The real constraint in advice firms is capacity

Insights from Tom Matthieson, Founder & Director, Glimzer

Capacity, not regulation

When people talk about the challenges facing financial advice firms, regulation is usually the first thing mentioned.

But in conversations with advisers, operations teams and firm leaders, a different constraint comes up far more consistently: capacity.

Not a lack of demand. Not a lack of intent to do the right thing for clients. Simply a lack of time and headroom in the day‑to‑day running of the business.

Advisers want to spend time with clients. Firms want to serve more people, improve consistency and grow sustainably. What gets in the way is the volume of administrative work required to keep everything moving. Manual updates. Duplicated data entry. Chasing information across systems. Maintaining spreadsheets alongside core platforms just to get a clear picture of what’s going on.

None of this work improves client outcomes. But it quietly consumes hours every week.

What’s striking is how normal this has become. Many firms accept admin drag as the cost of doing business, even though it directly limits how many clients they can realistically support. As teams grow, the problem often gets worse. More people means more handoffs, more checks and more effort spent reconciling information rather than using it.

Tools built for records, not delivery

A big part of this comes down to the tools firms rely on. Much of the infrastructure used in advice today was designed primarily to store records, not to support how advice is actually delivered in practice. Over time, firms adapt around these systems, building workarounds and manual processes to keep things running. The result is friction that feels unavoidable, but isn’t.

Small fixes that unlock capacity

At Glimzer, we’ve been spending time listening closely to how advice firms actually work day to day. What becomes clear very quickly is that small improvements in how information flows through a business can unlock meaningful capacity. Capturing data once instead of multiple times. Making workflows clearer. Giving teams visibility without having to build reports by hand.

This isn’t about changing the role of the adviser or introducing more complexity. It’s about removing unnecessary work so firms can use the capability they already have more effectively.

Collaboration matters

Being part of the FinTech Scotland community matters to us because these problems aren’t solved in isolation. They sit at the intersection of advice delivery, operations and technology, and they benefit from a shared perspective and honest discussion.

Our aim at Glimzer

We’re building in this space with a simple aim: to reduce friction, give advice firms back time and help them serve more clients without stretching their teams thinner. We’re keen to learn from others who are thinking about the same challenges, and to contribute to a broader conversation about how better infrastructure can support the future of advice.

When Technology Stops Being the Hard Part: The Real Constraint on Scale

By Patrick Byrne, Co-founder and CEO, Struan.ai

I’ve spent most of my career helping to grow technology-led businesses. Most often, I’ve been brought in when growth was the ambition, but the wheels were starting to wobble.

Years ago, the main risk was obvious. Would the technology work at all? Could it scale? Could the team actually build what had been promised to customers or investors? Infrastructure was expensive. Engineering talent was scarce. Shipping even something modest took time, money and a fair amount of nerve.

That environment shaped how a lot of us learned to build companies.

Today, that constraint has largely gone away. Cloud platforms are easy to access. Tooling is mature. AI has lowered the barrier to building and iterating to the point where small teams can move at a speed that would have felt unrealistic not that long ago. In many cases, the product gets built. It ships. It works.

And yet, despite all of that, growth still feels harder than it should.

I remember this very clearly in one of my former businesses. In 2017, as CEO, we kicked off what was meant to be a straightforward CRM migration. The plan was sensible enough. Four months end-to-end. Clean up the data, move systems, improve visibility, then get back to growing the business.

Seven years later, that project was still technically ‘ongoing’.

Not because the technology didn’t work. The tools were fine. The vendors did their part. The issue was everything wrapped around the technology. Data ownership was unclear. Processes changed faster than they were documented. Edge cases kept appearing. People worked around problems rather than fixing them, because there was always something more urgent to do.

Where Things Start to Strain

What I see repeatedly is execution starting to lag as momentum builds.

As organisations grow, the volume of everyday work rises quickly. Sales activity increases. Marketing needs to operate consistently, not just when there’s time. Customers need onboarding, support and follow-up. Different stakeholders need different reports to meet their own agendas. Controls tighten. None of this is optional, and most of it relies on context, judgement and continuity.

This kind of work doesn’t lend itself to an organisation that was once dynamic and nimble. Suddenly, everything is a priority and everything is urgent. So, more people are hired.

At a small size, teams cope. People know what’s going on. Gaps get filled informally. Someone stays late. Someone remembers how a thing was done last time. As volume increases, those informal fixes start to break down. Processes end up spread across tools, documents and inboxes. Important details live in people’s heads. Things still get done, but more slowly, and with less confidence.

When problems surface, they’re often written off as one-offs. In reality, they’re early signals that the operating model is under strain.

Predictable Reactions

When pressure builds, most organisations reach for the same levers.

They hire more people. They add more tools. They outsource parts of the operation.

Sometimes that helps, at least temporarily. But it usually introduces new trade-offs. More people means more overhead and more management. More tools mean more things to manage. Outsourcing can reduce visibility at the exact point where clarity matters most.

This is how many businesses drift into an awkward middle ground. The product works. Demand exists. The team is capable. But progress feels like running through treacle. Growth becomes something to manage carefully, rather than something to lean into.

What’s Usually Missing

In almost every case, the same things show up.

There isn’t a clear operating model for execution, or if there is, it’s not followed.

In organisations that scale well, execution isn’t something that happens between meetings or when people find the time. It’s treated as a system. There is ownership. There are rules, controls and clear escalation paths. Outcomes are visible and repeatable, rather than dependent on who happens to be involved on a given day.

AI can help here, but only if it’s applied in the right place. Used simply to assist individuals, it has limited impact. Applied to running defined workflows, it starts to change how work actually gets done.

Sales, marketing and operational processes benefit far more from reliability than creativity. When execution is predictable, people can spend their time on decisions, relationships and direction instead of firefighting.

Why Struan Exists

Struan came out of seeing this pattern first-hand, over decades of building high-growth businesses, operating at the edges of cashflow constraints.

While building an AI-first business that demanded a high level of control and consistency, it became clear that the real challenge wasn’t technical capability. It was execution. Specifically, who owned it, how it was run day to day, and what happened when things inevitably drifted.

Struan was built as a managed service to address that gap. It is delivered by a team with decades of experience building, scaling and running high-growth businesses, often in environments where cashflow was tight, stakes were high and there was no room for theoretical solutions. Between us, we have lived through most of the realities organisations face as they grow: performance issues that are hard to confront, people problems that drain energy, systems that fail at the worst possible moment, clients who don’t pay on time, difficult customer relationships, cashflow pressure, cultural changes as teams scale, multi-site complexity, poor management decisions, and the cost of reacting too slowly when things start to go wrong.

That experience is distilled into how Struan operates. We don’t sell tools or frameworks and leave clients to make them work. We take responsibility for execution itself, embedding AI into real workflows and running them on our clients’ behalf. The surface-level problems vary from business to business, but the underlying causes are remarkably consistent. By addressing those causes directly, Struan delivers practical impact where it matters most: reliable execution, reduced operational drag and the confidence to scale without losing control.

The Takeaway

The tools to build faster, operate leaner and scale more confidently are already here – accessible, proven and improving rapidly. What’s missing is conviction.

The real barriers to AI adoption are fear and trust. Fear of getting it wrong. Fear of disrupting something that currently works. A lingering suspicion that this only applies to technology companies with deep pockets and specialist teams.

That thinking is already out of date.

The organisations that thrive over the next decade will be defined by leadership that recognises what AI makes possible and acts on it before the competition does. Because competitors will act. In every sector, in every vertical, someone is already working out how to do more with less, move faster and operate with greater consistency. The gap between organisations that embrace this shift and those that hesitate will widen quickly and may not close again.

The question isn’t whether AI will reshape your market. It’s whether you’ll ride the wave or be swept away by it.

In conversation with Financial Services: Why innovation really matters

The term ‘innovation’ might bring to mind a race for better technology, systems and smarter data, but beneath it all lies a fundamental question: how do we create a fairer financial future for all?

For most people, financial advice isn’t about products, platforms, or policy. It’s about life: buying a first home, protecting a family, surviving a setback, or planning for a future that feels uncertain.

Yet for millions, financial advice remains out of reach.

As one of the most significant regulatory shifts in recent years begins to reshape how people access financial support, the financial services sector is radically reshaping how advice and guidance is delivered.

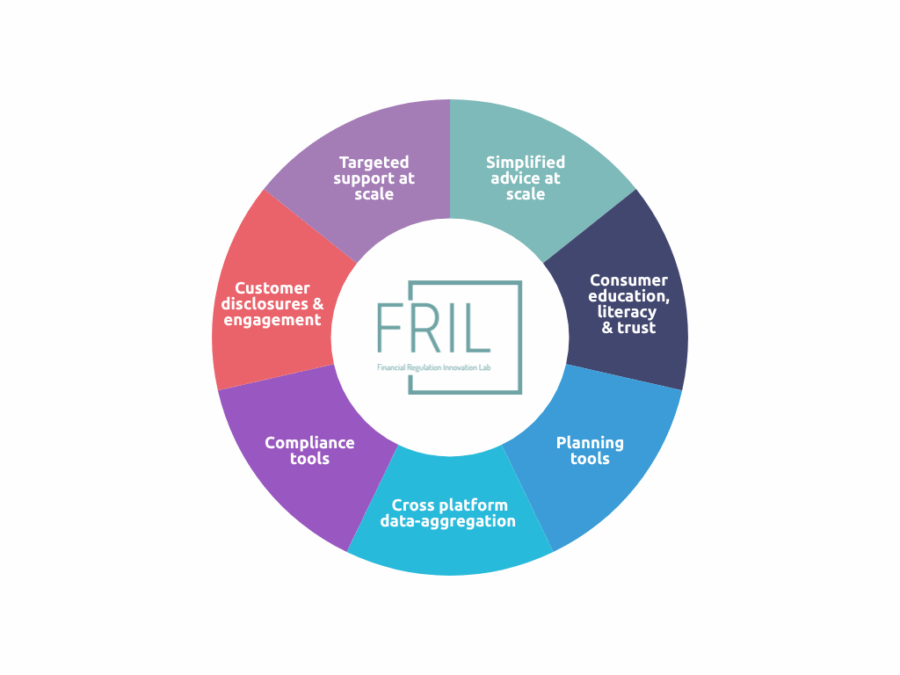

This is just the kind of challenge that our pioneering Innovation Calls take on, led by our team in the Financial Regulation Innovation Lab (FRIL). Our latest call focused on the Financial Conduct Authority’s (FCA) Advice Guidance Boundary Review, a technical name for a very human issue: how to make financial help clearer, fairer and available to far more people.

Bringing together fintech founders, academics, financial services leaders, and regulators, FRIL’s Innovation Call creates a space where policy, practice, and possibility meet.

Here, we speak with two financial services leaders involved in the call to find out more about why innovation is so important to their firms, as well as the future of the sector:

- Maria Herrero Bullich – Chief Customer and Digital Officer, Insurance, Pensions & Investments at Lloyds Banking Group.

- Kate Murray – Strategic Projects Lead, Scottish Widows & Lloyds Banking Group.

Addressing the Big Picture

“For me, the utopia is that everyone who wants to do the right thing for their future has real choice. Whether they’re looking for simple guidance, clearer recommendations, or full financial advice. What matters is that people have different options, depending on their needs, and the freedom to decide which path is right for them,” explains Maria.

“It’s important to us to close the advice gap by building tools that help people think about their futures, especially those who can’t afford traditional advice, so they still have access to clear, targeted support when making important financial decisions.”

And this work matters, because the numbers are concerning. Millions of people across the UK still receive no financial advice at all, and while support exists, it is often out of reach for those who need it most.

The Advice Guidance Boundary Review represents a critical moment for the sector, an opportunity to ensure that more people can finally access support when making some of the most important decisions about their money.

Kate explains: “Our purpose is to help more people secure their financial futures, in a way that aligns with our wider goal of helping Britain prosper. There’s a real advice gap in the industry, and whether someone is our customer or not, we want to help fill that void so more people can move towards a more prosperous financial future.“

“At one end of the spectrum, people can’t afford advice –so they self-serve through available guidance, but don’t know what to do with it. At the other end, people can access full, holistic advice. In the middle, many don’t know how to save, invest or prepare for retirement. That’s where we see innovation and new solutions helping people understand their next step, whether that’s saving and investing more, planning for retirement, or putting more into their pension.”

Meeting Consumer Needs

And when we look more closely at this issue, it becomes clear that a one-size-fits-all approach simply won’t meet the diverse needs of consumers. Across the industry, firms are increasingly focused on developing more tailored ways to support those who are currently slipping through the advice and guidance net.

Maria explains: “There are parts of society that face very different challenges, from the gender gap in pensions to younger generations trying to save for the future. We’re focused on how to bring people who often have less financial confidence into the conversation and help them think about their futures.“

“Different groups need to be engaged in different ways. Younger people can be hard to reach, so we use techniques like gamification to encourage them to start those conversations. Others, such as people who feel less confident about investing, or women who may have taken career breaks and are worried about having enough for a comfortable retirement, face different barriers.”

These are very real issues, affecting everyday lives. Kate stresses the impact of what happens if the gap isn’t closed:

“Through work like our annual Women in Retirement report, we can see a massive gap in people’s financial futures. Significant proportions of society, who are working today, are on track to reach retirement without enough money, and that means going from work to a retirement in poverty.“

“That’s a serious problem, not just for individuals, but for the UK as a whole. It’s a systemic, government-level issue that needs to be addressed now, to prevent that happening for people as much as possible.”

Future Solutions Now

Finding solutions to these challenges requires a collaborative approach – different perspectives, experience and skillsets. That’s why this FRIL Innovation Call matters so much.

“It’s been so interesting to meet the fintechs and to connect with strategic partners, to better understand what they can bring to help us move at pace and innovate – so we can, at scale, support more customers to secure their financial futures,” says Kate.

“It’s been so interesting to meet the fintechs and to connect with strategic partners, to better understand what they can bring to help us move at pace and innovate – so we can, at scale, support more customers to secure their financial futures,” says Kate

“This is a huge opportunity for us. Scottish Widows has been involved in earlier calls, and this feels like a real chance to do things differently. At Lloyds Banking Group, we’re constantly trying to change how we innovate and move faster. Bringing in outside thinking, new technology, and completely different perspectives helps us bridge that and go quicker.”

And that’s why innovation in financial services is about far more than technology, systems, and data. As Maria puts it:

“We focus on creating experiences that aren’t built around products, but around people. It’s about understanding what they need, where the gaps are, and how to help them close them.”

The Advice Guidance Boundary Review. Just what does it all mean?

Advice: A regulated service where a financial adviser looks at your full financial situation and gives you a personalised recommendation.

Guidance: Support that points you in the right direction based on limited information you share, without telling you exactly what to do.

Boundary: The line that separates advice from guidance, defining how much information is needed and what a firm can or can’t recommend.

Review: The regulator’s process of consulting industry and consumers, and government to create clear new rules that will shape how these services work in future.

What next?

Enjoyed this piece? Hear from the perspective of the fintechs involved in the call. If you’re interested in the work of FRIL more generally and would like to contact a member of the team email: FRIL@fintechscotland.com.

About FRIL

2026 and Beyond: FinTech Scotland’s Next Chapter

A Message from Aleks Tomczyk

In 2025, global fintech investment rose by 21% to $53bn, signalling a welcome return to growth across most markets. The US remained the global leader at $25.1bn, while the UK reclaimed second place with $3.6bn. These figures are more than just encouraging – they point to renewed confidence across the fintech ecosystem and set a strong foundation for 2026.

Against this backdrop, I feel a genuine sense excitement and responsibility as Chief Executive of FinTech Scotland. We’re at a pivotal moment for the cluster: it’s vibrant, the ambition is real, and the opportunities ahead of us are immense.

My immediate focus is clear, centred on three priorities.

Firstly, we will strengthen and scale our innovation programmes to deliver real value across the ecosystem including measurable social impact.

That means deepening the work already underway and improving on it:

- Through our award-winning Financial Regulation Innovation Lab, we will continue to strengthen the collaboration between innovators and regulators, ensuring Scotland remains at the forefront of fintech that supports regulation and reducing operating costs whilst improving consumer outcomes.

- With the Centre of Excellence in Digital Trust, led by Edinburgh Napier University, delivered in partnership with Edinburgh and Glasgow Universities, we will position Scotland as a global innovator at the intersection of digital trust, identity, crypto and data in financial services.

- We will scale the Finance and Health Lab, driving better financial wellbeing, resilience and long-term financial health for people across Scotland.

Secondly, we will build sharper, more targeted support for fintech entrepreneurs – from idea through to international scale-up.

This means clearer enabling pathways, stronger networks, better access to funding, and programmes (including our Innovation Labs) grounded in real company needs. Alongside this, we will amplify Scotland’s presence in priority global markets, making our firms more visible, better connected, and bringing more of Scotland’s fintech innovation onto the world stage.

Thirdly, we will drive greater collaboration across the ecosystem.

By enabling connections inside and outside Scotland amongst our strategic partners, fintechs, academic institutions and in related professional services we will help financial services and fintech companies large and small to prosper. This will be made possible by strong foundations – an excellent talent pool, world class research base and great, forward thinking, existing financial services companies – we will help to strengthen them, further.

These three things will result in growth, create high-value jobs, attract inward investment, encourage new startups and strengthen resilience in the cluster. Fintech will play an enhanced critical role in Scotland’s economic future.

I have a background in technology innovation and business building. I have run major change projects in financial services. I have built two fintechs from the ground up.

One of the things that has always excited me most is the role of people, networks and ecosystems in innovation. Technology doesn’t create change – people do. Innovation succeeds best when stakeholders collaborate to solve real problems, when trust is built, and when ambition and success are shared.

I am confident that by building further on our fintech community, and by staying focused, collaborative and ambitious, we can deliver tangible impact for our companies large and small, our people, and our country – plus companies and people elsewhere.

In the years ahead, I look forward to meeting many of you – employees, founders, investors, academics, regulators and partners – because relationships are the bedrock of success. I welcome your ideas, your energy and your feedback, and I encourage you to reach out to us here any time.

Here’s to the journey ahead.

Creating fairer financial futures: A focus on the fintechs

Innovation starts with people. That’s our belief at the Financial Regulation Innovation Lab (FRIL), and that’s why we bring together pioneering fintech entrepreneurs with industry and academia to address challenges facing financial services – both now and for the future.

At FRIL’s latest Innovation Call, fintech entrepreneurs took on one of the most significant regulatory shifts in the sector, pitching ideas that could change how millions of people access financial support and move us closer to fairer financial futures.

But what really drives these fintech founders, and what happens behind the scenes for them at an Innovation Call?

We spoke to two of the founders who took to the stage to find out more.

First of all, let’s meet Crawford Taylor, a co-founder of Afternoon, a data and AI operating model for financial advisors

Crawford, you’ve just come off the stage, but before we hear about that, please tell us, what exactly is a ‘data and AI operating model for financial advisors’?

“Sure, it means that we collect the data financial advisers need to support their clients, enrich it, and then use AI to automate their workflows. That significantly reduces the time it takes for advisers to deliver advice, so they can focus more on their clients.”

And why does this area matter to you?

“Before this, I worked as a consultant advising trustees and companies on defined benefit pension schemes, helping secure the future for people who already had a pension so they’d receive what they were due at retirement. This feels like a natural extension of that, helping more people manage their money better and be financially better off.”

You’ve just pitched at our Innovation Call, how did that go?

“I think it went well. With 19 other companies pitching to a panel of around 10 large corporates, including organisations like M&G, NatWest, and Sopra Steria, it’s a great opportunity to explore potential partnerships.”

As a fintech founder, what is your big ambition?

“There’s around £18 billion spent on financial services technology every year, and it’s only going to grow, yet there’s still a huge advice gap, where many people can’t access or afford support. So much time is lost joining the dots, from opening accounts to moving money. Our ambition is to automate that entire process, so advisers have everything at their fingertips and clients can go from advice to action – opening accounts and transferring funds – in seconds.”

Thanks Crawford, and final question, what has being involved in the Innovation Call meant for you?

“It’s been energising. The Innovation Call was exceptionally well designed; it respected how stretched early-stage teams are, while still pushing to sharpen our thinking and ambition. The combination of regulator insight, industry partners, expertise from Growth Builders and practical support created real momentum for us. Huge thanks to Fintech Scotland and everyone involved.”

And now let’s hear from another fintech founder, please meet… Dia Banerji, founder of Cherpa.ai, an AI money coach that delivers hyper-personalised financial education.

Dia, you’ve just done your pitch – how did it go?

“I was first up, which always adds a bit of pressure, but it felt good. The presentation went well. Most importantly, I was able to clearly tell the story of why Cherpa.ai exists.“

And on that note, Dia, why does Cherpa.ai exist?

“It is very close to my heart. So many people feel a real sense of shame when they don’t understand money, and that keeps them from asking questions. I recently ran a survey about money confidence, one person told us their biggest wish was simply to feel less ashamed about talking about money – and that really stayed with me. Cherpa is here to change that and help people connect with their money and navigate life with confidence. Because every life moment is a money moment.”

Why does this call matter to you?

“This call matters a lot to Cherpa & me personally. More than 90% of people in the UK can’t access financial advice, and there’s a big step before advice that’s really about awareness and education. People often see ‘investment’ as something for someone else, and financial education is still very low, which leaves people disconnected from their money. That’s why this call feels important, not just for the UK but for the world.”

And are there any particular aspects that have struck you over the last few weeks?

“I’ve been really happy to be part of this cohort. The run-up has been amazing, with sponsors coming in, sharing their problem statements, and giving us time to learn from them and from the other fintechs. It’s been great to feel part of a real community and to play a small part in helping Scotland thrive.”

What are your hopes for the result?

“I’m really excited to be part of this cohort and would love to work more closely with some of the sponsors. Beyond that, it’s about being part of a wider fintech community, learning from others, and helping Scotland, and ultimately people everywhere, build more confidence and connection with their money.”

So what next for the fintechs who took part?

With the winners now announced, the successful teams will receive grants of up to £50,000 to develop, scale and implement their ideas over the coming months.

But the journey doesn’t end there. Beyond the winners, many of these ideas are likely to spark further interest, partnerships and pilots in the months ahead.

If you’d like to find out more about the work of FRIL, please contact us at FRIL@fintechscotland.com.

About FRIL

Creating fairer financial futures: A spotlight on FRIL research

Technology-enabled advice, Regulation and the Advice Gap: 10 minute Insight from FRIL Research. 10 Questions with Chuks Otioma, Research Associate, Adam Smith Business School

As financial services explore new ways to close the advice gap, technology enabled advice and guidance models are increasingly part of the conversation – but what do they really mean for consumers, firms and regulation?

As part of the Financial Regulation Innovation Lab (FRIL), researchers from the University of Glasgow and University of Strathclyde are working alongside industry, fintechs and regulators to examine how innovation can be deployed responsibly in financial services.

In this conversation, Chuks Otioma, Research Associate, reflects on his research into these digitally- enabled advice models: what they are, why they matter, and how they sit within the Advice Guidance Boundary Review.

1. Chuks, let’s start with you first of all – what drew you to this field of research?

Before moving into academia, I worked in industry, in telecommunications. During my PhD, I looked at the links between digital capabilities, innovation and economic performance, and the role of entrepreneurs and innovators in leveraging digital advances; work that now informs my research into AI in financial services. I was particularly interested in how firms reorganise themselves, their processes, structures and activities in order to draw value from digital technologies.

At that stage, my work wasn’t focused on financial services specifically. It was broader, looking at firms across sectors and how they approach digital transformation. What I’m doing now is a natural progression of that work, but with a much sharper focus on financial services and the challenges firms face in deploying technologies like AI.

2. OK, let’s explore your research Chuks. First of all can you explain to us what “technology-enabled advice and guidance models” actually are?

At a basic level, the term refers to digitally enabled advice. It can be relatively simple, or more advanced, using AI to construct and refine portfolios.

What’s important is the way technology can help streamline advice around individual needs. But this also raises important considerations. You have to think carefully about the data being used, the potential for data breaches, and whether consumers genuinely understand the advice they’re receiving.

There are also different operating models. Some are largely consumer-led, with minimal human interaction. Others are more professional-led, where investment or wealth managers use automated tools to manage portfolios on behalf of clients. Each model raises different questions around responsibility and duty of care.

3. The Advice Guidance Boundary Review aims to ensure that financial help is clearer, fairer and available to far more people. How do these technology-enabled models play a part here?

Some forms of digital advice function as guidance, pointing consumers towards information or helping them explore options. Others go further, making recommendations or even decisions on a client’s behalf, which brings them firmly into the realm of regulated advice.

That distinction matters, particularly as systems become more advanced. The more decision-making is delegated to automated systems, the more important strong compliance, governance and accountability become.

4. Can these models really help address the financial advice gap?

There is evidence that automated advice has already improved access and inclusion, particularly among younger people and those who might not otherwise engage with traditional investment services.

Because these systems can draw on rich data and integrate information from multiple sources, they have real potential to support people who currently lack access to advice.

What’s especially interesting is the way some platforms are beginning to connect users to independent financial advisers, recognising that investment decisions don’t exist in isolation. Financial wellbeing also involves literacy, planning and understanding long-term goals.

“These systems have real potential to support people who currently lack access to financial advice.”

5. What risks need to be managed as technology-enabled advice and guidance becomes more common?

In our research, we look at several dimensions. There’s the operating model, and how responsibility is shared between consumers, professionals and platforms. There’s financial risk, including market volatility, trend-chasing and over-concentration.

We also examine data practices, including how platforms are designed, who has access to data, and how data is shared across third parties and jurisdictions. In many cases, the developer of the system is not the same as the organisation managing it, which raises important governance questions.

“When advice becomes more automated, firms need to be clear about who is responsible when things go wrong.”

6. What has surprised you most in your research?

One of the most striking findings is the level of consumer misunderstanding. Products are often designed on the assumption that firms understand their users, but in practice there can be significant misalignment between innovation and user understanding.

This isn’t necessarily about consumers lacking capability. It’s often about how products are designed, communicated and framed. That’s a critical lesson for firms designing these products.

7. What big questions does this raise for firms and for the industry?

One of the big questions is around responsibility and accountability, particularly as more decision-making is delegated to automated systems. When advice becomes more automated, firms need to be clear about who is responsible when things go wrong.

Beyond that, these developments also raise important questions about how firms organise themselves. Automated advice reshapes how services are delivered, which has implications for workforce skills and training. Technical teams increasingly need some understanding of finance, while those working in finance or customer support need a basic understanding of how AI-based systems work.

There are also strategic questions around how these systems are developed and deployed. Firms need to decide whether to build solutions in-house or rely on third-party providers, and how external systems integrate with existing or legacy technologies. These choices affect how services are scaled and managed over time.

Taken together, these are organisational challenges as much as they are technological ones, and they shape how firms deliver automated advice in practice.

8. With all this in mind, what future are you trying to help shape through this research?

For me, the most important thing is societal relevance. I’m interested in research that informs policy-making and speaks directly to real-world challenges.

FRIL is quite unique in that sense. The challenges we work on are industry-led. You have problem owners defining the issues they face, fintechs developing solutions, and researchers contributing evidence and insight that can help shape both practice and regulation. It’s impact-oriented research, and that’s very fulfilling.

Ultimately, the future I want to contribute to is one where research doesn’t sit in isolation, but actively helps address the problems faced by industry, policymakers and society more broadly.

9. Can you share some examples of wider real-world challenges you’ve been working on?

One example is our work looking at consumer complaints within financial services. By analysing the types of complaints that are escalated to the Financial Ombudsman Service, and how providers respond to them, we can better understand where things go wrong.

If we understand these friction points, there’s an opportunity to co-develop financial products differently, reducing the likelihood of harm or escalation in the first place.

In our work on automated advice, we’ve also explored how providers can embed responsible practices into their models. That includes linking clients to green or sustainable investment opportunities, and aligning portfolios not just with financial returns, but with broader social and environmental goals.

“Automated advice reshapes how services are delivered, with implications for workforce skills, training and how firms organise themselves.”

10. Finally, what feels special about doing this research here, in Scotland, and within the FRIL ecosystem?

What stands out for me is the research culture and the ecosystem we’re working within. The University of Glasgow, and the Adam Smith Business School, have a strong international research culture, and we work very closely with colleagues at the University of Strathclyde and with industry partners.

Beyond the universities, there’s something distinctive about how this work comes together in practice. Through FRIL, you have financial services providers, fintech developers, regulators and researchers working together on a daily basis. It’s what we often describe in theory as an “ecosystem”, but here it’s very real.

That makes it a unique environment for doing this kind of research, not in isolation, but embedded in the real challenges facing industry and society.

Explaining the terminology

- Technology-enabled advice: A digital tool that uses information about a person to help guide or automate investment decisions based on their individual needs.

- The Advice Guidance Boundary Review. Just what does it all mean?

- Advice: A regulated service where a financial adviser looks at your full financial situation and gives you a personalised recommendation.

- Guidance: Support that points you in the right direction based on limited information you share, without telling you exactly what to do.

- Boundary: The line that separates advice from guidance, defining how much information is needed and what a firm can or can’t recommend.

- Review: The FCA’s process of consulting industry and consumers, and government to create clear new rules that will shape how these services work in future.

What next?

Interested in the research generated by FRIL? Then check out our White Papers across a range of subjects.

For more detail on this topic, see Chuk’s white paper.

If you’re interested in the work of FRIL more generally and would like to contact a member of the team email FRIL@fintechscotland.com.

About FRIL

Creating Fairer Financial Futures – AGBR Innovation Showcase Day

On 15 January 2026 in Glasgow, more than 100 people gathered for a high-stakes showcase.

The purpose of the gathering?

To address one of the most important regulatory shifts in financial services today. A shift which could reshape how millions of people access financial support and create fairer financial futures for all.

The event was the final showcase day of an Innovation Call – a pioneering initiative led by the Financial Regulation Innovation Lab (FRIL) at the heart of FinTech Scotland.

But, what is an Innovation Call, what happens on showcase day and what is achieved?

Well, join us as we take you behind the scenes of the day and speak to some of the people involved.

Let’s start with Clare Reid, Strategic Innovation Director at FRIL.

Clare, explain to us what to expect on a Showcase Day of an Innovation Call?

“Nerves certainly run high on showcase day of an Innovation Call! It’s the culmination of months of work for Fintech entrepreneurs as they pitch their solutions to an audience of potential Financial Services partners. And the stakes are high – there is an award of £50,000 to successful fintechs and the opportunity to take forward some potential game changing solutions and partnerships with those partners.“

What was the challenge or opportunity today’s call addressed?

“This call focused on the FCA’s Advice Guidance Boundary Review – which is addressing a very human issue about how to make financial help clearer, fairer and available to far more people.”

“The call is all about finding new ways to help consumers make informed financial decisions, delivering more accessible and tailored support while staying within evolving regulatory expectations.”

Who was involved?

“The call brings together fintech entrepreneurs, financials services and academia, who are all tackling some of the biggest challenges in financial services today.”

Let’s hear from one of the Fintech founders pitching today to hear their side of the story. Dia Banerji, founder of Cherpa.ai:

Dia, you’ve just done your pitch – how did it go?

“I was first up, which always adds a bit of pressure, but it felt good. The presentation went well. Most importantly, I was able to clearly tell the story of why Cherpa.ai exists.”

What was your pitch addressing?

“Cherpa.ai is an AI money coach that delivers hyper-personalised financial education. The pitch focused on the huge gap before financial advice – helping people build awareness, understanding, and confidence about their money, so they’re better prepared to make decisions.”

What are your hopes for the result?

“I’m really excited to be part of this cohort and would love to work more closely with some of the sponsors. Beyond that, it’s about being part of a wider fintech community, learning from others, and helping Scotland, and ultimately people everywhere, build more confidence and connection with their money”

And on that note, let’s hear from Kate Murray who works for Scottish Widows as part of Lloyds Banking Group.

What has struck you about the pitches that you’ve heard today?

“What’s really struck me is the breadth of innovation on show – from fintechs tackling very niche, complex problems to those covering the entire end-to-end customer journey. It’s impressive what they’ve delivered in such a short time, and the quality of the user interfaces has really stood out to me. They’re slick, well thought-through, and genuinely exciting to imagine working with as we design our future journeys.”

What does AGBR mean for your firm, and why does this call matter?

“For us, AGBR is about helping more people secure their financial futures, in a way that aligns with our wider purpose of helping Britain prosper. There’s a real advice gap in the industry, and a big void in the middle where people don’t know what to do next — how to save, how to prepare for retirement, or how to make better decisions. We see innovation and new solutions as a way to bridge that gap, giving people the clarity and confidence to take the next step towards a more prosperous financial future.”

“The Innovation Call matters because we’re always reviewing how we change, innovate, and go faster. And sometimes, being part of a big organisation slows us down. Bringing in outside thinking, new technology, and completely different perspectives helps us bridge that and move quicker.”

And let’s finish with Christine Sinclair, Programme Director for FRIL at the University of Strathclyde.

Christine, that was quite a day…anything else that might surprise us about an Innovation Call?

“It doesn’t stop here. There are many layers to an Innovation Call. While the successful fintechs will go on to partner with a financial services firm and grow their businesses, the research by the academics involved in the call is captured in White Papers to support industry learning.“

“The insights also shape current and developing skills programmes hosted by the University of Strathclyde and the University of Glasgow. These are aimed at helping people develop the skills they need to adopt new technologies responsibly, whether that’s AI, data, digital transformation or ESG reporting.”

Sounds interesting? You can hear more about those courses in this interview with Christine.

So what next for the fintechs who took part?

Now, the wait begins! Next week the judges will decide which teams will be awarded grants of up to £50,000 to develop, scale and implement their ideas.

But the journey doesn’t end there. Beyond the winners, many of these ideas are likely to spark further interest, partnerships and pilots in the months ahead.

We’ll keep you posted.

In the meantime, if you’d like to find out more about the work of the Financial Regulation Innovation Lab, please contact us at FRIL@fintechscotland.com.

About FRIL

Why Upskilling can’t wait: Building Smarter Skills for a Smarter Financial Future

Q&A With Christine Sinclair

Programme Director, Financial Regulation Innovation Lab (FRIL), University of Strathclyde

Financial services is undergoing one of the most significant periods of change in decades. Technology is advancing at pace, new regulations are emerging, and organisations of every size are wrestling with the skills needed to keep up. The Financial Regulation Innovation Lab (FRIL) was created as a catalyst to help the sector respond, to support better outcomes for consumers, strengthen the industry, and enable fintech entrepreneurs to innovate with confidence.

Central to this mission is a progressive skills development programme delivered in partnership with the University of Strathclyde and the University of Glasgow. Together, they’re building a portfolio of Microcredentials (which gain academic credits), short courses and executive education that help people across financial services understand, adopt and apply new technologies responsibly and effectively.

Christine Sinclair, Programme Director, FRIL, University of Strathclyde

Here, Christine Sinclair, Programme Director for FRIL, explains why this work matters, and why now is the time to invest in the future skills of the sector.

Q 1 – Hello Christine, let’s start with the big questions first… what challenge are you addressing here, and why does this matter?

A 1- When you look across financial services, the message is the same everywhere: the pace of technological change is relentless, and people and industry need to keep up. The biggest example right now is generative AI. There’s a real desire to understand it, but also a lot of uncertainty.

When you look at the evidence around AI adoption, the barriers are strikingly consistent. Many organisations hold back because they don’t have the skills or confidence to implement it safely. They don’t fully understand the risks, or they’re concerned about data management and governance. A lot of this is driven by the hype cycle, which can be overwhelming.

So the challenge we’re addressing is simple but vital: helping people develop the skills they need to adopt new technologies responsibly, whether that’s AI, data, digital transformation or ESG reporting. And what we’re doing is demand-led, we’re not creating courses and hoping people want them. We’re listening closely to what financial services and fintechs tell us they need.

Interestingly, the needs differ. Fintechs tend to be highly technical but often need more support with leadership, negotiation and change management. Larger financial institutions have deep organisational knowledge, but they often need help with the technical understanding. So it’s about supporting both sides, and helping both work together…

…and it’s all really important because with the speed of change, the biggest risk is to do nothing.

Q 2 – Who are the courses for?

A 2 – They’re for anyone in financial services, from credit unions to fintechs and large institutions to board-level executives.

A lot of participants join because they want to refresh their own skills. Others are sent by employers who know they need to build capability quickly. And we’re seeing more early-career professionals who want to understand the fundamentals of digital transformation or AI as they move into new roles.

What’s important is that the courses meet people where they are. You don’t need a technical background. You just need curiosity and a willingness to learn.

As a result of the success of the programmes developed for financial services, we’ve also welcomed people from energy and health sectors where the challenges are very similar.

Q 3 – What’s unique about this particular skills offering?

A 3 – The comprehensiveness. There are plenty of short “how to prompt engineer” or “what is GenAI” sessions out there, but they tend to cover only one slice of the picture. FRIL’s courses build from fundamentals all the way through to practical application in financial services.

For example, our AI microcredentials are designed to allow learners to understand and engage with AI in a structured and progressive manner. Focussing on core concepts and techniques, such as machine learning and large language models, but also, cover risk, governance and data science, and communication skills, whilst including real industry use cases which demonstrate practical application. For executives, we even include topics such as decision-making through AI driving business insights in the boardroom, AI Governance and compliance, as well as AI in Enterprise Risk Management and developing strategies to implement and scale GenAI.

Everything is designed to be flexible and accessible. You can learn in your own time, supported by lecturers who track your engagement and are available when you need help. It’s comprehensive without being overwhelming.

Q 4 – What kind of courses are currently being offered?

A 5 – We’ve developed microcredentials in Digital Transformation, ESG for Executives, and a full AI literacy suite, from beginner to advanced, plus an executive-level course. And there are programmes in AI & RegTech, and ESG Leadership.

We originally planned to deliver two microcredentials. We’ve delivered ten due to demand. Seven at Strathclyde, two at Glasgow, and one short course through the UK Government’s Help to Grow programme at Strathclyde. Our microcredentials are accredited and can stack towards a postgraduate qualification, so learners build credits over time.

For those who don’t wish to earn credits, we are now looking at awarding digital badges so learners can showcase their acquired skills on LinkedIn or their CV.

Q 5 – What format do the courses take?

A 5 – In general, course delivery is blended. Each week, participants complete short online lectures, which are no more than 15 minutes each. This, along with reading and other practical activities helps them apply what they’ve learned and typically brings the total up to around two to three hours per week.

We run online inductions, drop-in webinars and a final in-person consolidation session on campus. That’s where the learning community really comes together. Everyone arrives with the same foundation and can share what’s worked in their own organisations.

Our blended delivery provides a safe space to learn at your own pace and without judgement.

Q 6 – Can you share a story of someone who’s been on a course, and the impact it’s had?

A 6 – One participant told us he’d never been to college or university. He came straight into work and never had the opportunity to study formally. He was the first person in his family to ever take a university course, and it was our Digital Transformation programme.

Something clicked for him. After completing the course, he asked what else he could do. He’s now enrolled on a graduate apprenticeship degree. Another participant has gone on to apply for an MBA. So these short courses aren’t just about skills, they can genuinely spark lifelong learning.

Short courses are powerful…they can change the course of someone’s career.

Q 7 – How does FRIL create the ‘engine’ that drives these skills programmes?

A 7 – Our skills work is tightly linked to the Research and Innovation strands of FRIL. The research teams produce white papers, and we analyse common themes. We attend FRIL’s Innovation Calls, listening to pitches from fintechs proposing solutions to challenges highlighted by industry partners. That’s where you hear the real issues, things like: AI, data, legacy systems, regulatory change.

We also have a skills subgroup with finance industry representatives who act as a sounding board and help us to shape course priorities. Everything is demand-led, grounded in industry conversations, networking and skills gap analysis. We’re supporting a sector that contributes hugely to Scotland’s economy, and we want to get this right.

We’re not just creating courses, we’re listening to what the sector is telling us it needs.

Q 8 – How can what we’re doing here influence learnings across other sectors?

A 8 – While the focus here is financial services, the content isn’t always sector-specific, which means we can swap out case studies to fit different industries. We’re already seeing learners from energy and health joining our courses. Because the pace of change is constant everywhere, the need for digital and AI literacy applies just as much outside financial services.

And the short video-based model means we can keep content fresh. If something changes in AI, which it does daily, we can re-record a section quickly.

Q 9 – While this might be our final question today, this really is just the beginning. What might we expect to come?

A 9 Visibility is a big focus. We’re launching the FRIL Skills Academy, which brings everything together including upskilling, reskilling, executive education, and early-career engagement. It will guide people through learning pathways based on their needs, offer microcredentials, and connect with the student FinTech societies across Strathclyde and Glasgow. There will also be the opportunity to engage with either University to gain support for projects, knowledge transfer partnerships and PhD@Work.

Longer term, we want to work more closely with colleges to support talent pipelines, widen access and create opportunities for people who wouldn’t normally enter higher education. We’re also exploring mentoring programmes, internships guest lectures and masterclasses.

This is about us all embracing the future together. When you engage with the universities through FRIL you’re part of a learning community for the long term.

What next?

If you’d like to find out more about FRIL’s skills programmes, please visit:

- Financial Regulation Innovation Lab (FRIL) – Skills development.

- 10‑credit Online Microcredentials from the University of Glasgow.

The FRIL Skills Academy will be launched at the end of January 2026.

About FRIL

New Year, New Skills: 10‑credit Online Microcredentials from the University of Glasgow

Whether you’re looking to enhance your skills or develop your team, short online courses are a fast, flexible way to upskill and advance your career. The University of Glasgow is offering 10‑credit online microcredentials to help you build in‑demand capabilities quickly, with start dates in January and February 2026. Explore the options below.

Project Management

Start-Date: 26 January 2026

Project management is an essential business tool that is being adopted worldwide. It is also a growing and highly sought-after profession, with the Project Management Institute estimating it to have grown by $6.61 trillion by the end of 2020. In this microcredential course, you will gain a deep understanding of practical project management skills using real-world case studies. You will examine the entire project lifecycle, from feasibility to closure, and explore important topics such as managing people, setting priorities, working to tight deadlines, developing schedules and managing risks.

Intro to Business Analytics

Start-Date: 26 January 2026

The Introduction to Business Analytics: Empowering Decision-Making Through Data course is designed to introduce learners to the concepts, techniques, and methods used to analyse an organisation’s operational performance and enable them to make informed business decisions using business analytics skills. The course will discuss the different sources of data and information necessary for analysis, and how to turn an understanding of business analytics into a competitive advantage. At the end of this course, learners will understand the challenges in sourcing data in today’s internet enabled world, what we can/cannot expect the data/information to tell us, and how we can analyse what we have to the best effect. Learners will also be introduced to the data visualization techniques to maximise the impact of data on decision-making, presentation, stakeholder engagement and stakeholder buy-in.

Business Financial Management

Start-Date: 26 January 2026

This course examines the role of accounting and finance in organisational decision‑making, control and performance management. It offers a broad overview of the function and introduces practical skills for interpreting and using financial information and reports to support these activities.

AI & RegTech in Financial Compliance

Start-Date: February 2026 (TBC)

This course provides a practical approach to understanding and applying Artificial Intelligence (AI) and Regulatory Technology (RegTech) in financial compliance and risk management. It introduces the fundamentals of AI capabilities, the evolution of RegTech, and the regulatory and governance frameworks that shape compliance across banking, fintechs, and the wider financial ecosystem.

ESG (Environmental, Social and Governance) Leadership

Start-Date: February 2026 (TBC)

This course aims to introduce recent graduates and early career professionals in the financial services and financial technology sectors to the areas of ESG policy and compliance, data and analysis requirements, and organisational and strategic opportunities. By focussing on ESG leadership, the course aims to equip learners with the practical knowledge, skills and capabilities to evaluate the strategic positioning of their organisation and to develop an ESG plan for their organisation.

Discount codes

As a valued member of the FinTech Scotland community, and with support from the Financial Regulation Innovation Lab (FRIL), you can use the following discount codes:

- AI & RegTech course: use code ‘FRIL’ at checkout. Standard price £499; FinTech Scotland members pay £349 with this code.

- ESG Leadership microcredential: use code ‘ESGFriends’ at checkout. Standard price £599; FinTech Scotland members pay £399 with this code.

Navigating the Advice Frontier – Supporting informed consumer decision making.

The Future of Wealth Innovation Call launches.

This challenge is about finding new ways to support consumers in making informed financial decisions, delivering more accessible and tailored wealth support, while staying within evolving regulatory expectations.

This Innovation Call sees 21 cutting-edge fintech businesses selected to collaborate directly with leading financial institutions, professional services firms, regulators and academics using data-driven innovation that can bridge the “advice gap” an improve outcomes for millions of customers.

This is our sixth Innovation Call and will address challenges affecting the sector including:

Launch and next steps

The programme officially launched on 13 November at PwC’s Glasgow offices, where the fintechs met with industry leaders and academic experts to kick-start their collaborative journeys.

Over the coming weeks, participants will take part in workshops and deep dive insight sessions designed to refine their solutions and align them with real-world industry needs. The most promising ideas may also receive grants of up to £50,000 to accelerate development

Who is involved?

The Future of Wealth Call is hosted by the Financial Regulation Innovation Lab (FRIL) in partnership with SuperTech West Midlands

We are proud to be working with 10 strategic partners - PwC, Barclays, Lloyds Banking Group, Sopra Steria Financial Services, NatWest Group, M&G, BNP Paribas, Dudley Building Society, Wesleyan and Standard Life – alongside academic partners at the University of Strathclyde and the University of Glasgow. Their combined expertise ensures that innovation is rooted in both cutting-edge research and real-world regulatory priorities.

We are also delighted to partner with Growth Builders to support in the delivery of this programme.

Our 21 successful Fintechs include:

Afternoon Finance, Alessia, Alethica, Amplifi, Aveni, Aventur Wealth, CherpaAI, Complia, Doconomy, Etcho, Finspector, Glimzer, Guiide, InicioAI, Iress, Open Book Analytics, Planda, Snowdrop Solutions & Stratiphy [joint entry] and The Wisdom Council & DocStribute [joint entry]

Find out more about each of the fintechs in our fintech brochure.

What next?

If you’ve liked what you’ve read, follow us on LinkedIn where we will keep you updated. Or, for more information about getting involved in future innovation calls contact us at FRIL@fintechscotland.com