Fintech Fuse – A Festive FinTech Fusion, preparing for 2020!

Just time to fit in a final fusion blog for 2019 before clocking off for 2019 and the festive holiday.

A frantic run in to the festive period has meant I’ve had little time to keep up with a regular blog so please forgive random rambling of the last couple of months!

Festive Community

Very fitting that the festive spirit was very much in the air at the FinTech Scotland Fusion event with the community last week at one of Edinburgh’s most popular fintech hubs, The Green Room!

Wonderful to see so many of fabulous fintech leaders and entrepreneurs join us for a glass of wine or two for the occasion magnificently hosted by special friend Sarah Ronald. Big thanks to the brilliant Stuart, Darren and LendingCrowd team for their generous Christmas hospitality.

A similar uplifting spirt was evident at the Modulr fintech community event the previous month, recognising the terrific progress by the team and the exciting plans ahead. It was super to see so many of the fintech community there for the evening.

The diversity of Scotland fintech community is one of the core strengths and engenders amazing collaboration and innovation.

For example, as shown in the support provided by how the community in getting behind the MoneyMatix crowdfunding exercise recently, inspiring to see.

Furthermore, collaboration boosted by fintechs coming to Scotland from all parts of the world.

For example, meetings over recently with Alex and Monika of Polydigi (Hong Kong), Gopal of BlackArrow , Shendon and Michael of Gobbill as well as Izzy and Paul of Veriluma (all from Australia) reinforce the global make up of the community.

This was a key theme I was able to share in presenting at the FinTech World Forum in London last month to a very diverse global leadership audience which I am told further reinforces Scotland position as an International fintech centre attracting entrepreneurs and innovators.

Meeting our close European partners has also been a key activity over last few months and we are excited to join eight other fintech centres across Europe in the Discovery Collaboration Programme connecting firms with opportunities across our continent.

In addition, it has been great to meet with senior leaders from the French Embassy to talk about collaboration opportunities.

Our ongoing close engagement and friendship with colleagues across our European continent continues to be a key focus in demonstrating to Scotland remains very much open to shared innovation.

Mickael’s ongoing value leadership in building our global FinTech connectivity to support the community in Scotland continues to play an important role.

Alongside this it has been brilliant to work with our super Scottish Development International colleagues to welcome fast growing fintech firms from Hong Kong , Canada, China, Korea all looking at Scotland as a future home for their innovations

Massive thanks to the fabulous Andrew Wykes, Kirsty Russell, Sarah Kenrick and team at Lloyds Banking Group for recently hosting the Hong Kong and Canadian delegations and arranging the festive market to add to the fintech atmosphere in December .

All of this is reflected in the brilliant examples of the FinTech community in the Herald Business supplement a couple of weeks ago. Terrific writing Kim McAllister very much appreciate your engagement and coverage of fintech developments in Scotland.

Kim and I had the opportunity to discuss these developments with other leaders one evening recently at a session organised by Malcolm Buchanan , Mike Crow and the RBS team .

The impactful innovation and leadership by Kristen and the RBS team is hugely valuable to the significant progress and we very much appreciate their ongoing collaboration and support. It is also great to see exciting initiatives such as the exciting Accelerator Hub in central Edinburgh

Festive Collaboration

Collaboration very sits at the heart of innovation progress across Scotland and one of the most memorable examples of this was the recent Glasgow University FinTech Society challenge event, it was also one of my best FinTech Friday’ evenings ever!!

Awesome leadership by Elisabetta, Andrea, Davide and the Society committee bringing together the energetic and diverse students, terrific academic leaders John Finch and Dominic Chalmers, fintech entrepreneurs Sustainably, heavyweights Deloitte and the innovative Chris O’Neill of M3.

Wow, what an evening of fintech, wine, curry and yes a Jazz band with entertaining presentation interlude by the fabulous Lou Smith and a half time fill in by me!!

Back home after midnight with fintech jazz’ ringing in my ears but the evening said everything that is so special about the fintech movement with focus on people and a festive atmosphere.

The festive collaboration was also very much in evident at the FinTech National Network investor pitch day’ at Level 39 in London this week.

Terrific work by the super Hayley, Peter and the Innovate Finance team in bringing together investors to hear from fintech firms from around the UK. Thank you Charlotte Crosswell for fabulous day, super atmosphere and the ongoing leadership in 2019.

Very proud of the presentations by Nick of Edinburgh based Zumo and Kyle of Glasgow based Financial Cloud in articulating their compelling and innovative fintech propositions

Also, really great to catch up with fintech comrades from Wales, Northern Ireland, North and West as well as Tom Helm from DIT as we all reflected on our shared ambitions for fintech and the collaboration opportunities in 2020.

The investor pitch event followed on from the very first FinTech National Network event in Glasgow back in October.

Bringing together the Scottish fintech community with peers and stakeholders from across the UK was one of the many big highlights for 2019.

The event saw Alex of Encompass, Laura of Amiqus, James of Direct ID and Andrew of Soar from the Scottish community share compelling stories about how they are developing their FinTech proposition to make a real difference.

Also, excellent presentations from the very engaging FCA team Laura Navaratnam and Steven McWhirter as well as Kevin Telford on sharing the impact the world of open finance can have on peoples lives.

Very fitting the event was hosted in the University of Strathclyde which is leading the awesome development of the Glasgow City Innovation District of which fintech is a growing and significant cluster as brilliantly covered by Eleanor Shaw.

Many thanks to the University and City Council for supporting this significant event along with Glynn Robinson and the super team from BJSS team.

Listening to great presentations from Andrew of Northern Ireland, Gavin of Wales , Julian of West and Dan of North on the day reminded us all that we can learn so much from each other as we develop our respective FinTech communities.

The wonderful finale of the day was a focus on people inclusion and diversity with such valuable insights coming from the panel of Lou Smith, Elisabetta from Glasgow University, Laura and Nicola

It was a privilege to co-host the day with my Ant and Dec’ partner, Chris Sier who was as engaging as always in bringing alive the importance of the FinTech innovation for everyone.

I know next year will bring even more wider international collaboration opportunities and it was great to chat this through with Phil, Rory and Isaac of FinTech Alliance over a few glasses on Tuesday evening . Thanks guys, looking to hit the ground running early next year.

Festive Innovation

The run up to the festive period has certainly fueled fintech innovation examples with the community covering a very broad range of themes

For example, it was great to have the inspiring entrepreneurs Phil from Castlight and Manu from Inbest come along to the FinTech Scotland Citizen Panel to share the positive impact of fintech innovation.

The Panel plays a crucial role in identifying how we can collaboratively address issues such as financial inclusion and tackling problem debt amongst citizens working with the third sector, universities, Government and regulator.

A huge thank you to colleague Nicola Anderson for leadership on this area and privilege to work with Nicola and have the secondment to FinTech Scotland extended for another year from the FCA.

More real innovative fintech examples were on show at the University of Edinburgh Business School non executive director course one Thursday evening recently.

This again was a real pleasure for me as I was joined by three absolutely inspiring leaders for the evening to share real life case studies on the leadership needs of growing fintech enterprises.

Many thanks again to the magnificent three, Colin of Float, Sonia of Level E and Aleks of newly formed Exizent for such engaging evening with the senior leaders from across Scotland .

Thank you also to John Amis of the University as well as Ailsa and Judy of FWB Park Brown for the opportunity to put fintech in the non-executive programme for senior leaders.

This week the festive innovation extended to the world of crypto assets and I was very proud to invite three leaders in this field to join me at the Scottish Government Working Group with the Lord Advocate and Lord Hodge.

Fantastic contributions to the discussion on the opportunity by Paul of Zumo, Christine of Women’s Coin, Richard of QWallets , thank you and more to come on this in 2020 especially in demonstrating fintech as a force for good.

This was also very much brought alive during the FinTech session I was invited to host at the Global Ethical Finance Conference at the RBS campus a couple of months ago.

Fantastic examples shared by Georgia of Tumelo and Christine of Women’s Coin on the role of FinTech innovation having an important social impact.

Another area getting some good focus from fintech innovation at present is cyber security and financial crime being led by Nicola.

The joint event recently with Police Scotland and National Crime Agency was very insightful. Many thanks to Leanne of Nucleus, Rachel and Dave of Amiqus and Mike of Modulr for their valuable engagement and leadership on this.

The FinTech collaboration initiatives extend across the public sector and it was brilliant to witness first hand the progress being made in collaboration with the Scottish Government Digital team.

Fantastic to see this demonstrated with Minister Kate Forbes by the fabulous Trish, Hugh, Carron, Mike and terrific teams last week, very much looking forward to the collaboration progress in 2020.

Fintech was very much on show at the CanDo Innovation Summit recently in Glasgow and it was terrific to be part of an amazing event with the other exciting industry clusters driving new initiatives.

The fintech examples were brought alive in the auditorium by Loral and Eishel of Sustainably, Colin of Float and Duncan of Modulr and it was a privilege to host the showcase.

Festive Cluster

The Glasgow fintech cluster is very much going from strength to strength in so many ways and it was great to share the progress with the City Economic Leadership team a few weeks ago, thank you Mark Napier, JP Morgan for the opportunity and continuing collaboration

The action packed FinTech Scotland partnership with University of Strathclyde team is giving valuable momentum to the fintech initiatives and we are really excited about progressing in 2020 as part of the City Innovation District.

Thank you to Eleanor Shaw, David Hillier and terrific team for valuable leadership on this

Building on this with great sessions with innovative leaders Samantha Bedford and Virgin Money team, Tara Foley and Bank of Scotland team, David Ratcliffe, Stuart Brown and Barclays team as well as Ali Law and Paul Gallagher of Royal London provide great new collaboration opportunities for 2020.

Sharing these Scottish fintech developments with a worldwide audience is always on the agenda and it was great to join Alex Ford of Encompass on a podcast along with Lou Smith.

Thank you Cheri Burns for making this happen and the opportunity to share the message. Also, very best wishes to Alex has she moves to New York to expand the Encompass innovation on the other side of the Atlantic.

Of course, the fintech cluster is developing across Scotland and it has been great to work with inspiring Jane Morrison-Ross, chief executive of ScotlandIS along with fabulous Svea, Katy and Ciara on joint initiatives to develop the digital economy. This is a core focus for us in 2020 with much more to come!

The fintech cluster developments require broad collaboration such as with ScotlandIS and Edinburgh Chamber of Commerce who provide valuable leadership in the Scottish economy.

Great working with the super Liz McAreavey, on the Scottish and international opportunity.

In addition, its been fantastic working in collaboration with our colleagues at Scottish Enterprise and the fintech network integrator team, Vivolution, making the Scottish cluster embrace the innovation opportunities.

Working with the University of Edinburgh team on a range of opportunities means the fintech cluster in the capital is going to go from strength to strength in 2020.

The Wayra cohort in Bayes , led by the brilliant Charlotte Waugh is a terrific example of this and it is great to see the progress by James of Xpand and Evangelos of Ocyan

Then wider across Edinburgh, great to catch up with Paul, founder of Inifinity Works who have recently set up in Edinburgh as well as Scott and Raymond from Exception to talk through collaboration opportunities. These are just two examples of many that make life so fascinating in Scotland’s developing fintech sector

We have been running hard to keep up with the fintech momentum across the whole cluster in Scotland and Shery has done an amazing job in keeping us organised between meetings , speaking engagements and project sessions throughout the year.

Festive Running

I’ve also been fortunate enough to maintain my running addiction during this last frantic few months of 2019, infact it seems to have helped my racing performance!

The highlight being the recent Loch Ness Marathon with my best time in nearly three years at 3 hours 16mins which is giving me great hope for my times next year!!

This was followed up a couple of weeks ago with a 1 hour 32mins for the Water of Leith Half Marathon which also left me buzzing.

As with fintech developments in Scotland, if I can keep this race momentum into next year then we could be hitting some new peaks results in 2020!!However, for now it is time to relax and enjoy the festive holidays with my very special family as well as a bit of running around the roads and paths of Scotland whilst having a few small dreams on what the year ahead will bring. Until then…..

Financial wellbeing and the impact in the workplace

Photo by energepic.com from Pexels

Financial wellbeing ”“ the theme of Talk Money Talk Pensions Week 2019 ”“ is about feeling secure and in control of your money as well as being able to manage day-to-day while working towards a healthy financial future. We think it’s important to not only consider how individuals can build their own financial resilience wellbeing but also how employers can support their staff in developing lasting financial capability strategies.

A recent report from Natwest (https://www.moneyadvicescotland.org.uk/Handlers/Download.ashx?IDMF=f4148ec3-ec0e-468b-ae07-7f615fc34548) recommends that employers should, at a minimum, include financial capability training and support as a standard part of their employee induction process, and a growing body of evidence shows that there are clear benefits of investing in this for all employees at all stages of their career. The importance of financial education at work and the benefits it has for both employees and employers is why we developed Money Works ”“ a programme that exists to promote financial wellbeing in the workplace and provide vital financial inclusion skills for employees and apprentices across Scotland.

Research has found that levels of financial capability and wellbeing very greatly from person to person. An individual’s salary, age, or employment history does not necessarily correlate to their confidence or ability to manage their earnings or their state of financial wellbeing. It therefore makes sense to offer financial wellbeing support to all employees.

The arguments for providing financial wellbeing support in the workplace are strong; firstly, the impact of poor financial wellbeing on productivity is significant. Anxiety about finances leads to worse mental, physical, and social wellbeing which can affect attendance and performance at work. The Chartered Institute of Personnel and Development found that money worries were the biggest source of stress for UK employees.

According to research from Barclays:

-Almost half of employees worry about their finances

-1 in 5 lose sleep worrying about their finances

-1 in 5 said that worrying about their finances affects their work

-Almost 80% of employees are not satisfied with the efforts of their employer when it comes to managing their finances

This evidence shows how great an impact an individual’s financial wellbeing has on their overall wellbeing, and how intrinsically linked money worries and work are. Both employers and employees agree that if employees had access to help and guidance, they would have better control over their money and feel better prepared for future planning. If this support is available in the workplace, employers can help ensure their staff are better prepared to respond to financial unpredictability, in turn alleviating some of the pressure points that lead to absence and stress.

One of the aims of Money Works is to provide a reliable, flexible source of financial guidance. Participation in our financial wellbeing in the workplace sessions benefits both employees and employers. Employees gain vital financial resilience skills and get access to resources that research shows is needed and wanted. Employers benefit from a more motivated and productive workforce, as well as highlighting them as an employer that is committed to investing in employees’ overall wellbeing.

Our Financial Capability team designs custom workshops and works with employers to meet the needs of their staff, and workshops are delivered in the workplace.

Possible topics include:

-Planning for retirement

-Day-to-day financial management

-In-work benefits

-Savings (including emergency funds, ISAs, saving for a deposit)

-Insurance (including life insurance)

-Managing credit card debt

-Understanding taxes and payslips

These topics are based on research of what employees would benefit from knowing more about. For example, 22 million working-age adults don’t feel that they know enough about pensions to make decisions about saving for retirement, so we offer sessions on this.

If you’d like to learn more about Money Works, contact financialcapability@moneyadvicescotland.org.uk or complete this form https://www.moneyadvicescotland.org.uk/forms/money-works-enquiry

Can diversity lead to better recruitment and retention?

Photo by Helena Lopes from Pexels

The challenges for growing Fintech’s in recruiting and retaining top talent in the face of larger firms with greater resources is well documented. This is particularly true in the main Scottish tech hubs of Glasgow and Edinburgh and with more large firms investing in new and expanded bases in the area this trend is likely to continue, so smaller, less well known firms with lower budgets really need to leave no stone unturned when it comes to seeking talent.

The main advantage smaller firms have is being nimble ”“ the ability to adapt hiring processes and to respond to market and candidate needs more quickly than their larger competitors. In this blog I provide some thoughts on diversity in the workplace and practical steps that can be taken.

I have attended numerous events and read countless articles on the benefits of improved diversity within workplaces. I hear the same things over and over as if employers still need to be convinced of the fact that more a more diverse workforce leads to greater creativity, innovation, staff retention and ultimately improved profitability.

It is my belief that employers do understand this. We need to move the dialogue on to the next step ”“ what should firms do about it? It’s a huge topic ranging across diversity in gender, age, disability, ethnicity, neurodiversity etc., and it can feel a bit overwhelming particularly for small to medium companies who may not have the resources that larger companies can lend to the topic.

If it seems daunting as a whole, break it down into manageable steps and prioritise these. Thinking about the stages where diversity plays a part, the biggest of these is probably recruitment as this is where the source of your diverse talent will come from. Breaking this down further how do you ensure you attract applications from the most diverse range of candidates then how do you ensure your selection process is fair to all?

Job Design

Consider what is actually essential for this hire and what can be taught once in post. What could be offered in terms of flexible working, part-time hours, agile working etc? What adjustments could be made for neuro diverse candidates?

Candidate Attraction

If your job design is done well this should automatically lead to a job advertisement which will attract a wider pool of applicants. Also check that the words used in your advertisement don’t accidentally appeal more to a particular gender, there are online tools to assist with this. Now consider how to actively target a wider pool of talent i.e. taking your roles directly to them rather than simply hoping they will find them e.g. where could the advert be placed?

Return to Work Candidates

There has been a rise in the number of returner programme in UK from 4 in 2014 to 70+ in 2019. These are for candidates who have a had a career break of one year or more and are looking to return to the workplace. Research shows that the biggest barrier for them is often loss of confidence so however appealing your job advertisement they still may not apply to you.

The Back in Business returner programme offers workshops to the candidates to help them regain that confidence and get them work ready. We will also consult with your firm to help design a “returnship” opportunity to ensure a manged return to work which more often than not will lead to a permanent hire for your business. Returner candidates tend to prove to be mature, established and loyal which is not always the case with regular hires.

Selection Process

Consider what steps you can take to anonymise applications e.g. removing name, age, gender etc., from CVs before they are passed to hiring managers. Unconscious bias training should be compulsory for all interviewers. Review any assessments being used for ”“ could they disadvantage any groups of candidates?

Back in Business is a diversity led recruitment service which offers returner programmes in Scotland and can also support with each of the other steps mentioned above.

Blog written by Morna Ronnie, Head of Programmes at Back in Business

Cryptoassets businesses and Money Laundering Regulations

From January 2020 the FCA will be the UK supervisor for cryptoasset businesses in respect of Anti-Money Laundering and Counter Terrorist Financing, under amended Money Laundering Regulations (MLRs).

Cryptoassets are developing change connected to the financial services sector.

Both the concept, and the underpinning distributed ledger technology are attracting significant attention and the UK Government established a Cryptoassets Taskforce in 2018 as part of its FinTech Sector Strategy.

The Taskforce published its final report in October 2018, providing an overview of its perspective on the subject, including the underlying technology, the associated risks, potential benefits and a way forward with respect to regulation in the UK.

In reaching conclusions the Taskforce outlined the need for action to mitigate the risks for consumer harm, prevent the use of cryptoasset for illicit activity and guard against threats to financial stability that could emerge in the future.

It’s report sets out three broad types of cryptoassets and typical uses, which together help establish a framework for considering the impact, potential risks and need for regulation.

In setting out its role the FCA has specified a range of Cryptoasset activities that are captured under the new regime and businesses conducting these activities will be required to comply with the MLRs.

The businesses include existing financial institutions that offer the option to convert cryptoassets to fiat (government issued currency), or accept cryptoassets as collateral against a loan or purchase.

The regime will also apply to new businesses and developing business models such as peer to peer providers, digital wallet providers offering a crypto service such as exchange or custodian services, Cryptoasset ATM’s, and issuers of cryptoassets.

Fintech innovators are taking advantage of the growing cryptoasset trend. Some are aiming to make crypto work seamlessly with traditional currencies by developing technology capability that will enable cryptoassets such as Bitcoin to convert to fiat money. It presents new opportunities and challenges for many and is another developing example of the potential directional change digital will bring to financial services.

All impacted businesses will be expected to comply with the MLRs in relation to cryptoasset activities by 10 January 2020. The expectations include the ability to demonstrate that each business has thought about the respective nature, scale and complexity of its activities and the associated risks. Businesses also need to have the appropriate controls in place to mitigate risks and will be expected to keep these under review and regularly assessed to ensure they remain fit for purpose and relevant.

In setting out its responsibilities and the approach it will take to this work the FCA has signposted firms to a number of existing resources to help build an understanding of its expectations when it comes to managing financial crime risks.

These include the FCA’s Financial Crime Guide: to countering financial crime risks, the Joint Money Laundering Steering Group (JMLSG) website, and recommendations from The Financial Action Task Force (FATF) an inter-governmental and global body. Further detail on the FCA’s approach can be found here.

Liberation: Banking

So, if you’ve been following the news lately you probably have heard PSD2’ and Open Banking’ mentioned at least a couple of times.

There’s a lot of fuss going on about them and we wanted to prepare all that we could find into a short article to get you up to date.

What is PSD2?

PSD2, formally referred to as the Second Payment Services Directive, is a regulation that covers the entire European Economic Zone.

PSD2 has been on the radar of European economies since 2015. It’s a major step towards keeping up with the rapid digitalization of the commerce industry.

PSD2 aims at making online payments more secure through various regulations that make online fraud much more difficult and third parties more accountable.

If you are remotely interested in finance and fintech you probably know all of these already. In case you have no idea what PSD2 is, you can check this comprehensive guide about the PSD2 regulation.

Other than regulating and securing the way online payments are done, PSD2 actually has paved the way for one of the biggest finance experiments ever.

What is Open Banking and Why Should I Care?

Open Banking is a gigantic experiment that is set to liberating the banking sector by returning the control of financial data to consumers.

This is possible thanks to a small detail that was introduced with PSD2. PSD2 allows third-party financial services to access banking data easier and more secure.

A bit of a history lesson here. Personal finance solutions aren’t something new and there are many successful companies that have provided such services. However, what they lacked was a consistent and secure way of getting access to the financial data of consumers.

The widespread method that these solutions relied on was named as screenscraping. When using third-party financial assistants, users would provide their username and passwords to the third-party software and the software would periodically login into the bank accounts and save the screen of the account information.

Based on the data they gathered, they would give suggestions to the user on how to better spend their money.

As you can guess, screen scraping wasn’t the most consistent or safe method of gathering user data. After all, who would feel safe sharing their banking credentials to someone else? On top of that, if you were using multiple banks you wouldn’t have a complete picture of your finances.

This is where PSD2 promises a safer and better ecosystem for third-party financial services to thrive.

In addition to making online payments safer, PSD2 also has provisions that aim at liberating banking data. Traditionally, your financial data (how much you spend, where you spend, what you but, etc.) was kept safe by banks. Now, to be honest, banks have historically done a great job of protecting their clients’ financial data.

The only problem here is that the data does not belong to the banks. It belongs to the consumers who normally have almost zero control over how the data is utilized.

With PSD2, banks will still be the keepers of the data. But, they are forced to share the data with verified third-party services only when requested by the user. This will be done through an Application Programming Interface (API). So, you won’t share your password with anyone and your data will be provided from a safer and more reliable channel.

Even better, you get to decide which data points will be shared. An option that was previously impossible through screen scraping.

By default, you shouldn’t care too much about Open Banking unless you’re relying on 3rd party financial service providers.

Is Open Banking Good?

On paper? Yes.

However, we still don’t know how things will play out.

The main idea of Open Banking is that it will transform the banking sector in such a way that it will become more competitive and innovative.

By giving control of the data back to the consumers and lowering the barriers to entry drastically, open banking is expected to force banks to innovate and adapt to the digital realities of our time.

The lower barriers of entry might make banking more competitive which should force banks to improve the quality of their services and also constantly innovate. At least that’s the assumption.

More actors, more transparent banking, better services, constant innovation. This is what awaits us if Open Banking will succeed.

Let’s not get ahead of ourselves for a second here.

All of these sound great but Open Banking is an enabler and not a proposition in itself. It is what companies do with Open Banking that will make it a success or not.

It’s true that competition fosters innovation but we need to ensure that innovation only happens to benefit customers and/or clients.

If customers don’t understand the value they’re getting back they won’t share their data and Open Banking will fail.

Author Name: Su Kaygun Sayran

Author Bio: Grown up in various corners of the world, Su loves writing about all things tech. His experience with various SaaS businesses has enabled him to carry his passion for writing into the tech industry.

Ethical finance extending the reach

The Scottish Government become signatory (21/22nd September) to UN Principles of Responsible Banking joining a third of the global banking system ($47 trillion worth of assets)

It is impressive that the United Nations has secured so many signatories to the Principles of Ethical Banking.

My plea is that Scotland provides a special “Scottish” addendum and extends the principle of ethical finance to include positive action for the unbanked, near prime financial and credit excluded population in Scotland

In October Global Ethical Finance Initiative acted as pacesetter bringing together UN Multi-faith global power roundtable and a conference dedicated to ethical finance with a global reach.

It is encouraging to see leadership from the Church of England and Islamic Bank collaborating to spread and scale faith centred ethical standards in banking Scotland has a long been recognised as a champion of ethical finance. Gremlin Bank (bank for the poor) founded by Mohamed Yunis, more recently Castle Bank Co-operative in Edinburgh support for low-income families and MoneyMatiX community approach to teaching children and families to manage money (and debt) are just a few examples

It is against a backdrop of a long historical tradition in democratic banking serving the poor and rich alike that the vision emerged of a Scottish Investment bank. The vision is nearing reality as the Scottish Investment Bank bill proceeds through parliamentary processes. Central to the bill is a remit to include equality impact assessment ”“ focusing on ethical investment for inclusive growth. Linking the establishment of the Bank to the Equalities Act (2010) is inspired. Ensuring the needs of people who share one or more of the protected characteristics are met is exactly what is needed to provide inclusive growth.

I would ask that we open the debate under the auspices of Fintech Scotland to extend the provision of the Scottish Investment Bank to include fintech mobile innovation as a means of extending the reach to those who are unbanked or “near prime” (not able to access credit due to minor infringement of credit ratings)

I travel with hope in my heart that Scotland will be the first country to aim for zero unbanked. Adopting SDG’s as key drivers of Scottish policy and acknowledging that wellness sits at the heart of an economically vibrant country is pretty good stuff.

As Founder/CEO of Women’s Coin (digital currency of social value) I believe that adoption of ethical financing at Corporate and SME level extending the remit to include digital innovation, tokenisation, and local currencies will accelerate the spread and scale of adoption of SDG’s (UN Strategic Development Goals).

There has never been a more critical time for ethical financing and ethical leadership across all sectors Public, Voluntary, Charitable, Corporates and SME’s

Scotland can really set the pace, the vision and has the know how to create an inclusive society that fosters wellness as the key to economic vitality

Blog written by (Prof) Christine Bamford, Founder/CEO of Women’s Coin

#MorePowertoher #fintechscotland @finance4change @modulr

womenscoin.com

voluntier.co.uk

globalethicalfinance.org

Will the growth in fintech innovation be the solution to tackling one of society’s big issues? Financial exclusion

Homeless, no address, unemployed and no bank account ”“ the future is bleak

2 Million without a bank account. Between 10-14 million “near prime” adults have no access to credit, despite minor blemishes on credit history or can only access credit at high APR 29.9-39.9%

There is an urgent need to open access to financial services for those without an identity and are homeless. or on low-pay income. It isn’t just the homeless but families managing on low incomes where one bill too many pushes them into debt crisis ”¦. into the hands of loan sharks or high APR pay day loans and a continuing spiral of debt. If wellness sits at the heart of Scottish Government policies and values ”“ then we need to recognise the impact of debt, low income, lack of access to credit and insurance as key impact measures on mental wellbeing

Fintech Scotland range of innovative solutions, mobile payment systems, education, blockchain, crypto-currencies, wallets, tokenisation of voluntary work open the opportunity to create an equal and more inclusive society. Mobile friendly approach to Identity secured through biometrics, face recognition, top up payment cards/mobile payments are now able to provide evidence of credit worthiness. This is a modern pathway to a bank account, credit worthiness, access to insurance, credit and a verifiable credit rating.

March 2018 The Mexican Congress approved Fintech Law that aimed to regulate electronic payments, crypto currencies, crowdfunding and open banking. The fintech Law promotes innovation in the financial services industry, stimulates the growth of new business models and reduces entry barriers for Fintech firms. Fintech Law can significantly improve Financial inclusion. Fintech Scotland has taken a non-regulatory approach to supporting financial technology innovation. But the impact possibilities are with us now to work with traditional financial service to provide a integrated solution to financial exclusion. Scotland is on the brink of providing a “world-class” solution to inclusive growth through financial digital solutions creating the link between wellness and economic vitality

Blog written by (Prof) Christine Bamford, Founder/CEO Women’s Coin

Acknowledgement to PWC blog and report

www.womenscoin.com #MorePowertoHer @ChrisBamford12

Crypto currency ATM’s appearing in more Scottish cities

Photo by David McBee from Pexels

Crypto currency ATM’s now in Dundee and Aberdeen

2 Scottish cities, Dundee and Aberdeen, have installed their first ever Bitcoin ATMs.

Alphavend UK, Scotland’s leading Digital Currency ATM operator, has just announced that it had installed Bitcoin ATM machines in Dundee (Nethergate) and Aberdeen (Bridge Street).

Citizens can now buy Bitcoin, without having to make long journeys to cities such as Glasgow or Edinburgh and in a way that’s easier than easier than before by simply exchanging cash for the famous cryptocoins.

Alphavend has planned to instal more machines in the UK and is growing rapidly to keep pace with the growing interest and demand which has never been higher.

The high demand can be explained by Bitcoin being chosen more and more as a cost-effective way of sending money around the world.

The challenges of scaling up and winning bigger business ”“ and how Proactis can help

Winning new business is difficult. Often it’s most difficult for new and emerging companies to challenge the established order, especially if they’re doing things in a different way. As businesses expand and develop, they begin to examine different avenues, moving away from ad-hoc smaller pieces of work to looking at more formal access routes to substantial contracts.

Here we arrive at the wonderful world of bidding, proposals and tendering (you’ll see these terms being used interchangeably, but don’t worry they all mean the same). As potential contract sizes get larger, the demands placed on prospective bidders become ever more arduous and detailed, formal submissions are required for public and private sector buyers alike.

As you might expect, larger companies have more resources to dedicate to business development and specifically to bidding for work. A recent survey of bid professionals showed just 20% worked in organisations of less than 100 employees and only 12% were the sole responsible resource in the organisation*.

Unfortunately for smaller organisations, research has repeatedly shown a direct correlation between the level of resource employed in preparing proposals and success rates. The good news for developing organisations is that there are some relatively easy steps to take to improve proposals. A recent industry study shows that nearly half of all procurement professionals believe suppliers are letting themselves down with their proposals and that they are of poor quality. With the general standard being low, smart thinking and some effort can make a big difference.

If you are at the stage where you are or soon will be submitting proposals as part of your business development strategy then we would like to support you. As a commitment to helping exciting fellow Scottish businesses within the Fintech community, we are offering a day of expert bid support to a limited number of organisations completely free of charge.

This support could be analysis of current bid strategy, support with a live bid or a review of a past proposal.

To discuss your free expert support, contact Andrew Watson, Bid Consultancy and Training Manager at Proactis Tenders Limited – Andrew.Watson@proactis.com.

Proactis Tenders Limited is one of the UK’s leading procurement companies. Its team of specialists has extensive knowledge and considerable experience in providing a range of eProcurement systems and services to buyers in the public sector. It also offers a range of services to private companies from all sectors throughout Europe who are seeking new business opportunities.

*APMP UK Compensation Report 2019

It’s worse than that”¦ Jim

Anthony Rafferty, Managing Director, Origo says recent research into integration between systems in financial adviser firms’ back-office systems reveals a worrying disconnect eating into time, resource and profits of businesses

Origo recently commissioned in-depth research into the integration between systems in the back-offices of financial advice firms, and how this affected the efficiencies and profitability of those firms.

The research was carried out independently by the lang cat, a specialist financial services consultancy based in Edinburgh, and combined hours spent in financial advice firms around the UK mapping processes and analysing how they use the systems they have in place, as well as conducting online research with another 116 financial advice firms.

The conclusion is best summed up by Mark Polson, the MD of the lang cat, who was heavily involved in the research. He says: “We knew things weren’t great before we set out to conduct this research. But even so, we were struck by the impact of these inefficiencies on adviser back offices. Even where integrations do exist, firms aren’t trusting them or using them ”“ with good reason in some cases.”

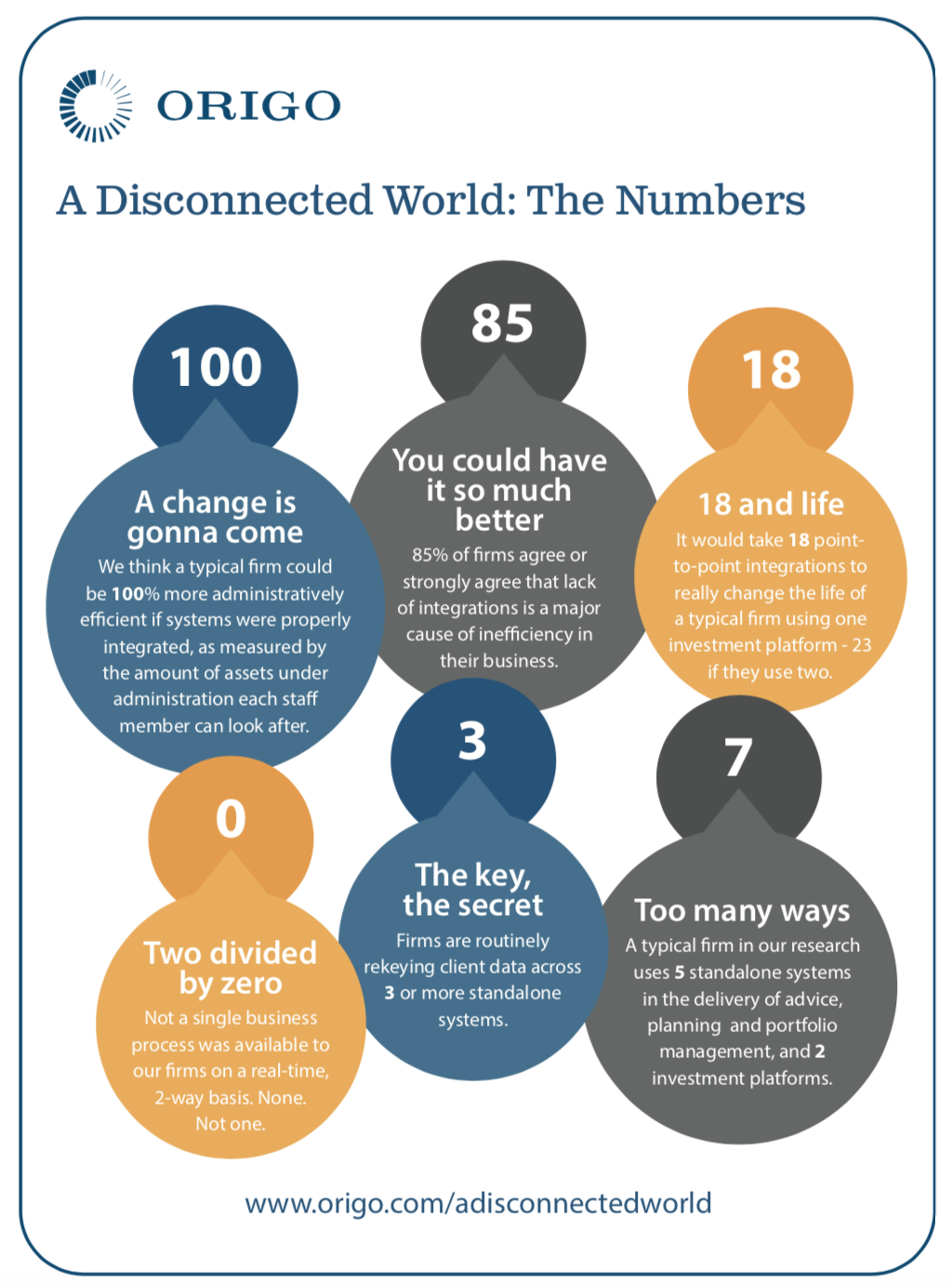

From closely studying firms’ processes, the research estimates that in a typical financial advice business, staff could be up to 100% more efficient, dealing with twice the assets under administration they currently manage, if the systems they used were properly integrated with one another. In other words, staff could potentially be dealing with up to twice the number of fee paying clients than they are at the moment.

That is both a shocking state of affairs and also one of opportunity ”“ not least for financial advice firms.

To explain what we found: Firms involved in the study on average used five standalone systems in the process of giving advice, building investment and savings portfolios and managing clients; seven when platforms (transaction and administration services) were added; 10 with the addition of more general systems like accounting and office software.

It showed that due to a lack of integration between systems, and trust in those systems, firms are having to plough time and money into otherwise unnecessary manual input and reconciliation. In a typical new business journey, for example, client details were being keyed into systems at least three times!

Key facts from the research can be found on the accompanying infographic.

Currently ”“ and to be fair, despite sterling work by some of the players in the market ”“ advice firms do not benefit from a level of integration that is of real use to them. Integrations are typically point-to-point, with one provider integrating with another for specific purposes, for example for portfolio valuations.

They are also driven by business case, with platforms, CRMs and other system providers naturally prioritising integrations that will bring in higher levels of returns.

On a practical level and worryingly, even where integrations exist, adviser firms said that the lack of consistent and quality data meant they distrusted the output the systems are delivering, the result of which was that they had reverted to inefficient, costly and potentially risk inducing manual processes, because it was a process over which they have more control.

Typically there are 23 point-to-point integrations required within a firm using two investment and savings platforms, without factoring in any systems for protection and mortgage services and general office systems. On a point-to-point basis, that level of integration is never going to happen.

But there is a solution. We identified that if there was a centralised hub, into which platforms, CRMs and adviser software systems and tools could integrate once and then connect to every other player in the market who was also connected to the hub, and which also dealt with making and maintaining the connections, the benefit to the industry could be huge ”“ in particular to the financial adviser firms.

Using a centralised hub would mean any provider new or established could connect with any other provider on the hub, for services pertinent to their operations, no matter the volume of business.

In this way, a centralised integration capability would significantly improve the market’s connectivity, helping advice firms to improve their efficiencies, their profitability and enabling them to deliver faster and better service to their clients, whilst potentially boosting business across the board.

Hence, for the past couple of years we have been building the Origo Integration Hub to help provide that solution.

From a business perspective, for systems and services providers, this hub-and-spoke approach to integration does away with the need for case-by-case decisions and resource restraints incumbent of the point-to-point integration method. Linking to a hub incurs one set of integration costs instead of many, and significantly reduces resource and IT costs, which platforms and system suppliers can better apply elsewhere in their business.

Importantly, it provides the opportunity for all software and service companies, including smaller companies and new entrants, to easily connect with new trading partners if they wish. Also, it enables adviser firms to use the software or service that best suits their business set-up.

Currently, the Integration Hub has 19 companies including some of the big names in investment and savings signed to it, with others in the pipeline.

From a top down perspective it seems illogical that in the 21st century systems do not talk to one another in an efficient manner. However, this is a legacy issue which Origo with its remit to help improve the efficiencies and cost effectiveness of the industry and deliver better outcomes for consumers, is in a position to help resolve.

Read more about Origo here