Rethinking cross‑border payments: Market Town’s Bitcoin approach from Edinburgh

Written by Henry Murray-Smith, Market Town

“Imagine a contract where every January first, forever, I will give you one dollar. You can sell and transfer this contract. You want to sell this contract to Charlie. How much does he pay?”

This question is really asking “why is a dollar today worth more than a dollar tomorrow?” and is as fundamental to finance as a writer of the English language starting on the left hand side of the page. Charlie buys the contract for about eight dollars.

In 2021, five years into an informal financial education, I stood in the kitchenette of a data centre waiting for tea to brew, closing a wealth management textbook from the CISI (the Chartered Institute for Securities and Investment). Concluding my first reading I was more certain finance was, at its most favourable angle, a hot mess. And for all the detail and breadth of my education, I still had no idea what money was.

Some years later, the best definition I can muster is that money is part of human nature. It’s a phenomenon that appears with any collection of people, expressed through technology. My favourite example is cigarettes in prison, because they’re so perfectly divisible and scarce. They also have a practical purpose: you *can* save them to trade another day, or smoke one in a moment of reflection. But step outside prison and cigarettes are no longer tender. A shopkeeper will no sooner trade cigarettes for groceries than they would accept a nugget of gold.

When investigating money, the inevitable subject of Bitcoin appeared. My cynicism only began to erode reading Fidelity’s ‘Bitcoin First Revisited’ which explains why Bitcoin, not the thousands of other ‘web3 projects’ satisfies the properties of money to a greater degree than fiat currencies and gold. I still despised its energy consumption, because I hadn’t connected the dots that, if electricity is almost all of your running costs, finding stranded and renewable energy would be incentivised.

I also hadn’t considered the energy cost of the current system: millions of offices, bank branches, and autoteller machines serviced by vehicles – that system full of failure points, gatekeepers and opaque fees. So what backs Bitcoin? Even if fiat currency isn’t backed by gold (anymore) it’s backed by a government’s ability to raise taxes and sell bonds. Well, it takes a lot of energy to mine one Bitcoin, almost a hundred thousand US dollars of electricity. It can’t be created without significant cost. Saying it’s backed by energy doesn’t exactly stir the soul, but it is, and the market values that captured energy, or that Bitcoin, very highly.

So why wasn’t there a browser for the Bitcoin network, I wondered? Why didn’t some clever developer build a portal like so many thousands of startups during the early days of the internet, which had Mosaic and Netscape? The sad truth is that many of the innovation dollars went to adjacent crypto projects pretending to be superior to Bitcoin, optimised for different things, and now they’re all fading. Only Bitcoin persists, everything else dies and, yet, few use it as currency.

Today, half a billion people own Bitcoin, most indirectly, and it’s one per cent of global money supply. Numbers like these inspire us to build the future of payments, banking and financial services.

After eighteen months of product development, our mobile app is being designed in California by Alexander Lambert, who led the design, often from day one, of Friendster.com, car sharing platform Getaround.com, and Airkit.com (acquired by Salesforce).

To explore our roadmap beyond global payments, say hello@market.town

Learn more about Edinburgh fintech Market Town and its Bitcoin‑powered cross‑border payments platform.

Regulatory Insights: September 2025 – Balancing Growth, Innovation and Consumer Protection

Our strategic partner Pinsent Masons has released the September edition of its FS Regulatory Risk Trends update, highlighting the latest developments shaping the UK regulatory landscape.

This third edition of 2025 comes at a time when government and regulators are under pressure to balance economic growth, innovation and competitiveness with strong consumer protection and the integrity of the financial system.

FCA focus: innovation with safeguards

The FCA continues to implement its five-year strategy, with an emphasis on innovation and efficiency. This quarter’s insights point to several areas of interest:

- AI regulation and adoption: the FCA is engaging with the opportunities and risks around AI in financial services.

- Payments innovation: consultations on contactless payments and targeted support show a regulatory push for consumer benefit and wider adoption.

- Market infrastructure: the FCA has approved the first PISCES platform, a milestone for digital settlement systems.

Wider government initiatives

Alongside the FCA’s actions, HM Treasury is consulting on significant changes to the redress framework overseen by the FCA and the Financial Ombudsman Service (FOS). These proposals could have a major impact on how firms manage complaints and consumer redress.

Risks on the horizon

While innovation is encouraged, firms also face heightened scrutiny. Recent regulatory activity includes:

- Market reviews into retail insurance, digital customer journeys and premium finance.

- Ongoing exploration of the future of cryptoasset regulation.

- Criminal prosecutions linked to financial crime.

- Preparations for an industry-wide redress scheme following the Supreme Court motor finance case in August.

To discover the full update click here.

Scotland’s Evolving Coworking Landscape: Glasgow, Edinburgh & Aberdeen Lead the Way in Q2

As Scotland’s fintech and innovation economy continues to thrive, so too does its flexible office infrastructure by offering agile, scalable workspaces that meet the needs of growing startups, enterprise teams, and remote workers alike.

According to CoworkingCafe, Scotland is now home to 279 coworking spaces, placing it firmly on the map as one of the UK’s most active regions for flexible work. The report draws on proprietary July 2025 data and offers in-depth insight into inventory levels, subscription pricing, and operator presence across the UK and Ireland.

| Scotland’s Coworking Snapshot: Q2 2025 Total inventory: 279 coworking locations National median prices across Scotland: Monthly memberships: £150 Day passes: £23 Virtual offices: £95 Meeting rooms: £25/hour Top Scottish operator: Wasps, with 18 locations |

As fintech companies continue to scale and decentralise, demand for high-quality, flexible workspace solutions is rising outside of London and the South East. Scotland’s coworking scene — especially in Glasgow, Edinburgh, and Aberdeen — offers a cost-effective, collaborative alternative to traditional office setups. Let’s take a closer look at how these top-performing coworking hubs are shaping the future of flexible work in Scotland.

Glasgow: Scotland’s Largest Coworking Market

With 61 coworking spaces, Glasgow ranks #4 in the UK overall and stands out as Scotland’s leading hub for flexible office solutions. The city combines affordability with an increasingly sophisticated offer — making it attractive to both startups and established businesses.

- Monthly memberships: £160 — below the UK median (£180), but slightly above the Scottish median (£150)

- Day passes: £23 — tied for the most affordable in the UK

- Virtual offices: £119 — significantly higher than the national and Scottish averages

- Meeting rooms: £23/hour — one of the UK’s most cost-effective options

Edinburgh: High Demand, Premium Pricing

Edinburgh ranks #5 nationally, with 55 coworking locations offering a premium experience in the heart of Scotland’s capital. The city’s thriving fintech sector and knowledge economy are reflected in above-average pricing.

- Monthly memberships: £192 — well above both Scottish and UK medians

- Day passes: £30 — a capital-level price, in line with greater London

- Virtual offices: £99 — slightly above the UK and Scottish averages

- Meeting rooms: £40/hour — among the most expensive in the UK outside of London

Aberdeen: A Growing Presence in the UK Top 15

With 26 coworking spaces, Aberdeen ranks #11 in the UK and completes Scotland’s trio of cities in the national top 15. Its coworking market is maturing steadily, balancing competitive pricing with national benchmarks.

- Monthly memberships: £160 — on par with Glasgow

- Day passes: £28 — higher than average, reflecting solid demand

- Virtual offices: £95 — matching both the UK and Scottish medians

- Meeting rooms: £30/hour — aligned with the national average

For a deeper look at coworking trends across the UK and Ireland — including operator rankings, detailed city-level data, and full pricing breakdowns — explore the full Coworking Industry Report for Q2 2025.

Photo by CoWomen: https://www.pexels.com/photo/woman-using-laptop-photography-2041398/

Navigating Imposter Syndrome in Tech Leadership Roles

Imposter syndrome at work can affect anyone, regardless of how senior they are or their impressive professional background. Even in the fintech world, where innovation and confidence are prized, self-doubt can manifest and affect high-performing leaders.

Imposter syndrome can emerge when leaders are confronted with the dual pressures of high expectations and rapid industry evolution, particularly in fintech, where technology moves at lightning speed. Imposter syndrome is more common than we often acknowledge, and knowing you’re not alone can be helpful in taking the first step.

Spotting the Signs of Imposter Syndrome

There are some tell-tale symptoms fintech leaders should be mindful of, particularly as they step into new roles or face significant challenges:

- Persistent Self-Doubt: Despite proven achievements, you may question whether you’re qualified enough to lead your team. This is especially prevalent in a field like fintech, where the technology and regulatory landscapes are constantly shifting.

- Attributing Success to External Factors: Many leaders downplay their role in success, attributing achievements to “luck,” “good timing,” or team efforts, sidelining their own contributions.

- Fear of Failure: The high stakes in innovation can cause hesitation in leaders, stalling key decisions out of fear of public mistakes.

- Difficulty Accepting Praise: Praise can feel uncomfortable, as though you haven’t earned it or it is not deserved, even if the results show otherwise.

- Feeling Like a Fraud: Despite scaling teams or raising funding rounds, a lingering fear persists that one day, “the truth” about your perceived inadequacies will come out.

What Drives Imposter Syndrome

The fast-paced, competitive environment in tech can often amplify feelings of inadequacy. When this is accompanied by a top-down management style, this can unintentionally exacerbate imposter syndrome. Leaders operating in progressive firms find value in adopting a coaching style.

Equally,a drive for perfection, common among tech leaders, can fuel imposter syndrome. In fintech, teams may be handling critical financial solutions or compliance-heavy challenges, which can make leaders feel overwhelmed by the need for flawless execution.

For many, a lack of a strong support systems can also drive that overwhelming feeling. While this is certainly improving, many tech organisations have limited opportunities to openly discuss vulnerabilities. Peer groups become a value asset for everyone, but especially for those feeling a sense of loneliness in their leadership role.

Recognising Growth vs. Imposter Syndrome

It’s important to distinguish between natural discomfort from stepping into a new, challenging role and true imposter syndrome. Feeling unsettled during periods of growth can be a positive sign. It means you’re stretching yourself outside of your comfort zone.

However, if self-doubt persists long-term or intensifies despite external success, it may signal deeper imposter syndrome that needs addressing.

I’ve worked with lots of highly capable leaders willing to challenge themselves to move beyond their existing comfort zone. Feeling off balance and/or a sense of discomfort is normal and to be expected when you’re growing. But if you’re still doubting yourself long after the wins stack up, that’s not humility, that’s imposter syndrome in disguise.

Strategies for Managing Imposter Syndrome

So how do you deal with the challenges of imposter syndrome? It doesn’t have to impede your leadership. Here are a few practical steps to combat it:

- Shift Your Mindset: Transitioning to a leadership role requires a company-wide perspective rather than just focusing on your niche. Spend time understanding how other departments, including engineering or compliance, align with the overall vision. Spend the first few meetings observing rather than contributing. Listen to understand team dynamics and alignments.

- Lean Into Coaching: Don’t rely solely on your current expertise. Coaching can help uncover blind spots in leadership and offer clarity, and provide a sounding board. In-person executive coaching is a powerful tool for deep personal growth. Complementing this with innovative solutions like AI leadership coaching apps, make coaching more accessible, offering real-time support across a wide range of scenarios and providing around-the-clock guidance when you need it most.

- Delegate and Empower: Avoid the trap of micromanaging as an enterprise scales. Effective delegation helps leaders maintain focus on high-value priorities while teams feel trusted with ownership of responsibilities.

- Build a Network: Connect with external leaders, both within and outside the world of FinTech. Whether it’s meeting other founders or attending conferences, these connections inspire new ideas and reinforce how widespread certain challenges are in the sector.

- Set Realistic Expectations: Startups and scale-ups thrive on innovation over perfection. Mistakes will happen, but they often lead to invaluable lessons. Start small, iterate, and improve.

- Reframe Success: There may be a mindset shift required, from considering the volume of tasks completed on a given day, to how, as a leader, you are contributing towards long term strategies.

Avoiding the Comfort Zone Trap

One of the biggest risks for leaders in any sector battling imposter syndrome is retreating to the comfort zone of their previous roles. Whether it’s over-involvement in day-to-day technical work or doubling down on tasks better suited to others, this behaviour can:

- Frustrate teams by signalling a lack of trust.

- Undermine broader strategic goals.

- Increase feelings of inadequacy, as managing every detail cannot solve complex challenges.

This can be a difficult shift. It’s common to like hanging on to the things we’re great at, it’s comforting, and can be a security blanket. But growth demands a shift. The real leadership move is letting go of what you can do well and stepping into what your company actually needs from you now.

Leaders’ Takeaway

Imposter syndrome may not discriminate, but it’s navigable. By acknowledging it, seeking support, and adjusting your focus from perfection to progress, leaders can drive innovation and growth without being derailed by self-doubt.

Imposter syndrome comes with the territory, particularly in tech. But when you reframe it as part of a learning experience rather than a limitation, you’ll find that it’s not an obstacle but a stepping stone.

Kirsty Bathgate, accredited executive coach, founder of gearingforgrowth.com and co-founder of www.bravyn.ai

Photo by Tim Gouw: https://www.pexels.com/photo/man-in-white-shirt-using-macbook-pro-52608/

Dealing with deal fatigue: managing your finances after selling a business

Selling a business can be both financially rewarding and emotionally exhausting. After months of negotiations, scrutiny and stress, it’s common for many entrepreneurs to experience ‘deal fatigue’. This is a state of mental and emotional burnout that makes it difficult to immediately tackle personal financial planning.

Yet, with potentially millions in proceeds at stake, it’s crucial to protect your wealth while giving yourself space to reflect and plan your next steps. Here’s how to strike that balance.

Take time to reflect

The period following a business sale is ideal for pausing and reassessing your goals. Beyond the financial windfall, the sale often marks a major lifestyle shift. Before making long-term financial decisions, it’s important to understand what you want your future to look like.

Rushing into investments or commitments without clarity can lead to costly mistakes or the need to unwind decisions later.

The four-box framework

To help navigate this transitional phase, a structured approach can provide both security and flexibility. One effective method is the ‘four-box framework,’ which segments your funds based on short and long-term needs:

1. Instant access

This is your emergency fund. It’s liquid, safe and ready for unexpected expenses. Typically held in an instant-access savings account, it won’t earn much interest but offers peace of mind. Just be aware of the £85,000 Financial Services Compensation Scheme (FSCS) protection limit per person, per bank, were the bank to fail. Note that FSCS protection does not apply to NS&I, but these accounts are guaranteed by HM Treasury.

2. Lost income replacement

Post-sale, many entrepreneurs see a drop in regular income, especially if they stay on in a reduced capacity. This box covers the shortfall, ensuring you can maintain your lifestyle while you transition. For instance, if your income drops from £200,000 to £80,000, this fund bridges the gap.

3. Capital expenditure

This box is for planned expenses such as celebratory purchases, tax bills, mortgage repayments or other large outlays expected in the next few years. Setting aside funds for these ensures they’re accounted for without disrupting your broader financial strategy.

4. Long-term investments

This is where your future wealth grows. However, it’s wise not to rush into investment decisions immediately after a sale. Your risk tolerance may be temporarily skewed, and markets can be volatile. Taking time to develop a thoughtful investment strategy is key. Investment firms also fall under FSCS protection, but this is only applicable if the firm fails, not if investment underperform. Remember, investments carry risk and you could get back less than you invested.

Using a gilt ladder

To manage these medium-term needs (such as those outlined in points two and three earlier) while avoiding the risks of equities or the erosion of cash by inflation, a ‘gilt ladder’ can be a smart solution. This involves purchasing UK government bonds (gilts) with staggered maturities that align with your income or capital needs.

For example, if you need £120,000 annually for the next three years, you can build a gilt portfolio that pays out that amount each year. These can also be adjusted for inflation. Additional gilts can be used to cover future expenses or serve as a temporary holding place for long-term investment funds.

While gilts are generally lower risk than equities, their value can fluctuate with interest rate changes, especially those with longer maturities. That’s why it’s important to seek professional advice when building a gilt ladder or exploring other investment options.

Creating space to plan what’s next

Selling a business is a major life event. The financial gain is significant, but so is the emotional impact. A structured approach like the four-box framework helps you secure your wealth while giving you the breathing room to consider your next chapter, whether that’s retirement, a new venture, or something entirely different.

Article written by Alison Fitzsimons at Evelyn Partners – alison.fitzsimons@evelyn.com

Photo by Photo By: Kaboompics.com: https://www.pexels.com/photo/black-calculator-on-top-of-paper-4491441/

Crypto, Code, and Kilts: Scotland’s FinTechs Eye the Metaverse

The metaverse is not the internet extended online; it’s a virtual, always-present universe where users can engage and with other users, and with the world, in real time. Decentraland, The Sandbox, and HTC Viverse are some of the earliest innovators, providing virtual worlds for social interaction, gaming, business, and entertainment. Platforms are growing exponentially, with virtual real estate markets alone reaching $1.4 billion in 2022, 180% year-on-year.

These virtual assets fund this new metaverse economy. The user payments in these areas need to be preceded by secure, scalable, and efficient financial services. Scottish fintech firms can bridge this gap at this point.

Why Scottish FinTechs Ought to Take Notice

Scotland is a natural candidate for fintech metaverse leadership for several reasons:

- Innovation heritage in finance and technology (host to the Bank of Scotland, one of the oldest in the world).

- Edinburgh and Glasgow as global fintech hubs.

- UK pro-business policies and regulatory sandboxing possibilities.

- Solid academic foundation facilitating blockchain, AI, and quantum computing R&D.

Harnessing these strengths, Scottish fintechs can offer the infrastructure to secure, grow, and make the metaverse economy accessible.

Scottish Fintech Opportunities in the Metaverse

- Facilitating Seamless Payments

Metaverse legacy payment systems also break down due to latency, security, and interoperability. Scottish fintechs can create and deploy metaverse-native payment solutions. Some of them are:

- Cryptocurrency Payment Gateways: Enabling users to pay in cryptos like Bitcoin, Ethereum, or stablecoins.

- NFT-Based Transactions: Enabling users to buy and sell digital assets using NFT marketplaces.

- Cross-Platform Payment Systems: Developing cross-platform transaction solutions.

With blockchain technology, such payment systems are able to provide transparency, security, and efficiency in the midst of the virtual economy’s inherent challenges.

- Digital Asset Management

The boom of the digital asset metaverse demands strong management solutions. Scottish fintechs can create platforms upon which users can store their digital assets securely, track, and manage them, for instance:

- Digital Wallets: Empowering users to be able to benefit from secure storage of cryptocurrencies and NFTs.

- Asset Tracking Tools: Providing information and insights into the value and performance of digital assets.

- Portfolio Management Services: Helping people to diversify and manage their portfolios of digital assets.

These services can make people experts in decision-making and achieving optimum advantages from their digital assets.

- Virtual Financial Services

With the maturity of the metaverse comes the maturity of the need for conventional financial services within such virtual environments. Scottish fintechs can be at the forefront in being innovative by providing such services as:

- Virtual Banking: Virtual branch establishment through which consumers can access banking services in the form of loans, savings accounts, and advice on finances.

- Insurance Products: Creating insurance products specific to the virtual environment and assets.

- Investment Platforms: Establishing venues through which users can invest in metaverse property, digital artwork, and other assets of the metaverse.

By incorporating these services into the metaverse, Scottish fintechs will connect mainstream finance to the virtual economy.

Strategic Benefits of Scottish Fintechs

- Organic Financial Ecosystem

Scotland has a well-established financial services industry with Edinburgh and Glasgow being key hubs for banks, insurers, and investment companies. This established environment is perfectly suited to allow fintechs to grow and thrive in the metaverse.

- Favorable Regulatory Environment

UK regulatory environment provides reassurance and relief to fintech firms, especially those dealing with new-generation technologies such as blockchain and cryptocurrency. Such a facilitative climate will assist in smoothening the spread and roll-out of financial products derived from the metaverse.

- Talent and Innovation Access

Scotland has a robust tech community and top-class universities, adequate access to leading talent, and frontier-level research. Access to the latter pool is most critical in creating innovative solutions fit for the metaverse.

- AML, KYC-as-a-Service, and Compliance

Meta-mode operations pose significant regulatory issues, particularly issues of money laundering, identity theft, and jurisdictional compliance.

Scottish fintechs with regtech experience can provide:

- AI-driven transaction monitoring platforms for virtual economies.

- Avatar-based KYC services using facial recognition or voice biometrics.

- Decentralized identity systems that are GDPR- and UK data protection legislation compliant.

Fintech providers such as Symphonic Software (policy-based access control) or The ID Co. (financial identity specialists) could leverage their products into this environment.

- Decentralized Finance (DeFi) and DAOs

Decentralized finance—DeFi—is one of the pillars of the metaverse ecosystem. It allows trustless, peer-to-peer financial systems without brokers or banks.

Scottish fintechs can:

- Develop DeFi protocols for lending, borrowing, and staking in metaverse tokens.

- Develop DAO governance platforms for controlling community-owned financial institutions.

- Provide DeFi risk analytics platforms to enable users to evaluate protocol safety.

By connecting with Ethereum-based DeFi or Layer-2s such as Arbitrum and Optimism, these businesses are able to tap into an emerging global phenomenon while taking Scottish fintech IP to the world.

Challenges and Considerations

- Regulatory Uncertainty

The metaverse is ubiquitous, frequently making legacy finance regulation useless. Scottish fintechs need to navigate this intricate regulatory environment to stay compliant and risk-free.

- Security and Privacy Issues

The virtual metaverse online environment is susceptible to cyber attack. Fintechs need to have proper security measures that protect user information as well as financial transactions.

- User Adoption

User adoption can destroy or create financial services in the metaverse. Scottish fintechs need to invest in user education and offer interfaces that are simple to use so that they can enable high usage.

Looking Ahead: The Next Five Years

As the metaverse transitions from experimental to critical, fintech will transition from backend utility to frontline enabler of digital life.

We can expect to see:

- A virtual Scottish stock exchange for digital assets.

- Interoperable digital IDs created in Scotland are used worldwide.

- Tokenized whisky or property exchanged within metaverse marketplaces.

- Avatar-based banking is linked to Web3 wallets and VR headsets.

By 2030, metaverse financial services might be a multibillion-pound industry, with Scotland positioned as a global hub for this emerging economy.

Conclusion

The metaverse represents a new and exhilarating frontier for the digital economy, with unprecedented scope for innovation in financial services. Scottish fintechs, in their cutting-edge capability and nurturing environment, are best placed to spearhead the progression of payment infrastructure capability, digital asset management ability, and virtual financial services fitting for this new virtual world. By embracing these opportunities, Scottish fintechs can spearhead the construction of the metaverse’s finance future.

Author’s Bio:

Druti Banerjee

Content Writer

LinkedIn: Druti Banerjee

Druti Banerjee is a storyteller at heart following the precision of research with the art of words. Druti, a content writer for The Insight Partners, combines creative flair with in-depth research to create words that bewitch. She approaches every piece she does with an academic yet approachable perspective, having a background in English Literature and Journalism.

Beyond the screen, Druti is a passionate art enthusiast whose love of creativity is rooted in the creations of great artists such as Vincent Van Gogh. An avid reader, dancer, and ever-ready to pen down thoughts, always up for binge-watching and chai on repeat. Preacher of the following vision by Vincent Van Gogh, “What is done in love, is done well”, draws inspiration from the realms of art, history, and storytelling to bring to life via writing the rich hues of culture and the complexity of human expression. The aim is to capture the nuance of the human experience—one carefully chosen word at a time.

Mind the Gap: Bridging the UK’s pension divide with digital solutions

The UK pensions landscape is at a crossroads: with 38% of the working-age population under-saving for retirement and 52% of people accessing their pensions without adequate advice, the risk of poor financial outcomes are at an all-time high. Yet, the market is set for huge growth, with defined contribution pension assets projected to explode to £800 billion by 2030.

This is not a new problem, and despite well-intentioned efforts like auto-enrollment from policy-makers and new digital products from providers, there is still a fundamental disconnect; customers lack engagement and understanding in later life planning and financial outcomes.

Solving this challenge presents a significant growth opportunity for providers, but to do so needs a design-led approach focused on deeply understanding your customers through three core elements: Empathy, Engagement and Empowerment. Technology – and particularly AI – of course plays a crucial role, but doesn’t replace the need for empowered advisers. The future will be hybrid: a combination of traditional digital interfaces, agentic AI, and human touchpoints to create hyper-personalised experiences based on an individual’s aspirations, circumstances and preferences.

This whitepaper, drawing on digital partner CreateFuture‘s decades-long experience in the Wealth & Pensions sector, provides a compelling vision for the future of pensions engagement, outlining how a hybrid approach leveraging digital innovation, AI, and empowered advisors can create truly customer-centric experiences and unlock a more secure future for savers.

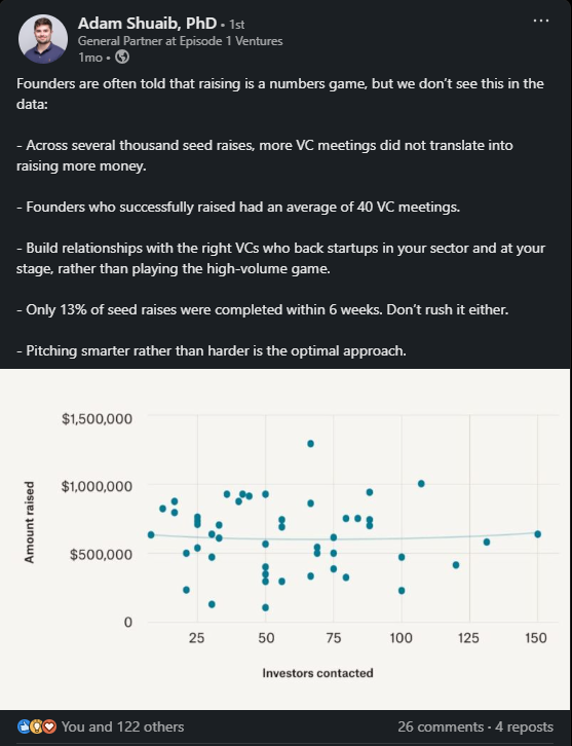

Fundraising? Here’s why you should optimise Quality Outreach Over Quantity

If you’re a founder looking for investment, you have a dilemma.

How much time to invest in identifying and building connections with investors, or to invest in immediate business traction.

Daniel Sawko, co-founder of shipshape.vc, the free to use investment search engine, shares his tips on how to maximise your chances of success.

Focus on Relationship-Building

When raising capital, a common misconception is that contacting more investors improves your chances of success.

This “spray and pray” approach—sending generic messages to numerous potential investors—has gained popularity with the rise of mass emailing tools.

However, analysis by Adam Shuaib, a Data Scientist and General Partner at Episode One Ventures reveals that this strategy is suboptimal.

Beyond a certain point, there’s no increase in the chance of success for the number of investors you contact. Instead, founders should focus on building meaningful relationships with carefully selected investors.

Research Potential Investors

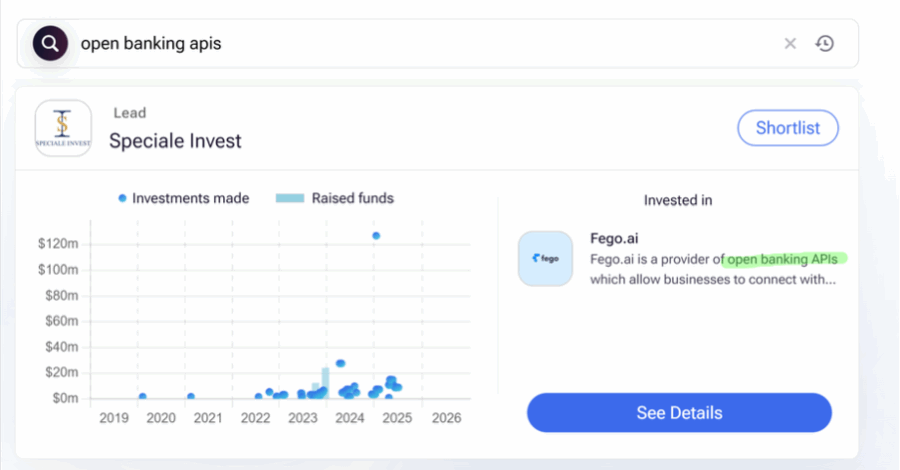

The challenge lies in identifying which investors deserve your attention, as this data is often disparate and poorly organised. This is one of the problems we’re solving with shipshape.vc.

Shipshape.vc aggregates data from over 25,000 funds, identifying the types of companies that they are investing in and the individuals that work at those funds. This enables founders to significantly cut down on the research time it takes to identify relevant investors.

Identify Investors who Understand Your Niche

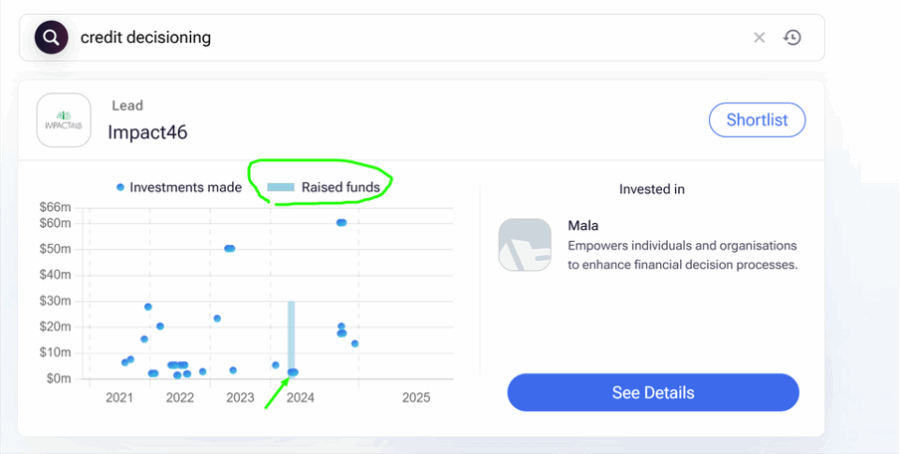

Beyond identifying investors who focus on, for example, Fintech, determine if they understand your specific niche. For example, if you’re developing credit decisioning technology using open banking data, look for investors with experience in related domains.

Be Aware of the Fund Lifecycle

Most venture funds operate on a lifecycle, say of 10 years. Funds deploy capital primarily in their early years to ensure returns before the fund closes. Recently raised funds are more likely to be in an active “planting phase,” while those 5+ years into their lifecycle may be in “harvesting mode”—focusing on existing portfolio companies rather than new opportunities.

Examine Recent Investment Activity

Monitor when funds last deployed capital. A fund that hasn’t invested in the past three to six months might lack fresh capital or be moving to a different phase of its lifecycle.

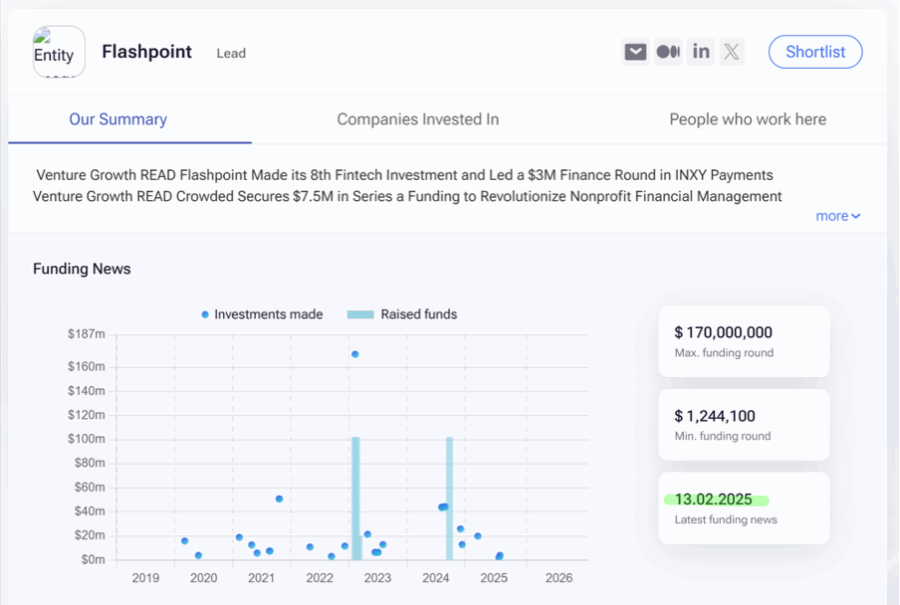

Target the Right Team Members

Research which individuals at the fund understand your space. See if you can deduce from the team descriptions on a fund’s website, their social media, or from a search engine, like shipshape.vc (which will often include team descriptions), with whom at the fund you should be building a relationship.

Approaching someone with the wrong specialisation signals poor research—and how you sell your equity reflects how you sell your product!

Don’t Present Investors with a Transaction aiming at an immediate “Yes” or “No”

Fundraising is not about getting an immediate yes or no. Your company is not a simple product and ‘sales discovery’ applies for potential purchasers of your equity.

Investors will almost always need multiple data points about your company over time before making decisions. The saying of “investors invest in lines, not dots” is real.

Each interaction and update (in-person or via other mediums) helps to build a trendline that either increases or decreases confidence in your venture.

Prioritise Depth over Breadth and Quality over Quantity

This approach requires depth rather than breadth. Similar to bulk mail outreach for selling products or services, founders will struggle to create sufficient data points and depth of relationship with hundreds of investors simultaneously via bulk outreach.

Focus on building relationships with a few dozen carefully selected investors you have determined demonstrate genuine interest in your sector and stage, have dry powder (e.g. via a recent fundraise for the fund) and identify those that can potentially lead a round.

By narrowing your funnel and prioritising quality connections over quantity, you’ll optimise your fundraising process and increase your chances of finding the right investment partners who truly understand and value what you’re building.

Want to share your thoughts?

If you have a question or further thoughts on this article – feel free to reach out to Daniel Sawko on LinkedIn!

Top 3 Strategies for Media and Communications in Fintech

Over the past three years we have seen significant changes, within the fintech sector, in how companies engage with investors, stakeholders, and customers – particularly in their use of digital communication. Through our partnerships, such as the London Stock Exchange, we have witnessed a growing trend toward high-quality virtual and hybrid events. These formats, which combine livestreaming, on-demand content and video conferencing, are becoming standard tools for fintech firms looking for greater transparency whilst maintaining global reach. Companies, now, have more ways than ever to see – and show – themselves through multimedia. To unpack this, we’ll look at three key areas.

Live Streaming – it’s a game changer

In the financial sector, where precision and trust are everything, live streaming may feel like a bold move. The idea of broadcasting high-stakes communications in real-time can understandably raise concerns what if something goes wrong? What if a question catches the C-suite off guard?

But here’s the truth: live streaming isn’t a risk, it’s an opportunity.

When used effectively, live streaming offers an unparalleled level of transparency and authenticity. Whether it’s half-year or full-year results, investor updates, or a capital markets day, going live enables executive leadership to speak directly to stakeholders, unfiltered and in the moment.

This format invites questions, promotes real-time engagement, and fosters trust in a way that pre-recorded or written statements simply can’t match. Stakeholders appreciate being part of the conversation, not just recipients of information. The result? A stronger, more connected relationship between companies and the audiences that matter most.

Pre-Recorded Content – Say it once, use it twice (or ten times).

While live streaming brings immediacy and authenticity, pre-recorded content opens the door to precision, polish, and depth.

For Fintech companies and C-suite executives navigating complex topics, pre-recording offers the ideal environment to deliver clear, considered messages with confidence. Whether it’s a fireside chat, product announcement, or strategic update,

this format allows for multiple takes, seamless editing, and visual enhancements ensuring every word lands exactly as intended.

But the value of pre-recorded content goes beyond production quality.

It’s a powerful tool for repurposing and reach. A single piece can be tailored to different audiences from institutional investors to internal teams while still maintaining time sensitivity. Fireside chats are an excellent alternative to traditional presentation formats. They invite discussion, showcase leadership personality, and provide space for more nuanced opinions and analysis.

Plus, pairing pre-recorded content with a live Q&A session can offer the best of both worlds: the confidence of a polished presentation and the connection of real-time engagement.

For forward-thinking companies, it’s not just about choosing between live or pre-recorded it’s about using both strategically to elevate communication.

Portfolio & Brand Content: Capture Their Imagination

In today’s landscape, the C-suite isn’t just thinking in slides they’re thinking in stories. The most impactful leaders are turning to video as a powerful tool to bring their ideas to life, not just explain them.

Whether it’s showcasing a fintech portfolio, launching a new product, or highlighting future growth areas, video helps translate abstract concepts into compelling, visual narratives. It captures imagination, sparks curiosity, and most importantly sticks. Audiences remember what they can see, hear, and feel. And in boardrooms or investor meetings where attention is limited, a well-crafted piece of brand content can be the difference between passive interest and real engagement.

But this isn’t just about external storytelling. Internally, portfolio and brand videos help teams align behind a shared vision. When introducing new business verticals or rolling out strategic updates, video can communicate ideas clearly, quickly, and with emotional resonance. It helps employees see where the company is going and why it matters.

In short, videos don’t just inform they inspire. They turn complex strategies into memorable stories and make big ideas feel tangible. In a world full of noise, that’s how you make your message land.

At the heart of it, fintech is about innovation and your communications should be too. Whether you’re streaming live, crafting polished pre-records, or telling stories through brand content, the goal is the same: to connect, to clarify, and to captivate.

These tools aren’t just trends they’re opportunities. When used well, they can elevate your message, engage your stakeholders, and bring your boldest ideas to life.

So don’t be afraid to mix formats, try new approaches, and think beyond the slide deck. The future of FinTech communication is already here and it’s more dynamic, more visual, and more human than ever.

Written by Ruairidh Duguid and Robbie Durham – CutAcross ™

Email:hello@cutacrossmedia.com

Photo by Pixabay: https://www.pexels.com/photo/black-camera-zoom-lens-in-close-photography-159442/

Accelerating Action: A Celebration of the FRIL Innovation to Address Financial Crime Programme

Welcome back to our spotlight series celebrating colleagues who are inspiring change and Accelerating Action across the technology sector. This month’s edition focusses on celebrating some of the inspirational colleagues who took part in our recent program of work under the 4th Financial Regulation Innovation Lab (FRIL) challenge – addressing financial crime.

Thank you to all who engaged with us across the programme, and to our spotlighted colleagues for contributing to this important campaign: Christine Sinclair, Skills Programme Director FRIL @ University of Strathclyde; Gill Green, Client Director @ Sopra Steria; Savannah Price, Founder & CEO @ Serene, and Roisin McCarthy, Founder & CEO @ Verifoxx.

Financial Regulation Innovation Lab (FRIL) – Recapping the progress made in the Financial Crime Programme 2025

The FRIL is an industry-led collaborative innovation and research programme with a focus in its 4th call on bringing together industry, regulators, innovators and academia to tackle financial crime and fraud. The challenge was centred around 5 industry led priority use cases and convened 15 Fintech entrepreneurs to work with regulators, academia and industry leaders to develop their innovative solutions. Across the programme, it was a privilege to work with inspirational colleagues across the cluster and we are excited to be celebrating their achievements in this blog.

Across the programme, BT has played a key role in driving collaboration and knowledge sharing across the cluster to tackle financial crime and fraud. This activity kicked off with the launch of the FRIL innovation programme at the BT offices, convening an audience of representatives from regulatory authorities, telco, academia and financial institutions. Continuing to build on this leadership, the BT team also hosted a collaborative podcast series, chaired by Charlotte Moir BT, offering an opportunity to hear from industry leaders across the FRIL – many of whom feature within the Accelerating Action campaign, to share knowledge and best practices in the fraud prevention sector.

“The FRIL is a great opportunity to innovate together to identify solutions”

Paul Taylor, MD Global Banking

Developing the Skills agenda through FRIL – Unlocking AI literacy potential

A key track of activity within the FRIL is skills development, led by our fantastic colleague Christine Sinclair, University of Strathclyde. Christine’s passion and commitment to progressing the skills agenda continues to inspire us to empower colleagues around us, and we are delighted to be sharing further details on the recent launch of the AI Skills Literacy Suite as part of the Women in Tech Campaign:

“AI is transforming the way we live and work at lightning speed, offering new opportunities and challenges – are you keeping up? Whether you’re just starting your AI journey, looking to deepen your expertise, or need a high-impact executive briefing, our AI Literacy programmes are designed to empower professionals at every level.

Unlock your AI potential with Strathclyde Business School by signing up today to one of our five comprehensive micro credentials to earn academic credits and future-proof your career. Find out more herehttps://bit.ly/FRILSkills_ SBS or contact sbs-fril@strath.ac.uk with any questions you may have.”

“Cross-industry collaboration really is key to help us stay ahead…its critical”

Charlotte Moir, Account Manager

We look forward to continuing to celebrate inspirational colleagues across this campaign and will be continuing to publish our monthly blog. If you would like to nominate a colleague to feature in our spotlight series, please reach out to

francesca.2.ritchie@bt.com

https://www.linkedin.com/in/francesca-ritchie-703325210