Opening Data Responsibly

Kent Mackenzie leads Deloitte’s Risk Analytics practice and has spent over 12 years in a range of financial services roles. With a passion for FinTech, data and advanced analytics, Kent has worked with local, national and international clients to develop tech and data solutions to manage financial crime, regulatory compliance, credit risk, and collections & recoveries.

“Data, quite frankly, should be considered as the lifeblood of any form of innovation and technological development,” says Mackenzie. “It’s very pertinent in our industry, financial services, that all products and advice for consumers require a hefty analysis of data; either on a personal level based on likes, preferences, hopes, dreams and desires, or with an overlay on those products of the broader population’s needs.”

In Mackenzie’s mind, having open access to data is what really helps innovation advance quickly, specifically in financial services, because it helps provide specific information on the types of products and services that can be offered. “If we can democratise data in this space, we can open up financial services to a variety of communities that perhaps haven’t in the past had the privilege of a financial product or service,” he explains. “It can help us to educate those that perhaps need a bit more help in understanding financial products.”

Before we get to this point, however, we need to rectify the opposing forces between the desire and ambition from organisations, regulators and innovators, to democratise data and create an open playing field, versus an anxiety around data privacy, respect of data and regulatory access to data. Mackenzie maintains that while we recognise the need to provide access, we need to do so respectfully and within the confines of respecting privacy, data integrity and bias. Over the past five years, he believes regulators within the UK have been doing a great job of opening up safe sandboxes, and credits the open data movements that have created anonymised data that is meaningful and can be accessed safely. He underscores that all this needs to be done in a non-competitive manner. “There’s a higher calling here to create these types of safe spaces to play,” says Mackenzie.

He believes the next incarnation of open data is eventually about providing a complete life-view of how one’s finances may be structured and how people could be guided and remain financially literate along their journey. This chain of events will prompt major innovations within the traditional financial services sphere. For example, real estate businesses can provide a number of add-on services around things such as affordability, insurance and tax standing.

The most important guiding principle of open finance, Mackenzie maintains, is the huge opportunity to level the playing field. “Fundamentally, financial services are a basic human right, and there are some staggering facts whereby large parts of the population do not have access to that basic human right,” he emphasises. “Also, I think that the ability to blend finance into our everyday lives is really exciting. It will create a really good opportunity to have financial services writ large.”

How Open Finance is revolutionising lending

Season 3, episode 9

Listen to the full episode here.

Lending money is a process that has long been around and for many years it was left undisrupted. People are very familiar now with credit scores and the idea that to get credit you need credit.

New solutions and technologies are coming to disrupt this market to make financial products more accessible to a greater number of people.

In this episode we’ll look at how Open Finance is changing the status quo and look at some fantastic examples of fintech innovation.

We’ll also look at how credit bureaus are adapting and partnering with fintechs to evolve their own models.

Guests:

Robert McKechnie – Head of Products at Equifax

Crawford Taylor – CEO and Founder at Nude

Standards for Innovation: Mapping the global financial landscape in Open Banking

The expansion of Open Banking across the globe has led to a burst of innovation within financial products, leading to improved customer money management where consumers give access, and consent to their data being used. The opportunities to transform the economy and society are even greater with more countries embracing Open Finance and putting in place a secure data-sharing infrastructure across multiple industries and not just banking.

With Open Banking initiatives gaining momentum around the world, a range of different standards are emerging. Smart Data Foundry and Ozone API have collaborated to develop the Standards Library and Innovation Atlas, outlining the features and similarities between different standards being set across the globe. Beyond a general desire to drive innovative outcomes, not all standards are designed with the same intentions in mind. As nations look to allow API access to customer-consented data, it’s clear that the main drivers may differ, from competition and inclusion to stability or innovation.

For the UK, with its ground-breaking Open Banking Standard, increasing competition was key. The Competition and Markets Authority’s (CMA) 2016 report found that big banks dominated the market and wanted consumers to benefit from introducing other players. Has the mandating of Open Banking worked to achieve this in the UK? The FCA reported in 2022 that large banks’ historic advantages were starting to weaken, in part due to digital innovation.

As well as increasing competition, Open Banking’s other advantages are consumer based- such as increasing the ease of charitable spending and financial decision-making.

So how do the main objectives of other standards vary?

Countries with financial inclusion in mind in their Open Banking regimes, such as Brazil, Mexico or Indonesia, look to embrace a broader scope of data exchange and invite new participants into the regime to ensure a greater diversity of products and services for the financially vulnerable.

From the outset, Banco Central do Brasil’s goals aimed for a more inclusive and competitive business environment’, highlighting the promotion of financial citizenship as one of their four objectives. Also listed were encouraging innovation, promoting competition and increasing the efficiency of the National Financial System and the Brazilian Payment System. From the outset, a broad range of products were included in their standards to tackle these objectives.

The Open Banking move for India was part of a bigger infrastructure build called India Stack, encapsulating a digital identity infrastructure, a digital documents system, a payments system (UPI) and the account aggregator framework. This was part of a massive digital overhaul of the management of the economy, with paperwork dominant, to address financial inclusion. Cross-border interoperability, particularly for remittance payments, is another target being addressed by the nation.

Financial access is a top priority in Mexico for the government, whose Fintech Law was enacted in 2018. However, regulated Open Banking is not yet a reality, but with a FinTech ecosystem growing rapidly and it being a hotbed of software engineering talent, Mexico will be one to watch when Open Banking does come into force.

Finally, in the Kingdom of Saudi Arabia, Open Banking has been driven as a pillar of the ambitious vision for Saudi 2030. Open Banking and Open Finance are key enablers in transforming the financial services sector, economy, and society.

As Open Banking standard frameworks are developed globally, it allows for innovative products to spread across borders. Smart Data Foundry’s aizle synthetic data engine looks to drive innovation and produces Open Banking compliant synthetic data. Ozone API provides compliant open API technology to monetize Open Banking globally. The global environment for applying APIs and synthetic data can be understood with Standards for Innovation.

Learn more about the global financial landscape by exploring Smart Data Foundry’s”¯Standards for Innovation.

Written by Magdalena Getler and Lucy Lloyd (Smart Data Foundry), Huw Davies, Chris Michael (Ozone API)

UK Fintech Week special – a chat on synthetic data with Smart Data Foundry

Season 3, episode 6

Listen to the full episode here.

In this special episode with speak with David Tracy, Head of Data Science, at Smart Data Foundry on the week they presented their new Aisle proposition at Innovate Finance Global Summit.

What is synthetic data is? How is it different from real-world data?

We’ll explore how it will speed up innovation and collaboration in the fintech world, what the risks and benefits are and much more.

David will also speak to us about the work they’ve done with the FCA and the PSR to tackle APP fraud using Agent Based Simulation.

Open Banking – the UK’s next biggest export?

According to Accenture, there’s $416bn of revenue at stake for fintechs and banks across the world by the end of this decade. That’s roughly four times the size of the scotch whisky market ($91bn) – so is Open Banking the UK’s next iconic export? Maybe”¦ but only if we make some important changes

Last week, we released a piece of research – The Global Open Finance Index. It tracks the development of Open Banking across the world and focuses on the 23 countries where we’re seeing the most progress. Its findings are fairly stark. The UK’s position as a leader in the space, which was once completely uncontested, is now in serious danger of evaporating.

Countries like Brazil and Australia are accelerating with regulatory regimes that already go far beyond the UK’s initial blueprint whilst markets like India and the US are finding different approaches leveraging market forces and industry collaboration to create huge potential. India’s Open Banking standard now covers a group of more than 1 billion accounts whilst in the US 42 million accounts have coalesced under the FDX standard with zero regulatory push. Perhaps even more significantly, that regulatory push is coming in the US and soon. The Consumer Federal Protection Bureau (CFPB) is already in the late stages of consultation on how that process should be rolled out and they have the legislative backing to get it done.

So where does this leave UK fintechs?

I have no doubt that Open Banking and (eventually) Open Finance will have profound impact on the UK, revolutionising our credit market, bringing huge, excluded groups into mainstream finance and providing differentiated competition to the card rails, but in terms of the economics, the real prize is still on the table.

UK firms have built businesses that are designed to handle large quantities of API-driven transaction data. They’ve developed the security systems to protect the data, the skills to handle, clean and contextualise it and the case studies to prove how impactful that data can be. They are, in short, in a position of huge competitive advantage vs companies at the beginning of this journey in evolving markets. In order to maintain that advantage though, they have to keep working at the cutting edge of the technology, here the UK is falling down.

Australian firms are already working with Open Energy data, Brazilians are getting to grips with the wider financial product set through their country’s Open Finance programme.

We have to accelerate progress in the UK and the opportunity to do that is here.

On the public policy side, we need to establish a strong, independent body to preside over the future of the sector, we need to move on Open Finance, (the data bill is sitting in a drawer in parliament and should be moved forward as a priority) and we need to think about how we can build regulatory passporting into trade deals as we sign them.

On the market forces side we need more banks to take a leaf out of NatWest’s book and accelerate the development of premium APIs, we need to align on risk and liability frameworks for the use of these and work towards clarity for the market on commercial details. Finally we need better engagement between institutional lenders and retail lenders that use open banking data. Cost of capital is a major hurdle for Open Banking’s proliferation in the lending space and this both can and should be addressed.

This is a blockbuster agenda for 2023, but if we can get it done the prize for UK firms will be transformational. If we can’t, Open Banking will still have a major impact on our domestic economy but it might not be the firms hiring UK talent and paying UK tax that deliver it. This is not beyond us. There’s a lot to do but if we lace up our trainers, I’m very confident that we can make it happen.

”˜Consumer’ data has failed its creators

Consumer data’ is a remarkable quantity for the lack of ownership afforded to its eponymous creator ”“ the internet browser, the Google-er’, the consumer. Indeed, all of us are the creators of digital data from which Big Tech ”“ Google, Facebook, Amazon (you know the names) ”“ have achieved their giant status.

In fact, each time we open a website or app we leave behind a digital footprint used to track our movements across different websites and applications. This trail is inspected by Big Tech’s pack of algorithms, subsequently, determining’ a web user’s probable interests in products, ideas, and trends. With such an accurate’ determination of human interest at its disposal, Big Tech amasses a library of consumer data that it sells to advertisers, generating a lucrative revenue stream.

The relationship between consumers and advertisers goes back to Roman market squares and still serves just as important an economic function today. Yet, in today’s digital context, the creators of the industry’s most prized resource ”“ data ”“ have been excluded from sharing in its reward.

How has such an intrinsically unjust state of affairs survived for so long? Largely because consumers have been misled. In the first instance, consumers have been made to believe that their data holds no personal value. Secondly, that lack of control over data and, indeed, privacy is inseparable from the internet. While, this is slowly changing, with users now able to opt out of certain trackers, Big Tech is still aggressively trying to force us to adopt them: even if a user chooses to reject certain targeting preferences, they are often forced to confirm every time they enter the site or until impatience overcomes concerns.

Although they have certainly been egregious, we cannot place the entire blame on Big Tech, advertisers also have much to answer for. Advertisers spend approximately £27 billion a year on digital marketing, for the most part, this goes straight to Big Tech. This enormous expenditure is justified because it is, in actuality, an investment ”“ an investment made to entice consumers to spend. Moreover, in today’s digitally entangled economy in which jobs, networking, and day-to-day life are so dependent on internet access, the reach of advertising is inescapable. And so, we exist within a digital ecosystem that demands we share our thoughts and data with Earth’s largest corporations, only to boost our own likelihood to spend.

Undoubtedly, this status quo must change. Consumers must recognise the worth of their data and demand remuneration. Meanwhile, advertisers must stop encouraging and feeding Big Tech with the dirty cash that encourages such malpractice. The objective of advertisers must shift from only selling to selling and rewarding. In short, advertisers who seek access to consumer data must provide them with benefits.

Fortunately, the emergence of direct-to-consumer marketing apps and platforms has made such solutions a reality. For advertisers who market via such platforms, they unlock the ability to directly communicate with target consumers, in return offering the latter cash benefits and rewards. It is the responsibility of the platforms themselves to keep the end-user in mind, leveraging their position to ensure consumers get access to the highest value rewards. Furthermore, consumers are able to identify a preferred level of privacy, exchanging a level of data access on a quid quo pro basis to maximise cash benefits, all while driving a positive feedback loop of more relevant ad targeting.

By using direct-to-consumer marketing platforms, consumers can finally reclaim the right to their data and expect a fair price for its exchange. The current economic environment, undoubtedly, makes such solutions particularly enticing.

Though, far more importantly, direct-to-consumer platforms are resetting the relationship between data and advertising, shifting power away from Big Tech and back to consumers. Slowly, we march towards a future where digital data is not a price tag of the modern economy, but a precious commodity back in the hands of its creators, who financially benefit from its transparent and consensual exchange.

Mohsin Rashid is the CEO and co-founder of ZIPZERO, which offers a mass-market consumer solution to the cost-of-living crisis. Shopping via the ZIPZERO app earns users cash to pay bills ”“ the cash rewards are funded by retailers and brands, which gain access to a formidable direct-to-consumer marketing platform, allowing them to divert a collective £27 billion digital advertising spend back to their own customers. Through its compelling consumer proposition, ZIPZERO has become a prolific source of first-party, product-level consumer data. ZIPZERO is inviting major utility firms, leading retailers & brands (advertisers) to make active use of its progressive platform and help UK consumers tackle the cost-of-living crisis.

The FinTech Research and Innovation Roadmap

Season 2, episode 1

Listen to the full episode here.

In March 2022, FinTech Scotland released its 10-year Fintech Research & Innovation Roadmap for the UK.

In collaboration with leading universities, large financial institutions, fintech businesses, citizens, industry experts and senior officials this report explores the opportunities that will help the UK maintain its fintech leadership globally.

In this episode we explore what this roadmap means for Scotland and what the next steps are to deliver on the roadmap recommendations.

Research & Innovation opportunity in Open Finance data

Article written by Julian Wells, Director at Whitecap Consulting

FinTech Scotland recently published its 10 year Research & Innovation Roadmap. Whitecap worked in partnership with the FinTech Scotland team to support the development of this roadmap, and is discussing the key outputs in a series of blogs. This blog focuses on Open Finance data, which is one of the four key strategic priority themes.

In the first blog in this series, we discussed the purpose, value and impact of a Research & Innovation Roadmap. In this blog, we discuss Open Finance data which is a strategic priority itself but also a facilitator of FinTech innovation in wider areas, and an enabler for the three other strategic priority themes in the Roadmap.

The other three themes are Climate Finance, Payments & Transactions, and Financial Regulation, each of which will be the subject of a subsequent blog in this series.

Open Finance data has the potential to significantly change consumers’ and businesses’ engagement with finance, and to deliver better outcomes. It spans the whole suite of financial products and services as we understand them today, including banking, savings, mortgages, pensions, investments, insurance, lending, and payments.

How can Research & Innovation support the development of Open Finance?

To help Open Finance achieve its potential, more leadership, actionable research, and innovation is required. FinTech Scotland’s Research & Innovation Roadmap sets out specific actions to help drive this opportunity ”“ through a collective approach that involves industry, innovators and researchers ”“ to create the future of finance.

Open Finance can create progressive change that will move the UK forward significantly, by moving beyond banking and asking other financial institutions (such as pension providers, asset managers and insurers) to enable customers to share their data with others.

This would open up a wider range of financial products and services to the transformative impact of third-party innovation through trusted data sharing. For consumers and businesses, it offers new ways to understand their finances, receive financial advice, and compare financial product features and prices.

Research and innovation are needed to facilitate the potential of Open Finance data, building economic growth and creating employment opportunities in high value sectors which in turn will make the UK an attractive destination for inward investment.

Furthermore, it will help us better understand, measure, and forecast the considerable impact that Open Finance could have on society and to shape future policy.

In the UK, one of the key enablers of research and innovation in Open Finance is the Smart Data Foundry (formerly The Global Open Finance Centre of Excellence), which has been established in Edinburgh to support the understanding and development of the capabilities of Open Finance. It has a leadership role in enabling the necessary research and innovation, and building confidence in Open Finance across the UK, and can encourage research and innovation by providing a highly secure environment that can host Open Finance data. The Open Finance data priority in FinTech Scotland’s Research & Innovation Roadmap supports and complements The Smart Data Foundry’s agenda.

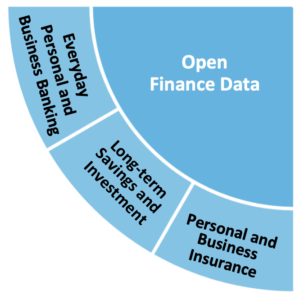

Priority areas in Open Finance data

When developing the Roadmap, analysis highlighted three industry priorities that will benefit from more focused research and innovation on this topic. They involve shaping the future of:

Everyday personal banking and business banking

- Insights through Open Banking data

- Future banking business models

Long-term savings and investment

- Financial resilience and wellbeing

- Future living & the ageing population

Personal and business insurance

- New data and insights for insurance

- Data privacy

- Data ethics and governance

Roadmap next steps: Open Finance data

A range of proposed next steps are laid out in the published report, which specifically identifies 22 actions relating to Open Finance, and categorises each into one of three phases over the next 10 years. These actions are illustrated in the graphic below. the report also references 23 different stakeholders who can support the implementation of these actions, which are broken down into research projects and innovation calls.

New business models in open finance to be analysed and judged.

Open Future World has launched a prestigious startup pitch competition to reveal some of the most interesting emerging business models in open banking and finance.

Six finalists will receive a complimentary ticket to the Open Banking World Congress in Marbella, Spain, on 24-25 May, where they will present their proposition to an all-star judging panel of industry experts, VCs and investors.

In addition, they will be interviewed on a live-streamed chat show to over 3000 viewers delegates from around the world attended. The winner will be announced at the evening party on the convention’s first day and will get to pitch on the keynote stage on day two of the conference.

“The last two years have been a hotbed for innovation in open finance. I come across so many impressive startups every week. Every one of them is harnessing open finance to transform the customer experience and make real improvements to our everyday lives.

The Open Banking World Congress will assemble leaders at the forefront of open finance from around the world into a dedicated setting over two days of keynotes, networking, discussions and collaborations. By bringing together new startups and seasoned open banking professionals, we hope to help enhance the potential of open finance and give promising startups the best chance of success.” says Marie Walker, Co-Founder of Open Future World.

To qualify for entry, startups must be in the open finance domain, be less than 3 years old and have received less than 3 million in investment.

Entries are open until 15th April with the 6 finalists to be announced on 22nd April.

To enter the free competition:

https://www.openbankingworldcongress.com/pages/startup-pitch-competition For all enquiries, please contact: georgina@openfuture.world

Open Future World

The leading source of information on progress in open banking and beyond. The Open Banking World Congress takes place in Marbella, Spain between 24-25 May.

https://www.openbankingworldcongress.com/

New partnerships to open finance for good

On the day it announces its new name, Smart Data Foundry, formerly the Global Open Finance Centre of Excellence, also shares the news it has joined forces with Equifax, Sage Group, Moneyhub and FreeAgent to support its mission to open finance for good.

The Smart Data Foundry was born our of a collaboration between the University of Edinburgh The Financial Data and Technology Association (FDATA) and FinTech Scotland.

The freshly rebranded company just completed a project with NatWest Group, The bank de-identified data from over a million householders to study the impact of the pandemic on household finances. All of the data was de-identified and analysed by accredited researchers in the security of the Smart Data Foundry Safe Haven, operated by the Edinburgh Parallel Computing Centre (EPCC) at the University of Edinburgh, a controlled and secure service environment for undertaking data research.

Insights from the NatWest data were shared with the UK Government at the start of 2021 and continue to be updated.

The Smart Data Foundry will now focus on understanding the impact of the pandemic on SMEs. Working with Scottish fintech FreeAgent, Equifax and with Sage, they will research the causes and impact of late and slow payments to small and medium sized businesses. The insights will be shared and continually updated with the UK Government as financial behaviour adapts to the pandemic environment.

Commenting on the announcement, Smart Data Foundry’s Chair, Dame Julia said:

“We have started a movement within the financial services sector which is gaining momentum at pace. Driven by our purpose to improve people’s lives, our new name, Smart Data Foundry, better reflects the challenges we face.

“Today’s announcement charts the significant progress Smart Data Foundry has made to date in securing partnerships with these significant organisations which will enable us to unlock the power of financial data that, up until now, was not available for public purpose or common good.

“It is important not to underestimate the work that has gone into getting to this stage which includes data governance agreements to protect privacy. This headway, and the success of the NatWest Group partnership, paves the way for many other partnerships as we strive to improve the lives of ordinary people and support the resilience of the SME sector.”

Dame Julia concludes:

“The science community has shown how important health data was to manage the pandemic. Our aim is to do the same for the economy by providing financial data. However, our collaboration will reach beyond Open Finance as we look at other significant challenges such as climate data and the transition to net-zero, addressing the Poverty Premium and supporting the intersection of finance and health.”

Simon McNamara, Group Chief Administrative Officer at NatWest said:

“The pandemic continues to be challenging for many, and the impact is unique for each customer, household and business. By sharing data with Smart Data Foundry, organisations can collaborate to create better insights for the good of our communities so that we can better support their recovery. We have a crucial role, guided by our purpose, to support our customers and communities to get back on their feet and thrive”

Roan Lavery, CEO and founder of FreeAgent said:

“Sticking up for microbusinesses is really important to us and so we’re proud that the insights from the data will help to shape public policy to support SMEs, sole traders and contractors. SMEs account for 50% of the UK’s output. Part of the success of this project is down to the very supportive data community here in Edinburgh and in other parts of Scotland.”