Operational Resilience by Mihir Joglekar Business Analyst, AutoRek

Globally, organisations’ operational resilience is currently being tested as key members of staff are working remotely. The need to access data in real time has increased and reporting accurately has become more critical than ever.

Operational readiness can be defined as an organisation’s ability to anticipate, prepare, respond and adapt to uncertainties and disruptions to successfully deliver services to its client base. It requires both tactical and strategic thinking.

The Financial Conduct Authority (FCA) suggests organisations follow these three steps to support operational resilience (CP19/32):

- Focus on continuity of its most important business services.

- Conduct an extensive impact vs threshold exercise of all business services, and the levels of disruption that could be tolerated. This exercise should be conducted and reported at the highest level of seniority of organisational management i.e. board level.

- Consider disruption as a certainty and ensure adequate plans have been agreed to mitigate its impact to services.

The FCA reinforces the need for firms to develop and improve capabilities so that any systemic impact event is contained. Focus should be on time taken to respond, effective internal and external communication, particularly with customers. The FCA have also linked operational resilience as part of its objectives involving Consumer Protection, Market Integrity, and Effective Competition by ensuring resilient firms can support ongoing availability of services, thereby reducing harm to the consumer.

While operational resilience is not a new concept to the business community, what is missing is a complete approach to address resilience. Organisations may already have components like crisis management plans, disaster recovery plans and secondary sites etc., but unfortunately over the last two decades there have been a number of stress factors that have contributed to this subject being relegated as more pressing issues have taken priority mainly due to:

- 2000-02: Dot-com bubble and the impact due to its crash i.e. only 48% tech companies survived post event

- 2007-2010: Financial crisis trigged by subprime loans and reduced oversight of the industry at that point

- 2010-15: European sovereign debt crisis due to EU Member States taking on unsustainable levels of debt

- 2014-17: Chinese financial crisis with the popping of the stock market bubble

- 2019-21: Corona virus (COVID 19) related lockdown and economic downturn

The current “Great Lockdown” due do COVID 19 has simply functioned as a catalyst for serious action, triggering management and leadership team to renew efforts.

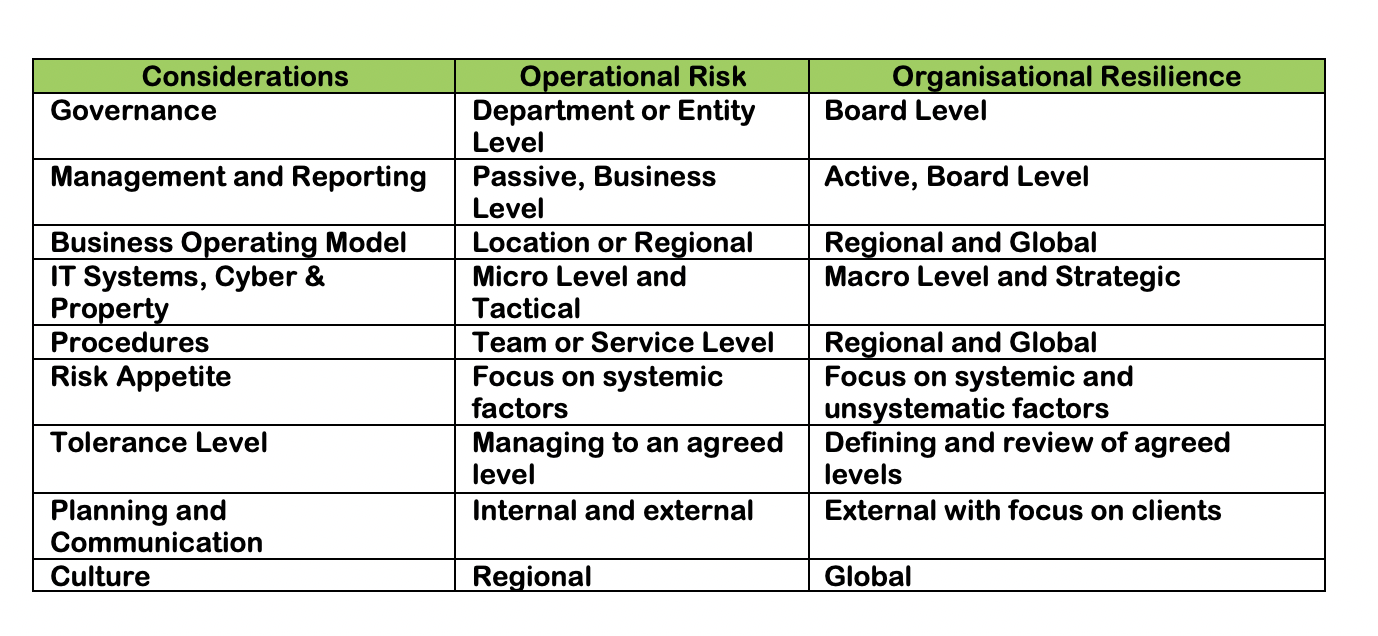

One way of differentiating operational risk from operational resilience is to consider the internal vs external force perspective. Operational risk is largely internal to an organisation due to a blend of systemic and non-systemic risks associated at micro level of business processes, while resilience is an organisation macro level initiative where all business units contribute towards establishing a resilient business and is inclined more towards external circumstances. Both risk and resilience are intrinsically connected and an organisation’s ability to effectively address operational risks across business functions will contribute to its overall resilience. The table below outlines these differences.

Following the publication of the discussion paper, Achieving Operational Resilience and the conclusion of the consultation process, the FCA has communicated its intention to review and where applicable, consider all feedback received as part of its final policy statement.

The FCA proposal include that firms:

- Identify and Categories their important business services.

- Set Impact Tolerance for each of these services.

- Test their ability to support these services across a range or scenarios

- Conduct active lessons learnt exercises

- Develop internal and external Communication plans

- Establish self-assessment and reporting documentations

Within the context of the current crisis our economic engines must start to fire up again and business must ramp up at the earliest safest opportunity. This is where AutoRek sees its innovative software making a significant contribution towards business, who still need to deliver service excellence to their clients in an unified manner, utilising new and innovative workflow and people management practices more than ever are reliant on distributed and remote team work.

In conclusion, organisations are now actively progressing their operational resilience programmes that will continue to evolve around new set-ups as leaders and managers gradually commence the return to a new and adaptive business as usual.

www.autorek.com

More on Autorek

An interview with Nicki Bisgaard, CEO at EedenBull

Congratulations on your recent announcement about the extension of your strategic partnership with Mastercard. Can you tell us a bit more about what it means for EedenBull?

Thank you. The strategic partnership with Mastercard is key as we continue to develop our new and innovative payment programmes, making it easier and safer for businesses to pay and get paid in an ever changing world. Both Mastercard and EedenBull service banks and their customers and seek to secure competitive advantages for the banks we service together. Having a partner like Mastercard strengthens our ability to innovate through direct access to Mastercard’s assets and expertise, it significantly strengthens our distribution power and it creates significant awareness throughout the European marketplace for who we are and what we can do. That said, there are obvious benefits to Mastercard too. Through EedenBull they gain access to highly specialized expertise particularly in commercial payments as well as an extremely committed team of developers.

Can you speak to us about some of the new developments at EedenBull?

As you know, we have already launched our Q Business payments and spend management platform which is a direct response to universal requirements of small and medium sized businesses, organisations of different sizes and the public sector for enhanced control, spend visibility, and streamlined payments processes. The programme is currently being distributed by 65 banks in Norway with several thousand businesses already using the service. We are continuously developing new and exciting features and functionalities, always with a customer centric approach, understanding and responding to customers’ real issues and challenges.

With the current COVID19 situation have you seen more companies approaching you to manage expenses remotely?

The short answer is yes. We are seeing a great interest in our services from exisiting and potential new partner banks around the world as well as from their customers. The pandemic has certainly brought about an increased awareness of payments related issues facing businesses of all categories and sizes. Even prior to the outbreak, we already had a situation where new regulations, new technologies and new players were changing the way businesses and consumers were thinking about payments. Many of the trends we saw emerging towards the end of 2019 have been accelerated by the pandemic. Think about contactless payments, e-commerce, cashflow, need for working capital to mention but a few.

You opened your Scottish office last year; can you tell us about what your experience of the Scottish fintech cluster has been so far?

It’s been great. Ever since setting up shop in Edinburgh, or even way before, we have enjoyed the support we have been receiving from the Scottish fintech community in general and FinTech Scotland in particular. The access to likeminded businesses and organisations, the government in Scotland and the many extremely talented people we have been lucky enough to employ has quite frankly been instrumental in securing the momentum and successes we have enjoyed thus far.

Are you looking to grow your presence in Edinburgh in the next 2 years? How many people will you be recruiting?

Just to make one thing clear: We are staying in Edinburgh, no question about that at all. We love being a part of the fintech scene in Scotland and are committed to continuing over years to come. We will be growing our presence in Edinburgh over the next 2-3 years for sure and will be investing further in attracting talent to work in our team in Scotland. I would be surprised if we by end of 2022 had not increased the number of team members by any less than 100%.

What are the main differences between scaling up a fintech in Edinburgh and Oslo?

What a great question. Upon reflection I would have to say that I think scaling up in Edinburgh isn’t very different from scaling up in Oslo. In fact, probably much more similar than compared to many other locations we could have chosen. We find that the cultural differences are fewer than the similarities, the talent pool is similar, the governmental support on the same levels and the fintech scene is energetic in both cities. There are some obvious current and historic bonds between the two small nations which made it easy for us to come to Scotland and has made it easy for us to stay and to grow in Scotland. We love being here.

An interview with AutoRek’s MD, Gordon McHarg

For those who don’t know AutoRek, could you tell us what you do and what makes you different?

AutoRek is a financial controls and data management platform which automates and streamlines data collection, validation and reconciliation of financial data. We were founded 25 years ago as a Glasgow based consultancy firm specialising in data management and bespoke applications development on the Microsoft platform. The majority of our customers are financial services companies with high transaction volumes and often complex data management requirements.

Our software is a configurable rules driven platform which can be applied to diverse business scenarios including Mortgage payments, Insurance premiums, ATM cash management, internal financial controls and various regulatory reporting requirements such as MIFIDII and CASS (client asset protection).

Over the course of 25 years, we have worked with our clients continually evolving our product to meet the needs of the financial services market adapting to new operational challenges and the ever changing local and global regulations. Our technology has also evolved transitioning from a client server windows application to being web enabled and is now available as a fully featured SaaS solution. Our upcoming Version 6 of AutoRek, scheduled for release August 2020 will be the first release of AutoRek with embedded AI & ML capability.

Making effective use of technology to solve business problems requires a team capable of understanding and delivering solutions. Our primary differentiator in the market is the capability of our people and the commitment of our team to deliver the best possible outcome for our clients.

You’ve signed some very impressive clients in the past few months including Nationwide and the Bank of England. What are the reasons of your success?

We have a number of the UK’s leading financial services organisations as clients which we are very proud to have on board and serve. The Bank of England and Nationwide, were of course, great names to add to our list. In both cases, we were competing with large global reconciliation platforms. Our understanding of the specific requirements of their business and the capability and flexibility of our software to deal not only with the huge volume but the complexity of data led to AutoRek being selected by both organisations.

You also appeared in the Regtech 100 list recently. This is a great achievement.

We were delighted to appear in the RegTech 100 list, one we have been associated with the last 2 years. It is always great to be recognised as a company for our efforts in the industry. It is hard to say if that has helped with recent wins, but it definitely didn’t put us on the back foot. These awards and recognitions are always great to appear in. It shows that our clients are satisfied with how we operate and that what we provide for them as a service helps them in their day to day jobs. They will certainly help AutoRek to be recognised as a leading software in future years.

Can you tell us more about your partnership with Cforia?

In 2019 AutoRek established a partnership with Cforia Software Inc,

a US-based global enterprise solutions provider delivering end-to-end global order-to-cash automation. CForia have embedded the AutoRek product into their Order to cash platform supporting automation of payment allocation and cash reconciliations. Our partnership is still at an early stage however having added 3 new global clients in the last 6 months it is looking very promising.

How has AutoRek been impacted by the COVID19 crisis?

In the early days of the pandemic the health and wellbeing of everyone at AutoRek was clearly our first priority. We moved the whole company to remote working one week prior to the government lockdown announcement. This wasn’t a particularly difficult decision as we were confident that most of our day to day operations could be executed remotely and that has proved to be largely the case. Some initial logistical challenges have been overcome and the initial novelty of video calling has worn off and become the typical day to day for most us.

As far as business is concerned our existing customers combined with a strong order book has kept everyone busy. Clearly there has been a significant impact on the market and going forward new business development will no doubt be challenging. That said, technology businesses are well positioned to help customers adapt to new operating environments, be that the support of effective home working or improving business efficiency through automation. Difficult market environments change business priorities and create opportunities for innovation, and it is important to be ready to adapt to meet client needs. A good example of this is the client money protection regulations introduced following the 2007/2008 Global Financial Crisis. This created an opportunity for AutoRek and now more than 30% of our clients use our software to help them comply with the regulation.

Operationally the company has continued to perform very well and deliver for our clients however undoubtedly many of our team, including myself, are missing the day to day interaction of the workplace. Our team culture is central to who we are as a company, while remote working has become the new “norm” and is undoubtedly here to stay we are all looking forward to the opportunity to get back together as a team.

What do you think the future of automated reconciliation is?

The availability, quality and integrity of data within a financial services company is critical to its success. Whether it is understanding the business performance of a new product line, delivering quality services to clients or complying with regulation a key requirement is almost always about getting data right.

Data volumes are growing at almost exponential rates and regulatory demands continue to create significant strain on the industry. At the same time market disruption from new Fintech start-ups and large multinational tech platforms like Apple and Google leave the more established financial services organisations needing to accelerate innovation while at the same time reduce the cost of operations.

Empowering key decision makers, finance functions, compliance or customer management teams requires tools which are easy to use and support non-technical users in collating, reconciling, aggregating and analysing increasingly large and complex data. Recent developments in robotics, artificial intelligence and machine learning technologies present significant opportunity to reduce the complexity, automate manual processes and accelerate decision making for our customers.

What are the main challenges for regulatory reporting?

Over the past decade, in the aftermath of the global financial crisis, the finance sector has been swamped by regulatory change. Large established organisations as well as new entrants are required to comply with these regulations while at the same time evolve their customer service offering to keep pace with the increasing expectations of the digital consumer.

- Being clear and transparent – Regulators continue to test firms with a focus on restoring confidence in markets and improving transparency and fairness. Automating and integrating regulatory reporting, increasing operational efficiencies and mitigating risks are key to relieving some of the pressures compliance brings.

- Managing Data – Both regulators and auditors expect organisations to be in full control of their data. This means understanding the completeness and accuracy of the data used to complete regulatory returns. AutoRek works in conjunction with existing systems to complete and perfect financial and operational control processes. Our solutions help firms overcome spreadsheet intensive data management and reporting processes, ensuring ongoing control and regulatory compliance.

How would you describe Scotland as a place to launch, develop and grow a tech company?

Scotland has a reputation globally of producing talented graduates with an excellent attitude to work. Our universities produce thousands of graduates in tech, maths and sciences allowing us to attract some of the world’s leading financial organisations. While this has an impact for home grown companies, e.g. when competing for staff, it has also been key to creating the thriving digital economy and growing Fintech sector that we have today.

Ultimately for most companies the key to success is having a great team. Of course, there are some overnight successes but the majority of businesses develop and mature over time. The fantastic quality of life with low commuting times and excellent cultural scene make Scotland a great place to start and grow a business.

What does the future look like for AutoRek?

Although we have a number of global clients, for the last 25 years, AutoRek has predominantly been working within the UK market focussed on Asset Management and Banking sectors. In 2020 and beyond (this year being slightly delayed), we are looking to grow our business in the US and further develop our presence in the Insurance sector. With having an established partnership with Cforia Software Inc, a working capital and accounts receivable (A/R) automation software, we are well on our way to achieving our goals.

UK tech demonstrates resilience amid virus crisis

Tech Nation and Dealroom published a report for the Digital Economy Council. It highlights that investors are still active in the tech space, despite the challenges posed by COVID-19.

UK digital tech companies are still attracting investors and are still recruiting. Most of them declared being optimistic about their ability to navigate the crisis. On the investment side of things the UK outperforms all of its European neighbours.

The report shows that British tech companies are resilient with tens of thousands of jobs advertised in cities across the UK in 2019 and the start of 2020, with salaries continuing to grow well-above inflation in almost all regions.

London leads the way and is a global tech leader with London-based companies raising $4bn since the start of January, more than Paris, Stockholm, Berlin and Tel Aviv combined. But other regions including Scotland are also doing well with Glasgow and Edinburgh leading the way.

Digital Secretary Oliver Dowden said:

“The UK’s tech sector has shown resilience in these challenging times and the levels of investment in the year to date have consolidated our Europe-leading position.

“We have a vast pool of talent in the country’s digital and tech firms who have played a big part in supporting communities across the UK and beyond throughout the pandemic and I applaud them for their ongoing efforts.

“The government will continue to champion and support the sector as it navigates the months to come as we step up our Coronavirus recovery plans. We will back entrepreneurs, encourage innovators and help businesses make the most out of the opportunities the digital and tech world provides.”

UK’s position of strength

The UK’s tech sector went into the coronavirus crisis in February in a strong position. From January to the end of May, tech companies raised $5.3bn, compared to a total raised in the rest of Europe of $4.1bn. However, there are concerns that many of these deals were agreed in principle before the onset of the virus, which has reset expectations. Capital inflows in the second half of the year are unlikely to be as strong as those in 2019, itself a record year.

In April, the Government unveiled its Future Fund of £250m of matched funding for startups, so that tech companies which are typically loss-making could access support. Equity backed small businesses right across the UK are developing vital innovative products and services that have the capacity to help the growth of our economy in the months ahead as we emerge into economic recovery. Yet many of these businesses need further support and investment to withstand the impact of the coronavirus crisis to ensure that they can survive and successfully continue to build and commercialise their innovations.

However, startups are fragile businesses and recent data gathered from 200+ companies for the venture capital community shows that:

-

Two-thirds expected revenues to drop by more than a quarter

-

39% of business to consumer companies saw March revenues drop by over 50%

-

A third of companies have slowed hiring, while almost a half have frozen hiring

-

Two-fifths of companies believe they have less than 12 months of funds

Gerard Grech, chief executive of Tech Nation: “Many businesses are adapting and innovating to support the fight against coronavirus, demonstrating the resilience and resourcefulness of the UK tech sector. Although we are seeing many tech companies closing key rounds of funding, the picture is being monitored closely at Tech Nation, especially across different parts of the country, where access to finance may not be as strong. These findings today confirm that the UK is well positioned to face the challenges that lie ahead and leave Covid-19 in a position of strength.”

Diversity up, Inclusion down – Business Impact & Solution

Let’s start with an existential question – why do we even exist as human beings?

An ultimate accomplishment is to have complete and unhindered self-expression. For most of humanity, this happens best in the context of love, respect and belonging since it makes us feel safe and courageous. We also know that the opposite of courage is not fear, it is conformity. And conformity suppresses creativity and self expression.

Honest D&I is an organization’s way of saying “I love you and I respect you” and leaders have the highest leverage and impact of anyone. For some time this has been a space where the answer to the question of being a company that believes in and practices D&I was “we think so”. It does not have to be that way anymore. People Analytics and in particular ONA (organization network analysis) is a tool companies can use effectively, at a relatively low cost in relation to ROI, to visualize, measure and constantly make increments. We will get to this a little later.

Diversity Doesn’t Stick Without Inclusion

As per HBR, “Diversity” and “Inclusion” are so often lumped together that they’re assumed to be the same thing. But that’s just not the case. I”‹n the context of the workplace, diversity equals representation. Without inclusion, however, the crucial connections that attract diverse talent, encourage their participation, foster innovation, and lead to business growth won’t happen. Numerous studies”‹ show that diversity alone doesn’t drive inclusion. In fact, without inclusion there’s often a diversity backlash.

As noted diversity advocate ”‹VernÄ Myers”‹ puts it, “”‹ Diversity is being invited to the party. Inclusion is being asked to dance.”

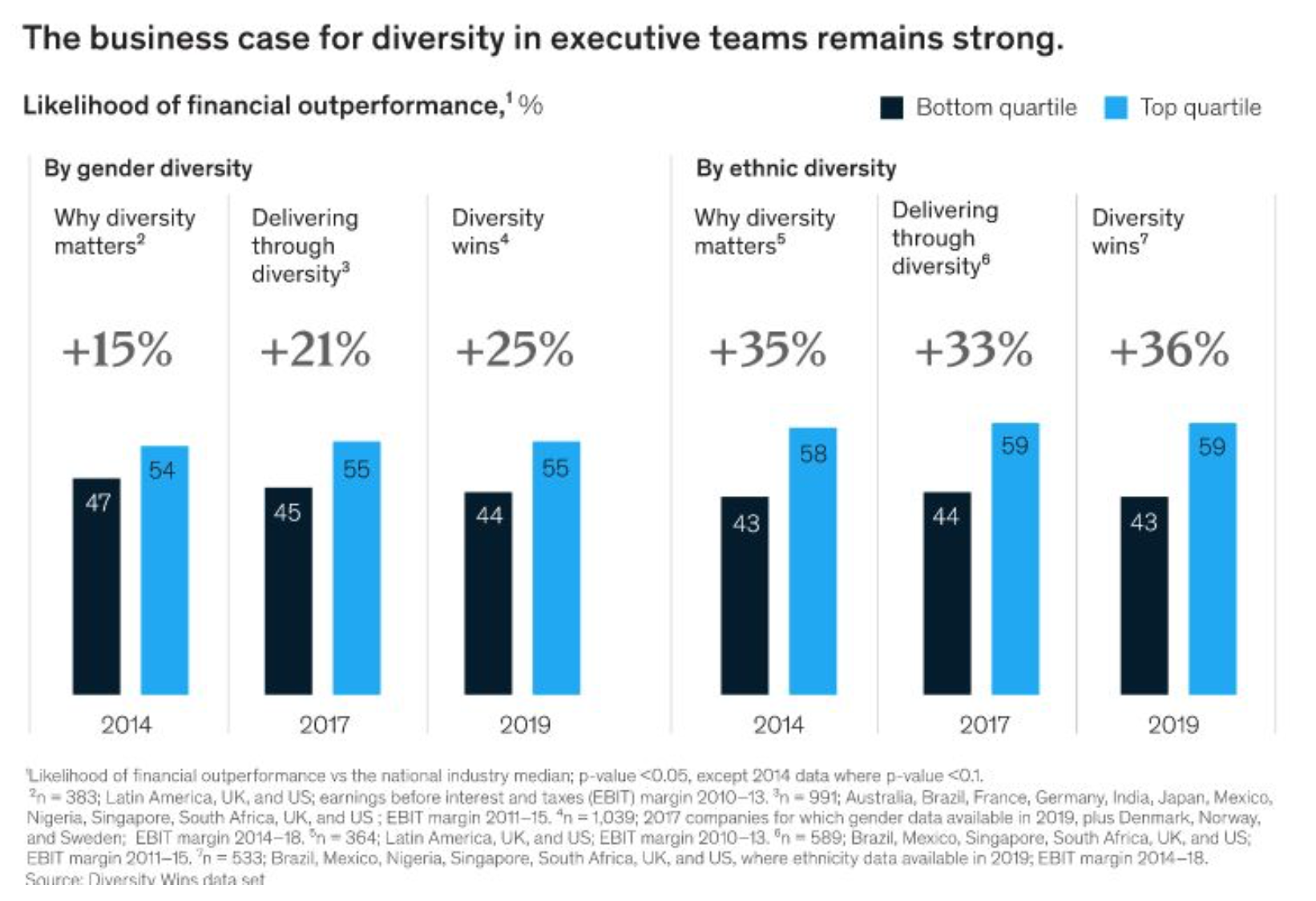

McKinsey has been researching this domain for numerous years. The findings below emerge from their largest data set so far, encompassing 15 countries and more than 1,000 large companies. They have incorporated a “social listening” analysis of employee sentiment in online reviews and their findings highlight that companies should pay much greater attention to inclusion, even when they are relatively diverse.

Diversity – Key Takeaways:

- Likelihood of outperformance continues to be higher for diversity in ethnicity than for gender – a substantial differential likelihood of outperformance””48 percent””separates the most from the least gender-diverse companies.

- The greater the representation of women, the higher the likelihood of outperformance; Companies with more than 30 percent women executives were more likely to outperform companies where this percentage ranged from 10 to 30,

- companies in the top quartile for gender diversity on executive teams were 25 percent more likely to have above-average profitability

- despite the awareness, there is a widening gap between D&I leaders and companies that have yet to embrace diversity; the representation of ethnic-minorities on UK and US executive teams stood at only 13 percent in 2019, up from just 7 percent in 2014

- In 2019, fourth-quartile companies for gender diversity on executive teams were 19 percent more likely than companies in the other three quartiles to underperform on profitability””up from 15 percent in 2017 and 9 percent in 2015.

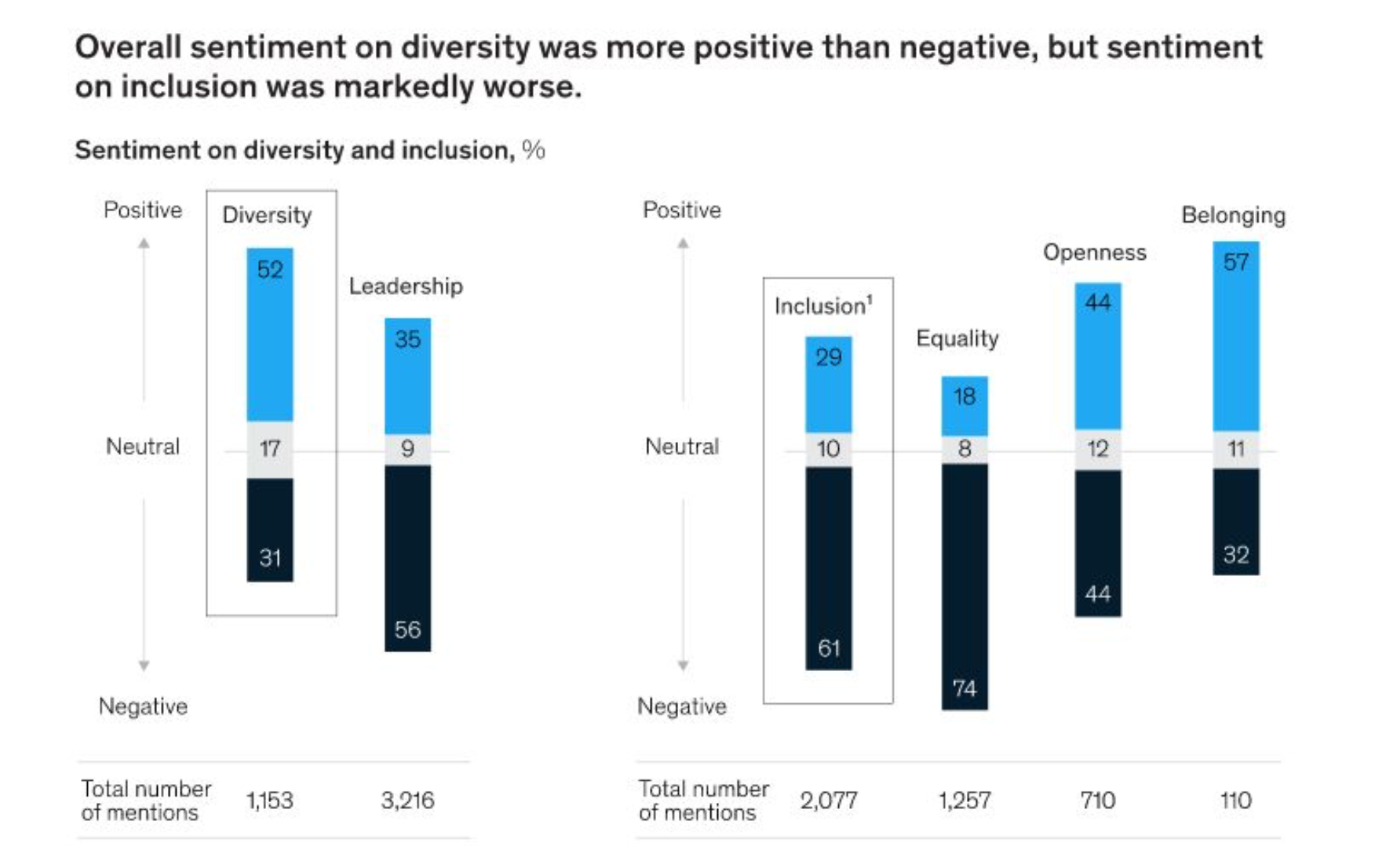

Diversity without inclusion is a story of missed opportunities. Here are some key takeaways from McKinsey’s outside-in research using “social listening,” focusing on sentiment in employee reviews of their employers posted on US-based online platforms. While this approach is indicative, rather than conclusive, it could provide a more candid read on inclusion than internal employee-satisfaction surveys do

Inclusion – Key Takeaways:

- While overall sentiment on diversity was 52 percent positive and 31 percent negative, sentiment on inclusion was markedly worse, at only 29 percent positive and 61 percent negative.

- For the three indicators of inclusion””equality, openness, and belonging”” their research found particularly high levels of negative sentiment about equality and fairness of opportunity.

- Negative sentiment about equality ranged from 63 to 80 percent across the industries analyzed. Negative sentiment about openness ranged from 38 to 56 percent

- Belonging elicited overall positive sentiment, but from a relatively small number of mentions.

HBR research finds that employees with inclusive managers are 1.3 times more likely to feel that their innovative potential is unlocked. And therefore employees who are able to bring their whole selves to work (i.e. who feel included) are 42% less likely to say they intend to leave their job within a year.

Societal Context

Let’s zoom out for a second into a wider societal context. Over 9 million people in the UK ”“ almost a fifth of the population ”“ say they are always or often lonely. The Brits may not be the only ones feeling this way. The overuse of technology is a cause of depression, social anxiety and a lack of meaningful connections. And if we add to this lack of feeling included at work, what kind of a society will we end up creating? This impacts everyone – our own partners, kids, parents. With only a handful of aware individuals (leadership), a world of good can be created in society.

Not only it D&I is right from a humane perspective, but data not only suggests that it makes a good deal of business sense; organizations with the D&I”‹ esprit de corps’”‹ position themselves for business success by attracting the right kind of talent and making them feel like they are in the right place. This spurs safety, feeling cared for and as a result the release of the creative genie out of the bottle for out of the box thinking, non-conformist thinking and exemplary performance. The stats are above to make the business case.

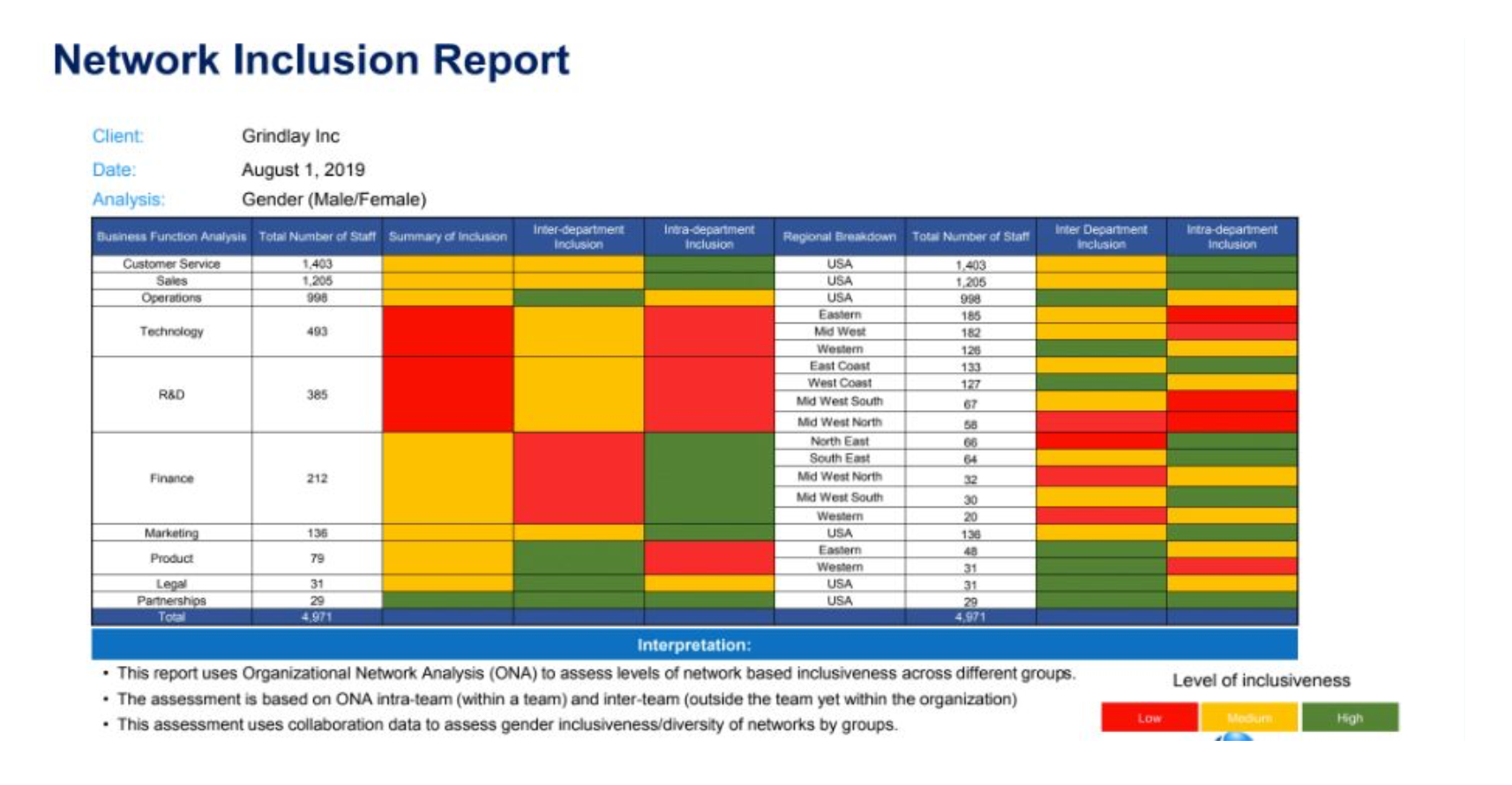

Using Organization Network Analysis for insights into D&I to track and report progress

For some time this has been a space where the answer to the question of being a company that believes in and practices D&I was “we think so”. With Organization Network Analysis (ONA), it does not have to be that way anymore! ONA can be used not only to measure diversity but also to measure network activity and analyze the immersion of different employees across the organization

With ONA, you can map and analyze patterns of interaction across relationship networks of every employee, so Diversity & Inclusion leaders can understand where differences exist in specific groups of employee’s networks in different hierarchies.

Even relatively diverse companies face significant challenges in creating work environments characterized by inclusive leadership and accountability among managers, equality and fairness of opportunity, and openness and freedom from bias and discrimination. However with the right tools, technology and data, you can measure the impact of your various D&I initiatives and make required improvements on an objective basis.

Puneet Sachdev is International Director, Human Capital at The Singularity Lab. The Singularity Lab is an integrated human capital consultancy, helping technology companies achieve exponential results by attracting and retaining top talent and creating high performing inclusive cultures based on data, design and technology. Learn more about our”‹ ”‹ONA solution”‹ for D&I.

Mental Health in the workplace under COVID-19

Coronavirus is inevitably something which has affected us all. It has affected how we feel, how we work, and how we live. We want you to know that no matter how you are feeling during this time, you are 100% not alone. You are completely normal. You are acting like a fully functional human being reacting to threat, and we are all hardwired to do this.

So what is the hardwiring of humans that makes us feel anxious, irritable, and unmotivated during this worldwide pandemic? We explore what roles various parts of the brain have to play in our reactions to this threat. We are hopeful that by gaining an understanding of these functions, we can recognise and respond in ways that will work more effectively for us.

None of us really have any control over the coronavirus spread, or the economic situation. But we can act to help ourselves. We believe that through having structure and routine; acknowledging our thoughts and feelings; practicing mindfulness; becoming aware of our breathing; taking care of our physical needs; and considering our personal values, that we all might be able to take some steps towards improving our mental health during these times.

Below you can find our blog around Mental Health and how OK Positive can help with supporting you individually and your company.

Coronavirus, Autism and Fintech

The Coronavirus crisis has led to the largest move to remote working that anyone has ever seen, with many companies switching to homeworking almost overnight. I have witnessed some surprising lessons on the power of neurodiversity in a crisis like this.

Autism and the fintech opportunity

When we founded auticon in 2011 we believed that diversity is a strength that enhances problem-solving ability. Neurodiverse people often excel at business intelligence, quality-assurance, test automation and complex software development projects. They have unique cognitive strengths: attention to detail, a systematic way of working, logical analysis, pattern recognition, error detection and sustainable concentration for routine activities.

Autistic individuals are equally capable of excelling in STEM subjects and many achieve degrees or advanced qualifications. However, in a recent survey of more than 3,000 technology leaders, IT outsourcer Harvey Nash and auditing firm KPMG found that 67% reported that a skills shortage was preventing their organisation from keeping up with the pace of change. Autistic people are often overlooked or not considered as a source of talent, with some studies showing that up to 90% are either unemployed or underemployed.

The fintech sector is one that could benefit massively from onboarding neurodiverse people with STEM related skills and above average attention to details.

Autism and homeworking

Prior to the coronavirus crisis, most consultants at auticon worked from client sites or from our offices. That seemed to be the best way to make sure everyone performed at their best. Autistic workers like consistency in their office environment and routines. We employ Job Coaches to work closely with our consultants. They suggest adaptations to work environment, smooth out any bumps and ensure that our consultants are set up for success. They are also on hand to support our clients.

We had to change all of this when the coronavirus struck and on 23rd March, we matched our clients and transitioned all of our team to homeworking. Fortunately, everyone already had laptops and mobile devices, so we didn’t have to worry about the technology part of the equation. Our main concern was whether we could maintain productivity.

Overall, this has gone better than we hoped. Traditional managers at many organisations may worry that team members who work from home may not put in the same level of focus or be able to meet deadlines. We never have to worry about this. Autistic people tend to be very direct and honest. If you ask them if they are being productive working from home, they will tell you the truth. (If they were watching Netflix, they will tell you that, too.)

auticon consultant, Kyle Walker says he actually prefers working remotely as for him, the most stressful part of his day was the bus journey to his client’s office. With that out of the equation, Kyle is very happy and probably a little more productive on his client’s project.

The tech tools we used for remote communication, such as Slack, Zoom and Microsoft Teams, also work very well for us. Autistic people often prefer to interface via a precise text or email. Verbal or face-to-face conversations, which involve body language and emotional expression, can be more subjective and challenging. Some of our consultants who aren’t comfortable making eye contact in person found that they were able to do so on Zoom calls, giving them a new way to connect.

The Coronavirus challenge and opportunities

We have seen additional business opportunity during the coronavirus crisis. Going virtual has meant our global operation is working together more closely, leveraging a much deeper resource pool with specific technical capabilities in near real time. We are working across multiple time zones to assist clients with rapid deployment in a very cost-effective way. This global virtualisation may have taken us months or years to realise prior to the crisis.

Having a team capable of working very effectively from home is powerful. Beyond the current coronavirus lockdown, many organisations will rely much more on remote working and need to have a workforce that’s capable of doing this effectively. In auticon’s experience, hiring more autistic people is an answer. Not only does it bring more diverse thinking to a team but it is also an ideal way to make sure that you are staffed up with people who naturally excel at remote work.

Written by Emma Walker, Regional Manager ”“ auticon Scotland

Auticon provides a neurodiverse and agile workforce to improve clients information technology projects predominantly in areas such as Data Science, Quality Assurance and Cyber Security.

Photo by Polina Zimmerman from Pexels

Time to secure our emails

In February I wrote about the growing awareness of cybercrime targeting the financial services and the industry’s need ”“ and I would say duty ”“ to help protect consumers and businesses against this invidious problem which has been growing year-on-year. Little did we know at that point what was coming down the line.

The current crisis in which we find ourselves ”“ with the public fearful of the pandemic and businesses having to enable staff to work from home ”“ have made both even more vulnerable to cybercrime. Cybercriminals are playing on not only people’s fears around the Covid-19 pandemic but also the unprecedented need for staff to work from home, stretching companies’ communications channels and security systems.

Regulators, including the Financial Conduct Authority (FCA) and The Pensions Regulator (TPR), have issued warning statements on cybercrime and scams, a clear indicator of the seriousness with which they take this issue and the extent to which it is a problem ”“ see FCA: https://www.fca.org.uk/news/news-stories/avoid-coronavirus-scams/.

Incidences of scams, like phishing and smishing’ ”“ i.e. when criminals use emails or text messages to impersonate individuals or organisations to trick people into giving away their personal and financial information or money ”“ are reported to have increased notably over the past few weeks as the Coronavirus has taken hold.

At the same time, the need for data and information, including that of a personal and confidential nature, to move outside of companies’ security systems, has increased the risks for businesses, including that their communications will be intercepted.

For the financial services industry, this risk has been exacerbated by the end of the tax year and the need to meet tax and investment planning deadlines, which has meant advice firms have needed to get client requests and information to platforms and providers in the most expedient way.

As you might expect, most communications are by email, particularly between adviser and client, because that is the most familiar, fastest and easiest channel to use.

As mentioned in my article in February, working with leading cyber security specialist Beyond Encryption, we have developed and launched a new encrypted email solution for the financial services industry, in particular aimed at protecting the communications between product providers, platforms, advisers and end clients.

So, to help financial advisers secure their email communications during the crisis, we’re providing two months free use of the Unipass Mailock premium service for our Unipass identity service users in advice firms. To take advantage of this, users simply enter a voucher code (2monthsfree’ via www.unipassmailock.com/) to get access and there is no automatic renewal and no payment information required to get started.

It is our way of helping the industry to tackle this particular issue which has been magnified by the current unprecedented crisis we are all experiencing.

I would add that in an industry where transmission of data is key, and emails are the primary communication channel and will remain so for the foreseeable future, now, more than ever, it is time to secure our emails.

Research – Why 4 in 10 businesses abandon banking applications?

200 companies took part in this survey which tool place after the Chancellor of the Exchequer announced a £330bn rescue package to help UK companies through the Coronavirus situation.The results also show that companies plan to prioritise spending on cybersecurity over anti-financial crime compliance. Indeed, over 80% of firms said they were confident in their understanding of exposure to financial crime with the appropriate processes being implemented.

However, when looking at the data, just over 40% of them said they did not regularly put customers and suppliers through formal KYC processes and 60% of them hadn’t trained their collaborators on how to be compliant with the Fifth Money Laundering Directive (5MLD)

You can read the full research and more here.

How Fintech Will Shape The Future Of The Forex Market

Among mainstream investing opportunities that exist outside of the stock markets, forex trading has long been a popular option. Today, this market is the most liquid in the world, and handles a massive amount of trading activity. But it’s also a market that has evolved over the years with some thanks to technology ”” which makes it one to watch as we observe how fintech continues to develop.

The earliest sign of technology helping to expand the forex market, aside from the actual beginning of the internet age, was perhaps the emergence of smartphones and the accompanying apps. Home Business wrote a piece just two years ago covering mobile tech’s effect on the world of investing. Basically, the idea is that the connectivity phones now provide give investors unceasing access to financial markets, which in turn leads to greater liquidity and volatility. This is absolutely the case in the forex market, which traders tap into from all over the world at all hours of the day.

Alongside the involvement of mobile devices, investment markets have also seen the rise of a growing number of accessible tools and analysis that can simplify the trading process (and in some cases even make it easier to generate gains). For instance, the same article from Home Business pointed out that mobile algorithms and applications are now available, and can often provide automated glimpses of the best trading strategies. And regarding forex specifically, FXCM shows how readily available profit calculators can now provide near-instantaneous clarification of the profit and loss potential of any given trade. This enables investors to make mathematically strategic decisions far more efficiently than in the past.

These are all examples of tech’s increasingly large role in investments, and in the forex market in particular. And while they don’t necessarily fit into what we now think of as fintech, they helped to pave the way for some of the fintech-related changes we’re beginning to see in how the modern forex market actually functions.

For an existing example, we can turn to our overview of Fexco, which is currently one of the world’s most established fintech companies. Fexco includes foreign exchange sectors among the areas it provides services to, and specifically helps to facilitate cheaper and more reliable transactions. It does so, as we noted in the overview, via the PayDirect portal, which is certified for information security. In simple terms, this is an example of tech-based secure transfer enhancing the appeal of forex transactions.

In the near future, we may see more examples like this, including some that take advantage of newer and more innovative pay transfer technologies. Specifically, it’s become increasingly likely that banks and private companies facilitating forex trades are going to take advantage of the blockchain. Business Insider spoke about this last year, making a note that HSBC had already “settled $250 billion in FX trades” using the blockchain in 2018. That’s an almost shockingly large number that would seem to indicate that this method of transfer is well on its way to widespread use. And the blockchain, some would argue, is the very definition of modern fintech.

As we look forward, there’s no reason to suspect anything but a deepening relationship between fintech and the forex market. Traders will continue to use the devices, tools, applications, and algorithms made available to them to make smarter and more informed decisions. And the investments themselves will continue to be carried out via the most secure and efficient technological methods.