Understanding MiCA Sustainability Compliance: How Zumo’s New Feature Simplifies the Process

Zumo, the B2B digital assets infrastructure provider, has introduced a new feature that will change the way crypto-asset service providers (CASPs) in the European Union (EU) manage sustainability compliance. The new addition to Zumo’s Oxygen product helps CASPs adhere to the upcoming sustainability reporting requirements under the Markets in Crypto-Assets (MiCA) regulation.

MiCA, aims to create a consistent framework for crypto-assets across the EU. It includes a range of obligations for CASPs. One such obligation, which many CASPs appear to have overlooked, pertains to the new sustainability indicators drafted by the European Securities and Markets Authority (ESMA). These indicators measure the environmental impact of crypto-assets offered by CASPs, a requirement that must be addressed by 30 December 2024. Industry data suggests that over 80% of CASPs are unaware of this looming deadline, placing them at risk of substantial fines.

MiCA Article 66 mandates that CASPs — including exchanges, brokerages, custodians, and trading firms — operating within the EU or planning to provide services to the EU must have website disclosures detailing the environmental impact of their crypto-assets. Failure to meet this requirement could result in penalties of at least €5 million or 5% of the company’s annual turnover.

Zumo’s Innovative Solution

Zumo’s latest feature, integrated into the Oxygen product, is designed to help CASPs effortlessly meet these new sustainability reporting requirements. The solution provides access to MiCA-compliant sustainability metrics for listed crypto-assets. It leverages high-quality data from the Crypto Carbon Ratings Institute (CCRI), a strategic partner of Zumo, to build upon Zumo’s ongoing efforts to align digital asset activities with net-zero principles.

One of the key benefits of this new feature is the ability to auto-generate MiCA-compliant website disclosure reports, making it easier for CASPs across the EU to stay on top of their sustainability obligations.

Nick Jones, Founder and CEO of Zumo said “MiCA’s sustainability requirements are going live to a tight deadline, and bring with them complex data questions as well as potentially hefty fines.[…] It’s become clear that CASPs across Europe simply aren’t ready. In response, we’ve taken another important step on our sustainability journey to add the indicators that will enable service providers to comply with current and future sustainability compliance requirements. With our MiCA solution, CASPs will be able to access a single interface that helps them cut through all the complexity associated with pulling data together, formatting an appropriate template, and providing the output that ESMA is looking for.”

A Pioneer in Sustainable Digital Assets

Zumo has established itself as a leader in sustainable digital assets, with a commitment to shaping a future where financial institutions can operate within a sustainable, compliant framework. The company’s efforts have been recognised by prestigious awards such as the Fintech Finance Awards, the City AM Awards, and the Scottish Financial Technology Awards.

Beyond this, Zumo was a member of the World Economic Forum’s Crypto Sustainability Coalition, which explored how blockchain technologies can support climate action. The company also signed the Abu Dhabi Sustainable Finance Declaration and co-founded the Emerging Technologies Sustainability Taskforce (ETST).

Photo by Kervin Edward Lara: https://www.pexels.com/photo/white-wind-turbines-on-gray-sand-near-body-of-water-3976320/

IDC Marketplace: Asia/Pacific Low-Code/No-Code Development Platforms 2024 Vendor Assessment

Smardaten is officially presented in the first IDC Marketscape Asia Pacific Lowcode NoCode report 2024, which is due to be published on 12th September.

As IDC Marketscape Vendor summary stated:“Smardaten has been positioned as a major player in the 2024 AP Lowcode Nocode Development platform vendor assessment”

The report is based on extensive research and benchmarking, through exhaustive vendor survey, users interviews and client survey. In this report IDC has scored highly on Smardaten’s R&D and Innovation, customer service level, market condition, marketing strategy.

IDC has commented: “Smardaten’s platform provides intelligent data-empowered auto-modeling to reduce the software development lead time. The fourth generation of data-driven NoCode auto-models data without much human interaction, allowing for quick adjustment and rebuilding in response to front-end changes or needs.

Smardaten’s all-in-one no-code platform offers visual suites, including full-stack data management, drag-and-drop application design, and analysis without conventional coding, to greatly expedite software development while improving agility, lowering costs, and increasing quality. Smardaten technology eliminates data silos and bridges the gap between business users and IT, minimizing failure rates in digitalization projects. There are eight view types for information display and over 100 module modules for various aspects of business operations. It also has AI capabilities such as OCR and NLP operations. Smardaten’s OneBuilder enables autonomous component production and industry integration, resulting in a more adaptable business ecosystem. ”

Based on Smardaten’s advanced roadmap on GenAI functionalities enabled functionalities in the platform, we expect to see leading position on the vendor mapping from this report and in the subsequent IDC Marketscape LCNC reports.

When Finance Meets Real Life

The financial landscape is rapidly evolving, with a growing emphasis on integrating financial services seamlessly into consumers’ daily lives. A new report from Rise, created by Barclays and Rainmaking explores this evolution in their report, “When Finance Meets Real Life.” The report, released as part of The Innovation Spotlight Series looks at the convergence of finance and real-life applications, driven by technological advancements, economic pressures, and regulatory changes.

Key Drivers of Change

The report identifies several key drivers reshaping the financial sector:

- Economic Pressures: Rising inflation, the cost-of-living crisis, and increasing interest rates are making it harder for individuals and businesses to access credit. These challenges are pushing consumers to become more resourceful, while businesses are shifting focus towards sustainable growth rather than relying on abundant venture funding.

- Artificial Intelligence and Personalisation: AI is increasingly being adopted across industries, with nearly 18% of global venture funding in the first half of 2023 going to AI-related companies. AI’s potential to transform financial services is immense, particularly in areas like customer experience and regulatory compliance. Personalised financial services, powered by AI, are becoming crucial as consumers demand more tailored and context-specific offerings.

- Regulatory Catalysts: New regulations, such as the UK’s Consumer Duty and the EU’s Green Deal, are shaping the future of finance. These regulations aim to protect consumers and promote sustainability, while also driving innovation by setting higher standards for financial products and services.

- Embedded Finance: The embedded finance market, valued at $65 billion in 2022, is expected to grow significantly by 2027. This model, which integrates financial services into non-financial platforms, is revolutionising how consumers access banking services. Examples include the growth of Buy Now, Pay Later (BNPL) services and other point-of-sale financing solutions.

Thriving in a Seamless World

The report also highlights the growing consumer expectation for seamless financial experiences. The report discusses how embedded finance can help banks integrate services more naturally into everyday activities to reduce friction for users. The challenge for financial institutions is not just about offering these services but making them intuitive, timely, and relevant to each customer’s unique needs.

Personalisation and Consumer Engagement

Personalisation in financial services is still catching up compared to other industries. While consumers can personalise products like M&Ms or choose customised content on Netflix, financial services often lack this level of customisation. The report argues for a more sophisticated use of data to predict and respond to individual customer needs, creating a more engaging and relevant banking experience.

Making Money Talks Easier

The report highlights the importance of making financial discussions less intimidating and more accessible to consumers. With rising debt levels and financial stress, financial institutions need to provide empathetic support. This includes using AI and other technologies to simplify interactions and make financial advice more accessible.

Interested in getting notified of the next release?

From payments to banking to wealth management, innovation is moving along at pace, fueled by an evolving, digitally savvy customer base. The Innovation Spotlight Series explores themes and trends within the world of fintech, and how they can impact all our lives.

Photo by cottonbro studio: https://www.pexels.com/photo/person-putting-coin-in-a-piggy-bank-3943716/

The Role of AI and Cybersecurity in the Financial Sector

Artificial Intelligence (AI) and cybersecurity are revolutionizing the financial sector. As the digital landscape evolves, financial institutions are increasingly relying on AI technologies to enhance security measures, optimize operations, and deliver personalized customer experiences. The intersection of AI and cybersecurity has become crucial for safeguarding sensitive financial data and maintaining trust in the industry. This article will explore how AI is transforming cybersecurity in finance, the challenges involved, and the essential skills needed to thrive in this rapidly changing environment.

The rise of AI in finance

AI technologies, such as machine learning, natural language processing, and robotic process automation, have been instrumental in transforming the financial industry. By automating routine tasks, AI helps financial institutions to streamline operations, reduce costs, and improve efficiency. Furthermore, AI-driven insights enable financial firms to make informed decisions, assess risks, and develop targeted strategies. One of the most significant benefits of AI in finance is its ability to enhance cybersecurity measures. As cyber threats become more sophisticated, financial institutions must adopt advanced technologies to protect their systems and data. By identifying patterns, detecting anomalies, and responding to threats in real-time, AI is an invaluable cybersecurity tool.

The importance of cybersecurity in finance

Cybersecurity is a top priority for the financial sector, as cyberattacks can have devastating consequences. Data breaches can lead to financial losses, reputational damage, and regulatory penalties. Furthermore, cyberattacks can disrupt financial services – impacting customers and the broader economy. The financial industry is particularly vulnerable to cyber threats due to the vast amounts of sensitive data it handles. Personal information, financial transactions, and proprietary data are prime targets for cybercriminals. Therefore, financial institutions must implement robust cybersecurity measures to safeguard their assets and maintain customer trust.

AI enhances cybersecurity for the financial industry

AI offers several advantages for cybersecurity in the financial sector:

- Threat Detection and Prevention: AI algorithms can analyze vast amounts of data to identify patterns and detect anomalies indicative of cyber threats. By continuously learning from new data, machine learning models improve their abilities to recognize and prevent emerging threats.

- Automated Incident Response: AI-powered systems can respond to cyber incidents in real-time and minimize the impact of attacks. Automated response mechanisms enable financial institutions to quickly isolate affected systems, mitigate damage, and prevent further breaches.

- Fraud Detection: AI can analyze transaction data to identify suspicious activities and potential fraud. By recognizing patterns and anomalies, AI systems can flag fraudulent transactions for further investigation, which can help reduce financial losses.

- Risk Assessment: AI-driven risk assessment tools can evaluate the vulnerability of financial systems and identify potential weaknesses. By proactively assessing risks, financial institutions can implement targeted security measures to protect their assets.

- Behavioral Analysis: AI can monitor user behavior to detect unusual activities that may indicate a cyber threat. Behavioral analysis enhances overall security by identifying insider threats and unauthorized access attempts.

Challenges in implementing AI for cybersecurity

While AI offers significant benefits for cybersecurity, there are challenges involved in its implementation:

- Data Privacy and Ethics: The use of AI in cybersecurity raises concerns about data privacy and ethical considerations. It’s imperative that financial institutions ensure AI systems comply with regulations and protect sensitive data.

- Skill Shortages: There is a growing demand for professionals with expertise in AI and cybersecurity. Financial institutions should invest in training and development to build a workforce capable of implementing and managing AI-driven security solutions.

- Integration with Legacy Systems: Integrating AI technologies with existing legacy systems can be complex and costly. Financial institutions need to carefully plan and execute integration strategies to maximize the benefits of AI.

- Evolving Threat Landscape: Cyber threats are constantly evolving, so financial institutions have to stay ahead of new attack vectors. AI systems must be continuously updated and refined to address emerging threats effectively.

Essential skills for success in AI and cybersecurity

Professionals in the financial sector must develop a range of skills to succeed in the era of AI and cybersecurity:

- Technical Expertise: A strong understanding of AI technologies, cybersecurity principles, and data analytics is essential. Professionals must be able to design, implement, and manage AI-driven security solutions.

- Problem-Solving Skills: The ability to analyze complex problems and develop innovative solutions is crucial for addressing cybersecurity challenges. Employees must be able to think critically and adapt to changing threat landscapes.

- Regulatory Knowledge: Understanding regulatory requirements and compliance standards is essential for implementing AI and cybersecurity measures. Staff must ensure that AI systems align with industry regulations and ethical guidelines.

- Collaboration and Communication: Effective collaboration and communication skills are vital for working with cross-functional teams. Experts must be able to convey complex technical concepts to non-technical stakeholders and work collaboratively to achieve security objectives.

Conclusion

AI and cybersecurity are transforming the financial sector and presenting companies with significant opportunities and challenges. By leveraging AI technologies, financial institutions can enhance their cybersecurity measures, protect sensitive data, and maintain customer trust. However, the successful implementation of AI-driven security solutions requires a skilled workforce, strategic planning, and a commitment to continuous improvement. As the financial landscape continues to evolve, professionals with expertise in AI and cybersecurity will play a critical role in shaping the future of the industry.

About Software Mind

Software Mind is a global digital transformation partner with operations throughout Europe, the US and LATAM. For over 25 years they’ve been enriching organizations with the talent they need to boost scalability, drive dynamic growth and bring disruptive ideas to life. Top-notch engineering teams combine ownership with leading technologies, including cloud, AI, data science and embedded software to accelerate digital transformations and boost software delivery.

Photo by Christopher Burns -Kj2SaNHG-hg-unsplash

Transforming wealth management: Trends from the Banking Transformation Summit

Advances in cloud computing, data analytics, and artificial intelligence (AI) are driving significant transformation in wealth management; reshaping how firms manage and serve their clients. Such is the scale and potential of these advances; wealth management firms face an abundance of both challenges and opportunities.

This blog explores some of the most pressing challenges firms must face and how they can overcome them to leverage this technological innovation effectively. It’s a journey that promises to enhance customer experience, operational efficiency, and competitive advantage, offering a bright future for wealth management.

Balancing existing clients and new client bases

Wealth management firms face the challenge of catering to existing clients who prefer a more traditional approach and a new breed of younger, digitally savvy clients.

Whereas more established clients value a human-facing service, younger generations expect and indeed favour seamless digital interactions. To effectively engage this younger demographic, firms must be able to complement professional validation with diverse communication channels beyond email.

Firms must remove barriers to attract and retain these clients by creating accessible, digital-first experiences, offering incentives, and increasing marketing budgets to encourage interest.

Personalisation and mass customisation

Rather than simply a feature, personalisation is the essence of effective wealth management. Whether delivered on a per-client basis or by using a more segmented approach, it fulfils the essential role of making each client feel uniquely important.

Next-generation AI enables this mass customisation, allowing firms to provide tailored advice at scale and reinforcing the value of each client’s individuality. For example, wealth managers can offer timely, relevant advice to enhance client engagement and satisfaction by leveraging data from various life events and triggers. However, handling customer data sensitively and tailoring services explicitly for client benefit is critical to the success of this approach.

New digital products and AI integration

Investment platforms and open banking tools, like Moneyhub and Moneyinfo, simplify financial management by allowing clients to aggregate data in one place. Meanwhile, AI provides opportunities to enhance these platforms by automating manual tasks, such as capturing meeting notes and client conversations and ensuring regulatory compliance.

AI’s role in wealth management goes beyond improving efficiency and accuracy – it also plays a crucial role in protecting clients. For example, AI can flag if a client appears to misunderstand a piece of advice that would not be picked up from word transcripts alone, ensuring that clients are well-informed and protected.

Speed, accessibility, and presentation

Today’s clients expect quick, online access to their financial information, slick data presentation, and the option to speak to a professional when needed. Speed and accessibility across hybrid channels are paramount.

Wealth managers must invest in intuitive, visually appealing interfaces that make complex information easy to understand. Customer expectations on the ability to interact with services seamlessly are now generalised across financial services, set by advances such as Open Banking. They require robust authentication and providing immediate access to professional advice when necessary.

Regulatory demands and data quality

An increasingly demanding regulatory ecosystem requires wealth managers to enhance their data completeness, quality, and accuracy. The FCA’s 2023 Dear CEO’ letter stressed the importance of tackling financial crime and putting customer needs first by meeting high standards underpinned with strong data governance.

If wealth management firms are to meet these standards and lay the foundation for compliant product innovation, investment in technology is needed. For example, AI systems can assist in identifying regulatory triggers, such as testing customer understanding and vulnerabilities to ensure compliance. Nonetheless, firms must remember their duty to the customer and ensure AI ethical policies are established from the outset.

Customer journey and operational efficiency

Building customer journey-based services while delivering operational efficiencies to provide a holistic client experience involves a coordinated approach across financial services and insurance. This approach is crucial for ensuring client retention and satisfaction. Data analytics can then optimise internal services, such as risk and compliance, further reducing costs and improving service delivery.

Firms need to start with a well-defined customer journey and build out services across all relevant areas. Taking this approach helps remove barriers to entry for the younger demographic, to prepare for the ‘great wealth transfer’ where trillions are anticipated to be handed down to future generations in the coming years.

In Summary

Integrating cloud, data, and AI is revolutionising the wealth management industry. Firms embracing these technologies can enhance personalisation, improve operational efficiency, meet regulatory demands, and engage and protect a new generation of clients. Those who delay moves towards modernisation risk losing out to the competition.

Article written by Orla Parry, Head of Private Sector Business Development at BJSS

BJSS is a leading partner to the financial services industry. Over the past 30 years, we’ve helped multiple wealth and asset managers to innovate at scale.

Talk to us about your transformation goals and find out how we can help you leverage cutting-edge technology and stay ahead in a wealth management industry undergoing unprecedented evolution.

This is not a sponsored article and no commercial agreement exists between BJSS and FinTech Scotland.

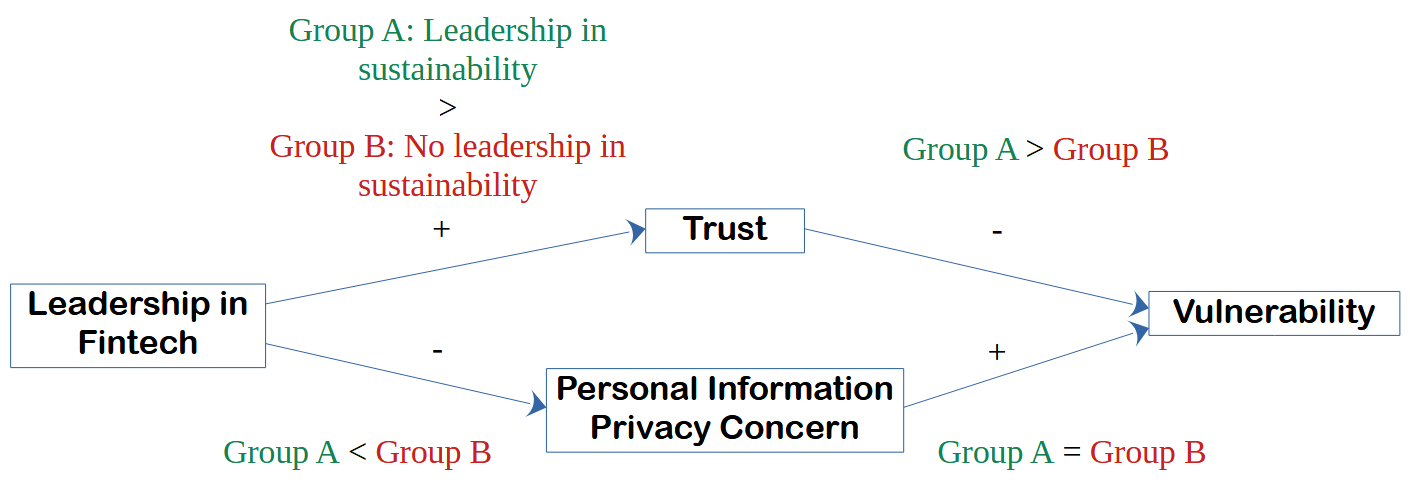

Leadership in Fintech builds trust and reduces vulnerability

Article written by Dr Alex Zarifis

Fintech and sustainability

Financial technology often referred to as Fintech, and sustainability are two of the biggest influences transforming many organisations. However, not all organisations move forward on both with the same enthusiasm. It is, therefore, important to find the synergies between Fintech and sustainability. For this reason I carried out research on how leadership in Fintech builds trust and reduces vulnerability when combined with leadership in sustainability (Zarifis, 2024).

Leadership in Fintech and sustainability

One important aspect of this transformation many organisations are going through is the consumersʹ perspective. It is important to clarify whether leadership in Fintech, with leadership in sustainability, is more beneficial than leadership in Fintech on its own.

This research evaluates consumers”™ trust, privacy concerns, and vulnerability in the two scenarios separately and then compares them. Firstly, this research seeks to validate whether leadership in Fintech influences trust in Fintech, concerns about the privacy of personal information when using Fintech, and the feeling of vulnerability when using Fintech. It then compares trust, privacy concerns and vulnerability in two scenarios, one with leadership in both Fintech and sustainability, and one with leadership just in Fintech without sustainability.

The benefits of combining leadership in both Fintech and sustainability

The findings show that, as expected, leadership in both Fintech and sustainability builds trust more, which in turn reduces vulnerability more. Privacy concerns are lower when sustainability leadership and Fintech leadership come together; however, their combined impact was not found to be statistically significant. So contrary to what was expected, privacy concerns are not reduced more effectively when there is leadership in both together.

Figure 1: Model of leadership in Fintech, trust, privacy and vulnerability, with and without sustainability

Fintechs can use these findings to make consumers feel less vulnerable

An important practical implication is that this research finds that even when there is sufficient trust to adopt and use Fintech, the consumer often still feels a sense of vulnerability. This means leaders in Fintech must not just do enough for the consumer to adopt their service, but they should build trust and reduce privacy concerns enough for consumers to feel less vulnerable. These findings can inform a Fintech”™s business model and the services it offers.

Reference

Zarifis A. (2024) Leadership in Fintech builds trust and reduces vulnerability more when combined with leadership in sustainability”™, Sustainability, 16, 5757, pp.1-13. https://doi.org/10.3390/su16135757

Biography

Dr Alex Zarifis research and teaching are on the practical applications of technology in business. Before the University of Southampton, he worked at several academic institutions including the University of Cambridge and the University of Manchester. He is currently a research affiliate of the Cambridge Center for Alternative Finance (CCAF).

His research interests include trust, electronic business, artificial intelligence, blockchain, Fintech and Insurtech. He has over forty publications and his work has featured in journals such as Computers in Human Behaviour and Internet Research. He has explored cryptoassets such as cryptocurrencies since 2012. As part of this research, he published the first peer reviewed research on trust in digital currencies in the world in 2014.

Regulatory Risk Trends in June 2024: A Comprehensive Overview

As we move through 2024, the landscape of regulatory risk continues to evolve, presenting both challenges and opportunities for businesses worldwide. The latest report from Pinsent Masons, “Regulatory Risk Trends – June 2024,” provides an in-depth analysis of current and emerging risks. This blog post summarises key insights from the report, highlighting the major trends and their implications for businesses.

Key Regulatory Risk Trends

Operational Resilience

The Bank of England’s focus on operational resilience remains a cornerstone of regulatory scrutiny. Firms are required to demonstrate their ability to withstand and recover from significant operational disruptions. The Financial Policy Committee’s macroprudential approach underscores the need for robust operational risk management frameworks.

Consumer Duty

The Financial Conduct Authority (FCA) has intensified its efforts to enforce the Consumer Duty, which mandates that firms must act to deliver good outcomes for retail customers. This involves ensuring fair treatment of customers, providing clear and transparent information, and fostering an environment where customers can pursue their financial objectives effectively.

Financial Promotions and Influencers

The FCA has been particularly vigilant regarding financial promotions, with a crackdown on misleading advertisements and unauthorised financial advice from social media influencers. Recent enforcement actions highlight the need for firms to ensure their promotional materials comply with regulatory standards and do not mislead consumers.

Money Laundering Regulations

HM Treasury’s consultation on improving the effectiveness of money laundering regulations signals ongoing governmental focus on combating financial crime. The consultation aims to enhance regulatory frameworks to prevent money laundering and terrorist financing, ensuring that the UK’s financial system remains robust and secure.

Vulnerable Customers

The FCA has issued finalised guidance on the fair treatment of vulnerable customers, emphasising the need for firms to take into account the diverse needs of their customer base. This guidance outlines practical steps for firms to ensure that vulnerable customers are not disadvantaged and can access the financial services they need.

Politically Exposed Persons (PEPs)

The FCA’s review of the treatment of PEPs aims to strike a balance between preventing financial crime and ensuring that PEPs are not unfairly discriminated against. This ongoing review seeks to refine the regulatory approach to PEPs, ensuring compliance while mitigating undue burdens on these individuals.

Cybersecurity and Data Protection

With the increasing reliance on digital technologies, cybersecurity and data protection have become paramount. Regulatory bodies are pushing for enhanced measures to protect sensitive data and prevent cyberattacks, requiring firms to implement rigorous cybersecurity protocols and regular assessments.

Implications for Businesses

Businesses must stay ahead of these regulatory changes to mitigate risks and ensure compliance. Here are some practical steps firms can take:

ӢEnhance Operational Resilience: Develop and regularly test robust business continuity plans to handle potential disruptions.

ӢPrioritise Consumer Duty: Foster a customer-centric culture and ensure that all customer interactions are fair, transparent, and beneficial.

ӢMonitor Financial Promotions: Implement stringent compliance checks for all promotional materials and be cautious when using social media influencers.

ӢStrengthen Anti-Money Laundering Measures: Stay updated on regulatory changes and enhance internal controls to prevent financial crimes.

ӢSupport Vulnerable Customers: Train staff to identify and support vulnerable customers, ensuring they receive appropriate services and advice.

ӢReview PEP Policies: Balance compliance requirements with fair treatment of PEPs, avoiding unnecessary restrictions while maintaining security.

ӢInvest in Cybersecurity: Regularly update cybersecurity measures and conduct vulnerability assessments to protect against data breaches.

The regulatory landscape is becoming increasingly complex, and businesses must remain vigilant to navigate these changes successfully. By understanding and addressing these regulatory risk trends, firms can build trust and resilience in their operations. The insights from Pinsent Masons’ June 2024 report provide a valuable roadmap for navigating this dynamic environment.

For more detailed information, you can access the full report here.

The MoneyMatix 2024 Financial Inclusion Manifesto

Financial stability often determines one”™s quality of life, ensuring that everyone has access to fair and inclusive financial services. The MoneyMatix 2024 Financial Inclusion Manifesto, authored by Tynah Matembe, addresses the pressing need to break down barriers and build a financial system that works for everyone.

Vision for Inclusive Finance

The manifesto lays out a comprehensive vision for financial inclusion that goes beyond traditional banking services. It emphasises the importance of creating a financial ecosystem where everyone, regardless of their background, has access to the resources they need to succeed. This includes affordable credit, savings programs, and investment opportunities tailored to underserved communities.

Tackling Systemic Barriers

One of the core focuses of the manifesto is identifying and addressing the systemic barriers that prevent marginalised groups from accessing financial services. It calls for collaborative efforts between financial institutions, policymakers, and community organisations to create inclusive financial products and services that meet the diverse needs of the population.

Financial Literacy and Empowerment

Empowering individuals with the knowledge and tools to make informed financial decisions is a cornerstone of the MoneyMatix manifesto. It proposes targeted financial education initiatives designed to enhance financial literacy among all demographics, ensuring that everyone can navigate the financial system confidently.

Innovative Solutions for the Future

The manifesto also highlights the need for innovation in financial services. It encourages the development of new technologies and products that can bridge the gap between traditional banking and the needs of modern consumers. This includes leveraging fintech solutions to provide more accessible and efficient services.

Call to Action

The MoneyMatix 2024 Financial Inclusion Manifesto is not just a document but a call to action. It urges all stakeholders, from individuals to large financial institutions, to take proactive steps in creating a more inclusive financial landscape. By working together, we can ensure that financial services are fair, accessible, and beneficial for all.

Read the Full Manifesto

To truly understand the depth and scope of the initiatives proposed, read the full MoneyMatix 2024 Financial Inclusion Manifesto. This document is a blueprint for change, offering practical solutions and a visionary approach to making financial inclusion a reality.

Banking on Everyone

In an era where digital technologies shape our daily lives, financial inclusion remains a pressing issue worldwide. Many individuals and communities still face barriers to accessing basic financial services. However, amidst these challenges, Financial Technology (Fintech) is emerging as a transformative force, bridging the inclusion gap and bringing banking services to everyone, regardless of their background or location.

The Rise of Fintech

Fintech refers to the innovative use of technology to deliver financial services. In recent years, Fintech has gained momentum globally, disrupting traditional banking models and democratising access to finance. Scotland, with its vibrant tech ecosystem, has been at the forefront of this revolution. From mobile banking apps to peer-to-peer lending platforms, Fintech startups are reshaping the financial landscape, making it more inclusive and accessible to all.

Empowering the Unbanked

One of the most significant contributions of Fintech is its ability to reach the unbanked and underbanked populations. In Scotland, as in many parts of the world, there are individuals who have limited or no access to traditional banking services due to factors such as geographic remoteness, unemployment, disability or lack of documentation. Fintech companies are addressing this challenge by offering digital banking solutions that can be accessed through smartphones, eliminating the need for physical bank branches and paperwork.

Innovative Solutions for Financial Access

Fintech innovation goes beyond traditional banking services, offering a wide range of solutions to enhance financial access and inclusion. For example, microfinance platforms leverage technology to provide small loans to entrepreneurs and individuals who lack collateral or credit history. Similarly, blockchain-based payment systems enable cross-border remittances at lower costs, benefiting immigrant communities and their families back home. These innovations are not only expanding financial access but also promoting economic empowerment and social inclusion.

Challenges and Opportunities

While Fintech holds immense potential for promoting financial inclusion, it also faces challenges such as digital literacy, cybersecurity, and regulatory compliance. Moreover, there is a risk of widening the digital divide if segments of the population are not included in the transition to digital finance. To drive financial inclusion collaboration between Fintech firms, government agencies, and civil society is essential. By working together, stakeholders can develop policies and programs that promote inclusive Fintech solutions and ensure that no one is left behind in the digital economy.

In Scotland and beyond, Fintechs play a pivotal role in bridging the inclusion gap and creating a more equitable financial system. By leveraging technology and innovation, Fintech firms work towards empowering individuals and communities to access essential banking services, build assets, and improve their livelihoods. The unbanked are the people who hold the key, organisations willing to go the extra mile to attract, employ and work in partnership with individuals to understand their challenges and fears will be the organisations that cross that finish line first. Occasional focus groups and questionnaires are not enough, building strong robust and trusting communities is the only way to solve challenges.

As we continue to embrace the digital age, can we harness the power of Fintech to build a more inclusive and prosperous future for all? No one can be left behind.

About the Author

Laura Bosworth has worked in the recruitment and employer branding industry for many years. Based in Scotland and working with clients across a range of sectors and industries in the UK and the US.

A diversity, equity and inclusion leader she aims to unlock economic opportunity for all

because everyone deserves a fair chance. Over the course of her career, she has had the privilege of building and executing hiring strategies and programmes that help level the playing field and create employment pathways into Technology, Professional Services and Financial Services.

Laura consults with senior executives at FTSE 250 and Fortune 500 companies on developing diverse recruiting strategies backed with insights, including empowering and connecting emerging and established minority leaders across the globe. Motivated by the ability to have a social impact at scale, building empowered teams and influencing leaders to make more inclusive and intentional decisions.

Photo by Andrew Neel: https://www.pexels.com/photo/apple-iphone-desk-laptop-6633921/

Revolutionising Financial Futures: UK Fintech Challenge Pioneers Data-Driven Solutions for Later Life Planning

FinTech Scotland and Smart Data Foundry are collaborating to bring an industry-wide UK fintech innovation challenge to the market. This challenge seeks to inspire the development of inclusive financial services for consumers, empowering them on their journey towards a secure financial future.

Building on the success of the previous SME business banking programme in 2023, the 2024 emphasis will be on new innovative solutions that can support people’s financial journeys as they plan for their later years.

UK fintechs can now apply to take part in the challenge, and up to six successful applicants will be awarded a £5K participation fund to allocate resource to developing their idea. In addition to funding, the challenge offers a fantastic opportunity for participants to present to some of the largest financial institutions in the UK, including NatWest Group, PwC, and Royal London, as well as engage with experts in data, technology, and fintech. This exposure will allow innovators to gain valuable insights, receive expert guidance, and enter potential collaborations, maximising the chances of success for their projects.

Another key feature of the challenge is Smart Data Foundry’s provision of synthetic data replicating both consumer banking and investment and savings products*. This will enable fintechs to thoroughly test and refine their innovations, ensuring the development of robust and effective solutions that address consumers’ real needs.

As life expectancy in the UK and around the world continues to increase, the number of people living later in life is growing rapidly. It is expected that average life expectancy in the UK will be 85.9 years by 2050 – in 1950 it was 68.6 years.1 This demographic shift has a significant impact on the current and future cost of living, as there is an increased need to be financially secure for longer. Fintech solutions need to consider future products and services that will help prepare people financially for a longer life.

Through support from the Strength in Places UK Research and Innovation Grant, a prize fund of £45K will be offered to promising projects arising from the challenge. This will allow entrepreneurs and innovators to further develop and implement their ideas, which will help unlock later-life planning for consumers.

Those interested in taking part have until 17 May to submit their application.

Samantha Brand, Innovations & Partnerships at NatWest Group, said:

“We are thrilled to partner with FinTech Scotland and Smart Data Foundry on the innovation call for Supporting Later Financial Lives. This growing customer segment spans life stages with varying product requirements, and we believe there are specific needs to be solved in this space. We look forward to working with innovators to understand how we can create the best solution for our customers. The challenge aligns firmly with NatWest’s purpose to champion potential, helping people, families and businesses to thrive.”

Sarah Collins, Director PwC United Kingdom, commented:

“We are thrilled to support this innovation challenge, which represents an exciting opportunity to harness the power of open finance data. The power of fintech can help consumers gain greater control over their financial futures, ultimately enabling them to make smarter decisions as they plan for later life. We are delighted to be working with FinTech Scotland and Smart Data Foundry to accelerate data driven innovation.”

Bryn Coulthard, Chief Product and Technology Officer at Smart Data Foundry, said:

“Our continued partnership with FinTech Scotland in this innovation challenge underscores our commitment to empowering consumers with innovative, data-driven solutions. By leveraging the power of data, technology, and fintech expertise, we hope this challenge will help to revolutionise financial services, ensuring individuals can embark on their later years with confidence and security. Through initiatives like this, we’re envisioning the future and actively shaping it.”

Nicola Anderson, CEO of FinTech Scotland, said:

“Together with Smart Data Foundry, we are excited to launch this new innovation challenge focusing on later financial lives. As we explore innovation in this domain we hope it will also generate fresh insights into the potential for Open Finance data. This is a great opportunity to explore that potential, with a focus on delivering smarter, and future-focused customer solutions. We are excited to see how these new ideas will help evolve the digital financial landscape with a focus on accessibility and using data to capture the needs of our rapidly evolving society.”

Those interested in taking part can find out more here: FinTech Scotland | Innovation Challenge to support consumers in their later financial lives.