New Appointment for Growing Tax Specialists in Scotland

Access2Funding R&D Tax Specialists have announced the appointment of their new Regional Manager for the whole of Scotland, Suzy Carter. Suzy will be leading the team as they look to continue their impressive growth, with Research and Development technical claim writers and Business Development team in all four corners of the country.

2020 saw the launch of Access2Funding in Scotland, and since March last year Suzy, along with Taylor Franchetti and team, have achieved a return of over £3million for Scottish businesses, proving to be a lifeline for many through this trying financial time.

Heading into 2021, Suzy, whose finance background spans 25 years, is set to recover more hidden funds through the R&D tax credits scheme in a variety of sectors with her team, with plans to grow further in 2021.

Currently, the R&D specialists are recruiting for 14 vacancies throughout the company, along with announcing their appointment of Jemma Taylor as head of Alternative Products.

Access2Funding are looking to further support businesses through appropriate services and products and by garnering a valuable relationship with their clients.

Director and COO of the business Dawn Coker stated:

“We’re really proud to be supporting businesses across Scotland, and we are excited that Suzy has accepted the Regional Manager role. Together with her financial background, knowledge of R&D Tax Relief and her networks across the country, we are in the best position possible to assist even more growth in Scotland.”

As we navigate through another lockdown, Access2Funding are looking to help even more clients throughout the uncertainty. If your business has had to adapt as a result of the pandemic, or carry out development in products or processes, then a chat with one of their BDE’s is worthwhile.

Here is what Suzy’s client, Director Sandy Anderson of Edinburgh-based business Block 9 Architects, had to say:

“What a fantastic service! The Access2Funding team were outstanding, and we are due to receive way more than expected on our Research & Development claim. This is a huge help to the business in these times!”

This news comes alongside the announcement that Access2Funding returned over £23m to SMEs across the UK last year, and have more than doubled their national team since the start of 2020.

If you want to discuss R&D tax credits, Access2Funding are organising an event on the 4th of February at 5pm. You can register here.

0333 990 0125

Boosting FinTech innovation Across the UK

Proposals to grow fintech innovation opportunities and deliver positive economic outcomes throughout the UK

FinTech Scotland and FinTech Wales have released a report proposing increased Research and Innovation (R&I) to drive acceleration in fintech development across the UK, nationally and regionally to support growth and new jobs.

The report, entitled “Research and Innovation for UK FinTech” jointly authored by Gavin Powell and Johnny Mayo of FinTech Wales along with Nicola Anderson and Stephen Ingledew of FinTech Scotland sets out a number of key actions to build a longer-term Research & Innovation across the UK, including:

- Challenge led innovation programmes identified through collaborative national and regional exercises to develop ground-breaking propositions through a funded research pilot programme

- Mapping the longer term needs for FinTech R&I in partnership with established researchers to develop support through a long-term funding portfolio.

- The development of a FinTech Innovation Institute by collaboration of UK fintech regions to lead the steering and operation of a long-term funded portfolio.

- Regional fintech contributions that leverage the local strengths and connected networks to help drive economic growth and build greater resilience across the UK.

The proposed actions have been supported by contributions from experts across industry, regulators, research experts and academic organisations across the UK.

FinTech Scotland CEO Nicola Anderson said:

“We know from experience that fintech across the UK offers real potential for economic growth, future employment and greater financial inclusion.

“This paper proposes a suite of purposeful and collaborative actions that can achieve success through commitment and regional contributions. The paper is just the start and we’re looking forward to continuing this work with fellow fintech leadership colleagues and teams across the UK.”

Sarah Williams-Gardener FinTech Wales CEO said:

“This paper recommends a clear plan to secure a more prosperous future for FinTech through innovation and we need to act now to ensure that we can continue to grow in FinTech and not fall behind our international competitors.

“We must create an environment where opportunities to innovate ”“ and break through the crowd ”“ can be achieved. The importance to build back better post Covid19 is even more pressing. If we don’t commit to providing the right conditions now for our FinTech innovators, we will almost certainly lose out to our international competitors.”

Ian Campbell, then CEO of Innovate UK said:

“This paper demonstrates the imperative to act and to ensure the UK, as a whole, embraces Fintech innovation across the financial services sector and the broader economy; leveraging regional skills and expertise to execute a unified strategy and unleash the full potential of all nations and regions within the UK.”

Ron Kalifa OBE, and former CEO of Worldpay, who is leading the Governments fintech review said:

“We are delighted to see FinTech Scotland and FinTech Wales combining forces to propose a UK wide joined up approach to Fintech innovation. We all have a common goal to make UK Fintech resilient and prosperous on the global stage.”

Gerard Grech, founding chief executive of Tech Nation said:

“Fintech is a competitive strength for the UK and it’s terrific to see the regions looking to explore how a focus on innovation, and nationwide collaboration, can further increase UK fintech’s potential. This is exactly the kind of theme that the national connectivity stream I’m leading as part of the independent FinTech Strategic Review commissioned by the Treasury is seeking to build upon.”

“Undertaking this work has allowed us to create an independent perspective of innovation requirements and strategy. This is a much-needed tool for UK FinTech and action needs to be taken if we are to protect our position against growing competition from across the globe.“The need is ever more pressing as the world looks to innovate heavily in areas like FinTech to boost economic recover post Covid. This is about creating the right environment in the UK to generate plentiful opportunities and enable prosperity.”

In the summer of 2020, the complementary FinTech Strategic Review was launched and is expected to report its findings and recommendations to HM Treasury in Q1 of 2021.

You can download the long and summary versions below

Fintech Scotland, new norms, new fintechs

2020 ”“ Establishing New Norms

We’re starting to wind down and think about finishing up for a break over the festive period at FinTech Scotland and like so many of you and other organisations out there we’ve been reflecting on what a year!

2020 has felt like a year where we’ve lost what was normal. Like so many, we’ve been working from home since March ”“ our last day in the office was the 12th of March, forever etched in my memory! Since then, we’ve been getting used to a new norm’, new ways of working and phrases like you’re on mute’ have made it into our everyday working vocabulary.

Life moved online with technology and digital connectivity vital for new norms that were being established at work and school, for learning, shopping, social interaction and connection with family and friends!

We’ve been able to count our blessings in so many ways and continue to be privileged, inspired and energised by the FinTech Scotland Cluster.

Fintech driving New Norms’

The purpose and commitment to enable greater financial inclusion is a strength right across the fintech community in Scotland. The financial impact of COVID-19 on businesses and people has presented even more need to drive this agenda and Scotland’s fintech SME’s are providing a range of different products and services to help, enable and empower people.

Amiqus has progressed a collaborative initiative to ensure those facing homelessness and a loss of address can maintain access to vital services. @Proxy address, a new normal perhaps, is a solution that aims to overcome issues of financial exclusion because proof of identify to access products is closely tied to a permanent address. It’s an innovative approach that’s enabling new insights on old issues and focused on purposeful outcomes.

Empowering people by making personal finance more insightful and transparent, while using technology to see all your accounts in one place, is fast becoming a new norm and driven by fintech’s such as Money Dashboard. The team there were recently successful in the NESTA Rapid Recovery Challenge to help people financially hit by COVID-19. The award recognised both Money Dashboard’s innovation to help people manage money and its ability to quickly scale to support more people and a growing need.

New ways are also driving the team at Nude, who are working to enable aspiring first time buyers to build a deposit for their first home. The innovation aims to help people build that deposit quicker and is working to support new savings norms to empower people through data, behavioural insights and investments.

The team at Sonik Pocket have been innovating to help children with money. They’ve been focused on the potential new norm that generation Alpha will have less experience with physical cash and are building a product to help teach them about the value of money in a digital way. The inspiring team come from a teaching background and want to see children included and engaged with money and finances.

Float, working with SME’s, is integrating a range of activities to give businesses new tools to manage cashflow, accounts, and other business finance needs. Driving a new norm that helps business owners forecast accurate cashflow using real time information to get a visual view of ins and outs, pinch points and supporting confident business decisions.

There are many more fintech’s working and collaborating with industry partners, regulators, consumer organisations and universities to build the next phase of New Norms where technology in financial services supports inclusive outcomes for businesses and people.

New Fintech SME’s

The FinTech Scotland community of fintech SME’s has grown throughout 2020 and it’s a pleasure to welcome a host of new enterprises who are all aspiring to build and support other new norms and ways of working. Focused on cyber security Lupovis helps identify and divert cyber hackers away from crucial operating systems to keep businesses digitally safe, an increasingly vital need as we embrace new ways of digital working. Love Your Employees is focused on employee health and financial wellbeing, enabling employers to support colleagues through changing financial, emotional and other health needs.

In addition, an established norm continues to see international fintech’s join the FinTech Scotland community. Montoux, Access FinTech, UNest, all international fintech’s, have started to establish and build business in Scotland. All attracted to Scotland because of the strength of talent and data driven innovation expertise available here, and all working in different markets. Montoux, a New Zealand business is focused on the life and health insurance industry. AccessFintech from New York is using its innovation to help financial operating and risk models evolve, and UNest, a Californian business is focused on enabling people to save for university and education costs.

New Connections

The positive outcome of the new working from home norm has been the ability to broaden our reach and speak to more innovative fintech communities across the world. This opportunity to welcome global innovations and to learn from shared experiences continues to energise us. Mickael, our French Scot has been building new alliances with fintech hubs around the world. The FinTech Scotland festival reach worldwide audiences across the 70 virtual events held in September and we’re hoping to build on this experience for next year.

FinTech Scotland visited seven different countries virtually in 2020 and virtual events have brought about a new meaning to airmiles as we visited’ India, Australia, Hong Kong, Singapore, Europe and the US without leaving home. The ability to connect and learn from these experiences is wonderful as is the opportunity to profile Scotland’s fintech community at these international events.

New Year Ahead

Team FinTech Scotland are all hopeful for a healthier 2021 for all. We’re also looking forward to welcoming more fintech entrepreneurs into the FinTech Scotland community, through continued homegrown talent and through attracting international enterprises. We know Scotland will continue to inspire us through innovation, collaboration and inclusion, that there will be opportunities to continue to establish many more positive new norms and we’re ready to welcome all of that too.

Creating a Culture of Support in the Financial Services Industry

Pinsent Masons recently published a report Creating a Culture of Support in the Financial Services Industry’, produced in collaboration with a number of key stakeholders in the financial services industry, including financial institutions, fintechs and third sector organisations, to explore this important topic in more detail.

As part of the report, Pinsent Masons commissioned a consumer survey to obtain insight into the role individuals see their bank playing in helping to support them if they are affected by a mental health condition. Their findings show that consumers are very much in favour of banks taking a proactive approach in helping consumers to manage their money, for example by implementing spending controls or notifying the consumer if an abnormal spending pattern is identified.

One of the key areas of focus for the FCA is ensuring that consumers with mental health issues are treated fairly and the report looks at the FCA’s approach, the legal issues associated with banks and other financial services institutions being proactively involved in supporting consumers, what the industry is doing to support consumers with mental health issues and how the COVID-19 pandemic has increased the need for additional support to be offered to consumers.

Creating a Culture of Support in the Financial Services Industry’ highlights the positive steps already taken by the financial services industry to ensure that consumers with metal health issues have access to the support they need and shows that that there is a huge opportunity for collaboration between industry players to offer even better solutions for consumers in the future.

A copy of the report is available here.

In-depth fintech research and analysis with specialist MSc students

Article written by Ksenia Siedlecka, Financial Services and Fintech Sector Engagement Manager at Edinburgh Innovation

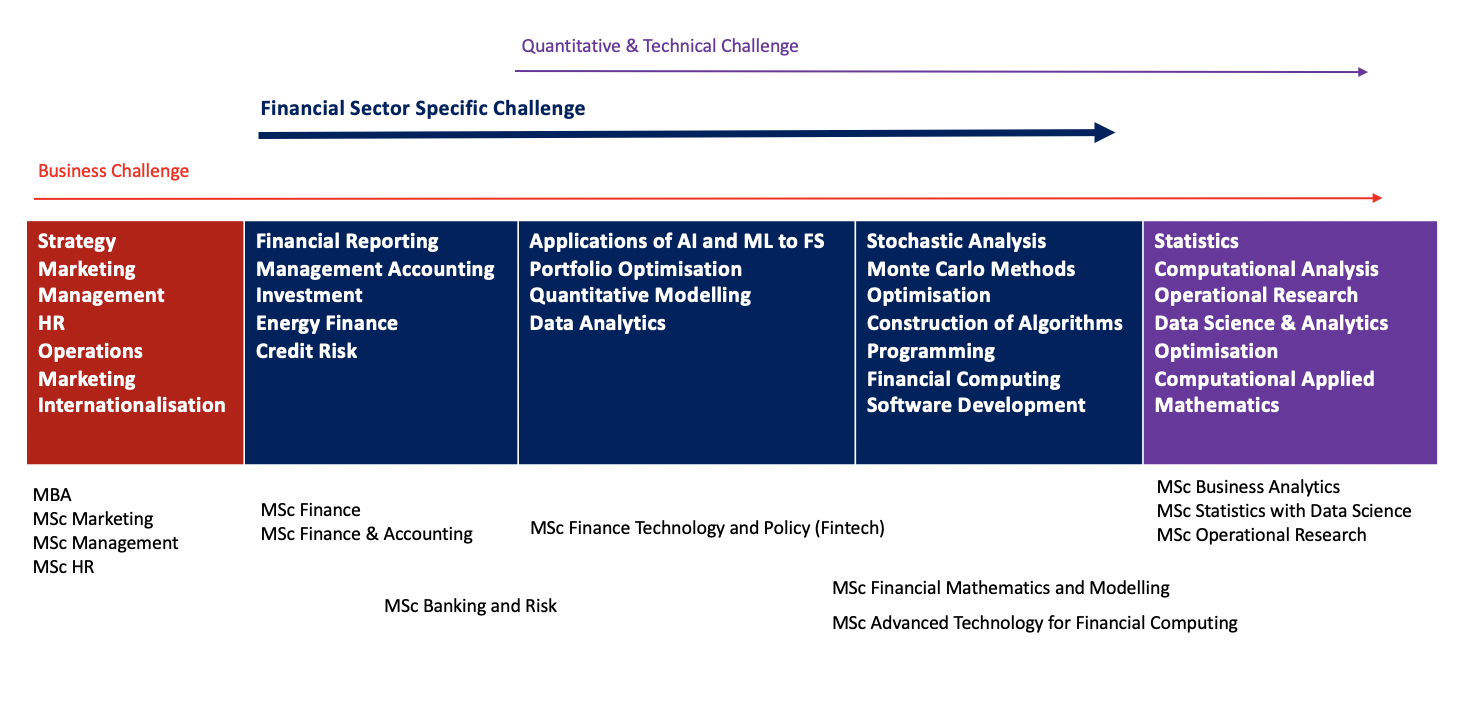

We are currently looking for projects for a variety of MSc programmes with finance and fintech focus (MSc Fintech ”“ Finance, Technology, Policy, MSc Banking and Risk, and MSc Finance, MSc Financial Mathematics). We also have a number of business and data science MSc programmes which are popular with Financial Services and Fintech companies looking to propose projects (e.g. Business Administration, Business Analytics, Statistics). With such a fantastic selection of programmes, we are able to tackle a variety of business challenges. Our students are among the best in their field and combine their specialist subject knowledge and management skills with the refinement offered through our 12-month, intensive programmes. Projects are delivered free of charge and supported by our world-leading academics at The University of Edinburgh. We offer different types of projects and will match you with an individual postgraduate student with the specialised skill set suited to your business challenge and research needs.

Our Business School students can help tackle questions related to corporate strategy, marketing, finance, internationalisation, product development, HR, operations management, change management and many others. The MSc in Finance programme covers all aspects of investment, corporate and energy finance. MSc Accounting and Finance could help with topics on financial reporting and management accounting. MSc Banking & Risk projects could cover such topics as analysis of corporate financial information, credit risk management, econometrics applications and many others. We can consider almost any topic that has a finance, accounting, investment, energy market, banking or risk focus. Successful projects tend to have an empirical element, which has practical relevance. Our students are keen to work with practitioners on projects which will be of real value to them, helping them find solutions to strategic financial issues such as validity forecasting, forecast asset market returns, risk modelling, dynamic lifecycle strategies etc.

MSc Financial Mathematics students will work on a real mathematical finance problem and can utilize specialist techniques such as stochastic analysis, Monte Carlo methods, statistics and optimisation, construction of algorithms and programming skills. Projects often require the design and implementation of computational analysis to a specific area, and can involve the application and implementation of existing mathematical models, or development of new approaches to solution methods. Quantitative modeling, data analytics, financial computing and software development projects can be tackled by our computer science students from MSc Advanced Technology for Financial Computing.

The MSc Finance, Technology and Policy (Fintech) prepares students with technical skills and knowledge of programming, artificial intelligence and machine learning who also understand financial markets and regulations so they are ready to develop technological solutions fit for the financial sector. We are particularly interested in dissertation topics in applications of artificial intelligence and machine learning, data analytics, and portfolio optimisation. Example topics include: building robo-advise algorithms using ML; pattern recognition in big data (including alternative data) using ML; optimal execution strategy with particular emphasis on trading securities in ratio, and many others. Can you help?

If so, we’re looking for companies to submit project ideas by approx. 25 January 2021. In return, you’ll benefit from the insight of one of our high-calibre postgraduate students, including a substantial report featuring extensive research, rigorous analysis and practical conclusions.

To discuss further, contact Ksenia Siedlecka, Financial Services and Fintech Sector Engagement Manager, ksenia.siedlecka@ei.ed.ac.uk

Inclusion, fintech and future talent

Inclusion drives fintech innovation

This has been an action-packed time for everyone involved in the FinTech Scotland Cluster. With COVID-19 continuing to have an impact on our lives both at work and at home the energy across the cluster continues to inspire us.

In particular there has been an even stronger focus on inclusion. Since I’ve known it, this topic has always been front of mind for all involved in the FinTech Scotland Cluster. The work over the recent weeks has continued to demonstrate the drive to build an inclusive environment that enables diversity to win, innovative environments to advance future opportunities for all and build business success.

Inclusion driving future talent

We’re continuing to learn about the full range of organisations across Scotland that are working in practical ways to build skills, experience and communities to help people from different backgrounds explore opportunities in FinTech and Tech. It’s always a pleasure to learn about the practical approaches being taken to support and enable inclusion.

Code your Future is strengthening its focus in Scotland. It works with people who have had limited access to education, offering practical tech training to anyone that’s experience problems in getting meaningful work. There are ten graduates on course to graduate in November, who will be looking for opportunities. Previous graduates are working at BBC Scotland and STV, and code your future has plans to support another class of 30 students next year.

We’ve also been working directly with the team Inlcusion Scotland over the past few weeks as we look to expand the FinTech Scotland team through an internship. Inclusion Scotland work to ensure the full inclusion of disabled people into all aspects of Scottish society can be achieved. All of us a FinTech Scotland very much looking forward to adding to the team.

Inclusion drives business development

It’s been great to see the hard work from the team Lloyds Banking Group pay off so successfully as they launched the Launch innovation lab. The innovation themes of digital services and ESG are another example of the conscious focus being given to the topic of inclusion. Congratulations to Inbest and Legado who are both participating in the programme.

Obashi also shared an exciting development this week as it joins the World Economic Forum’s innovators community. An inclusive first for this forum, for Obashi and for Scotland. Obashi’s work is another great example of inclusion driving business development, moving from the oil industry to share its experiences of dataflow frameworks to bring clarity to new sector.

Inclusion drives financial inclusion

Over the last few weeks we have continued to see the efforts of many across the FinTech Scotland Cluster continue their unwavering focus on financial inclusion.

Amiqus continues its work with proxy address and launched a new trial to test the proposition. It works to provide those in danger of losing their home and subsequently their address with a proxy address and the innovation has the potential to ensure people continue to get access to vital services including access to the benefits they need.

FinTech focus on financial inclusion has also been supporting the UK’s Money and Pension Service (MAPS) who has recently launched a UK Financial Wellbeing Strategy. Thank you to, Nude Visible Capital Soar Directid FastPAYE and Money Dashboard for sharing your views. We know there will be more on this over 2021 and that COVID-19 has brought the topic of financial inclusion into sharper view.

Pinsent Masons recent research on Creating a Culture of Support in Financial Services has focused on the topic of Money and Mental health. It draws on a range of perspectives from a wide and diverse group of industry participants and explores a range of initiatives being built to offer inclusive support for those that want it.

And on a final related note, this week has been Talk Money week, another initiative to encourage people to engage in money and to get us all talking about it. Experience shows that money continues to be a taboo subject and research has highlighted that often people find the subject to daunting and complex. FinTech’s such as Sonik pocket and Moneymatix are working to help children engage with money and financial decisions at an early age. A bit like those why’ questions our children are so good at asking, innovations like this might go some way to helping us all talk about money.

Hoping you all stay safe and well.

Nicola

How Fintech is Disrupting Customer Service

Technology has changed our way of life so rapidly that it’s hard to even call them “disruptions” any more. Indeed, today’s technological innovations are all about looking at our current way of life and seeing how else to improve it. This also means that technological innovations will play a big role in shaping our way of life post-COVID.

In particular, the World Economic Forum notes that fintech will play a key role in helping businesses recover from the effects of the pandemic. And while fintech’s role in helping businesses raise capital or invest their funds is clear, there’s also another key way that fintech can help accelerate business processes.

Fintech and customer service

Customer service is one of the biggest pillars of any business operation, and this holds especially true in today’s increasingly connected society. The average consumer is more discerning than ever, and it only takes one bad Tweet or Facebook post for word to quickly get out about your company.

As such, ramping up customer service practices will play a key role in ensuring that these goals are met. Digital adoption is already strong thanks to fintech innovations such as e-wallets and mobile investment apps, but customers still need to know how to properly manage their money. Providing accessible customer service options will therefore become a true marker for whether a bank is ready to succeed in 2021 and beyond.

How Fintech is Disrupting Customer Service in Different Industries

Banking

The Telegraph has recently called for an overhaul of the traditional banking business model in order to address rapidly shifting customer changes, particularly when it comes to value creation amongst consumers. This process can start by offering in-chat services within mobile applications; as it stands, many banking applications still rely on uploading phone numbers and emails onto their applications should customers need more assistance. Adopting in-app chats speeds this process up, but it also means that fintech companies themselves will have to adopt unified data systems that allow agents to get the information they need within a few clicks.

Supply chain

The speed information is shared is now the foundation of a successful supply chain. A post on staying productive in the new normal by Verizon Connect states that fast information sharing is a marker to customers that your business is constantly improving its services to meet their demands. The site also notes that the faster information is shared the more agile a company can be in responding to a customer’s needs. This allows companies on the supply chain to serve more customers faster. Logistics companies who rely on GPS tracking and management systems to give timely parcel updates are but one example of how this speedy information improves customer service.

Retail

Our previous post entitled ‘Card Issuing and Management: Staying Relevant Facing Ever Faster Changing Customer Expectations‘ shows that fintech companies have a huge role to play in paving the way for a stronger retail industry in the aftermath of Covid-19. Card issuing solutions are in line with the rise of alternative payments, whether through digital platforms or via online currencies. These developments prove that access to varied payment channels plays a big role in improving a business’ overall customer service.

Fintech disruptions are part and parcel of our new normal. Indeed, the impact of fintech on customer service across several industries proves just how pivotal these disruptions are when it comes to streamlining business operations while still keeping customers in the loop. Businesses are now looking to plan for post-pandemic business growth, and it looks like fintech solutions will be an essential tool to meet these goals.

FinTech and Translation Industries; Interesting Bedfellows

When one looks at the business challenges and technological advancements, shared by both FinTech and Translation Industries, alike, quite a few interesting synergies emerge, including:

- Both being enablers of global online client interactions

- Both enjoying unlimited client reach

- Both disrupting traditional workflows, via technological advancement

- Shared concerns regarding data security

Enablers

FinTech is one of the most rapidly expanding sectors in the world, revolutionising personal & business finance, via online banking and applications. FinTech has changed the finance game, forever, and has rendered traditional banking methods, extinct.

Whether it is, the exchange of foreign currency, the ability to trade in cryptocurrency, the ease of access to the world of investment, or making payments via mobile, the sheer scale of opportunity is remarkable.

The translation industry, of course, performs the translation & localisation of banking apps, websites, and communications that all enable global trade. New advances & developments in translation technology, have played their part in changing the entire client experience. This could be through automated translation as opposed to human translations, secure portals for the transfer of client files, API technology to connect client and supplier systems, or Online Editor facilities.

Unlimited Client and Workforce Reach

Online workflows & operations mean that, in both industries, there are no geographical barriers to having a global workforce or client base. Translation & localisation also ensure no limitations in the launching of new products to international audiences.

Accredited translation agencies have invested and incorporated the latest technologies within their workflows. Their skillset in managing complex localisation projects, ensures that the FinTech industry can quickly & effectively market their services globally.

Although FinTech communications can be handled seamlessly, accreditation is an altogether different story. One principal issue that FinTech faces when expanding, is navigating the relevant local regulation. With codices differing between, and even within, countries, the legal side of FinTech growth is far from simple.

Technology: Disrupting Traditional Ways of Working

FinTech and Translation companies can successfully operate without necessarily needing brick & mortar facilities. Of course, there are both advantages & disadvantages to fully-online-based organisations; for those with global operations, however, the advantages are manifold. For example, lower operational costs allow SMEs and Start-Ups to invest in personnel and the business itself, rather than being burdened with the heavy cost of facilities.

Although, being location-independent does present its own set of challenges. The puzzles of how to best: manage, motivate, or support staff effectively, for instance.

Data Security

Data security is essential in all industries and sectors; this is especially acute with respect to financial transactions and the security of client translation documents. Unfortunately, we are all too frequently confronted with news of ransomware cyber-attacks, against companies such as North Hydro and Travelex. That said, this threat is perennial to all industries and companies.

Most translation agencies enable clients to order & transfer files online, via a secure Client Portal’. For the most technologically advanced translation companies, the client files are not issued directly to external translators, as was done in the past.

This new workflow facilitates the translation of files directly within the online translation platform, accessed via the unique & secure portal. Maximum security for client IP, is thus, guaranteed.

A Conclusion

As little as five years ago, it was unimaginable to foresee such a rapid shift to mobile apps & online-only operations; it is fascinating to contemplate where we will be in five years’ time.

These technological developments are not only advancing services & capabilities within the industries themselves, but also other, more indirect, business benefits. These include: a global unlimited client base; online-only operations; physical office facilities becoming no longer necessary; or flexible working options.

All of this significantly lowers the barriers to entry for entrepreneurs in all industries internationally. It will be enthralling to see this continued evolution, and what lies ahead for all of us.

This blog was written by Fiona Feldermann McCrae, Managing Partner, at McFelder Translations.

McFelder Translations, an ISO accredited powerhouse with almost two decades of technical experience, is your passport to building a global brand.

If you’d like to find out more about localising your FinTech communications, email: fiona@mcfelder.com.

Website

LinkedIn

Twitter

Instagram

Image created using Canva

GLEIF and Open Future World Directory to enter partnership

The Global Legal Entity Identifier Foundation (GLEIF) and Open Future World have announced a new collaboration to help open finance organisations to work together.

This comes after the launch of the Open Future World Directory , the open finance organisation directory. Thank soo the addition of the Legal Entity Identifiers (LEIs) within the directory, it will be easier to identify who to connect to and do business with.

“The Legal Entity Identifier is a global standard for transparent and unique identification of legal entities. Users of the Open Future World Directory now benefit from quick and easy identification of the listed organization by linking to its validated and verified profile in the Global LEI Repository,”

Clare Rowley, GLEIF Head of Business Operations

“Whether you are talking about customers choosing to share their financial data, or financial institutions and fintechs working together, trust is a key theme in open banking and open finance. LEIs help enhance transparency by making it easier to know who you are dealing with.”

Nick Cabrera, Open Future World co-founder

Small business resilience and the evolution of ecommerce

The continuing shuttering of small businesses on high streets across the country is being accompanied by an unseen birth of new, exciting digital-only small businesses.

Periods of economic downturn typically result in a decline in new business registrations and at the beginning of the pandemic, it looked like UK SMBs were set to follow in this trend. For instance, statistics released by the ONS revealed that business creations slowed during April and May.

Despite this, Companies House figures reveal an overall increase in the number of new company incorporations in Q2 when compared to the previous year. This is indicative of a plethora of new business ventures inspired by our changing way of life.

Many of these emerging businesses are digital-first by necessity of the global lockdown they were born out of. Take for instance an independent hardware store which was already struggling prior to the pandemic. They may now find themselves in a position of renewed success, selling specific gardening tools via Shopify and Instagram marketing. While they may not have a strong credit history they do have a vast data footprint, owing to the numerous systems they rely on to run their business. Each data source, from their accounting package to their POS or ecommerce system provides a valuable yet siloed view of performance.

The shifting value exchange

However, the modern SMB expects systems and services to work together seamlessly and appears more willing to share their data in an open and automated fashion in order to ensure this. For instance, in September of this year, it was reported that the use of open banking had doubled in just nine months – an increase of one million users since January.

This increased appetite for interconnectivity between financial systems has opened the door to a much more collaborative, bespoke and diverse service between small businesses and their financial service providers. This is evidenced by the growing convergence of the POS, ecommerce and lending industries. Square Capital, Shopify Capital and Worldpay Working Capital are just some examples of funding facilities utilising transactional data to determine creditworthiness and offering finance at the point of need for small businesses.

Moving forward, customers who are willing to share their financial data digitally via accounting, ecommerce & POS package authorisation or open banking will likely benefit from a better service and more affordable products. For instance, lenders will be able to offer more favourable rates due to their enhanced ability to calculate risk and the notable reduction in the cost of serving these customers. The end result will be a shifting value exchange for small businesses whereby the benefits of sharing their data will become even more tangible than ever before.

The rise of ecommerce

The conditions of the global lockdown required existing businesses to pivot in order to remain viable. As a result, the period between April and July saw 85,000 UK businesses launch online stores or join online marketplaces. Many of these SMBs thrived during the pandemic as their adoption of ecommerce solutions coincided with a rapid increase in online sales, accelerating e-commerce growth by five years.

With the pandemic shifting the primary channel of trade online, gaining access to ecommerce and point of sale data is now crucial for financial service providers. The mutual benefits of doing so are multifaceted. For instance, commerce data can be used by lenders in particular to improve underwriting processes and credit decisioning. Small businesses will therefore benefit from a faster and fairer service which goes beyond traditional methods of credit scoring to consider their performance from multiple data sources in real-time.

This cultural shift towards enhanced digitisation and the growing importance of ecommerce will likely have a lasting impact on the way we think about the financial health of small businesses. In order to take advantage of this opportunity, financial service providers will need to replace siloed data with a connected ecosystem of unified financial data sources.

This article was written by Pete Lord, CEO and Co-Founder at Codat. Codat lets banks and fintechs plug into their small businesses and the software they use, giving them seamless access to real time customer data. Codat is building an ecosystem of connected datasets that handle the heavy lifting of integrations, leaving providers free to focus on improving their offerings for small businesses.

Photo by BedBible