Shaping the Future of ESG in Financial Services

Season 5, episode 6

Listen to the full episode here.

In this episode Richard Nicol from the Phoenix Group and Tom Mcfarlane from EY speak to us about the ESG challenges they are facing and why they decided to join the Financial Regulation Innovation Lab programme to find solutions to those challenges as well as what they are looking for with applicants.

To apply for this innovation call visit this page.

Fintech – a force for good

Season 4, episode 1

Listen to the full episode here.

Episode recording with Fintech Australia.

Fintech has emerged as a transformative force in the financial sector, offering innovative solutions that not only enhance financial services but also address broader societal issues, including environmental sustainability, customer vulnerability, and overall financial well-being.

Those objectives are heavily featured in the Research & Innovation Roadmap that we published 2 years ago.

In Scotland, we have an important number of fintechs addressing those challenges. In fact, the majority of Scottish fintechs are fintech for good.

Today we’ll take some time to consider how those organisations are driving positive changes.

Guests:

Ren Hooi, Founder and CEO at Lightning Reach

Robin Peters, Co-founder and CEO at Snugg

Sheila Hogan, Founder and CEO at Biscuit Tin

Scotland Fintech Festival – Episode 2 – Snugg & TSB

Season 3, episode 11

Listen to the full episode here.

In this special 2023 Scotland Fintech Festival episode we spoke with Mike Teall, Co-Founder and Chief Commercial Officer at Scottish fintech Snugg and Adam Betteridge, Partnerships and Open Banking Lead at TSB.

We discussed TSB Innovation Labs that saw Snugg secure a partnership with TSB, helping the bank’s customer make their homes greener.

We focus specifically on what makes for a good collaboration between established financial firms and fintechs.

A £250 Billion Opportunity: How fintechs can lead the charge in greening UK homes for Net Zero

One of the newer startups of the Scottish fintech ecosystem, Snugg, is dedicated to making energy efficient homes simple and affordable for everyone. Co-founder Robin Peters spoke to us about his concept of climate finance and challenges, as well as his recommendations for fintech companies entering the space.

In the UK, homes make up a fifth of total carbon emissions, and it is estimated £250 billion pounds of investment is needed to make homes energy efficient if we’re to hit our net zero objective by 2045. To get there, the private sector will have to play a significant role in support of that. While investment in large infrastructure projects, such as wind farms, are supported by quite mature financial vehicles, there has been very little progress in innovative finance solutions for homeowners.

“One of the key challenges is that investment related to decarbonising homes is generally quite expensive and intrusive. And frankly, the investment case often isn’t very attractive to people,” points out Peters. “So it’s quite a difficult nut to crack, but also extremely important.”

Climate finance plays an important role in tackling this challenge because it brings together different elements of the private sector to underpin finance initiatives to help the world achieve its net zero ambition. The goal is to not only direct investment into getting projects off the ground, but it’s also about helping financial services customers to invest in climate-positive activities.

Yet there are a number of barriers that need to be overcome, including the need for more consistent government policy around green incentives, and the fact that general consumers have got to want this more. Further, there needs to be more integration across the supply chain. “People need things to be made simple for better take-up of the pro-climate incentives that are on offer,” explained Peters. “There should be a deeper alignment amongst the different providers across the supply chain, for example, between a trusted installer, the financial provider, manufacturers and the government.”

The financial sector now also has an opportunity to pave the way more seamlessly. Firstly, they can put all their data to more intelligent use by targeting personalised initiatives and engaging with customers in a more meaningful way. Secondly, there is scope for innovation in green financial products, such as pay-as-you-go (where people can repay loans based on savings they have achieved from making their homes more energy efficient) or property-linked finance (where a loan is linked to a house rather than a person). Peters notes a slight degree of reluctance in the financial sector at present, yet he is optimistic that in the future there will be better auditing of banks to assess whether financial products are truly delivering.

His top three recommendations to Scotland’s fintechs wanting to incorporate climate concerns into offering?:

- Focus on the data: There’s a lot of data out there that can be improved and interrogated for better insights

- See the opportunity: A perception shift is needed to see that this is an opportunity for real innovation. There’s a huge investment opportunity for financial services, yet patience is needed as banks can be particularly slow in adopting truly new innovations

- Collaborate: It’s an incredibly dynamic market which literally needs to grow by a factor of ten in the next 4-5 years. There’s also an enormous amount of innovation, and sharing different ideas with emerging players and other participants will help come up with the best solutions for the market.

Defining Climate Finance

Kirsteen Harrison, the Environment & Sustainability Advisor at the digital-assets platform, Zumo, is a stubborn optimist with a fierce conviction that businesses should be a force for good. As such, she works with leaders to facilitate the mindset shift required for businesses to thrive in a net zero future.

She notes that the term climate finance’ is a multifaceted concept, which in her view, may be used as an all-encompassing term and often gets confused with green or sustainable finance. “Climate finance has been specifically defined by the United Nations Framework Convention on Climate Change (UNFCCC) as finance for climate mitigation, adaptation or resilience,” Harrison explains. “To me it also includes generally enabling and delivering flows of climate finance to the parts of the world where it’s needed most.”

To support the flow of climate finance, financial institutions are having to establish transition plans that show not only how they will meet their own net zero targets, but to ensure financial flows actually shift towards supporting decarbonisation. This requirement has not quite yet filtered down to most fintechs. Harrison cautions that the requirement for fintechs to consider the financed emissions they are facilitating will arrive sooner than they think, and that the pace towards transition will move extremely quickly and not in a linear fashion. “I think as businesses, we tend to look at past events and timelines as a way to predict what might happen in the future. And with climate change we cannot do that, that is actually quite a dangerous thing to do,” cautions Harrison. “In terms of evolution, I think it is going to be much faster than we are used to seeing. Not only is that needed, it’s to be encouraged.”

Harrison also believes that improvements to ESG investing need to be made. She acknowledges that while this is a fast-evolving landscape and there is rightly a fear of greenwashing, there is nevertheless a much higher burden put on ESG investing. “ESG investments rightly need to prove that they meet certain criteria through data, whereas non-ESG investment does not.”

She has confidence, however, that blockchain technology will be a true enabler for delivering climate finance. Because blockchain provides an immutable ledger, it can ensure that finance is delivered to the points it actually needs to be delivered to, which is especially important for jurisdictions lacking in good governance structures. Blockchain can also play an important role in supporting the role of quality carbon credits and renewable energy certificates (RECs) by avoiding legacy issues such as double counting.

Harrison has three main pieces of advice for fintechs wanting to incorporate climate finance into their offerings:

- Do it authentically: Rather than simply launching a green product, sustainability principles need to be embedded in your business alongside credible net zero commitments.

- Stay two steps ahead: Because we’re working within such a rapidly changing landscape, planning needs to determine what might be needed in three, five or seven years’ time, or risk quickly becoming out of date.

- Be mindful of financed emissions: A big part of the carbon footprint of the financial industry is financed emissions’, which are the greenhouse gas emissions linked to investment and lending activities. Fintechs need to very carefully consider how their work might be impacting financed emissions, and, if necessary, pivot and support climate-friendly choices and investments instead.

Awareness is key. Ultimately, fintechs need to take responsibility for the impact that investment decisions can have on harming the environment, as well as the impact that they as technology providers might have on affecting the system as a whole for the greater good. In doing so, they will attract and retain new talent, increase trust in their brand and prepare themselves for the fast-evolving sustainability disclosures landscape.

Carbon Markets: How can fintech avoid green washing?

Season 3, episode 2

Listen to the full episode here.

The FinTech Scotland Research and Innovation Roadmap highlighted the growing focus on climate considerations for the financial services sector.

Whilst this is in part driven by consumers, demanding better transparency for the products they invest in, this is the launch of new regulations that is accelerating the move to a more sustainable financial sector.

Financial services providers are facing growing challenges around ESG reporting due to the difficulties around the availability of trustworthy data. This has led to mounting concerns around greenwashing.

In a bid to clamp down on greenwashing, the Financial Conduct Authority (FCA) is proposing a package of new measures including investment product sustainability labels and restrictions on how terms like ‘ESG’, ‘green’ or ‘sustainable’ can be used.

In this podcast we discuss how to best avoid greenwashing moving forward.

Guests:

Colin Carmichael – Sustainability Director at PwC

Jules Salmond – Founder at Ciendos

Matthew Brander – Senior Lecturer in Carbon Accounting at The University of Edinburgh Business School

Fintech and space: Innovation examples

Season 2, episode 8

Listen to the full episode here.

Fintech innovation is powered by data. New solutions appear every day, always consuming new data to develop new services to help people and organisations deal with money. Innovators are constantly in search for new data sources. The Scottish space sector has developed to be one of the largest in Europe. This industry, thanks to technology advances, can generate an incredible amount of data, from climate data to supply chain data, and much more., The fintech sector in Scotland is developing rapidly alongside an already very well-established financial sector. As new innovative solutions require more and more data, we’ve turned to the sky to understand how earth observation type data can help leverage the fintech opportunity. Guests: Christophe Christiaen – the Data, Innovation and Impact Lead within the Oxford Sustainable Finance Group Robin Sampson – CEO and founder at Trade In Space

Fintech and Space

Season 2, episode 7

Listen to the full episode here.

As we transition to a more sustainable future, data, technology and innovation will help to drive and accelerate the insights, products and services to enable the changes needed.

Earth Observation Data can enable new innovations that can help to advance financial inclusion, incentivise better climate related behaviours, and support the net zero agenda.

Scotland has built significant experience in Space Tech and Space Data. Combined with the strength in FinTech innovation, this offers a substantial opportunity for future FinTech innovation and research.

We can accelerate change through greater collaboration across Space and FinTech. This starts with building an understanding of current capabilities, in both space and fintech innovation.

FinTech Scotland and Space Scotland are working closely together to bring our ecosystems together to share learnings & explore the challenges in the financial services sector that innovation could address, shaping more sustainable finance, and building confidence in future investments

Participants

Host: Mickael Paris – Marketing Director at FinTech Scotland

Guests:

Peter Young – CEO at Global Surface Intelligence & co-founder of the Scottish Space Leadership Council

Kirsty McKenna – Innovation programme Manager at FinTech Scotland

The FinTech Research and Innovation Roadmap

Season 2, episode 1

Listen to the full episode here.

In March 2022, FinTech Scotland released its 10-year Fintech Research & Innovation Roadmap for the UK.

In collaboration with leading universities, large financial institutions, fintech businesses, citizens, industry experts and senior officials this report explores the opportunities that will help the UK maintain its fintech leadership globally.

In this episode we explore what this roadmap means for Scotland and what the next steps are to deliver on the roadmap recommendations.

FinTech Research & Innovation for Climate Finance

The impact of climate change across the world is disrupting national economies and affecting lives. It requires urgent action from all to address the growing issue.

In its 2020 Global Risks report, the World Economic Forum highlights that the risk signals show the horizon for addressing climate risks has shortened. For the first time in the history of the report, the top five risks that it outlines are in a single category: climate environmental change’

In the Research & Innovation Roadmap, we use the term Climate Finance to describe the role that finance, technology and data can play in addressing the climate change crisis and powering a sustainable future.

The importance of Climate Finance

Enabling a more sustainable future was a prominent theme throughout the research for the development of the Roadmap. Throughout our analysis, the influence of finance together with the potential for exponential change through technologies was thought to be a powerful combination to help the necessary transition to a carbon neutral economy.

In the UK, financial regulators are aiming to influence positive climate outcomes through a series

of new expectations, rules and guidance. The Bank of England is working to encourage an early and orderly transition to a carbon neutral economy and to “play a leading role, through policies and operations, in ensuring the financial system, the macroeconomy, and the Bank are resilient to the risks from climate change and supportive of the transition to a net zero economy.”

The Financial Conduct Authority also has a sustainable finance strategy, aiming to build greater transparency and trust, developing guidance and tools to provide mutual support to address the challenges of climate change.

Climate Finance is a complex matter. Our research with FinTech Scotland showed that it connects many things, including:

- Investment

- Regulatory change

- Better data

- Advanced analytics

- A deeper understanding of consumer behaviours and consumer engagement

- A deeper understanding of new technologies, biodiversity, carbon, and carbon markets

The challenge ahead is huge. Nevertheless, the research behind the Roadmap pinpointed three priority areas where further FinTech research and innovation could advance progress by helping nations adapt to the impact of climate change, manage the risks of transition and lead to them becoming greener, more resilient and more inclusive. All three offer Scotland and the UK an opportunity to use strengths in research and innovation, and to build collaborative action across the FinTech and finance industry and the research community.

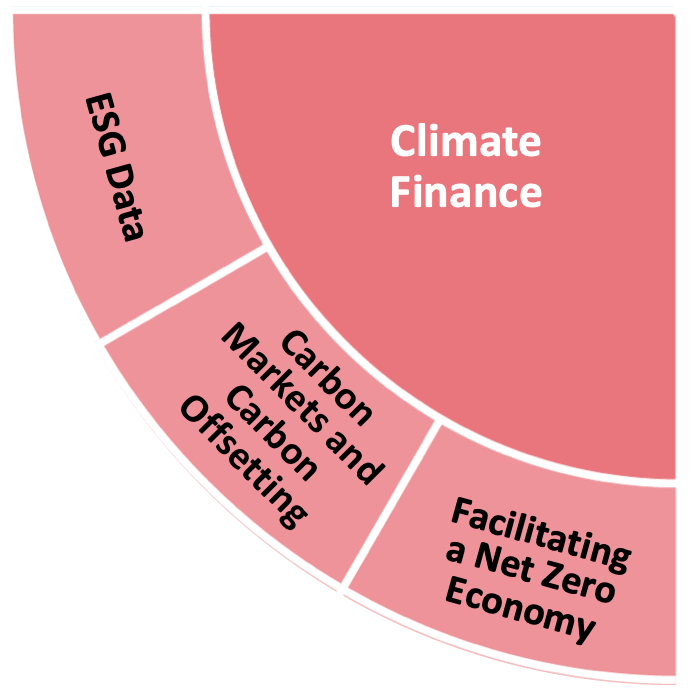

Priority areas in Climate Finance

Environment, Social, Corporate Governance (ESG) data.

Assessing the current situation and outlining the ambition for new data sources, clearer standards and advanced analytics to build greater trust and transparency in the sustainable claims made by finance and business.

- ESG reporting

- Investor confidence

- ESG data

- SME market

Carbon markets and carbon offsetting

Considering the role that each plays in realistically transitioning to a net zero low-carbon economy while exploring the technologies and innovation that could drive further progress.

- Voluntary carbon markets

- Carbon offsetting

Facilitating a net zero economy

Moving beyond finance-as-usual practices. Using innovation and technology to reinvent financial markets and stimulate the change needed to support a healthier planet.

- Investment decisions for net zero

- Circular economy

- Housing

- Insurance

- SME market

Roadmap next steps: Climate Finance

A range of proposed next steps are laid out in the published Roadmap, which specifically identifies 8 actions relating to Climate Finance, and categorises each into one of three phases over the next 10 years. These actions are illustrated in the graphic below. the report also references 25 different stakeholders who can support the implementation of these actions, which are broken down into research projects and innovation calls.

More information about FinTech Scotland’s Research & Innovation Roadmap can be found here, where the full Roadmap can also be downloaded.