How fintechs are driving financial inclusion

In this guest blog, Magdalena Krön, Rise Global FinTech Platform Director, Barclays Ventures, takes a look some of the work that the global fintech community is doing to address one of the biggest blights in society ”“ financial exclusion. This blog is based on the latest Rise FinTech Insights, a regular publication from Rise, created by Barclays.

One thing that COVID-19 teaches us, if we needed reminding, is how many people across the world remain disadvantaged by not having access to basic financial services. Although efforts to improve financial inclusion have come a long way in a relatively short period of time, there is still much more to achieve, especially for the 1.7 billion individuals who are currently unbanked(1). The work being done in the fintech space to address this issue, intended to open doors for individuals and families in a way that many of us take for granted, has seen entrepreneurs deploy everything from cryptocurrency to Open Banking and APIs in efforts to find new ways to support the financially vulnerable.

Chris Britt, Co-Founder and CEO of Chime ”“ a leader in the US challenger banking segment that offers internet-based, fee-free services ”“ says, “There is a huge segment of America that has a lot of anxiety around their money and day-to-day finances.” Helping them achieve “financial peace of mind”, he says, starts with providing a banking relationship that doesn’t rely on fees. “As many as 70% of Americans live paycheck to paycheck ”“ we offer free services such as early access to paychecks and overdraft protection.”

Innovative fintech thinking has come to the aid of another swathe of US society: the 2.5 million newcomers to the country on long-term visas who are, for the most part, unable to access credit. Collin Galster, Head of Business Development at Nova Credit, identified a solution to this problem facing the US’s foreign-born population, which is set to rise to 50 million by 2030. The company, a cross-border credit bureau, transfers individuals’ financial histories from one country to another, remedying the issue of lenders not being able to access enough financial information to feel comfortable lending, and therefore enabling immigrants to start funding their futures.

The need to tackle financial exclusion is felt even more acutely elsewhere. In India, for example, almost 11% of the adult population is unbanked. The report highlights a number of successful government initiatives, including Jan Dhan Yojana and Aadhaar Pay, that are spearheading more accessible paperless Know Your Customer (KYC) identification processes and biometric-based identity payment systems. This is a tactic that saw the number of people holding bank accounts increase by just over 50% between 2014 and 2017. Manish Khera, Founder and CEO of HAPPY ”“ a digital lending app targeting a multi-billion-dollar credit gap in India’s micro businesses ”“ emphasises how the internet now plays a vital role in facilitating and widening this access, citing the fact that India currently has 520 million mobile internet users.

Alternative banking solutions are springing up elsewhere, too. In east Africa, for example, Anisha Kothapa, Fintech Analyst at CB Insights, says cryptocurrency is being “adopted widely” ”“ offering a new way for the unbanked to save money and complete transactions without needing an account or credit card. One firm leading the way is Kenya’s BitPesa, a digital currency payments platform that “allows users to accept bitcoin payments, exchange bitcoin for local currency, and deposit bitcoin into accounts or mobile money wallets.”

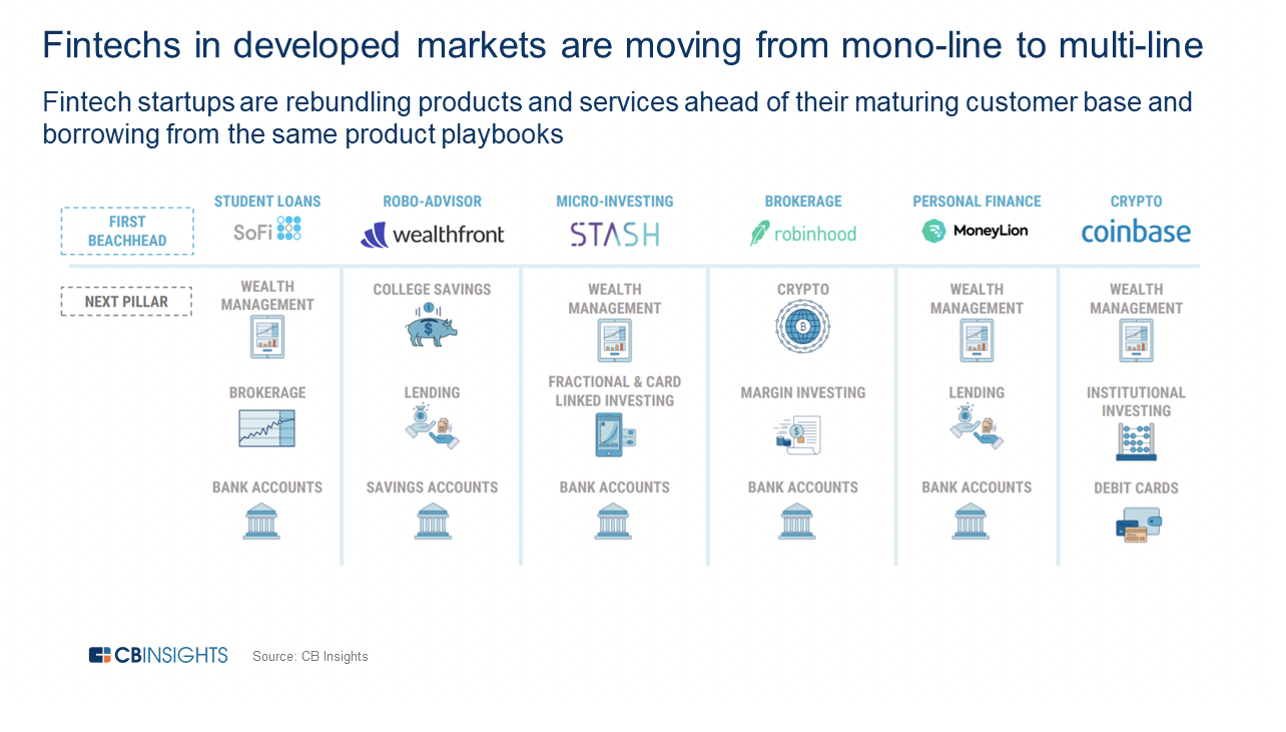

In contrast to developing countries, their developed counterparts are enabling financial inclusion differently by focusing on customer engagement and transforming the entire banking business model. FinTechs in developed markets are also moving from mono-line to multi-line offerings and re-bundling products and services to acquire more new customers.

It’s not just individuals that face financial exclusion, the report emphasises, but SMEs and budding entrepreneurs. According to Grant Bickwit, Associate at Barclays International, access to capital is one of the biggest challenges faced by entrepreneurs. It’s a sad truth, he explains, “that both entrepreneurs and investors are still reliant on individual networks and legacy processes for sourcing opportunities, entrenching geographic and social limitations”. In response to this, online platforms like OnDeck and Kabbage, launched in 2006 and 2009 respectively, offered firms access to credit digitally ”“ a trend that has proliferated.

Rise innovators have been responding to some of the other unique issues brought about by the pandemic, from employment to supply chain management. Rise Mumbai members, MMS.IND and GeoSpoc ”“ experts in geospatial information systems, platform-building, and consumer and micro-market data ”“ have joined forces to develop a COVID-19 impact tool which provides insights into how the pandemic is affecting consumers ”“ and enables businesses to better predict demand and ensure supply chain optimisation. Meanwhile, over at Rise New York, Brainceek, a workforce simulation company, has been helping corporates design virtual summer internship curriculums, providing extra support for the hundreds of thousands of graduates entering a difficult job market.

Addressing financial exclusion is a huge task, but one that is achievable, particularly with targeted collaboration across banks, technology companies and fintechs and a focus on achieving financial inclusion for those 1.7 billion individuals.

Download all editions of Rise FinTech Insights here.

(1) https://www.worldbank.org/en/topic/financialinclusion/overview

What is on this page:

Related content

How Agentic AI can redefine Financial Services

Mind the Gap: Bridging the UK’s pension divide with digital solutions