UK Fintech Week special – a chat on synthetic data with Smart Data Foundry

Season 3, episode 6

Listen to the full episode here.

In this special episode with speak with David Tracy, Head of Data Science, at Smart Data Foundry on the week they presented their new Aisle proposition at Innovate Finance Global Summit.

What is synthetic data is? How is it different from real-world data?

We’ll explore how it will speed up innovation and collaboration in the fintech world, what the risks and benefits are and much more.

David will also speak to us about the work they’ve done with the FCA and the PSR to tackle APP fraud using Agent Based Simulation.

Fintechs DirectID and Faciit partner to make accessing credit easier

DirectID, the global credit and risk platform for risk managers, has announced a partnership with Faciit, an alternative lending solution for individuals without a UK credit history. This partnership utilises DirectID’s open banking insights to assist people with new-to-country status in accessing affordable credit.

Faciit’s save-to-borrow solution operates by requiring users to save one-third of their loan requirements for a minimum of three months. Following this, Faciit provides the remaining two-thirds as competitive loans. Faciit distinguishes itself from traditional lenders by not relying solely on bureau data to make credit decisions. Instead, the company employs DirectID’s income verification, using open banking data to determine whether an individual can afford to repay the loan.

James Varga, CEO & Founder of DirectID, said:

We’re delighted to partner with Faciit to help new-to-country individuals access affordable credit using DirectID’s open banking-powered insights. The partnership is perfectly placed alongside our mission to promote financial inclusion and responsible lending practices. By using open banking, we can enable better access to financial services for everyone, regardless of their credit history or financial status.

The partnership between DirectID and Faciit is rooted in their shared mission to promote financial inclusion. Faciit aims to provide new-to-country status individuals with the loans they need to achieve their financial goals, while DirectID believes everyone should have access to the financial services they need.

Olaolu Olaleye, CEO & Founder of Faciit said:

Our name Faciit means we facilitate it, and it sums up our mission to help create financial possibilities for those who will struggle otherwise. We are excited to partner with DirectID to deliver our complimentary missions of enabling financial inclusion.

ZavFit

New solution for Pensions Dashboards onboarding

A consortium of four leading technology providers has joined forces to offer a comprehensive end-to-end solution for pension providers seeking to integrate into the UK pensions dashboards ecosystem.

The collaboration between Target Professional Services, mypensionID, Bravura, and Delta Financial Systems is designed to simplify the complex processes and regulatory requirements that providers face when connecting to the ecosystem.

Each firm specialises in a particular area of expertise to ensure a seamless journey toward dashboard readiness before the staging deadline. Target Professional Services uses its leading tracing capabilities to screen and cleanse member data while mypensionID verifies and traces individual members using a verification app tailored to the pensions industry.

Bravura and Delta then provide a jointly developed cloud-hosted Integrated Service Provider (ISP) solution for providers’ data, with a focus on configurability and compliance with the Pensions Dashboards Programme’s (PDP) Code of Connection. The four firms’ technical expertise and market knowledge combine to create a unique solution capable of addressing pensions providers’ urgent and specific needs.

Jonathan Hawkins, Principal Consultant & Pensions Specialist at Bravura, said:

“Delta, mypensionID and Target’s deep expertise and technical know-how in the pensions and data sectors, combined with our ability to process huge volumes of assets and trades on our systems, brings a level of reliability and scalability that pensions providers require right now.

“Pensions dashboards are a crucial step towards modernising and digitising the UK’s pensions sector and, with the clock ticking, pensions providers up and down the country need tech partners with proven scale and expertise. This unique collaboration delivers that solution.”

Photo by Andrea Piacquadio: https://www.pexels.com/photo/young-woman-helping-senior-man-with-payment-on-internet-using-laptop-3823488/

Inbest and MaPS launch New benefits calculator

In collaboration with Scottish fintech firm Inbest, the Money and Pensions Service (MaPS) has introduced a benefits calculator.

The tool, which is free of charge, will be integrated into the MoneyHelper website of MaPS to assist individuals in determining the benefits and social tariffs for which they may be eligible.

Entitledto.co.uk claims that there may be billions of pounds in unclaimed benefits across the United Kingdom. By entering their basic information, users will be able to conduct a quick search and receive results in less than a minute.

The calculator will then request that they complete a more detailed search to verify their eligibility for any potential claims. MaPS emphasizes the importance of identifying other sources of income and any available assistance to help individuals manage their money and pensions, given the rising cost of living.

This initiative was launched after MaPS launched a new campaign in the previous month to increase awareness of the free help and advice available.

Michael Royce, Senior Policy and Propositions Manager at the Money and Pensions Service, said:

“The most common reasons why so much goes unclaimed in benefits is that people are unaware of what they’re entitled to or assume that they aren’t eligible.

“We look forward to working closely with Inbest and hope that making their benefits calculator available through our MoneyHelper website helps millions of households who are currently missing out to maximise their income.”

Manu Peleteiro, founder and CEO at Inbest, said:

“We are thrilled to partner with MaPS and power their MoneyHelper benefits calculator. Working with MaPS colleagues is a fantastic learning experience, and their input is crucial to continuously improve our calculator and shape our product roadmap.

“We are looking forward to working with MaPS and contributing to the delivery of the UK’s Strategy for Financial Wellbeing by helping people access the benefits, grants and social tariffs they are eligible for.”

€9m Investment by Ingka into Scottish fintech DirectID

DirectID, one of the leading fintech in Scotland, that specialises in credit risk assessment, risk analytics and predictive modelling, has announced that it has received a minority investment of €9m from Ingka Investments, the investment division of Ingka Group.

DirectID’s main objective is to promote financial inclusion worldwide through its global credit risk score, by providing advanced data to optimise credit and risk decisions in an increasing number of countries. The company provides risk managers with a real-time dataset that can drive efficiency, improve decisions and lifetime value across the credit lifecycle. DirectID’s insights enable decision makers to assess risk better, regardless of age, location, and past credit performance.

James Varga, CEOand Founder of DirectID, said:

“We’re proud to join Ingka Investments’ portfolio of market-leading firms. We are excited to be shaping a new global standard in credit scoring that enhances people’s lives by enabling access to products they need in an affordable way. Our coverage, advanced insights and predictive models provide a unique opportunity to achieve this by creating the world’s first real-time, inclusive, credit score based on open finance data.”

The funding received will help expedite the launch of DirectID’s most advanced predictive models for credit and risk, built from open banking data. Additionally, the company plans to expand its credit risk offering into new markets and accelerate the development of models for each stage of the credit lifecycle, from originations through portfolio management to collections.

Peter van der Poel, Managing Director of Ingka Investments, said:

“We are pleased to have made this investment in DirectID and are confident of their continued growth in the open banking market. They have developed an innovative solution with the potential to complement and disrupt the traditional credit and risk market and help drive financial inclusion for more people. Open Banking-enabled credit and risk insights is an area we believe can add value to Ingka’s financial services proposition in the future.”

This investment is just the latest in a series of investments made by Ingka Investments, which aims to strengthen Ingka Group’s core retail business by investing in innovative companies in areas such as digitalisation, customer fulfilment, fintech and sustainability. These investments support the ongoing transformation of Ingka Group to become more affordable, accessible, and sustainable.

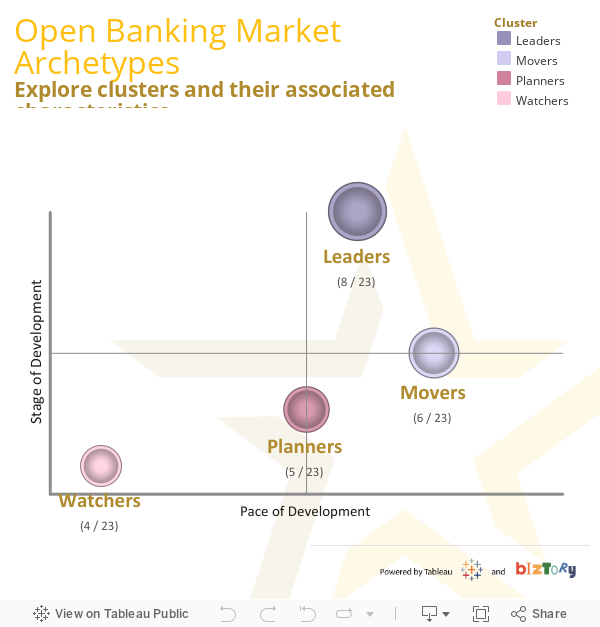

Open Banking – the UK’s next biggest export?

According to Accenture, there’s $416bn of revenue at stake for fintechs and banks across the world by the end of this decade. That’s roughly four times the size of the scotch whisky market ($91bn) – so is Open Banking the UK’s next iconic export? Maybe”¦ but only if we make some important changes

Last week, we released a piece of research – The Global Open Finance Index. It tracks the development of Open Banking across the world and focuses on the 23 countries where we’re seeing the most progress. Its findings are fairly stark. The UK’s position as a leader in the space, which was once completely uncontested, is now in serious danger of evaporating.

Countries like Brazil and Australia are accelerating with regulatory regimes that already go far beyond the UK’s initial blueprint whilst markets like India and the US are finding different approaches leveraging market forces and industry collaboration to create huge potential. India’s Open Banking standard now covers a group of more than 1 billion accounts whilst in the US 42 million accounts have coalesced under the FDX standard with zero regulatory push. Perhaps even more significantly, that regulatory push is coming in the US and soon. The Consumer Federal Protection Bureau (CFPB) is already in the late stages of consultation on how that process should be rolled out and they have the legislative backing to get it done.

So where does this leave UK fintechs?

I have no doubt that Open Banking and (eventually) Open Finance will have profound impact on the UK, revolutionising our credit market, bringing huge, excluded groups into mainstream finance and providing differentiated competition to the card rails, but in terms of the economics, the real prize is still on the table.

UK firms have built businesses that are designed to handle large quantities of API-driven transaction data. They’ve developed the security systems to protect the data, the skills to handle, clean and contextualise it and the case studies to prove how impactful that data can be. They are, in short, in a position of huge competitive advantage vs companies at the beginning of this journey in evolving markets. In order to maintain that advantage though, they have to keep working at the cutting edge of the technology, here the UK is falling down.

Australian firms are already working with Open Energy data, Brazilians are getting to grips with the wider financial product set through their country’s Open Finance programme.

We have to accelerate progress in the UK and the opportunity to do that is here.

On the public policy side, we need to establish a strong, independent body to preside over the future of the sector, we need to move on Open Finance, (the data bill is sitting in a drawer in parliament and should be moved forward as a priority) and we need to think about how we can build regulatory passporting into trade deals as we sign them.

On the market forces side we need more banks to take a leaf out of NatWest’s book and accelerate the development of premium APIs, we need to align on risk and liability frameworks for the use of these and work towards clarity for the market on commercial details. Finally we need better engagement between institutional lenders and retail lenders that use open banking data. Cost of capital is a major hurdle for Open Banking’s proliferation in the lending space and this both can and should be addressed.

This is a blockbuster agenda for 2023, but if we can get it done the prize for UK firms will be transformational. If we can’t, Open Banking will still have a major impact on our domestic economy but it might not be the firms hiring UK talent and paying UK tax that deliver it. This is not beyond us. There’s a lot to do but if we lace up our trainers, I’m very confident that we can make it happen.

”˜Consumer’ data has failed its creators

Consumer data’ is a remarkable quantity for the lack of ownership afforded to its eponymous creator ”“ the internet browser, the Google-er’, the consumer. Indeed, all of us are the creators of digital data from which Big Tech ”“ Google, Facebook, Amazon (you know the names) ”“ have achieved their giant status.

In fact, each time we open a website or app we leave behind a digital footprint used to track our movements across different websites and applications. This trail is inspected by Big Tech’s pack of algorithms, subsequently, determining’ a web user’s probable interests in products, ideas, and trends. With such an accurate’ determination of human interest at its disposal, Big Tech amasses a library of consumer data that it sells to advertisers, generating a lucrative revenue stream.

The relationship between consumers and advertisers goes back to Roman market squares and still serves just as important an economic function today. Yet, in today’s digital context, the creators of the industry’s most prized resource ”“ data ”“ have been excluded from sharing in its reward.

How has such an intrinsically unjust state of affairs survived for so long? Largely because consumers have been misled. In the first instance, consumers have been made to believe that their data holds no personal value. Secondly, that lack of control over data and, indeed, privacy is inseparable from the internet. While, this is slowly changing, with users now able to opt out of certain trackers, Big Tech is still aggressively trying to force us to adopt them: even if a user chooses to reject certain targeting preferences, they are often forced to confirm every time they enter the site or until impatience overcomes concerns.

Although they have certainly been egregious, we cannot place the entire blame on Big Tech, advertisers also have much to answer for. Advertisers spend approximately £27 billion a year on digital marketing, for the most part, this goes straight to Big Tech. This enormous expenditure is justified because it is, in actuality, an investment ”“ an investment made to entice consumers to spend. Moreover, in today’s digitally entangled economy in which jobs, networking, and day-to-day life are so dependent on internet access, the reach of advertising is inescapable. And so, we exist within a digital ecosystem that demands we share our thoughts and data with Earth’s largest corporations, only to boost our own likelihood to spend.

Undoubtedly, this status quo must change. Consumers must recognise the worth of their data and demand remuneration. Meanwhile, advertisers must stop encouraging and feeding Big Tech with the dirty cash that encourages such malpractice. The objective of advertisers must shift from only selling to selling and rewarding. In short, advertisers who seek access to consumer data must provide them with benefits.

Fortunately, the emergence of direct-to-consumer marketing apps and platforms has made such solutions a reality. For advertisers who market via such platforms, they unlock the ability to directly communicate with target consumers, in return offering the latter cash benefits and rewards. It is the responsibility of the platforms themselves to keep the end-user in mind, leveraging their position to ensure consumers get access to the highest value rewards. Furthermore, consumers are able to identify a preferred level of privacy, exchanging a level of data access on a quid quo pro basis to maximise cash benefits, all while driving a positive feedback loop of more relevant ad targeting.

By using direct-to-consumer marketing platforms, consumers can finally reclaim the right to their data and expect a fair price for its exchange. The current economic environment, undoubtedly, makes such solutions particularly enticing.

Though, far more importantly, direct-to-consumer platforms are resetting the relationship between data and advertising, shifting power away from Big Tech and back to consumers. Slowly, we march towards a future where digital data is not a price tag of the modern economy, but a precious commodity back in the hands of its creators, who financially benefit from its transparent and consensual exchange.

Mohsin Rashid is the CEO and co-founder of ZIPZERO, which offers a mass-market consumer solution to the cost-of-living crisis. Shopping via the ZIPZERO app earns users cash to pay bills ”“ the cash rewards are funded by retailers and brands, which gain access to a formidable direct-to-consumer marketing platform, allowing them to divert a collective £27 billion digital advertising spend back to their own customers. Through its compelling consumer proposition, ZIPZERO has become a prolific source of first-party, product-level consumer data. ZIPZERO is inviting major utility firms, leading retailers & brands (advertisers) to make active use of its progressive platform and help UK consumers tackle the cost-of-living crisis.

Codat recognised in Open Finance Global Rankings

Fintech Codat, part of the FinTech Scotland community, has been recognised in the Open Finance Global Rankings.

The rankings is released every year by Open Future World to highlight the organisations, countries and individuals who are leading progress in open finance around the world.

Codat, the fintech that helps companies build B2B solutions for SMEs using Open Banking, appeared in the top 20 of this year’s rankings. This is a real achievement when taking into account that Open Future World look at over 1,000 organisations from almost 80 countries.

Marie Walker, Open Future World co-founder commented:

“After a year that has seen plenty of challenges, the global rankings are a timely reminder of just how much the open finance movement is achieving ”“ and how much more there is to come,”

Rankings are calculated based on appearances in Open Future World’s widely-read Daily Edit of news, opinions, launches and raises.

DirectID appointed as Fintech Champion for Nations

The Department for International Trade (DIT) has announced the Fintech Champions for Scotland and Wales at the Board of Trade meeting in Wales today.

DirectID have been appointed as the Fintech Champions for Scotland, with Yoello selected as the Welsh Fintech Champion. They join the previously announced Northern Ireland Fintech Champion FinTru, meaning that a Champion is now in place across each of the devolved nations.

The Fintech Champions scheme was established by DIT last year as a way of better supporting the UK Fintech industry. Each Fintech Champion will be tasked with working alongside other industry leaders to elevate the UK’s status as a global Fintech hub.

They’ll also be asked to help promote expansion around the world and help businesses scale-up and up-skill by providing one-to-one sector-specific advice.

Minister for Exports Andrew Bowie said:

“Fintech is already worth billions to the UK economy, and we’re keen to see the industry continue to grow over the coming years.

“With these two companies joining the Fintech Champions programme, we now have expertise supporting businesses across all four nations who want to scale up their operations.

“Both are leaders in the industry and will do a fantastic job promoting the UK’s place as a global Fintech hub.”

The UK is already a world leader in Fintech, owning more than 10% of the global market share and is forecast to grow dramatically to £380 billion by 2030.

The UK also secures 11% of all global investment into the sector, attracting nearly half of all investment in Europe. Innovate Finance estimate total investment into British fintechs jumped more than 217% to $11.6bn in 2021.

With an increasing number of Fintech firms exporting globally from the UK, DIT is helping the sector take advantage of our global trade links, ultimately creating more jobs and driving further investment into all corners of the country.

The new Scottish Fintech Champion, DirectID, was the earliest open banking pioneer, and provides advanced open banking data for credit & risk decision makers in 46 countries.

James Varga, CEO & Founder at DirectID said:

“I was incredibly humbled and excited when I was invited to help champion exporting in the Fintech sector.

“DirectID now powers some of the world’s biggest brands in North America, Europe and Asia to scale, drive efficiencies, manage risk, and create fairer outcomes for their customers.

“Whether it’s working with other industry figures to promote the UK as a place to do business, or sharing knowledge of our experience exporting to multi-national organisations, I’m proud to be supporting the growth of the £11 billion UK fintech economy.”