Safello and Zumo Partner to Elevate Crypto Sustainability Compliance in Sweden’s Crypto Sector

Swedish cryptocurrency exchange Safello has partnered with Zumo, a leading digital assets platform specialising in carbon calculation and sustainability reporting. This strategic alliance is designed to help Safello meet the rigorous sustainability disclosure requirements set by the EU’s Markets in Crypto-Assets Regulation (MiCAR).

As MiCAR’s Article 66 comes into effect, crypto asset service providers (CASPs) operating within the EU must publicly disclose the environmental impacts of the digital assets they offer. With this collaboration, Safello proactively addresses this requirement, positioning itself as an early adopter of sustainability best practices in the cryptocurrency industry.

Zumo’s expertise will provide Safello with precise, transparent data on carbon emissions associated with crypto activities. This partnership allows Safello to meet regulatory standards and to strengthen trust among its stakeholders by demonstrating an active commitment to sustainability.

Tara Abid, Chief Compliance Officer at Safello, commented,

“Compliance is central to our business strategy. Our partnership with Zumo ensures we can deliver accurate sustainability data to our customers, maintaining our leadership position in regulatory alignment and transparency.”

Nick Jones, Founder and CEO of Zumo, said,

“Safello’s choice to partner with us highlights the increasing importance of sustainability reporting in crypto. Our Oxygen product suite enables businesses like Safello to align digital asset operations with net-zero targets and comply effectively with evolving EU regulations.”

With Sweden’s Financial Supervisory Authority mandating compliance with MiCAR by 30 September 2025, Safello’s proactive partnership with Zumo represents a forward-thinking step toward sustainability integration within the crypto sector.

For further details or to explore collaboration opportunities, contact Zumo

Snugg Introduces ‘Carbon Cashback’ for Energy-Savvy Homeowners

Businesses across the UK now have an exciting new opportunity to support their customers in becoming more energy efficient, thanks to Edinburgh-based fintech Snugg. The Carbon Cashback platform, launching initially in beta, enables businesses to offer homeowners annual cash rewards for achieving verified carbon reductions through home energy improvements.

This approach uses smart meter data to track home carbon savings such as those from installing insulation, heat pumps, or solar panels. Snugg then transform those savings into carbon credits for sale in the Voluntary Carbon Market. It’s a powerful incentive for homeowners, tackling one of the most significant barriers they face: the upfront cost of sustainability upgrades.

For businesses, the benefits are equally compelling. Partnering with Snugg offers companies a distinctive proposition to attract and retain customers, reinforcing brand commitment to sustainability. Additionally, participating companies gain valuable insights into customer energy consumption and carbon footprint reductions, crucial data for businesses aiming to lower their Scope 3 emissions and meet net-zero goals.

George Wilson, Carbon Markets Lead at Snugg, explains:

“The Carbon Cashback platform directly addresses the financial barriers homeowners encounter. For businesses, it’s a unique way to differentiate their offerings while actively engaging customers in sustainability initiatives. It also provides access to valuable emissions data, empowering companies to advance their net-zero strategies more effectively.”

The platform’s development was supported by the UK Government’s DESNZ ‘Green Home Finance Accelerator’ programme and has already demonstrated significant interest, with over 90% of testing participants keen to engage. Snugg is actively seeking early adopter businesses to join the beta phase, ahead of the wider market launch planned for later in 2025.

Businesses can play a very important role in accelerating the UK’s residential decarbonisation efforts (a market estimated at £250 billion). Importantly, this isn’t a greenwashing exercise. Rather, it positions businesses as genuine leaders in sustainability, supporting real, measurable carbon reductions.

If you are Interested in becoming a partner or learning more about Carbon Cashback, visit snugg.com/carbon-cashback.

Consumers as Innovators and the UK Financial Conduct Authority’s Consumer Duty

We address the scope, purpose, and initial implementation from July 2023 of the UK Financial Conduct Authority’s (FCA) Consumer Duty. As an instance of financial regulation innovation, the Consumer Duty is having a major impact in the financial services sector and has impacted on the organisation of markets for financial services and in the interactions of consumers and providers.

The Duty brings to prominence the ways in which the production, marketing and use of financial services products and services are strongly interrelated. It highlights: (1) Consumers’ financial literacy; (2) Providers’ confidence that their products and services and communications about these are being understood; and (3) How providers are anticipating and coping with vulnerability among their customers.

Together, these recognise consumers as being active, engaged, adaptive and innovative. We position the paper in terms of active consumption and market and marketing channels so as to focus on active consumers, and consumer vulnerability. To illustrate how the Consumer Duty is shaping the development, marketing and uses of financial services, we explore a sample of cases reported by the Financial Ombudsman Service, in which the issues referenced are akin to the elements addressed in the Consumer Duty.

We find that consumer understanding is a prominent factor, which also impacts on a number of other categories and subcategories. We also see, through the perspective of Consumer Duty, a somewhat pacified or pacifying view of consumers and in some instances, tensions emerging between consumer adaptations and the contractual terms for financial products and services. This adds to our conceptual framing of market channel and its implications for consumer vulnerability.

Why Community Financial Institutions Need an AI Operating System

The financial services landscape is at an inflection point. Recent industry data shows AI adoption by UK financial institutions doubled from 32% to 63% between 2023 and 2024, with over 80% of banking executives now viewing AI as a business opportunity. Yet this transformation is uneven – while large banks invest heavily in AI, community financial institutions often lack the infrastructure to compete.

Working with over 300 credit union staff across Scotland, we’ve observed a critical reality: small teams are spending much of their time manually maintaining, distributing, and correcting data – constraining their bandwidth for value-added activities. This isn’t just an efficiency problem; it’s preventing vital community institutions from achieving the economies of scale needed to compete with larger banks.

The U.S. market provides compelling evidence for how AI can level this playing field. Nearly 30% of U.S. community banks and credit unions plan to implement generative AI tools in 2025, with early adopters already seeing significant gains in operational efficiency and member service. Through innovators like Eltropy, even the smallest credit unions are using AI to handle routine queries, process documents, and personalise communications.

At Niovant, we’re bringing this transformation to the UK market. Our thesis is simple: semi-autonomous AI agents will fundamentally elevate productivity by eliminating routine work at scale, giving organisations back time for higher-value tasks. Our platform ingests raw data from core systems, structures it for AI agents, then triggers the actions and workflows that previously consumed staff time.

The Building Societies Association noted in 2024 that mutual lenders are actively exploring how AI can boost staff productivity and customer satisfaction “at scale – but reduce cost” in line with their values. We’re making this possible by building an operating system that helps financial institutions orchestrate AI automations while adapting to shifting goals, regulations, and member needs.

The future of financial services won’t be built on static software, but on adaptive AI systems that give organisations back their most precious resource: time. We’re building that future, starting with the institutions that need it most.

Please reach out to me at lewis@niovant.com to discuss collaboration.

I went to a Digital Banking conference and an AI event broke out!

The theme for June’s American Banker’s Digital Banking Summit was “Welcome to the Bank of the Future” – and in this case the “future” is artificial intelligence. Specifically, Generative AI (Gen AI) and how it can enhance aspects of various banking operations. One CIO keynote declared “The strategic risk of not using Gen AI is higher than the operational risks of using it”.

While Gen AI itself does not directly create new banking business opportunities, it does have potential to accelerate improvements to customer experience, product development and operating practices that support keeping and attracting depositors. In short, Gen AI is potentially a much quicker means of adapting to disruptive challenges and to improving operational productivity.

Speakers highlighted use-cases of Gen AI deployed or in development within banking. For example:

- Customer Care/Support

- Help customer care reps resolve customer issues more accurately and quickly. Using real-time speech-to text combined with Gen AI models, relevant guidelines and documentation can be automatically retrieved and displayed on customer care rep screens.

- Fraud Claim Routing

- Poor execution in handling fraud claims motivates depositors to switch banks. Time is critical to contain costs and allay customer fear. Gen AI models can assess fraud types based on customer answers about the problem, then accurately route the case to departments with relevant fraud detection and resolution expertise.

- Near Real Time Product Matching

- Gen AI enabled near-real-time customer insights can promote bank product offers more likely to relate to stated customer needs. value and customer share of wallet.

- Faster, higher quality Underwriting

- Using Gen AI to overlay specific customer needs and preferences within the decisions process could improve responsiveness without taking on more risk, thus winning more worthy loans from competitors.

Blockers to Gen AI adoption in banking:

- Gen AI Skill gaps. Huge money center banks have sizable technology teams. Smaller banks don’t.

- Data quality and accuracy for LLM development. The axiom Garbage In, Garbage Out holds true, and banks are particularly sensitive to erroneous results from AI models.

- In the fraud use case, concerns are that false flags could erode customer loyalty. While customers value alerts pertaining to potential fraud, they do not want overly sensitive AI models freezing them out of their bank accounts.

- Avoiding bias within the LLMs that could result in a negative customer experience for some customers and expose banks to other liabilities.

Aside from AI, the conference underscored common pain points facing traditional bankers in the highly competitive, dynamic US market:

- Customer attraction, retention and deposit growth – With over 10,000 banks and credit unions, customers have so many to choose from; how can banks differentiate and drive loyalty?

- Fraud – Cost of fraud is increasing 25% per year, with half of all banks reporting zero to moderate confidence that they can keep pace with current and emerging threats – all which impact customer satisfaction.

- Managing transformation to enhance value, retention, and attracting younger depositors – The balancing act of building new user experience and functionality to retain/attract customers while maintaining decades old backend systems.

SDI works with Scottish fintechs and technology companies to support their international growth ambitions. If you are considering growth in the US market we would love to have a conversation.

Bob Fogarty, VP Business & Trade Development, SDI

Please contact:

- Bob Fogarty, Boston (robert.fogary@scotent.co.uk)

- John Fritz, Silicon Valley (john.fritz@scotent.co.uk)

- Anne Hilarion, Scotland (anne.hilarion@scotent.co.uk

Navigating Double Materiality in ESG: Practical Steps for Businesses

Introduction to Double Materiality

Double materiality emerged as a concept relatively recently, but has been gaining interest as a practical, actionable conceptualization of ESG outputs. Materiality itself traditionally focused on how a factor impacted firm financial performance, a decidedly unidirectional approach. Double materiality looks to identify both the financial materiality of an issue as well as the impact materiality, which assess the material impact upon society and the environment. Rising stakeholder demands and regulatory pressures are making double materiality more and more prevalent in today’s business climate. To practically navigate double materiality, companies must adopt comprehensive strategies that integrate both financial and societal/environmental dimensions into their decision-making processes.

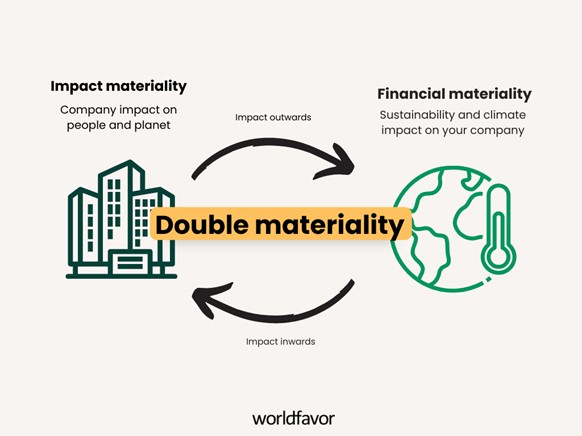

The EU Commission’s Supplementary Directive 2013/34/EU states, “…double materiality as the basis for sustainability disclosures”. The two dimensions of double materiality, impact and financial, are further noted as being ‘…inter-related and the interdependencies between these two dimensions shall be considered” (section 3.3). This is best visualized in the following graphic:

Image credits: Worldfavor, July 2023

As shown, the assessment impact or financial materiality are interconnected and mutually reinforcing. The impacts are, from a company perspective, split between impact inwards and impact outwards, meaning the materiality of an issue as it impacts the company itself (impact inwards) and the material impact of a company’s actions on society and the environment (impact outwards). In today’s reporting climate, those two directions are seen as more closely related than ever before.

In industries such as Aerospace, the concept of materiality is closely linked to innovation. Companies like SpaceX, Orbex, or Collins Aerospace have defined themselves as organisations with a sustainability element. This is a clear demonstration of the circular nature of double materiality, in that the impact materiality (the firm’s sustainability efforts) are directly impacting the financial materiality (inwards impact in the form of sales and customers, outwards impact in the form of environmental innovation and positive social investment) and vice versa. For instance, when discussing potential environmental impacts of manufacturing for aerospace and defense technologies, S&P Global argued that the climate transition would be significantly material for stakeholders as manufacturing and transportation emissions require long-term strategic planning but is less likely to impact near-term credit (S&P Global, 2022).

In defining impacts, it is important to note that risk and opportunities are both components of impact, but that they are not necessarily the entirety of the impact. For instance, an environmental impact may become financially material due to changing weather patterns. Conversely, a financial issue may develop impact materiality through a change in regulations or soft law pressures.

Practical Steps for Businesses

To effectively navigate double materiality, businesses need to implement a series of practical steps, encompassing governance, stakeholder engagement, data collection, and reporting.

1. Establish Strong Governance Frameworks

Leadership and Oversight: Establish a governance framework that includes oversight by the board of directors or a dedicated ESG committee. This structure should ensure that double materiality is integrated into the company’s strategic objectives.

Roles and Responsibilities: Clearly define roles and responsibilities for ESG initiatives across various departments, with a defined company-wide strategy to ensure efficiency of data collection and reporting. Assign senior executives to oversee both financial and impact materiality aspects, ensuring alignment with the company’s overall strategy.

2. Engage Stakeholders

Identifying Stakeholders: Identify and actively engage with key stakeholders, including investors, employees, customers, suppliers, regulators, and local communities. Understanding their concerns and expectations is vital for addressing both financial and impact materiality.

Dialogue and Collaboration: Engage in open and continuous dialogue with stakeholders through surveys, meetings, and advisory panels. Collaboration with stakeholders helps in identifying material ESG issues that are relevant from both financial and impact perspectives.

3. Conduct Materiality Assessments

Materiality Matrix: Develop a materiality matrix that plots ESG issues based on their importance to stakeholders (impact materiality) and their potential financial impact on the company (financial materiality). This visual tool helps prioritize ESG issues that require attention.

Dynamic Assessments: Conduct regular materiality assessments to adapt to evolving ESG landscapes and stakeholder expectations. This ensures that the company remains responsive to new challenges and opportunities.

4. Integrate ESG into Risk Management

Risk Identification: Identify ESG-related risks that could affect the company’s financial performance and societal impact. This includes environmental risks (e.g., climate change), social risks (e.g., labor practices), and governance risks (e.g., corruption).

Risk Mitigation: Develop and implement strategies to mitigate identified risks. This might involve adopting sustainable practices, improving supply chain transparency, or enhancing corporate governance standards.

5. Develop Robust Data Collection and Reporting Mechanisms

Data Collection Systems: Implement robust data collection systems to gather accurate and reliable ESG data. Use technology solutions like IoT, blockchain, and AI to enhance data accuracy and transparency.

Reporting Standards: Align reporting with established frameworks such as the Global Reporting Initiative (GRI), Sustainability Accounting Standards Board (SASB), and Task Force on Climate-related Financial Disclosures (TCFD). These frameworks provide guidelines for comprehensive and comparable ESG reporting.

Integrated Reporting: Consider adopting integrated reporting, which combines financial and ESG information into a single report. This approach provides a holistic view of the company’s performance and its impacts, enhancing transparency and accountability.

6. Foster a Culture of Sustainability

Employee Engagement: Educate and engage employees at all levels about the importance of double materiality and sustainable practices. Encourage employees to contribute ideas and initiatives that promote sustainability.

Incentives and Recognition: Establish incentive programs to reward employees for their contributions to ESG goals. Recognize and celebrate achievements in sustainability to reinforce the company’s commitment to double materiality.

Challenges and Solutions

Data Complexity

In speaking to any ESG practitioner, one of the first challenges to arise is data collection. The data itself is often spread throughout a company, does not fit neatly into easily-organised spreadsheets, or may be difficult to understand in differing contexts (i.e. data from suppliers regarding their carbon emissions may not be shared in the format required by reporting standards).

To address this, companies can invest in advanced data management tools, third party support or automation systems, and design internal systems for data collection. It will be an investment of time and personnel but is also likely to be regulated and required in the near future.

Stakeholder Alignment

Particularly in industries with heavy manufacturing or extractive practices, it may be difficult to align stakeholder interests in a manner that is socially and environmentally material, without sacrificing financial performance. Engaging with stakeholders and third-party expertise while seeking innovative solutions and long-term strategic planning allows companies to effectively address ESG concerns.

Conclusion

Navigating double materiality requires a strategic and integrated approach that aligns financial performance with societal and environmental impacts. By establishing robust governance frameworks, actively engaging stakeholders, conducting dynamic materiality assessments, integrating ESG into risk management, developing comprehensive reporting mechanisms, and fostering a culture of sustainability, companies can effectively integrate double materiality. Success in this area not only enhances corporate reputation and stakeholder trust but also drives long-term value creation in an increasingly sustainability-focused world.

Resources

Boeke, E., York, B. N., London, D. M., Tsocanos, B., York, N., & Paris, P. G. (2022). Sustainable Finance Credit Ratings ESG Materiality Map Aerospace And Defense.

Commission Delegated Regulation (EU) 2023/2772 of 31 July 2023 supplementing Directive 2013/34/EU of the European Parliament and of the Council as regards sustainability reporting standards, (2023).

Sean Michael Kerner. (2024, April). Double Materiality. Https://Www.Techtarget.Com/Whatis/Definition/Double-Materiality#:~:Text=Double%20materiality%20acknowledges%20risks%20and,Environment%20and%20society%20at%20large.

S&P Global. (n.d.). Materiality Mapping: Providing Insights Into The Relative Materiality Of ESG Factors https://www.spglobal.com/esg/insights/featured/special-editorial/materiality-mapping-providing-insights-into-the-relative-materiality-of-esg-factors

Worldfavor. (2023, July). CSRD: what is the double materiality assessment? Https://Blog.Worldfavor.Com/Csrd-What-Is-the-Double-Materiality-Assessment.

Erika Anderson’s work has focused on ESG and sustainability in the tech and finance space for the better part of a decade. In working closely with industry partners, she focuses primarily on issues of sustainable finance, social and environmental intersections, and actionable research for strategic ESG implementation. She also serves as Co-Founder of the Guam Human Rights Initiative, a collaborative research nonprofit focused on human rights issues on Guam and throughout the Pacific.

A Guide for MiCA sustainability disclosures for cryptoassets

Scottish Fintech Company, Zumo wrote a very detailed guide on the implications of the Markets in Crypto-Assets Regulation (MICA) and its sustainability disclosure requirements for the crypto industry. The central idea is that MICA’s new regulations will significantly impact how cryptoassets are reported, particularly concerning their environmental sustainability.

Key takeaways from the article begin by explaining;

- The MICA framework, established by the European Union, aimed at creating a unified regulatory environment for cryptoassets. This regulation addresses issues such as market integrity, consumer protection, and the environmental impact of digital currencies.

- MICA mandates that cryptoasset service providers must disclose detailed information about the sustainability of their operations. This includes the energy consumption and carbon footprint associated with the production and use of cryptoassets. The article highlights that these disclosures are crucial for fostering transparency and accountability in the crypto sector.

- The challenges that crypto firms may face in complying with MICA’s sustainability requirements, including the technical difficulty of measuring energy consumption accurately, the cost of compliance, and the need for standardised reporting methods. Zumo Tech emphasises that while these hurdles are significant, they are essential for the long-term viability of the industry.

- Zumo Tech outlines the broader implications of MICA on the crypto industry. The regulation is expected to drive innovation towards more energy-efficient technologies and practices. It could also influence investor behaviour, as greater transparency may attract environmentally conscious investors. The article suggests that, in the long run, these changes could lead to a more sustainable and resilient crypto ecosystem.

The guide written by Zumo provides a comprehensive overview of MICA’s sustainability disclosure requirements and their potential impact on the crypto industry. The regulation will enhance transparency and drive sustainability, but it presents significant compliance challenges.

To read the full guide, click the link here.

Preparing for DORA: What UK Fintechs Need to Know

Season 5, episode 5

Listen to the full episode here.

Set to reshape how financial entities across Europe and beyond approach digital resilience, DORA is more than just another compliance requirement, it’s a game-changer for fintechs, financial institutions, and third-party service providers.

What does this mean for UK fintechs, particularly in a post Brexit landscape? How can firms prepare, adapt, and turn compliance into a competitive advantage?

In this podcast we break down everything UK fintechs need to know about DORA, from key requirements to practical implementation strategies.

Participant-Rob Mossop – Chief Digital Officer (CDO) at Sword Group

-Luke Scanlon – Head of Fintech Propositions, Legal Director, Pinsent Masons

-Mick O’Connor – Founder and CEO at Haelo

BLK’s £50 Million Funding, a Turning Point for Digital Commodities Trading

The commodities trading industry, historically reliant on traditional methods, has recently seen a surge of digital innovation. At the forefront of this digital revolution is Scottish fintech BLK, a pioneering UK-based online commodities marketplace, which has just secured an impressive £50 million equity investment from Panama-based Nimbus Capital. This substantial funding signals a shift toward technology-driven solutions within an industry ripe for transformation.

Commodities trading, involving everything from metals and energy to agricultural goods, has long suffered from inefficiencies and lack of transparency. Traders frequently navigate complex logistics, opaque pricing structures, and cumbersome administrative processes. BLK’s mission has been clear from the start, to disrupt these traditional trading barriers using advanced technology like blockchain and artificial intelligence (AI). With Nimbus Capital’s backing, BLK is now in an even stronger position to realise this vision.

Blockchain technology, well-known for its application in cryptocurrencies, holds immense potential for commodities trading. It enables unprecedented transparency by securely recording each transaction on an immutable ledger. This reduces the risk of fraud and error and fosters greater trust between buyers and sellers. With AI, BLK is further streamlining trade by optimising logistics, forecasting market trends more accurately, and significantly reducing operational costs. These technological advancements will reshape how commodities markets function, offering substantial competitive advantages to early adopters.

The £50 million investment will also directly support BLK’s operational expansion. Key plans include the strategic acquisition of new shipping vessels, which is crucial for expanding BLK’s logistics capabilities. Enhancing logistics will ensure BLK can efficiently meet rising demand, reduce shipping times, and improve the overall reliability of commodity supply chains.

The investment is a clear indication of BLK’s long-term strategy and market ambition. BLK has announced plans to list publicly via an IPO in 2025, a major milestone that will open new avenues for growth, visibility, and investor engagement.

Accelerating Action: Enabling Female Leadership

Welcome back to our spotlight series celebrating colleagues who are inspiring change and Accelerating Action across the technology sector. This month’s edition focusses on female leadership and the enhancement of progression opportunities.

International Women’s Day 2025

For every 115 UK tech roles only one will be filled by a woman, thus revealing a significant underrepresentation in the sector and huge loss given the benefits for financial performance and innovation generated from gender diversity. This is further illustrated by the fact that although women make up nearly half of the overall workforce, only 24% of the UK tech force is female.

These barriers in tech result in major difficulties for promotion and career growth for women in the sphere. In fact, a 2022 report from McKinsey found that only 52 women are promoted to manager for every 100 men in the tech industry. This figure is surprising considering inclusive environments mean career advancement are significantly more likely for both men (15%) and women (61%).

BT Group and FinTech Scotland are committed to championing female progression and recognise that inclusion and diversity is critical to growth.

BT Group Celebrations

This year, BT Group are choosing to focus on the theme of “Remarkable Women” to highlight the inspirational and innovative work of many talented female colleges within BT and across various industries.

BT Group are passionate about ensuring women have the skills and tools to move into the tech sector and advance their careers. For instance, BT’s Passport scheme and ‘three together and two wherever’ encourages flexibility in the workforce by allowing those who need it, to work from home. This inclusive scheme acknowledges familial responsibilities, enhancing opportunities and increasing diversity in the workplace.

BT works to inspire and encourage women to enter the Telco sector, teaming with charities including CodeFirstGirls and Black Girls Tech Summit to empower women and help them stay ahead in a competitive industry. BT Group’s Returner initiative supports women to re-enter the workforce, recognising the unique hurdles career returners face. The program is designed to provide mentorship, training and hands-on experience to help individuals regain confidence and thrive in their careers (Flexa., 2024).

Fiona Vines, Chief Inclusion, Equity & Diversity officer at BT Group, is a key example of a woman who has reached a successful leadership position despite facing unexpected challenges and prejudice in a very male dominated industry. Fiona is a keen feminist and an inspiration, particularly to women who are looking to grow their career and have a family at the same time. Another notable example is Claire Gillies, CEO of Consumer, who is passionate about supporting women and advancing female leadership by being apart of the International Women’s Forum.

Fintech Scotland Celebrations

Exceptional leadership at FinTech Scotland was highlighted in the Innovate Finance Women In Fintech Powerlist in March 2025 with both its CEO, Nicola Anderson and its Research & Innovation Programme Manager, Lauren Cassell making it to the list.

Nicola appeared in the 45 Standout List recognising women who have made an incredible, lasting impact in fintech, going the extra mile to enable sustainable change.

Lauren was named amongst the Rising Stars for her amazing contribution to fintech innovation through her work at FinTech Scotland’s Financial Regulation Innovation Lab and for the FCA’s Innovation Lab.

Allison Kirkby, CEO, BT Group

Allison Kirkby is a pioneer in the world of business, breaking barriers and traditional perceptions. BT Groups’ first female CEO, started off as a Chartered Accountant Apprenticeship. Described as a “proven leader, with deep sector experience” she is already immersing herself in the business, transforming the organisation by cutting costs, restructuring areas and finding saleable assets. Her determination to find savings and optimise efficiency is visible through the 3% reduction of the workforce and negotiations to sell BT’s 50% stake in TNT Sports, formerly known as BT Sport. Allison’s hands on approach has already resulted in rising share prices and efforts to improve productivity has been successful with the more strictly monitored “three together, two wherever”.

“None of them look, talk or think like me… so I need to get in there!”

Allison is passionate about showcasing incredible female talent at BT Group and advises colleagues to “Be brave, be bold, be fearless” and “regularly put yourself out of your comfort zone”. This advice is highly beneficial to all women looking to succeed and inspires confidence in senior leadership as the company goes through a restructuring. Her career growth from a Chartered Management Accountant apprentice to now one of only 10 female CEOs among the FTSE 100 companies is a testament to her resilience and determination.

“Always think of the ‘So what?’ or ‘What if?’ questions”

Nicola Anderson, CEO, FinTech Scotland

Nicola Anderson, CEO of FinTech Scotland since January 2021, has been pivotal in establishing Scotland as a leading fintech hub.

Under her leadership, FinTech Scotland was recognised as a cluster of excellence at the European level, reflecting the region’s prominence in financial innovation. Nicola’s commitment to driving collaboration is evident in initiatives like the Financial Regulation Innovation Lab (FRIL), launched in 2023. This industry-led program brings together regulators, financial institutions, and fintech firms to explore technological solutions for regulatory challenges and build a safer and more inclusive financial services sector.

Beyond her role at FinTech Scotland, Nicola serves as a non-executive director at Advice Direct Scotland and is a member of both the Scottish Taskforce for Green and Sustainable Financial Services and the Scottish Government’s Financial Services Growth and Development Board.

Throughout her career, Nicola has been an influential advocate for making finance work well for customers, society, business, and markets. She has been directly engaged in digital and data transformation, regulation, and policy development, with an emphasis on innovation, collaboration, and customer-focused outcomes.

Nicola’s dedication to diversity and inclusion is also noteworthy. She has been instrumental in developing lasting relationships between FinTech Scotland and a broad range of consumer and citizen advocate groups, such as Money Advice Scotland, Advice Direct Scotland, Age Scotland, and Mental Health and Money Advice. This work led to the creation of the first fintech consumer panel in the UK, enabling cross-sector collaboration in building fintech propositions focused on citizen needs.

In her own words, Nicola emphasizes the importance of collaboration for driving better consumer outcomes:

“Bringing together ambitious fintech firms and leading financial institutions not only enhances good consumer outcomes—it accelerates the development of inclusive digital financial services and supports the evolution of the future digital economy.”

Below you will find sign up links where you can get involved in celebrating this year!

- House of Nine Sorority – 8th March – 2nd Annual International Women’s Day Assembly & SIS Program Finale Registration, Sat, Mar 8, 2025 at 11:00 AM | Eventbrite

- Changing the face of Northern Ireland – 8th March Members of the Irish Writers Union since 2019 | How Ulster makes its money

- The World Association for Sustainable Development (WASD) – 8th March – International Women’s Day 2025 Tickets, Sat 8 Mar 2025 at 10:00 | Eventbrite

- EMPLUMAR – Own Your Wins – an Imposter’s Dilemma Game – 13th March –International Women’s Day 2025 – Emplumar

- WIBF – Fertility in the workplace- 12th March 12:30-1:30pm – Fertility in the workplace – WIBF

- MiGSO-PCUBED Project Management Consultancy – 12th March – 3:30-6pm International Women’s Day Project Panel Discussion MIGSO-PCUBED Tickets, Wed 12 Mar 2025 at 15:30 | Eventbrite

- Bright Network ~ Making HERstory – 12th March Bright Network Making HERstory | Bright Network

- Transformative potential of gender equity in negotiation and leadership – 16th March – 3-4pmNegotiating equality: unlocking the power of diverse teams : WorldCC

- National Council of Women GB – Women and Poverty – March 20th 12-2pm-Women and Poverty Tickets, Thu, Mar 20, 2025 at 12:00 PM | Eventbrite

- ETHERA Empower Tech Women – 18th March 4-4:45pm – March – Introduction to ETHERA: Mentoring for Women in Tech Tickets, Tue 18 Mar 2025 at 16:00 | Eventbrite

- Rewriting the Code ~ Unite & Ignite Women in Tech Summit – March 25-27th Unite & Ignite Summit | Rewriting the Code

- One Tech World 2025 – Conference for Women in Tech – 28th March – 9:30-5 wearetechwomen.com