Forging the Future of Financial Services: TSB Spotlight Innovation in Open Banking

Three fintech innovators, Sikoia, Credit Canary and Aperidata, have been named winners of the 2024 TSB Innovation Labs programme, a partnership between TSB and FinTech Scotland. This is a collaborative effort to shape the future of financial services through responsible use of data and technology.

Now in its fourth year, the Innovation Labs programme offers early-stage fintech firms a platform to explore real-world applications of their technology. With access to expert mentorship at TSB’s Technology Hub in Edinburgh, the cohort has worked over the last year to develop propositions that aim to improve customer experiences across banking.

The focus of this year’s winners is very much Open Banking technology to simplifies and accelerates customer support.

Sikoia is working to streamline finance applications, potentially reducing barriers for new customers. Meanwhile, Credit Canary and Aperidata are exploring solutions to improve credit scoring and accelerate lending decisions. All three firms will now develop proof of concepts in partnership with TSB, testing how their solutions might translate into practical improvements for customers.

The TSB Labs programme has previously seen success with fintechs such as Lightning Reach, which helps users access benefits and financial support through a single portal. Since its implementation, TSB customers have accessed over £160,000 (£500 per customer) in grants. Another alumnus, ApTap, has supported customers in saving more than £65,000 (£150 per customer) on broadband bills by helping them switch to better deals.

Speaking on the latest announcement, Nicola Anderson, CEO at FinTech Scotland, said:

“We are delighted to witness the success of Sikoia, Credit Canary and Aperidata through the TSB Labs programme. These innovative fintech companies show how data and AI can be harnessed to deliver real impact for people and communities. At FinTech Scotland, we believe meaningful collaborations are the key to unlocking innovation and this partnership with TSB demonstrates the powerful outcomes that can be achieved when new innovative firms and progressive established companies work together to shape the future of financial services.”

Adam Betteridge, FinTech & Open Banking Lead at TSB said:

“We are incredibly proud of the progress made by these three innovative fintechs during the TSB Labs programme. Over the last 12 months, Sikoia, Credit Canary and Aperidata have demonstrated exceptional potential to help TSB customers get support more quickly. Their innovative solutions use data and technology in new creative ways to help provide an even better experience for TSB customers. We’re looking forward to what comes next.”

The programme reflects wider themes highlighted in the FinTech Research & Innovation Roadmap 2022–2031, developed by FinTech Scotland. Central to that vision is the role of Open Finance and collaborative innovation in addressing societal, economic and environmental needs. The roadmap points to a future where fintech drives financial inclusion, better consumer outcomes and a more sustainable economy.

SensFish

Sword Group Expands Cybersecurity and AI Capabilities with Acquisition of Edinburgh-based iDelta

Sword Group, a FinTech Scotland’s strategic partners, has announced its acquisition of Edinburgh-based fintech iDelta Ltd, a specialist firm focused on customised data solutions, cybersecurity monitoring, AI automation, and fraud analytics.

Founded in Scotland’s thriving tech ecosystem, iDelta has developed a strong reputation for its bespoke solutions in infrastructure and application monitoring, particularly within financial services. Its specialist consultants have created innovative tools for managing Open Banking data APIs and have developed extensions available on the popular Splunk marketplace. These solutions streamline the integration process with third-party technologies, enabling customers to effectively harness their data assets.

Kevin Moreton, CEO of Sword UK, described the move as a strategic step towards enhancing Sword’s capabilities in cybersecurity and artificial intelligence, particularly within the financial services sector.

“We’re pleased to welcome iDelta into Sword Group. This acquisition is well-aligned with our strategic vision for 2028 and significantly strengthens our cybersecurity strategy. Combining our expertise will enable us to deliver even greater value to our customers,” Moreton said.

Stuart Robertson from iDelta also welcomed the acquisition, noting the shared commitment between both companies towards innovation and technical excellence.

“Joining Sword opens exciting new opportunities for growth and collaboration. Our strong partnerships with Splunk and Cisco, combined with Sword’s extensive resources, mean we’re perfectly positioned to expand our offerings and accelerate our capabilities,” Robertson said.

Sword Group, known for providing business technology solutions across energy, public, commercial, and financial sectors, currently employs over 600 staff across its UK locations, including Aberdeen, Glasgow, Teesside, and London.

The acquisition underlines Sword Group’s strategic approach to bolstering its technical expertise in critical domains like cybersecurity and AI, reflecting broader industry trends towards greater digital resilience and smarter data utilisation.

The Future of Financial Advice: Consumer Expectations for 2025 and Beyond

The Financial Advice Consumer Survey 2025, conducted by Scottish fintech Aveni in collaboration with YouGov, highlights key trends shaping the future of financial advice in the UK.

With rising concerns about financial security, regulatory demands for enhanced consumer protection, and the increasing role of artificial intelligence (AI) in financial services, this report highlights the areas where financial firms must innovate to stay ahead.

There full survey can be found here.

Key Findings from the Survey

Consumers Demand More Personalised and Accessible Advice

A growing number of consumers expect financial advice to be tailored to their specific needs rather than generic recommendations. According to the survey, many individuals feel underserved by traditional financial advisory models and are looking for more dynamic, AI-driven solutions that provide real-time insights.

Trust in Financial Advice is at a Crossroads

Trust remains a critical issue in financial services. While robo-advisors and digital platforms are gaining traction, many consumers still prefer human interaction for major financial decisions. (42% of respondents expressed concerns about receiving financial advice solely from AI-powered tools).

AI and Automation are Reshaping Financial Advice

AI is playing a larger role in financial planning, from analysing spending habits to recommending investment strategies. However, consumers have mixed feelings about relying solely on AI-driven solutions.

Regulation and Consumer Protection are Driving Change

As regulatory bodies push for greater consumer protection, financial firms must adapt to new compliance standards. The Consumer Duty Act, for example, is set to reshape how firms engage with customers, ensuring fairer outcomes and more transparent advice. (72% of respondents stated they want clearer explanations of financial products and risks).

Rising Financial Anxiety and the Need for Proactive Guidance

Economic uncertainty, inflation, and concerns about long-term financial stability are leading consumers to seek proactivefinancial guidance rather than reactive advice.

What Does This Mean for Financial Firms?

The findings highlight several key takeaways for financial firms and advisors:

- Embrace AI-powered financial tools while maintaining a human-centric approach.

- Increase transparency around fees, data usage, and product recommendations.

- Develop digital-first advisory models that cater to on-demand financial guidance.

- Improve consumer education to enhance engagement and financial confidence.

- Stay ahead of regulation by prioritising customer outcomes and compliance.

Read the full report here.

Funding Boost for Smart Data Foundry

Edinburgh-based Smart Data Foundry (SDF) secures £3 million in funding to launch a new Financial Data Service. This initiative, funded by Smart Data Research UK, part of UK Research and Innovation (UKRI), will provide researchers with unparalleled access to secure, de-identified financial data, helping to paint a clearer picture of the UK’s economic resilience and household financial health.

This new service will form part of a national network of six data services aimed at positioning the UK at the forefront of smart data research. By enabling access to financial behaviour data from households and businesses, SDF will empower researchers to tackle pressing societal challenges, such as the cost-of-living crisis, financial inclusion, and regional productivity disparities.

Transforming Research with Secure Financial Data

Dougie Robb, Interim CEO of SDF said:

“This initiative fosters data-sharing partnerships that unite academia, public institutions, and private enterprises to deliver outcomes that improve lives across the UK.”

SDF has already gained national recognition for its innovative use of anonymised financial data for public good, including partnerships with NatWest Group to analyse financial behaviours during the COVID-19 pandemic and collaborations with Sage and CEBR on SME economic tracking.

A Network Driving National Innovation

The Financial Data Service is one of two newly funded services, alongside the Smart Energy Data Service, joining four existing services dedicated to imagery, geographic data, sustainable places, and data donations. Together, this network will accelerate the UK’s position as a leader in data-driven solutions, guided by the Economic and Social Research Council (ESRC).

Stian Westlake, Executive Chair of the ESRC, emphasises the importance of this investment:

“Data infrastructure is as critical to our shared prosperity as transport or power networks. With this investment, we are paving the way for economic growth, improved public services, and a sustainable future.”

From Insights to Actionable Impact

The Financial Data Service will bridge the gap between financial institutions, researchers, and policymakers to tackle real-world challenges. Its findings will inform targeted policy responses to economic shocks, support innovation in financial inclusion, and enhance understanding of how communities experience financial change.

Magdalena Getler, Head of Academic Engagement at SDF, remarks,

“With the anticipated Data (Use and Access) Bill, we are entering a new age of empowered, secure data use. This legislation will enable transformative research that tackles societal challenges, from poverty to economic inactivity.”

Lloyds Banking Group Partners with Scottish FinTech Inbest to Launch New Benefits Calculator

Lloyds Banking Group has partnered with Scottish fintech Inbest to launch a new tool aimed at helping millions of UK households access unclaimed benefits. The benefits calculator, now available in the Lloyds mobile banking app, is designed to bridge the gap between people and the £23 billion of unclaimed benefits such as Universal Credit and council tax support.

How It Works

The calculator is simple and intuitive. Users start by answering six quick questions about their household, income, and living situation. Based on this initial input, the tool provides an estimate of potential benefits they might be entitled to. For a more detailed analysis, users can complete a five-minute questionnaire to receive a final summary of their benefits eligibility.

If eligible, the calculator doesn’t just stop at telling users what they might claim; it also provides direct links to begin the application process. Additionally, the tool highlights potential grants for home improvements or energy efficiency upgrades.

Tackling a National Problem

Lloyds Banking Group’s initiative is a direct response to the estimated eight million UK households missing out on financial support. With the cost-of-living crisis intensifying, the “More Money in Your Pocket” hub in the Lloyds app aims to provide tangible assistance to those who need it most.

Since its soft launch, the benefits calculator has already helped thousands of users identify new sources of financial support. The tool is available on both iOS and Android devices, ensuring broad accessibility for Lloyds customers.

A Collaboration for Impact

This innovative solution was developed in partnership with Inbest, a leading Scottish fintech specialising in financial inclusion technology. Inbest’s expertise in building user-friendly tools to simplify financial complexity was instrumental in creating the benefits calculator.

FinTech Scotland, which supports collaborations like this, continues to highlight the power of partnerships between established financial institutions and fintech innovators. By joining forces, Lloyds Banking Group and Inbest are leveraging technology to deliver impactful financial solutions for everyday consumers.

“We’ve launched Benefit Calculator, helping customers to identify the benefits they may be eligible for and providing clear guidance on making a claim.”

This partnership with Inbest is a testament to the growing importance of fintech collaborations in addressing societal challenges. By combining Lloyds’ reach and resources with Inbest’s innovative capabilities, this initiative marks a significant step towards greater financial inclusion across the UK.

Open Finance and Carbon Neutral Banking

Recent industry insights show that banks still face significant constraints in measuring indirect Green House Gas (GHG) emissions owing to data limitations and a lack of harmonised methodologies.

At the same time, banks and other financial institutions hold large volumes of consumer data that can be leveraged to estimate GHG emissions albeit financial transaction data are privately owned with restricted access. This paper discusses how an open finance framework can be used to aggregate consumer transaction data across multiple financial products to compute carbon footprints.

It highlights a step-by-step approach to carbon footprint estimation and discusses the consideration for using microdata for emission computation.

Open Finance – What’s next?

Season 4, episode 10

Listen to the full episode here.

Open Finance is set to unlock a new level of transparency, accessibility, and control for consumers, businesses, and financial institutions. But what does this mean for the future of the financial ecosystem, and how will key players navigate the opportunities and challenges that come with it? We discuss what Open Finance really means, the progress made so far, and what the future holds for consumers, fintechs, and traditional banks alike.

Guests:

Ezechi Britton – CEO at the Centre for Finance, Innovation and Technology (CFIT)

Jen Lothian – Founder at MyArk

Space-Comm Expo Scotland 2024: How Can Fintech and SpaceTech Come Together?

The inaugural Space-Comm Expo Scotland will be the largest space industry event ever held in Scotland and will take place at the SEC Glasgow from September 11-12, 2024. Hosted by Will Whitehorn, the former President of Virgin Galactic and current Chancellor of Edinburgh Napier University, this event promises a fantastic lineup of keynote speakers from various sectors, including government, aerospace, defence, and academia. Among the speakers, Nicola Anderson, CEO of FinTech Scotland, will offer her reflection on the growing intersection between space technology and financial technology.

A Showcase of Scotland’s Space Industry Prowess

Space-Comm Expo Scotland is set to shine a spotlight on the nation’s dynamic space sector, which has become one of the fastest-growing in Europe. With over 150 space companies and 80 aerospace companies, Scotland supports nearly one-fifth of all UK space sector jobs and builds more small satellites than anywhere else in the world, second only to California. The event will feature more than 100 exhibitors and is expected to attract over 3,000 attendees, including representatives from government, industry clusters, academia, and commercial enterprises.

Keynote Speakers and Industry Leaders

The Expo’s impressive roster of speakers includes notable figures such as Dr. Paul Bate, CEO of the UK Space Agency; David Parker, Space Exploration Director at the European Space Agency; and Professor Malcolm Macdonald, Chair of Applied Space Technology at the University of Strathclyde. The opening address will be delivered by the Lord Provost of Glasgow City Council, Jacqueline McLaren.

Nicola Anderson’s presence is particularly noteworthy for the fintech cluster. As CEO of FinTech Scotland, Anderson has been driving innovation and collaboration within Scotland’s financial technology sector. Her participation shows the critical role fintech plays in supporting and enhancing space technology ventures. A previous initiative between FinTech Scotland and Space Scotland highlighted how data from satellites can be used to enhance propositions in the financial sector such as supply chain management, measuring carbon impact of various assets or better handling of insurance claim management to name a few.

Exploring the New Commercial Space Age

The speaker programme at Space-Comm Expo Scotland will cover a wide range of topics, including spaceports, launch capabilities, satellite manufacturing, downstream data, AI, cyber security, space law, investment, skills development, and space sustainability. These discussions come at a pivotal time in the commercial space age, highlighting both the opportunities and challenges the industry faces.

Anticipated Outcomes and Collaborations

Kevin Scullion, International Trade Specialist at Scottish Enterprise, expressed high hopes for the event, anticipating further collaboration between Scottish, UK, and international partners. The Expo is expected to foster discussions on trade opportunities and strengthen ties within the global space community.

Supported by key organisations such as the UK Space Agency, Scottish Enterprise, and FinTech Scotland, the Space-Comm Expo Scotland will be an unmissable event for anyone involved or interested in the space industry. With a world-class programme of content, product demonstrations, panel sessions, and 1-2-1 networking opportunities, it offers a comprehensive platform for knowledge exchange and business development.

Space-Comm Expo Scotland will be held from September 11-12, 2024, at the SEC in Glasgow. Registration is free, and those interested in attending can sign up at space-comm-scotland.co.uk. For information on exhibiting, email spacecomm@hubexhibitions.co.uk.

EY Launches First Scottish Fintech Lab with Space Agency Partnership

EY has launched its first Scottish fintech lab in Edinburgh. The innovative space is designed to foster collaboration, experimentation, and rapid prototyping among start-up and scale-up companies in the fintech sector.

Purpose and Vision

The Edinburgh fintech lab brings together fintechs, investors, clients, regulators, and other partners, the lab will facilitate the development of real-world solutions that enhance market and customer service. The focus will be on creating innovative solutions to key financial challenges, particularly in sustainable finance.

First Cohort and Space Collaboration

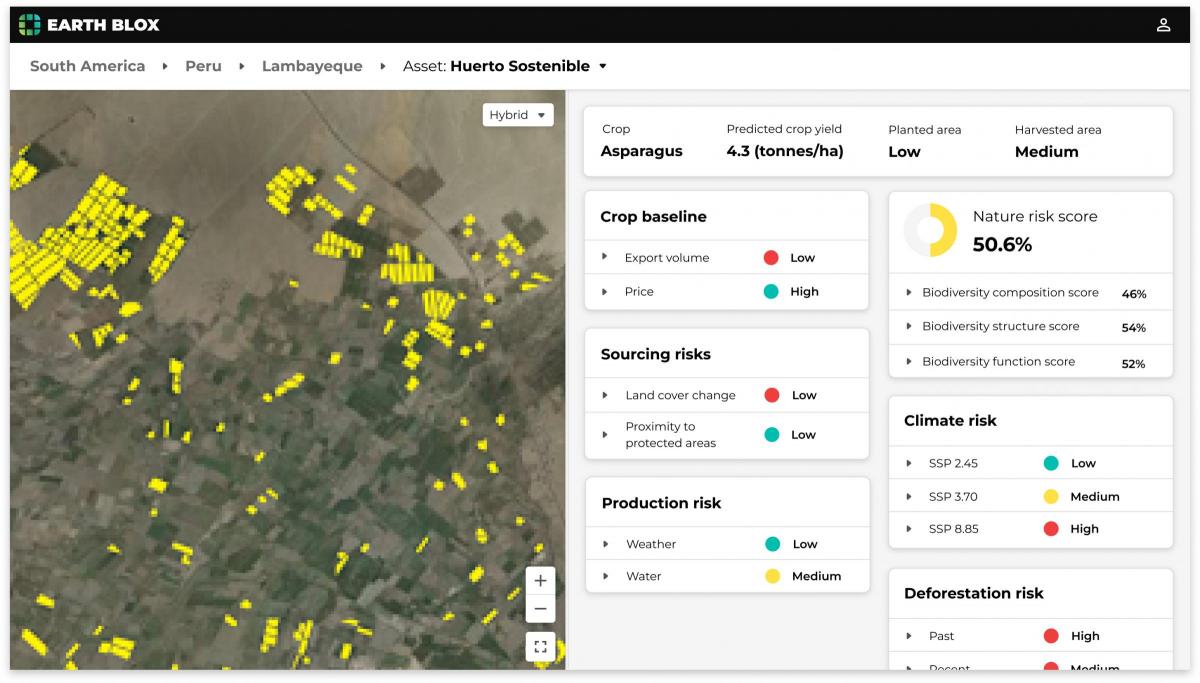

The lab’s first cohort explored the intersection of space science data and finance. In partnership with FinTech Scotland, Space Scotland, and supported by the UK Space Agency (UKSA), the program aims to deepen the understanding between financial services and the space industry. A notable project by Environment Systems and Earth Blox utilised spatial data to optimise agricultural commodity production while ensuring compliance with environmental regulations.

Leadership Insights

Sue Dawe, EY Scotland’s financial services managing partner, highlighted the importance of sustainable finance and the lab’s role in fostering innovation within Scotland’s fintech sector. Nicola Anderson, CEO of FinTech Scotland, and Hina Khan, Executive Director of Space Scotland, emphasised the collaborative efforts to drive positive economic and social change.

For more information, visit EY Fintech Lab.