Why FinTech Brands Use Content Marketing

The FinTech industry is one of the fastest-growing sectors in the world. By the year 2022, the global financial sector is expected to be worth over US$26.5 trillion with a compound annual growth rate of 6%.

FinTech brands are now increasingly looking to include content marketing as a key pillar of their marketing and growth strategy.

We spoke to FinTech giants Klarna and Modulr as well as their content marketing partner, Copy House to find out more about the role content marketing plays in their strategy to increase brand awareness and engage audiences.

What is Content Marketing?

Content marketing is a strategic marketing approach that focuses on creating and distributing valuable and consistent content to attract and retain customers from a clearly defined target audience. On average, content marketing pulls in 3x as many leads and costs 62% less than traditional marketing. A well-written piece of content also continues to drive traffic to your site long after you publish it.

Marketing Challenges For FinTech Brands

When it comes to marketing FinTech, most brands face challenges around trust and education.

Traditionally, finance marketing has been aimed solely at IFA’s and the content typically used complicated and jargon-heavy language, which shut out smaller businesses and left customers confused about how financial services work.

FinTechs brands often look to challenge this status quo by creating a more accessible world, which naturally means they also have to educate their audiences in the process.

Klarna’s Senior Marketing Manager, Elias Pitsavos, explains:

“Many traditional financial institutions are afraid of Open Banking because it challenges established business processes and poses the threat of their customers abandoning them. There are also many small companies that we need to reach that don’t know about Open Banking. So we need to find a way to educate them about the service and its value.”

How Content Marketing Conquers These Challenges

“Content marketing is all about building trust and educating people. If your website looks and sounds good people are more likely to trust you. Content helps you give them quality insights without them having to ask for it.”

Kathryn Strachan, MD at Copy House

Content marketing also helps FinTechs to:

Increase Brand Awareness

Being a relatively new player in the field of finance, FinTechs are competing against household names like RBS and HSBC when trying to acquire new clients. Content marketing is an excellent way to increase brand awareness and educate people about their solution.

Klarna’s Elias Pitsavos explains: “

Klarna already has an established brand name when it comes to our core business and our payments solutions. We want to increase brand awareness in the Open Banking world and establish Klarna as a thought-leader in the field. Content marketing helps us do that.”

Build Trust & Credibility

Rightly so, people are nervous about who they trust with their money, so to gain new clients, FinTechs must let people know who they are and what they offer.

Content marketing helps FinTech brands build trust and prove their credibility before someone even speaks to their company. Businesses can then use content marketing to scale those relationships and reach a wider audience, regardless of team size or budget.

Modulr’s Chief Marketing Officer, Edwin Abl, informs:

“As we are a scaling business, we need to get people to understand our brand and our services. Content marketing helps us build credibility and prove that we’re a viable alternative to traditional banking. It’s a key pillar in our strategy to achieve that.”

Exercise Thought-Leadership

“We educate our audience through content marketing. Since traditional marketing methods like events aren’t available to the same extent because of COVID, content plays an even more vital role in getting our message out there.”

Elias Pitavos, Klarna.

By sharing useful information in a blog article or on social media, FinTech brands can demonstrate their expertise in the field and kickstart conversations.

Modulr’s Edwin Abl, adds:

“Content marketing helps us communicate what we stand for and how helpful we can be from an education standpoint. It’s not just about marketing, but teaching the audience about changes in the industry and informing people of what’s going on. We use content marketing to build our community.”

Whether you’re an established FinTech brand or a startup, content marketing is critical to creating a successful marketing strategy. Other marketing methods come and go, but people have always, and will always want content.

By putting energy into creating high-quality, SEO optimised content ”“ or outsourcing your content creation to a content marketing agency ”“ is a long-term investment, but will bring great results. So start investing now.

Note: Copy House is a content marketing agency specialising in FinTech content and provides content marketing support for Modulr and Klarna. By crafting SEO-optimised, educational content, Copy House helps these FinTech giants increase brand awareness, build trust and educate their audiences. Find out more about Copy House byscheduling a call or visiting their website.

Photo by Kaboompics .com from Pexels

Card issuing and management: staying relevant facing ever faster changing customer expectations

How card issuers are rethinking their business models and technical architecture

Our payments landscape is changing rapidly, and traditional card issuers need to keep up with new competitors that meet customer expectations. Especially now, during times of lockdowns and working from home, customers are expecting digital services that are seamlessly integrated into their every-day lives. This means that Issuers have to rethink both their business models as well as their technical infrastructure to keep up with competitors and customer expectations.

Convenient, fast and reliable

First of all, how popular are card-based payments nowadays? As research shows, this payment method will play a major role in the near future. By 2022, it is estimated that 47 percent of global e-commerce payments will be made using eWallets, while 28 percent will be made using credit and debit cards. At the point of sale (POS), it is expected that 52 percent of all global POS payments are made using either a credit or debit card, with eWallets (28 percent) assuming the third place. These numbers have to do with the fact that consumers find card-based payments convenient, fast, familiar, reliable and secure. A little further in the future, we are likely to see the general replacement of tangible plastic cards by alternative means of payment like mobile payment apps and virtual cards. However, the payment itself will remain card-based and will, thus, to a large extent rely on the established infrastructure of schemes like Visa, MasterCard and local schemes.

Crowded Landscape

This is the reason that the card issuing landscape is getting increasingly crowded as new players spot opportunities to tap into the unresolved growth potential of the card payments industry. Over the years, many traditional banks have delivered card payments services on a license to operate’ basis, meaning that they have typically issued basic products like debit, credit and prepaid cards and have not shown any interest in differentiating themselves through these products. Neobanks seem to be utilising the full potential of cards and card payment services by making them the focal point of additional services. This places the cardholder at the center of the payment experience. Think about services and features like real-time information on transactions, convenient onboarding processes and product control (for example spending limits and geo-blocking).

Challenges

As a result, traditional card issuers are feeling the pressure of increased competition. It urges them to transform their card processing platforms to remain competitive, but there are a number of internal and external challenges that need to be overcome. Think of diversifying channels and the demand for a consistent experience or the creation of new technologies that are disrupting financial services and the arrival of regulations like Open Banking, PSD2 and GDPR. Other than that, players are forced to focus on efficiently processing massive volumes to make the business case viable. In the meantime, internal challenges play a key role as well. Traditional players are, for example, struggling with their legacy systems and their ability to leverage the vast amount of data points produced by transactions. Besides that, players need to protect sensitive data and actual monetary transactions against fraud. And there is also the struggle of managing the increasing number of compliance procedures.

The Solution: Open Innovation

While there are many interesting solutions from Fintechs and other third parties available that address some of these challenges or simply offer a superior frontend experience, they are often hard to integrate into existing legacy applications and some processing partners do neither offer a modular platform nor the commercial flexibility required to quickly test and integrate third party solutions. At Worldline, we are convinced that the best results come out of open innovation. That is why we are hosting the annual Worldline e-Payments Challenge where we bring together our clients and fintechs to create innovative use cases together with our experts. Our modular, real time processing platform allows for simple integration of these solutions based on a large and powerful set of APIs.

Are you looking for creative ways to address the challenges Issuers are facing today? Get in touch with our experts to learn how Worldline can support you. Contact Us: worldlinecommunications@worldline.com

Fintech Recruitment: Top Tips From the Professionals

It’s no secret that great fintech candidates are rare. It’s a growing industry that’s becoming cooler all the time. Face to face and phone interactions are decreasing (let’s not lie, we’re all experts at talking to chatbots now!), so the highly skilled roles needed to facilitate these changes are becoming pretty in-demand.

Add an increase in the need for cyber security and financial insurance and you’ve got a talent gap. But, if you’re reading this, you probably already know that…

In Scotland, we boast some of the best fintech businesses in the world; as the BBC reported in January 2020, the number of Scottish fintech firms grew 60% in 2019. That’s obviously slowed in 2020, but the outlook remains strong.

So, in this competitive market, how can your fintech recruitment strategy make your business survive and thrive? I’ve put together the top tips I’ve learnt working in tech and fintech recruitment that should help.

Refine your EVP

Highly skilled people in fintech can command high salaries. So, you need to differentiate your business to make it stand out. You need to give people a reason, more than money, to work for you.

And no, we’re not talking pool tables and free coffee.

The pandemic has increased the demand for flexibility and that means working from home, moveable hours, and part time working.

People also want to know that they’ll be looked after as your employee. Do you provide private healthcare? Counselling? Gym memberships? Clearly communicate what you do to improve quality of life in your careers page, your marketing, and any external sites.

Then think about your company culture, particularly important when most of us are working from home. Show how you’re inclusive, how you welcome new employees, and show this to potential candidates.

If you don’t provide the things above, why not? They’re what will make you stand out from the competition.

Widen your talent pool

Fintech in Scotland is still a relatively small industry. If you really want to discover great talent you might want to look outside either the fintech pool or your locality.

Thankfully, with great advancements in tech (especially recently) it’s much easier to work remotely and most are finding it a positive experience.

By widening your search, you get a bigger talent pool and more diverse candidates. A May 2020 McKinsey report said that “companies in the top quartile for gender diversity on executive teams were 25 percent more likely to have above-average profitability than companies in the fourth quartile.”

How candidates view their careers is changing too. We used to work in the same role for most of our lives, but now, people are continually changing roles, reskilling, and upskilling. Now, this ethos means it’s easier to hire people who can be trained to do specific roles, rather than only looking for those already in them.

Someone who works in customer service might be a great fit for sales, and we’ve seen designers move to development roles easily.

Get methodical about hiring

In a market with talent gaps, it’s easy to make the wrong hire. In the long-term, this can cost you a lot ”“ both financially and in your company culture. If you have a robust hiring method though, you won’t make these mistakes.

At Solutions Driven, my team and I use RPI ”“ Recruitment Process Intelligence ”“ to make the right hire, first time, every time. We use RPI with everyone from big banks hiring CEOs and startups hiring sales execs. And it always works.

Through RPI, we use various methods to find and secure the best talent. The two fundamental ones are the 6s and the 6F processes.

The 6S process is how we find and secure candidates:

We hold an initial Scoping meeting to identify the hiring needs

We create a Scorecard that matches the businesses’ criteria

We source candidates via the latest technology and human intelligence,

We Select them against the scorecard, interviews and psychometric testing

We Secure them via our 6F Process (more on that in a sec)

We Satisfy both the candidate and our clients by measuring the results and regular check-ins.

For the 6F process, we ensure that candidates and companies are matched on six key areas ”“ Fit, Freedom, Family, Fulfilment, Fortune, and Future ”“ so that your potential hire becomes a long-term, happy employee who helps propel your business forward.

Exciting passive talent

Your ideal hires are probably already in roles. Thanks, talent gap! So, when talking to fintech companies, we’ve found a big problem they have is activating passive talent who are already happy in their roles.

Many don’t even want to entertain an initial conversation.

The first thing you can do is one we’ve already discussed – improve your EVP and how you market it. In this industry, top talent wants to work with companies that are going somewhere or doing something exciting. It’s important that your brand is known for being forward-thinking and allowing people to work on great projects and progress.

It can be hard to activate passive talent by yourself. It takes indepth technology, experience, and a lot of time. So sometimes, it’s best to get the professionals in.

If you’re really serious about getting the best people to join your company, a good recruitment company, who knows your industry and knows how to attract great people will be far more cost effective in the long-run than doing it yourself.

Blog written by Nicki Paterson. Nicki is Global Head of Business Growth at Solutions Driven, a Glasgow company that has specialised in business-critical recruitment for over 20 years. Working on a flat-fee basis and 12 month guarantees, Solutions Driven’s focus is getting the right people for the right roles, first time, every time.

If you’d like to find out more about how you can recruit effectively in the fintech market, get in touch with Nicki at npaterson@solutionsdriven.com.

Small business resilience and the evolution of ecommerce

The continuing shuttering of small businesses on high streets across the country is being accompanied by an unseen birth of new, exciting digital-only small businesses.

Periods of economic downturn typically result in a decline in new business registrations and at the beginning of the pandemic, it looked like UK SMBs were set to follow in this trend. For instance, statistics released by the ONS revealed that business creations slowed during April and May.

Despite this, Companies House figures reveal an overall increase in the number of new company incorporations in Q2 when compared to the previous year. This is indicative of a plethora of new business ventures inspired by our changing way of life.

Many of these emerging businesses are digital-first by necessity of the global lockdown they were born out of. Take for instance an independent hardware store which was already struggling prior to the pandemic. They may now find themselves in a position of renewed success, selling specific gardening tools via Shopify and Instagram marketing. While they may not have a strong credit history they do have a vast data footprint, owing to the numerous systems they rely on to run their business. Each data source, from their accounting package to their POS or ecommerce system provides a valuable yet siloed view of performance.

The shifting value exchange

However, the modern SMB expects systems and services to work together seamlessly and appears more willing to share their data in an open and automated fashion in order to ensure this. For instance, in September of this year, it was reported that the use of open banking had doubled in just nine months – an increase of one million users since January.

This increased appetite for interconnectivity between financial systems has opened the door to a much more collaborative, bespoke and diverse service between small businesses and their financial service providers. This is evidenced by the growing convergence of the POS, ecommerce and lending industries. Square Capital, Shopify Capital and Worldpay Working Capital are just some examples of funding facilities utilising transactional data to determine creditworthiness and offering finance at the point of need for small businesses.

Moving forward, customers who are willing to share their financial data digitally via accounting, ecommerce & POS package authorisation or open banking will likely benefit from a better service and more affordable products. For instance, lenders will be able to offer more favourable rates due to their enhanced ability to calculate risk and the notable reduction in the cost of serving these customers. The end result will be a shifting value exchange for small businesses whereby the benefits of sharing their data will become even more tangible than ever before.

The rise of ecommerce

The conditions of the global lockdown required existing businesses to pivot in order to remain viable. As a result, the period between April and July saw 85,000 UK businesses launch online stores or join online marketplaces. Many of these SMBs thrived during the pandemic as their adoption of ecommerce solutions coincided with a rapid increase in online sales, accelerating e-commerce growth by five years.

With the pandemic shifting the primary channel of trade online, gaining access to ecommerce and point of sale data is now crucial for financial service providers. The mutual benefits of doing so are multifaceted. For instance, commerce data can be used by lenders in particular to improve underwriting processes and credit decisioning. Small businesses will therefore benefit from a faster and fairer service which goes beyond traditional methods of credit scoring to consider their performance from multiple data sources in real-time.

This cultural shift towards enhanced digitisation and the growing importance of ecommerce will likely have a lasting impact on the way we think about the financial health of small businesses. In order to take advantage of this opportunity, financial service providers will need to replace siloed data with a connected ecosystem of unified financial data sources.

This article was written by Pete Lord, CEO and Co-Founder at Codat. Codat lets banks and fintechs plug into their small businesses and the software they use, giving them seamless access to real time customer data. Codat is building an ecosystem of connected datasets that handle the heavy lifting of integrations, leaving providers free to focus on improving their offerings for small businesses.

Photo by BedBible

On-Land Payment Infrastructure for Rapid Growth

Two means to help protect against cybercrime

Firms need a combination of robust policies/procedures and technology to help protect against themselves against cybercrime, says Anthony Rafferty, Managing Director, Origo

It seems hardly a week goes by without news of the vast sums of money which has been scammed or otherwise stolen by criminals through cybercrime.

The extent to which cybercrime is prevalent within pensions and financial advice services ”“ two of Origo’s principal areas of focus ”“ has been brought home during the Covid-19 crisis as criminals have ramped up their attempts to trick individuals and businesses into giving away personal and financial details to enable fraudulent transactions.

Recent reports have highlighted that the Financial conduct Authority (FCA) has been investigating more than 150 Coronavirus-related scams since the outbreak began (1) and spent over £300,000 on fighting fraud online in the first six months of the year (2).

The industry’s compliance consultancies have been warning financial advice firms on scams and email hacking. Paradigm Consulting recently warned advice firms about fake email surveys purporting to be from the Regulator (FCA) on the impact of Covid-19 (3), while ATEB Consulting warned on fraudsters hacking personal email accounts and impersonating clients to encash investments (4).

Alongside this are reports of company owners and directors receiving highly realistic scam emails from trusted organisations, including banks, requesting usernames, passwords, and bank details.

This increase in reports and news stories serves to illustrate that the threat to financial services businesses from cybercriminals cannot be ignored by any company.

Data published by the Information Commissioner’s Office (ICO) has revealed that phishing’ by cybercriminals was the second highest reported incidence of the inappropriate disclosure of data’ by company staff (5).

However, the most common incidence of data breach reported to the ICO was information being emailed to the incorrect recipient. That suggests a breakdown or lack of internal procedures.

Clearly, whether dealing with cybercrime or staff error, having a well-documented policy, robust procedures and monitoring of processes, can go a long way to preventing potentially costly data breaches.

Education is another area where firms can help protect themselves from external threat and internal error, including regular cybercrime awareness sessions and training of staff.

Implementing technology ”“ such as employing military-grade encrypted email, particularly when exchanging personal and sensitive information with clients or between organisations ”“ should become standard every-day practice. Encrypted email secures against hacking, enables authentication to ensure the right person has accessed the information, and provides an audit trail for security and regulatory purposes.

We are operating in a world where disclosure of information is a threat on many levels and putting in place preventative measures is essential for any size of firm within our industry.

(1)The data was obtained under the Freedom of Information (FOI) Act by the Parliament Street think tank’s cyber research team.

(2) https://www.ftadviser.com/regulation/2020/09/03/fca-spends-300k-to-fight-fraud/

(3) ttps://www.moneymarketing.co.uk/news/scammers-posing-as-fca-send-out-advisers-covid19-impact-survey/

(4) http://www.atebconsulting.co.uk/news/beware-email-hacking-scam/

(5) https://ico.org.uk/action-weve-taken/data-security-incident-trends/

How fintechs are driving financial inclusion

In this guest blog, Magdalena Krön, Rise Global FinTech Platform Director, Barclays Ventures, takes a look some of the work that the global fintech community is doing to address one of the biggest blights in society ”“ financial exclusion. This blog is based on the latest Rise FinTech Insights, a regular publication from Rise, created by Barclays.

One thing that COVID-19 teaches us, if we needed reminding, is how many people across the world remain disadvantaged by not having access to basic financial services. Although efforts to improve financial inclusion have come a long way in a relatively short period of time, there is still much more to achieve, especially for the 1.7 billion individuals who are currently unbanked(1). The work being done in the fintech space to address this issue, intended to open doors for individuals and families in a way that many of us take for granted, has seen entrepreneurs deploy everything from cryptocurrency to Open Banking and APIs in efforts to find new ways to support the financially vulnerable.

Chris Britt, Co-Founder and CEO of Chime ”“ a leader in the US challenger banking segment that offers internet-based, fee-free services ”“ says, “There is a huge segment of America that has a lot of anxiety around their money and day-to-day finances.” Helping them achieve “financial peace of mind”, he says, starts with providing a banking relationship that doesn’t rely on fees. “As many as 70% of Americans live paycheck to paycheck ”“ we offer free services such as early access to paychecks and overdraft protection.”

Innovative fintech thinking has come to the aid of another swathe of US society: the 2.5 million newcomers to the country on long-term visas who are, for the most part, unable to access credit. Collin Galster, Head of Business Development at Nova Credit, identified a solution to this problem facing the US’s foreign-born population, which is set to rise to 50 million by 2030. The company, a cross-border credit bureau, transfers individuals’ financial histories from one country to another, remedying the issue of lenders not being able to access enough financial information to feel comfortable lending, and therefore enabling immigrants to start funding their futures.

The need to tackle financial exclusion is felt even more acutely elsewhere. In India, for example, almost 11% of the adult population is unbanked. The report highlights a number of successful government initiatives, including Jan Dhan Yojana and Aadhaar Pay, that are spearheading more accessible paperless Know Your Customer (KYC) identification processes and biometric-based identity payment systems. This is a tactic that saw the number of people holding bank accounts increase by just over 50% between 2014 and 2017. Manish Khera, Founder and CEO of HAPPY ”“ a digital lending app targeting a multi-billion-dollar credit gap in India’s micro businesses ”“ emphasises how the internet now plays a vital role in facilitating and widening this access, citing the fact that India currently has 520 million mobile internet users.

Alternative banking solutions are springing up elsewhere, too. In east Africa, for example, Anisha Kothapa, Fintech Analyst at CB Insights, says cryptocurrency is being “adopted widely” ”“ offering a new way for the unbanked to save money and complete transactions without needing an account or credit card. One firm leading the way is Kenya’s BitPesa, a digital currency payments platform that “allows users to accept bitcoin payments, exchange bitcoin for local currency, and deposit bitcoin into accounts or mobile money wallets.”

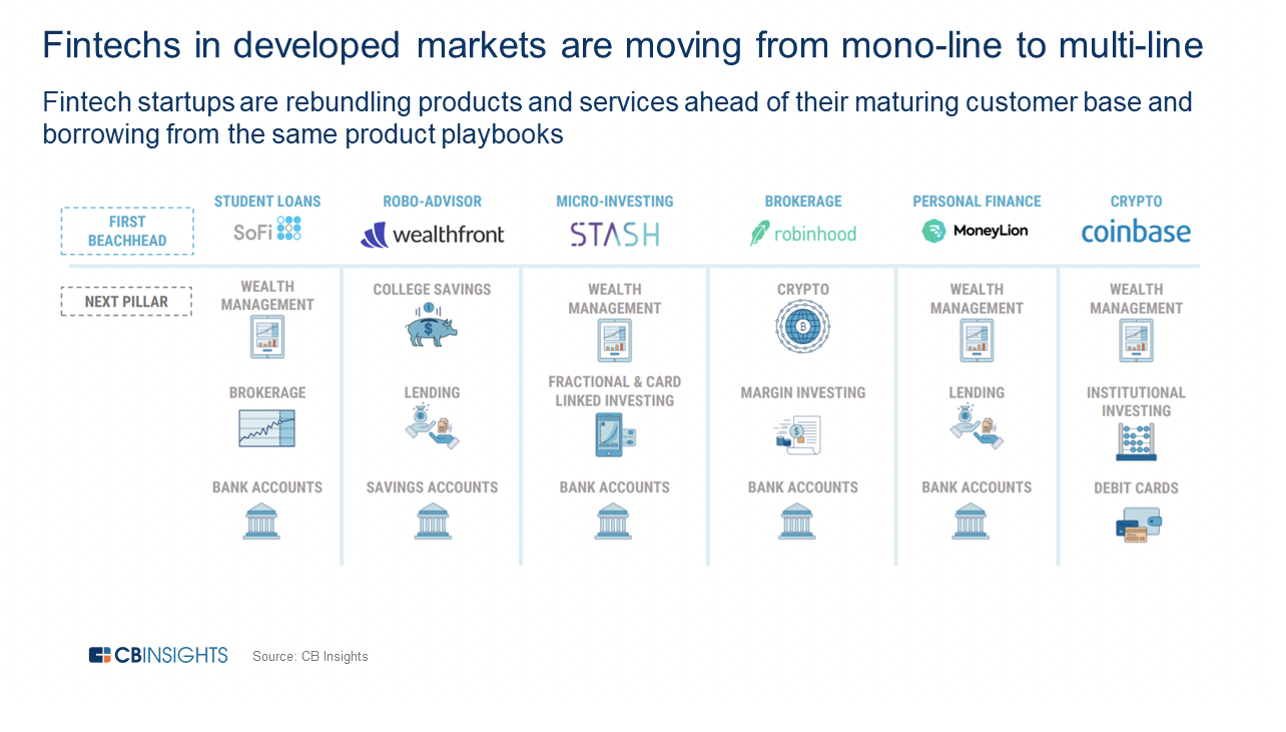

In contrast to developing countries, their developed counterparts are enabling financial inclusion differently by focusing on customer engagement and transforming the entire banking business model. FinTechs in developed markets are also moving from mono-line to multi-line offerings and re-bundling products and services to acquire more new customers.

It’s not just individuals that face financial exclusion, the report emphasises, but SMEs and budding entrepreneurs. According to Grant Bickwit, Associate at Barclays International, access to capital is one of the biggest challenges faced by entrepreneurs. It’s a sad truth, he explains, “that both entrepreneurs and investors are still reliant on individual networks and legacy processes for sourcing opportunities, entrenching geographic and social limitations”. In response to this, online platforms like OnDeck and Kabbage, launched in 2006 and 2009 respectively, offered firms access to credit digitally ”“ a trend that has proliferated.

Rise innovators have been responding to some of the other unique issues brought about by the pandemic, from employment to supply chain management. Rise Mumbai members, MMS.IND and GeoSpoc ”“ experts in geospatial information systems, platform-building, and consumer and micro-market data ”“ have joined forces to develop a COVID-19 impact tool which provides insights into how the pandemic is affecting consumers ”“ and enables businesses to better predict demand and ensure supply chain optimisation. Meanwhile, over at Rise New York, Brainceek, a workforce simulation company, has been helping corporates design virtual summer internship curriculums, providing extra support for the hundreds of thousands of graduates entering a difficult job market.

Addressing financial exclusion is a huge task, but one that is achievable, particularly with targeted collaboration across banks, technology companies and fintechs and a focus on achieving financial inclusion for those 1.7 billion individuals.

Download all editions of Rise FinTech Insights here.

(1) https://www.worldbank.org/en/topic/financialinclusion/overview

Developing a Change-Ready Mindset

The only constant is change’. At least, that’s how Heraclitus put it, leading me to believe that resistance to change was as common in Ancient Greek society as it is today. Whilst quite obviously a lot has changed since 570BC ”“ medicine, architecture, Tesco Expresses ”“ our aversion to change, especially when forced, has remained steadfast. Over the last few months I’ve been speaking to a great many business owners, young and old, about the effects of COVID-19 on their businesses. What has really stayed with me is how many have really resisted these changes and still yearn to get back to business as usual’.

But what is business as usual? Can we go back to a pre-COVID method of operation? Even if we can, should we? Business owners have felt the full impact harder than many and for that reason I can understand the desire to sweep the whole affair under the rug and move on. However, in doing so we might just miss out on crucial opportunities.

The questions I keep coming back to are: if another global event occurred right now, how would your business be better able to handle the situation and what has been learned and implemented this time around to get your business into better shape? A big part of honestly facing up to those questions comes down to our own mindset and sense of control. When the pandemic hit and threw everything out of sync, the natural reaction was to cling onto what we knew and what gave us that sense of control and certainty, but very quickly it became apparent that wasn’t a viable option this time and nor will it be with future situations. The real issue here is that nobody truly likes being told what to do, especially not by a microscopic virus with absolutely no redeeming qualities and so, to come back to mindset, what can WE do to normalise our relationship with change to ensure it’s never forced upon us in future?

Managing change is a bit like going to the gym; the first time you go, it hurts and (speaking from personal experience) frustrates you when you haven’t dropped a stone by the next day. When you maintain a rhythm, the pain subsides and the benefits begin to show. So if we adopt the same relationship with change and by actively seeking it, stay ahead of the curve, we’ll slowly develop our mindset around change much like a muscle at the gym. With that in mind, I wanted to share with you my 5 steps for developing a Change-Ready’ mindset.

- Analyse what is happening now? ”“ Look at your business to really understand what is happening right now. Analysis tools like the PESTEL, competitor analysis, SWOT analysis are great tools to help you really understand the change. What are the indicators that change is needed: revenue has declined; customers aren’t buying through the shop any longer; or suppliers are no longer able to supply you?

- Identify the changes required ”“ What needs to change within the business to resolve this issue? Do you need to look at alternative channels to market, such as selling online? Do you need to look at or alternative suppliers? Do you need to completely pivot what you do?

- Identify the obstacles ”“ What issues are there with making that change? Once you’ve identified a possible solution, you need to apply your critical thinker and consider all of the obstacles stopping you form implementing that change ”“ Lack of funds? Lack of customer validation? Lack of man power (or woman power)?

Now at this point it’s worth noting that, as a demographic, entrepreneurs and business owners are phenomenal at rapid decision-making, however, in some cases this needs to be checked. When change is forced upon us, there is a risk that these decisions could be made on the basis of emotion rather than reason. Even when change is unexpected, there is usually a little time to step back, analyse and identify. If we don’t, required changes can be blown out of proportion and become too general to have a lasting, meaningful impact.

- Assess the risk & cost of change ”“ Determine the degree of risk and the cost of change looking at different scenarios to help you map alternative paths. Before progressing with any significant change you need to assess the risk and costs involved with adopting this new approach. How does this affect your overall costs? Do you need additional resources? Are there any risk involved?

- Plan the way forward ”“ Once you have all the information you can then decide on a clear way forward and put steps in place to integrate that change. Break it down into manageable steps and make sure you are testing at every step of the way to make sure the change is working.

There are two forces underpinning these steps. Firstly the clarity of your vision: if you know where you’re going and what you want to achieve, you’re likely to accommodate change better, provided you can see how it helps you achieve what you wish to. You wouldn’t get in your car and ask your sat nav where you want to go, so don’t expect the same from your business. If your vision needs a refresh, make sure you prioritise that! Secondly, resistance to change: as we’ve covered, this is a challenge millennia in the making, so take some time to understand your own resistance to change, by questioning where it comes from and when was the last time change adversely and/or positively influenced your business.

The ironic thing about all of this is that resistance to change stems from a perceived loss of control and yet, if our vision is unclear and our self-awareness is lacking, the uncomfortable truth is that we lost control long ago.

Mindset, Managing Change and a whole host of other business support content is available via the Royal Bank Business Builder programme ”“ a free virtual tool for new and established businesses. Open to everyone, Business Builder supports you to stay in control across a wide range of business topics, available 24/7. Sign up today by clicking here.

Why Scotland should harness its influence in the global fintech industry

Guest blog from Corporate Partner and Technology Lawyer at Addleshaw Goddard, David Anderson

In Scotland, we undoubtedly have one of the strongest fintech clusters in Europe. At the turn of the year, the Scottish fintech sector became the first in the UK, and only the third in Europe, to receive formal accreditation as a cluster of excellence from The European Secretariat for Cluster Analysis (ESCA).

The body looked at 36 economic factors before awarding Scotland this accolade, and our innovative, dynamic and collaborative ethos must, I believe, have had an important role to play in why we received this title.

Looking at growth from 2019 to 2020, the number of fintech SMEs based in Scotland increased by more than 60% from 72 to 119. This notable boost is something that we should continue to celebrate and use as a foundation to build upon to attract even more leading fintechs from across the globe to expand and invest in Scotland.

Most recently, it was announced that our fintech sector will receive a further £22.5 million of funding to establish a Global Open Finance Centre of Excellence (GOFCoE) in the Edinburgh and Central Belt region. Funded by the Strength in Places Fund, this is a remarkable opportunity for Scottish fintechs as the new research and development centre will explore how open banking and financial date can be used to deliver social and economic benefits.

We have world-class talent on our doorstep and as a Corporate Partner and Technology Lawyer at Addleshaw Goddard, I am fortunate to get the opportunity to work with a number of entrepreneurs, CEOs, advisors and customers in the fintech discipline every day.

As a firm, we recognise the importance and wealth of the fintech sector. That’s why in 2017 we launched our dedicated Addleshaw Goddard Elevate programme – a 10-month initiative for selected fintechs designed to accelerate them through legal challenges faced by start-up and fast growing businesses.

Year on year, we are enthused at the calibre of entrants to the programme and to date we have supported 22 fintechs with our expertise across financial services, regulation, IP and corporate and commercial transactions.

Successful applicants to Elevate programme receive advice covering funding, payments, financial regulation, investment and technology at no cost to them as well as ongoing mentoring and access to the firm’s resources. By combining our client-side experience with regulatory and legal expertise, gives us great insight into the concerns and priorities to help fast growing businesses become more productive and even more successful.

In 2019, we welcomed nine businesses to the cohort including Scottish businesses Amiqus , OBR-Open Banking Reporting and Trace, all of which are contributing to and bolstering the tech scene in Scotland. In the next few months, we will be launching the 2020/21 programme and are already looking forward to working with more forward-thinking technology firms with revolutionary ideas.

Whilst this paints an incredibly positive picture of the Scottish fintech sector, which is true, we must remember the Covid-19 cloud that currently hangs over our professional and personal lives. It is a challenging and sometimes worrying time, and the consequences of it will live on long past the ease of lockdown and other restrictions.

The last few months have, however, allowed many Scottish tech firms to adapt and highlight their invaluable contribution to society. I have been extremely encouraged at the response of Scottish technology businesses to the current situation as they adapt themselves or help to aid businesses, people and the economy with their agile approach.

For example, Airts, which uses AI tech to help people at large professional services firms plan projects, has reshaped its working pattern and working from home structure to ensure clients still receive an excellent service.

XDesign ”“ which plans, builds and develops digital products that solve your business challenges – has moved quickly to introduce new processes across the business to succeed throughout this challenging period. This has even resulted in the firm welcoming new clients and staff, which is incredibly encouraging for the industry.

A great local example of this came from Occupyd – which connects businesses to underused workspace ”“ who has used the time to support chefs and caterers access underused commercial kitchen space in closed pubs, cafes, churches and other locations. Occupyd also created a Secret Takeaways’ list which has helped diners in Edinburgh and London find their favourite local restaurant options which are not present on the main apps.

Tech has of course always been important, but through the covid-19 pandemic it is proving to be invaluable as we rely on it to communicate with family, friends, colleagues and in some cases, life-line services. From my perspective, I have seen an acceleration in strategictechnology projects which are driven by improving customer experience and developing the best possible customer proposition.

Looking to the immediate future, nobody can predict to what extent the pandemic will impact the tech ecosystem in Scotland. However, the agile, innovative and inclusive nature of the industry, particularly the fintech ecosystem gives me great confidence that we will come through this with the ability to continue our success and growth, but with new insights and perhaps a refreshed outlook.

Interested technology businesses can register their interest for the 2020/21 AG Elevate programme here.

Scotland is Tomorrow: Developing Responsible Investing in Scotland with rTech?

Scottish Fintech has been a key highlight of Scotland’s modern economic rotation. A more sustainable, inclusive and progressive ecosystem. It is helping to change the shape and face of Scottish e-commerce and finance but has it always been changing it to be more responsible?

Despite the COVID-19 lockdown, the delayed COP26 presents a unique opportunity to reinforce Scotland’s position as a global centre for responsible investing. In doing so Scotland competes with every other country to drive leadership and achieve United Nation Sustainable Development Goals (SDGs). Like Scottish Fintech and the formation of the Scottish National Investment Bank, developing and growing Scotland’s responsible investing landscape is a powerful way to move Scotland’s economy to something more purposeful. The key is collaboration, which stimulates innovation, which encourages inward investment, which produces change in Scotland and overseas.

May 2020 saw the launch of Ethical Finance Hub’s new report, Mapping the Responsible Investing Landscape in Scotland’, which examines the responsible investment market in Scotland, looking at:

- History: the history of responsible investing with a focus on Scotland;

- Ecosystem: the composition of the Scottish responsible investment market, and the linkages between different participants;

- Taxonomy: the terms used by Scottish fund managers to describe their approaches to responsible investment; and

- Market Size: The size of the responsible investing market in Scotland, and how it compares to Ireland and the rest of the UK.

The motivation behind the report was to raise awareness and support the growth of the responsible investing market in Scotland. Having engaged with a number of stakeholders, as well as undertaken internal desk-based research, it was apparent that, whilst data on the sector exists for the UK as a whole, there was little or nothing specific to Scotland available. A link to the report can be found here: https://www.ethicalfinancehub.org/investingscotland2020/.

The report sets out the following call to action:

“Across the globe individuals, organisations and governments are starting to move from talk to collective action as we strive to achieve inclusive economic growth without depleting natural resources. It is now widely recognised that the financial services sector has a fundamental role to play in delivering universally supported targets such as the Paris Agreement and the SDGs. However, despite its potential, the current financial system can be a cause of, rather than a solution to, some of the pressing challenges our planet and its people currently face. In trying to address this predicament Scotland is reflecting on its heritage and seeking to emerge as a leading centre for a new financial paradigm that looks beyond profit and shareholder value to deliver social, economic or environmental impact as well as financial returns.”

In parallel Scottish Fintech can now boast over 120 Fintechs, connected with 15 universities, 16 tech spaces, accelerators and incubators. The conditions are fertile for cross pollination between responsible investing initiatives and Fintech. Yet Scottish Fintech and Scottish Asset Management are, at best, acquaintances rather than partners driving true innovation in responsible investment. Only by linking the success and innovation of Scottish Fintech with the opportunity in responsible investing can Scotland truly compete and succeed as a global leader. Bluntly put, Scottish asset managers and asset owners are missing a step in utilising the talent within Scottish Fintech.

Indeed a key observation in the report was the lack of collaboration between Scottish Fintech and Scottish asset managers in creating new solutions to expand investment, improve data and clarify the taxonomy (the universe of terminology). This is totally in keeping with what I set out as a New Fund Order’, the enablement and transformation of asset management through Fintech.

Stephen Ingledew, Chief Executive at FinTech Scotland said:

“Fintech innovation in asset management and capital markets is a fast emerging trend with a growing number of fintechs in Scotland developing innovative propositions to help the sector be more efficient and deliver better outcomes to investors. THis is being boosted by Scotland attracting many international fintech firms for example Agrud from Singapore and Actelligent from Hong Kong, who are attracted to Scotland because of university research capabilities and highly qualified students and professionals.”

The Scottish Asset Management Market

With £8 trillion AUM (as at end of 2019) the UK is currently the second largest global centre for asset management after the United States. Within the UK, Scotland is the second largest financial services centre after London, and includes the headquarters of Aberdeen Standard Investments – the largest active manager in the UK with a total AUM of £525 billion as of June 2019. Scotland is also a growing centre for fund administration (also referred to as asset servicing’), with strong corporate links with firms based in London and overseas.

Today, asset managers in Scotland include: Aberdeen Standard Investments, Aberforth Partners, Amati Global Investors, Ardstone Capital, Baillie Gifford, Blue Planet Investment Management, Cadence Investment Partners, Cameron Hume, Castlebay Investment Partners, Circularity Capital, Cornelian Asset Managers, Dalmore Capital, Dundas Global Partners, Edinburgh Partners, Kames Capital, Martin Currie, Panoramic Growth Equity, Pentech, Revera Asset Management, RM funds, Saracen Fund Managers, Stewart Investors, SVM Asset Management, Walter Scott & Partners and Valu-Trac. The following are now subsidiaries of larger asset managers based elsewhere: Kames Capital (Aegon Asset Management), Martin Currie (Legg Mason/Franklin Templeton), Edinburgh Partners (Franklin Templeton) and Walter Scott & Partners (BNY Mellon). Firms originally founded in Scotland, like Newton (also part of BNY), still retain a Scottish presence.

In addition, a number of asset managers headquartered elsewhere have branch offices in Scotland including: Liontrust Asset Management, Investec, Janus Henderson Asset Management, Franklin Templeton, BlackRock and Barclays. Lastly there are a number of smaller boutique firms, many of which straddle fund management and financial advice such as; Alan Steel Asset Management, Balmoral Asset Management, Charlotte Square Investment Managers, KPW Investments, Murray Asset Management, Odysseus Capital Management, Par Equity, Rossie House Investment Management, Rutherford Asset Management, Social Investment Scotland, TCAM and Trafford. Together these asset managers manage a mixture of open-end, mandates and closed-end funds for domestic and overseas investors, across a broad gamut of asset classes. The vast majority noted above (if not all) are categorised as active managers’ (that is, they do not track an index). Currently there are no Exchange Traded Fund (ETF) or passive’ (index tracking) providers based in Scotland.

Fintech Innovation is Happening but not Everywhere

We see more innovation in the asset servicing part of the market but again could grow significantly from here. Currently Scotland does not have any investment exchanges upon which to trade assets. Currencies are traded without a centralised location, rather the FOREX market is an electronic network of banks, brokers, institutions, and individual traders (mostly trading through brokers or banks). Scotland has no central clearing companies; for asset managers, the main firms that serve the UK are Euroclear, Clearstream, LCH Clearnet and Calastone. All are based in London or overseas. Similarly all of the large global custodians like State Street, RBC, BNY and Blackrock (that control >90% of the market) centralise their custody operations outside of Scotland. Scottish stock brokers include Redmayne Bentley, Speirs and Jeffries (acquired by Rathbones in 2018) and StockTrade. However the majority of brokerage is controlled by large investment banks like Morgan Stanley, JP Morgan and Goldman Sachs outside of Scotland.

Meanwhile smaller providers like Valu-Trac, based in Inverness, and Multrees Investment Services, based in Edinburgh, offer a range of fund management, administration, custody and back office services. A number of asset managers (e.g. JP Morgan, Morgan Stanley, Blackrock) also base their asset servicing and technology operations in Edinburgh and Glasgow. Computershare is a global leader in financial services and data management, working with around 16,000 global clients and their 125 million customers and having an established operation in Scotland providing relationship management and registry services to around 150 listed companies in Scotland and beyond.

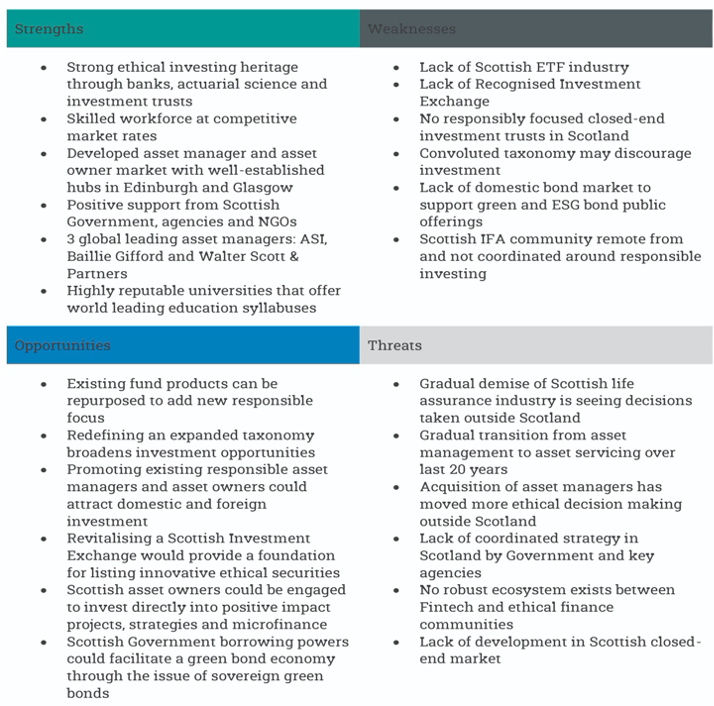

The analysis of the Scottish responsible investing market can be summarised in the following table of strengths, weaknesses, opportunities and threats.

Fig. Extract Mapping the Responsible Investing Landscape in Scotland’.

Page 55: SWOT Analysis’:

Conclusion: A Missed Opportunity

This innovation is not being replicated in the front and mid office of asset managers or asset owners and here the opportunity arises. Scotland lacks many of the traditional levers to stimulate responsible investment. This stymies the size the market could grow to. It also presents as a missed opportunity for Scottish Fintech. The goal is encouraging external investment into Scotland through asset management and asset owners. In doing so to become a global headquarters for responsible investment. Developing technology solutions and platforms to transplant these deficiencies calls on Fintech investment. The dawn of rTech’, responsible and sustainable Technology, with it the New Fund Order’ is set to becoming increasingly Green.

JB Beckett, Consultant, Ethical Finance Hub, Global Ethical Finance Initiative #GEFI #newfundorder #fintechscotland #scotlandisnow #scotlandistomorrow

Co-Author Mapping the Responsible Investing Landscape in Scotland’

Author New Fund Order 2.0 A Digital Resurrection’

Co-Author: The WealthTec Book’, AI Book’ and Paytech Book’

Photo by Karolina Grabowska from Pexels