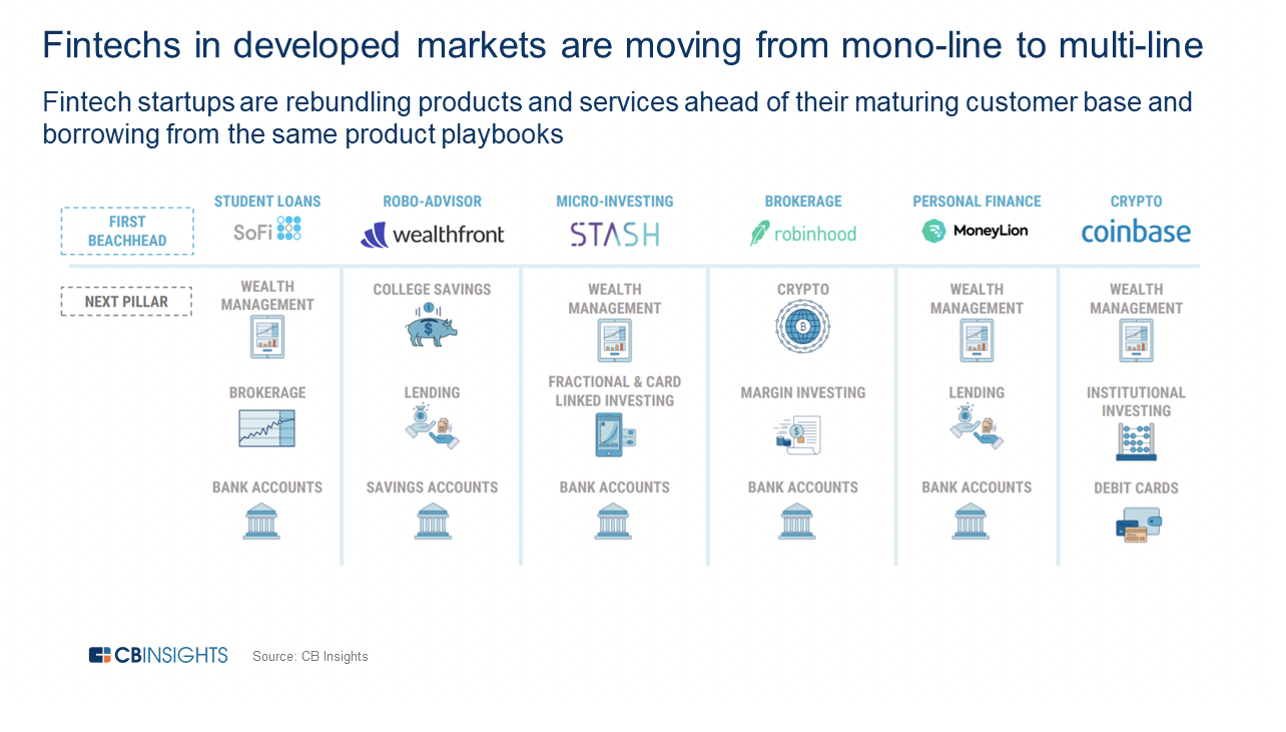

In contrast to developing countries, their developed counterparts are enabling financial inclusion differently by focusing on customer engagement and transforming the entire banking business model. FinTechs in developed markets are also moving from mono-line to multi-line offerings and re-bundling products and services to acquire more new customers.

It’s not just individuals that face financial exclusion, the report emphasises, but SMEs and budding entrepreneurs. According to Grant Bickwit, Associate at Barclays International, access to capital is one of the biggest challenges faced by entrepreneurs. It’s a sad truth, he explains, “that both entrepreneurs and investors are still reliant on individual networks and legacy processes for sourcing opportunities, entrenching geographic and social limitations”. In response to this, online platforms like OnDeck and Kabbage, launched in 2006 and 2009 respectively, offered firms access to credit digitally ”“ a trend that has proliferated.

Rise innovators have been responding to some of the other unique issues brought about by the pandemic, from employment to supply chain management. Rise Mumbai members, MMS.IND and GeoSpoc ”“ experts in geospatial information systems, platform-building, and consumer and micro-market data ”“ have joined forces to develop a COVID-19 impact tool which provides insights into how the pandemic is affecting consumers ”“ and enables businesses to better predict demand and ensure supply chain optimisation. Meanwhile, over at Rise New York, Brainceek, a workforce simulation company, has been helping corporates design virtual summer internship curriculums, providing extra support for the hundreds of thousands of graduates entering a difficult job market.

Addressing financial exclusion is a huge task, but one that is achievable, particularly with targeted collaboration across banks, technology companies and fintechs and a focus on achieving financial inclusion for those 1.7 billion individuals.

Download all editions of Rise FinTech Insights here.

(1) https://www.worldbank.org/en/topic/financialinclusion/overview

DirectID Launch Collections & Recoveries Solution

Scotland based FinTech, DirectID just announced the launch of its Collections & Recoveries solution.

DirectID has built a solution to make the collections process easier and faster in collaboration with the UK’s leading banks, lenders and debt collections agencies,

Using Open Banking data, agents will be able to access accurate customer’s financial statement and an assessment on their disposable income, and how much they can afford to repay.

The new solution combines DirectID’s categorisation engine with the categories defined within the Standard Financial Statement.

For individuals who have built up large amounts of debt, it removes a lot of the stress and uncertainty. The use of bank data negates the need for them to supply lots of details around financial commitments with existing creditors.

Currently, collections agents can spend a large volume of time with a customer assessing how much income they have, and what their discretionary and non-discretionary spend looks like. This process is also prone to customer error, downplay spend, or deliberately mislead, in an attempt to keep repayments low.

DirectID’s product circumvents the often unpleasant collections process from a period of weeks to just minutes.

Collections & Recoveries uses an individual’s bank data to help lenders streamline the collections process. This supplies the lender with an up-to-date and accurate view of an individual’s debt commitments and subsequently their capacity to repay debt.

DirectID’s Collections & Recoveries solution identifies income streams; expenditure; insight into a customer’s profile; including discretionary and non-discretionary; and summarises payments to lenders.

James Varga, CEO of DirectID, said:

“I am immensely proud to be today launching our new Collections & Recoveries solution. This is an extremely important proposition which will help both collections agents and their customers, during which can be a difficult process.

“With the launch of this product, and because of the impact of bank data, DirectID now covers the whole customer lifecycle, from onboarding, portfolio management, and now Collections & Recoveries.

The launch of DirectID’s Collections & Recoveries product marks an important step for DirectID, as we not only launch our first product of this year, but the first of several that we have completed, or are near to completion. Now that we can cover the whole product lifecycle with bank data, we are in a position to work with businesses across industry, and differing needs and challenges.”

Ex-Paypal CEO joins Money Dashboard

Scottish fintech Money Dashboard has just announced that Renier Lemmens would join the company as Chairman.

This is a great news for the fintech as Money Dashboard is gearing up to launch payment capabilities. With experience on the board of Revolut and as CEO of PayPal EMEA, Renier brings a lot of fintech knowledge.

Those are busy times for Money Dashboard with recent announcements about partnerships with Nutmeg and Wealthify.

Steve Tigar, Money Dashboard CEO commented:

“We’re delighted to welcome Renier to the board. His impressive experience as a fintech VC, CEO of Paypal EMEA and board member of Revolut will be invaluable as we enter our next phase of growth. We are particularly excited to have Renier on board as we prepare to launch our payments service, in addition to a number of other features that will revolutionise the way people organise and grow their money.”

Renier Lemmens, Money Dashboard Chairman added:

“Steve and the Money Dashboard team have done a fantastic job at building a product that truly helps people master their money. I am delighted to join them on this mission and look forward to helping the company go from strength-to-strength and leverage open banking to help millions of people.”

Money Dashboard recognised once more at the British Banking Awards

Scottish fintech Money Dashboard, was named Best Personal Finance App at the 2020 British Banking Awards. Money Dashboard also won this award in 2017 and 2018. The British Bank Award is a celebration of new innovative services which benefit UK consumers.

The company now has over 500,000 registered users who use the platform on a regular basis to manage their finances.

The solution allow people to see all their accounts in one place and now connects with products such as Revolut, Monzo, Starling and Wealthify – all of whom also took home awards on the night.

“We’re delighted to have been recognised by our customers as the UK’s best personal finance app for a third time. This is such an exciting time for independent fintechs like Money Dashboard. Millions of customers are now embracing new fintech products and are therefore benefiting from cheaper, faster and better services. We play a crucial role in bringing all those services together on a personalised dashboard for our customers.”

Steve Tigar, Money Dashboard CEO

Money Dashboard is preparing for a major product launch in the coming months and people can register their interest now.

Scottish fintech iDelta launches Open Banking Insights app

Edinburgh-based fintech iDelta announced the launch of its Open Banking Insight app to traditional banks combat the rapid rise of online challengers.

Last year, the implementation of Open Banking required the UK’s 300 banks and 45 building societies to release customer bank transaction data to authorised third parties with customer approval. Customers can therefore access their bank accounts using new solutions that make it easier to see several accounts in one place.

Scottish fintech iDelta developed a new app that provides retail banks with data driven insights on all aspects of business and infrastructure performance.

The iDelta Open Banking app allows incumbents to gain visibility on whether or not they are satisfying their customers needs. Indeed, with iDelta they can analyse and understand the interactions their customers are having with other providers.

“Open Banking is intended to increase competition in the marketplace, and in a competitive environment you get innovation. While challenger banks and other financial third parties are revolutionising the marketplace, there is still huge opportunity here for the incumbent banks to drive forward innovation, using insights gleaned from existing customer data to develop customer-focused products”.

“Our app gives the market a low-cost, highly efficient and extensible way of providing a business with a central view of their customer banking channel. Banks that choose to fully use the data they are generating, with the app we have built, will position themselves at the forefront of this new channel of business.”

Stuart Robertson, director at iDelta

The app uses an abstraction layer to deal with the fact that every bank will have different technology stacks. This allows its dashboards and reports to work with each bank’s systems with minimal customisation.

Money Dashboard and Wealthify to team up

Money Dashboard, the Scottish fintech that helps people manage their finances has just announced an integration with robo-investor Wealthify. This integration will let users view their investment accounts alongside the other current, credit and savings accounts they hold.

The Money Dashboard app lets people aggregate their various accounts and understand their spending habits to help them save and budget. Wealthify are the first investment integration rolled out by the app.

Wealthify provides an an online investment service. People can easily start investing with as little as £1. The investments are made via investment products such as ISAs, General Investment Accounts, and Junior ISAs and soon-to-be-launched Self Invested Personal Pensions.

This announcement follows Money Dashboard’s recent collaborations with leading challenger banks including Monzo, Starling Bank and Revolut.

“Our mission is to help people from all walks of life master their money, so we’re delighted to be rolling out integrations with innovative FinTechs such as Wealthify and making it simple for users to track their investments as well as their day-to-day spending and saving. Having complete visibility over one’s finances in real-time makes it much easier for people to understand their overall financial situation and to progress to where they want to be. This integration is one of a number of exciting new connections we’ll be making with providers across the financial landscape in the coming months”.

Steve Tigar, Money Dashboard CEO

“At Wealthify, we aim to make investing as simple, accessible and transparent as possible. Our integration with Money Dashboard is a fantastic fit for both brands, allowing our customers even greater visibility and control of their money. We are thrilled to be the first digital wealth management platform to partner with Money Dashboard ”“ our values are closely aligned and we have great respect for what they are doing.”

Richard Theo, Wealthify CEO

It’s worse than that”¦ Jim

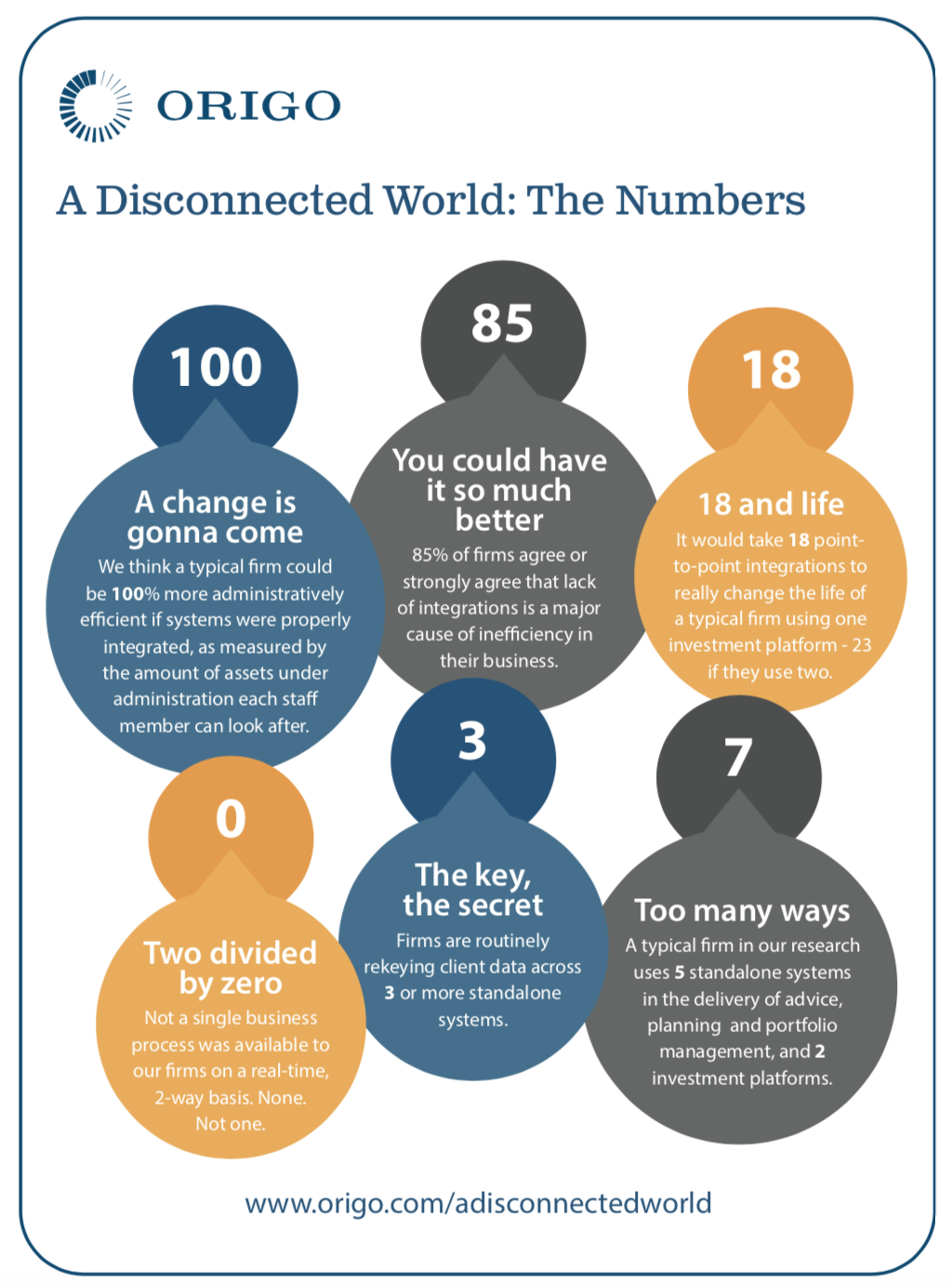

Anthony Rafferty, Managing Director, Origo says recent research into integration between systems in financial adviser firms’ back-office systems reveals a worrying disconnect eating into time, resource and profits of businesses

Origo recently commissioned in-depth research into the integration between systems in the back-offices of financial advice firms, and how this affected the efficiencies and profitability of those firms.

The research was carried out independently by the lang cat, a specialist financial services consultancy based in Edinburgh, and combined hours spent in financial advice firms around the UK mapping processes and analysing how they use the systems they have in place, as well as conducting online research with another 116 financial advice firms.

The conclusion is best summed up by Mark Polson, the MD of the lang cat, who was heavily involved in the research. He says: “We knew things weren’t great before we set out to conduct this research. But even so, we were struck by the impact of these inefficiencies on adviser back offices. Even where integrations do exist, firms aren’t trusting them or using them ”“ with good reason in some cases.”

From closely studying firms’ processes, the research estimates that in a typical financial advice business, staff could be up to 100% more efficient, dealing with twice the assets under administration they currently manage, if the systems they used were properly integrated with one another. In other words, staff could potentially be dealing with up to twice the number of fee paying clients than they are at the moment.

That is both a shocking state of affairs and also one of opportunity ”“ not least for financial advice firms.

To explain what we found: Firms involved in the study on average used five standalone systems in the process of giving advice, building investment and savings portfolios and managing clients; seven when platforms (transaction and administration services) were added; 10 with the addition of more general systems like accounting and office software.

It showed that due to a lack of integration between systems, and trust in those systems, firms are having to plough time and money into otherwise unnecessary manual input and reconciliation. In a typical new business journey, for example, client details were being keyed into systems at least three times!

Key facts from the research can be found on the accompanying infographic.

Currently ”“ and to be fair, despite sterling work by some of the players in the market ”“ advice firms do not benefit from a level of integration that is of real use to them. Integrations are typically point-to-point, with one provider integrating with another for specific purposes, for example for portfolio valuations.

They are also driven by business case, with platforms, CRMs and other system providers naturally prioritising integrations that will bring in higher levels of returns.

On a practical level and worryingly, even where integrations exist, adviser firms said that the lack of consistent and quality data meant they distrusted the output the systems are delivering, the result of which was that they had reverted to inefficient, costly and potentially risk inducing manual processes, because it was a process over which they have more control.

Typically there are 23 point-to-point integrations required within a firm using two investment and savings platforms, without factoring in any systems for protection and mortgage services and general office systems. On a point-to-point basis, that level of integration is never going to happen.

But there is a solution. We identified that if there was a centralised hub, into which platforms, CRMs and adviser software systems and tools could integrate once and then connect to every other player in the market who was also connected to the hub, and which also dealt with making and maintaining the connections, the benefit to the industry could be huge ”“ in particular to the financial adviser firms.

Using a centralised hub would mean any provider new or established could connect with any other provider on the hub, for services pertinent to their operations, no matter the volume of business.

In this way, a centralised integration capability would significantly improve the market’s connectivity, helping advice firms to improve their efficiencies, their profitability and enabling them to deliver faster and better service to their clients, whilst potentially boosting business across the board.

Hence, for the past couple of years we have been building the Origo Integration Hub to help provide that solution.

From a business perspective, for systems and services providers, this hub-and-spoke approach to integration does away with the need for case-by-case decisions and resource restraints incumbent of the point-to-point integration method. Linking to a hub incurs one set of integration costs instead of many, and significantly reduces resource and IT costs, which platforms and system suppliers can better apply elsewhere in their business.

Importantly, it provides the opportunity for all software and service companies, including smaller companies and new entrants, to easily connect with new trading partners if they wish. Also, it enables adviser firms to use the software or service that best suits their business set-up.

Currently, the Integration Hub has 19 companies including some of the big names in investment and savings signed to it, with others in the pipeline.

From a top down perspective it seems illogical that in the 21st century systems do not talk to one another in an efficient manner. However, this is a legacy issue which Origo with its remit to help improve the efficiencies and cost effectiveness of the industry and deliver better outcomes for consumers, is in a position to help resolve.

Read more about Origo here

Money Dashboard raises £4.6m, the biggest fintech raise on Crowdcube this year

Money Dashboard‘s personal finance management platform that connects to over 70 financial institutions to help users manage all their accounts in one place has just raised £4.6m.

Additionally, existing investors Scottish Investment Bank and Calculus Capital also invested. The initial target was £1.5m, however that number was reached in just 45minutes.

Funds are to be used to build out the market leading personal finance app and triple the company’s Edinburgh-based team from 20 to 60 staff.

Luke Lang, co-founder of Crowdcube, commented:

“Money Dashboard’s vision to help people better manage their money has once again resonated with many of our investors. It’s fantastic to see an innovative business connect their community, fuel their growth and take those investors, in this case, on their journey to create a fairer financial landscape.”

Steve Tigar, CEO said:

“We’re absolutely thrilled to have secured this latest round of funding, particularly with the backing of over 3000 people who share our vision. We are now equipped and ready to help people from every walk of life master their money.”

Kerry Sharp, Director of Scottish Investment Bank said:

“Having supported Money Dashboard from an early stage, it is great to see the business raising the funds required to implement the next stage in its growth. The FinTech sector is a key industry in Scotland’s economy and we look forward to continuing to work with the company, both from an investment perspective and through our account management support, to deliver its long-term growth ambitions.”

Scotland’s fintechs can unlock the power of open banking

There are over one hundred fintech companies thriving in Scotland’s fintech community with a range of new start-ups, existing firms developing their fintech offers and tech-driven firms re-locating north of the border. The launch of open banking last year has played a key role in fuelling the growth of this sector and the UK as a whole is now recognised as a world leader in open banking innovation.

So far, much progress in open banking has been made in the small business environment where innovative products and services are already in the marketplace such as tools for monitoring cash flow and accessing finance. An important contribution to this innovation was the first Open Up Challenge in 2017 and 2018 ”“ spearheaded by the Competition and Markets Authority (CMA) and run independently by Nesta Challenges. The Challenge was part of the CMA’s package of measures introduced to stimulate competition in the financial sector and help small businesses save time and money, find better services, reduce stress and discover the intelligence in their financial data. Winners included fast-growing fintech brands such as Swoop, Funding Options and Coconut whose products are frequently used by freelancers and small businesses across Scotland. However, as important as it is, the small business space is just the start of the open banking revolution.

When we consider the consumer market, while there are products that are already in use it’s fair to say that take-up has not yet been widespread – especially in light of research showing UK consumers stand to gain £12bn a year from open banking-enabled services[i]. Awareness of open banking is still low, with new research from Nesta Challenges showing that 55% of people in Scotland have not heard of it.

On the other hand, 46% of Scottish people say that they want to feel more in control of their finances and 33% want personalised information and guidance to help them manage their finances. For people in Scotland the two biggest benefits of using an open banking enabled product are seen to be: saving money and finding better deals. These findings present big opportunities for those fintech companies and start-ups in Scotland developing open banking-enabled innovations for consumers.

That’s why Nesta Challenges, in partnership with Open Banking Ltd, has launched the Open Up Challenge 2020 – a £1.5m prize fund to encourage fintech innovators to create solutions that will help people to make more of their money.

With Open Up 2020 we want to attract breakthrough innovations designed to support hundreds of thousands of people ”“ particularly the most vulnerable. We’re looking for fintech innovators that can unlock open banking’s potential to change the way that the UK manages its money ”“ especially for the 15.2 million who regularly run out of money each month.

Open banking represents a genuinely new way of empowering people with their data ”“ it is a key milestone on the journey to a digital economy, and the Open Up Challenge has an important part to play in encouraging people to make their data work for them. Open Up 2020 will not only help people better manage their money and take control of their data, but it will also support Scotland’s growing and thriving fintech sector by fast-tracking innovative new products and services. Applications for Open Up 2020 are open until October 2nd2019 and guidance on how to apply can be found at https://openup.challenges.org/apply/. In addition, the Open Up 2020 team will be holding office hours at Codebase, Edinburgh on Thursday 12thSeptember ”“ book your slot hereto benefit from tailored application support from the Open Up Entrepreneur-in-Residence Sarah Tierney.

[i]Consumer Priorities for Open Banking 2019

Scottish fintech Sustainably launches a new way giving

Sustainably is launching today at the Fundraising Convention in London.

The company offers a new way of giving to charities they care about without having to think about it, just by living their lives.

Sustainably is rounding up its users’ cashless transactions. The spare change is donating to the causes they care about, aligned to the UN’s Sustainable Development Goals. In an increasingly cashless society, it will unlock a new income stream for charities and enable supporters to see the difference they’re making instantly.

Inspired by Tom’s Shoes, Pokemon Go and Acorns Investing, Sustainably won the WeWork Creator Awards and is a top 10 Virgin Startup, with both global brands set to help Sustainably’s growth.

Speaking of Sustainably, Richard Branson said: “Sustainably is so simple, but effective, which most of the good ideas are. I loved the simple idea of rounding up everyday transactions and giving your spare change to chosen good causes. Sustainably is a great example of why I wanted to start Virgin StartUp in the first place – I knew there were entrepreneurs with good ideas who just needed a little support who could go on to achieve incredible things and have a positive impact on the world.”

Sustainably launches connected to 10 local and national charities, including British Heart Foundation, and will be adding new charities daily when it officially launches on 1 July.

Speaking of Sustainably, Simon Gillespie, CEO of British Heart Foundation said: “At the BHF, we’re continuously innovating to ensure our supporters have opportunities to donate to us in ways that fit in with their busy everyday lives. Innovation and the use of technology has been core to many of the breakthroughs we’ve made to improve treatments for heart and circulatory diseases, and we need to take this same cutting-edge approach to raising funds and building relationships with our supporters.

“Our partnership with Sustainably is a fantastic example of this approach in action. It will make supporting our research possible in the swipe of a finger as part of millions of transactions ”“ something that’s completely new. While the individual amounts might not seem like much, many small donations could add up to big breakthroughs in finding new treatments for conditions including heart disease, stroke and vascular dementia. We’re excited to see what this new way of fundraising has in store.”

Loral Quinn, co-founder and CEO of Sustainably explains: “We’re excited to launch our technology that makes doing good something you can do easily, everyday.”

Sustainably links to people’s bank card rounding up on their behalf. It’s also very easy easy to see impact of donations thanks to a new form of impact messaging between charities and supporters to help inspire engagement and trust, by providing an instant impact update.

The team at Sustainably is 8 staff strong with plan to grow in the next year as they target business donations.

The charity donations market is estimated at more than £12 billion in the UK per year.

Founded by mother and daughter team, Loral and Eishel Quinn, Loral, CEO, was head of digital marketing and strategy for Aberdeen Asset Management, where she set up the global digital team and helped scale the business from 6 to 30 countries in 10 years. Eishel, Chief Product Officer, has a background in ethical retail, working with Neal’s Yard Remedies. Eishel was recently named one of Digital Leaders top 10 Young Digital Leaders.