Together we can do so much more: introducing Finclusion 2021

In this guest blog, Victoria Roberts, director of the Fintech Delivery Panel and Insurtech Board at Tech Nation, announces plans for Finclusion 2021, a month-long focus on fintech and financial inclusion that aims to raise awareness, inspire and support innovation, and promote collaboration.

It was Helen Keller that once said: “Alone we can do so little; together we can do so much”. She didn’t say this to disparage the efforts of individuals ”“ far from it ”“ but to highlight the power and potential of people working together.

Because there is some sort of magic ”“ some intangible spark of creativity and inspiration and innovation ”“ that happens when human beings come together in pursuit of a common goal, particularly when that goal is for the greater good.

Fighting financial exclusion

In the UK, we are at the cutting edge of fintech and innovation in financial services, and yet there are still around one million people in the UK who find themselves financially excluded.

A global pandemic hasn’t helped. While on one hand the economic and social disruption of Covid-19 has increased fintech adoption and customer use of digital propositions, it has also magnified pre-existing challenges of financial exclusion and vulnerability across society ”“ and at the same time created new ones. These include financial and personal vulnerabilities, access to services and information on financial products, intersecting struggles between health and care challenges and income instability, access to a safety net’ of affordable credit and insurance products, and the impact of lower financial literacy and planning which is often particularly highlighted in times of crisis.

Fintech as a force for good

Those of us who work in fintech can see the potential power of technology to make a real and lasting difference in this area. As we look to help individuals throughout the recovery, there is an opportunity for fintech to play a significant role in helping both those adversely impacted by recent events, and those who have traditionally been underserved by the existing financial system.

The Kalifa review highlighted the need for low cost, far-reaching fintech solutions to reach the financially excluded. Whether it is digital IDs to combat fraud, financial wellbeing apps to support sustainable financial behaviour, or a potential game-changing technological innovation that is as yet only a glimmer of an idea in the mind of a forward-thinking individual, we know from our work with fintech entrepreneurs and in helping to scale fintech companies that the talent, ideas and drive are out there ”“ we just need to support and scale it to create the change we want to see.

“Financial Inclusion is a significant driving force and motivator for so many of the fintech SME’s working in Scotland. They are working to create a more inclusive financial sector for all. Finclusion 2021 helps us highlight fintech’s power to address important social and economic challenges, and improve financial well-being for people across Scotland and the UK. We are hugely excited to be part of the Finclusion 2021 campaign, and to do what we can to encourage the whole ecosystem, from investors, founders, institutions and advisors, to embrace this opportunity to design an inclusive future of finance.

“As the Kalifa Review made clear, there is a pressing need for the undoubted ingenuity and disruptive power of fintech to be energetically applied to eradicating the obstacles to financial resilience impacting the everyday lives of our fellow citizens in the UK. This was a big problem pre-Covid: it is, arguably, nothing short of an emergency today.”

Shan M. Millie, founder of Bright Blue Hare, member of Tech Nation’s Insurtech Board, and co-chair Finclusion 2021

Introducing Finclusion 2021

That’s why we’ve launched Finclusion 2021, a series of connected happenings designed to stimulate, inspire, showcase and scale fintech’s contribution to financial inclusion, from potential game-changing products and collaborations, to the here-and-now actions being driven by the UK’s leading firms reshaping financial services.

Throughout November 2021, there will be virtual and in-person workshops, show-and-tell-events, and sprint challenges, together with thought leadership and discussion across social and traditional media.

We hope that the month-long focus will promote conversation about the key issues, inspire innovation for financial inclusion and wellbeing, and kick-start a broader call-to-action for the entire fintech community to collaborate to directly solve financial inclusion challenges to the benefit of end consumers.

“The impact of financial exclusion on peoples’ lives can be devastating, leaving many without savings or insurance, and sometimes even without access to a bank account, often having to turn to unaffordable, unregulated credit when they have no other options. If we can turn the energy and innovative ideas of the fintech community towards the development of products and services that meet people’s needs, we could help build resilience and improve financial well-being for millions.”

Chris Pond, chair of the Financial Inclusion Commission, member of Tech Nation’s Fintech Delivery Panel, and co-chair of Finclusion 2021

No one left behind

Fintech is driving fantastic innovation in financial services but, as this digitisation continues apace, we need to ensure no one is left behind. It’s great to see the fintech industry already stepping up to this challenge, and I have been inspired to see fintech firms and financial institutions coming together to listen and learn from lived experience experts during development of the campaign.

I’m really excited to see what more Finclusion 2021 can do to help educate the sector on which challenges are most pressing, and encourage innovative action to address these.

We hope as many people as possible will join us online for the virtual launch of the campaign on 3 November, where we will be sharing more information on our vision, mission and the programme of events.

We’re also inviting fintech entrepreneurs and ecosystem stakeholders to get involved by organising an event, joining the conversation, showcasing existing fintech solutions and registering to attend Finclusion events. More information on the campaign is available on our website.

#FinclusionUK2021 ”“ what part will you play?

82% of 50s market would not take robo-adviser financial advice

New research from Visible Capital on the over 50s market shows that 82% would not take financial advice from a robo-adviser and 88% would not be willing to give details of their finances to a robo-adviser to enable them to give a better personalised service.

The results come from new research carried out amongst UK adults with an age range from 50 upwards, with the bulk of the respondents aged 60 to 80. 38% said they currently access financial advice through an adviser or accountant.

This aversion to pure digital advice was amongst a cohort of whom over 60% said they had been relying on technology more during the pandemic period and are comfortable with technology and have clearly adapted well to navigating the huge range of interactions and services which have gone online during COVID19.

Among the group, 84% were using online services for general banking, 52% for insurance, 44% savings and investments, 64% for payments and transfers and their 55% were managing their credit cards digitally. Yet only 15% of respondents used online services for advice.

A fifth (20%) of respondents said they trusted technology less coming out of the pandemic; perhaps some of their digital encounters have been frustrating and only borne of necessity.

Ross Laurie, CEO Visible Capital, comments:

“This should be interesting reading for financial advisers being a wealth cohort of which 64% said they felt reasonably well off’, which for the majority of advice firms will sit squarely within their core client group.

The results of our survey show that age 50+ savers and investors are no strangers to using digital services, which has been accelerated by the pandemic and is likely to grow in the post pandemic world. But, as yet, they have not taken advantage of online financial advice. Our survey results show that trust is a major factor here. Utilising the tools and services with which this group are already familiar ”“ online banking, investing, saving, etc, ”“ advice firms can offer this day-to-day technology with the kind of personal, trusted human advice which many of them already value.

Advisers have a real opportunity to step into the hybrid advice space and claim it as their own.”

Scotland Fintech festival! We loved it and can’t wait for next year!

We recently concluded the FinTech Scotland festival ending a wonderful four weeks where we got to celebrate fintech innovation in Scotland, across the UK and around the world!

With 60 events covering a broad range of interesting topics, discussions, and views for the future there was plenty to talk about and more to excite us for the next 12 months ahead.

We started in Edinburgh and ended in Glasgow taking a trip around the world via Australia, America, Europe, Dundee, Stirling and London!

Among my favourites were the face to face events, where the buzz and energy in the room confirmed there’s much going on in FinTech innovation in Scotland, and that we all were excited to be out and about reconnecting face to face, enjoying new conversations and sparking new ideas.

Digit’s FinTech Summit kicked everything off in true Digit style. It was great to see Visible Capital, LendingCrowd, Amiqus, Sustainably, ShareIn, Zumo, Nude, Exizent and Love Electric, all Scottish home grown fintech talents, building and scaling businesses, and developing the future of finance.

Other one of my favourite events was a truly brilliant and informative discussion on the meeting of Space Data and FinTech! Thank you, the University of Strathclyde, Trade in Space, Go-to-Market for sharing your insights, experience and expertise on how Space Data gives us an exciting prospect for more fintech innovation!

FinTech innovators never fail to inspire me, it was an privilege to share an event that saw Know-it, Doqit, Biscuit Tin, PolyDigi and Gigged.ai talk about their businesses, innovations and aspirations for the future.

We connected around the world, sharing experiences of Open Banking innovation with FinTech Australia and hearing directly from a range of European regulators on their experiences of fintech.

Our own regulator the FCA hosted a record number of events covering topics from crypto, Innovation, Sustainable finance and RegTech!

We rounded the festival off in Glasgow with the Times Scotland and Canongate event and an opportunity to discuss accelerating fintech across the UK! Another event that reminded me of the value of connection, the true potential for UK fintech innovation and role that Scotland plays in influencing that story and setting direction.

Thank you for joining us, being part of our story and helping us to shape the future.

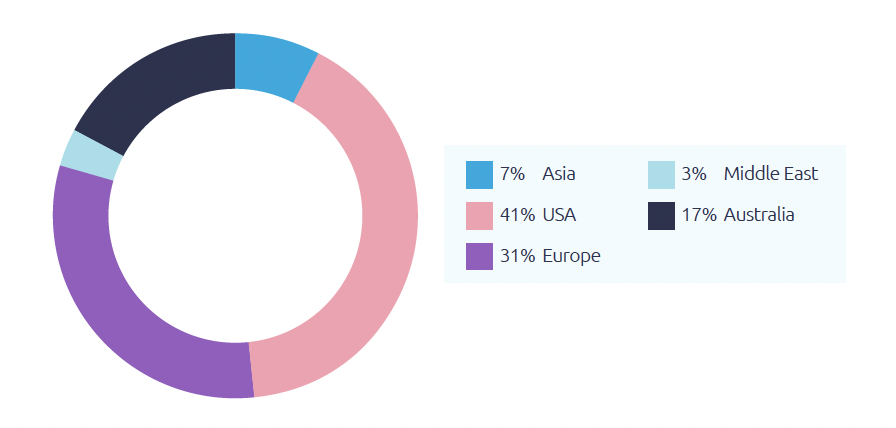

Growing International Diversity of Fintech SMEs in Scotland

Fintech has accelerated as a global innovation movement during the pandemic and Scotland is making a positive contribution to this force of change in the digital economy

FinTech Scotland has confirmed that the number of international fintech SMEs in the SME community has grown by over 40% over the past twelve months, complementing the growth of local start-up and growth enterprises.

In recent months companies such as YayPay and Pace AP from the USA, WeFund from Australia and Pulse Market from Ireland have become part of the growing Fintech Scotland community.

The diverse origination of the international SMEs in Scotland’s Fintech community is highlighted by the visual below.

This growing global influence in the Scotland fintech community was a key theme of this year’s Fintech Festival which concluded last Thursday its four-week programme of sixty plus events, innovation meet-ups and conferences.

The Festival included FinTech Scotland’s collaboration with Scottish Development International and UK Department for International Trade Festival to host events with enterprises in Australian, USA and Asia to highlight inward investment and export opportunities.

The Festival included FinTech Scotland’s collaboration with Scottish Development International and UK Department for International Trade Festival to host events with enterprises in Australian, USA and Asia to highlight inward investment and export opportunities.

The global fintech opportunities was also one of the themes discussed at the Accelerating UK FinTech Conference’ hosted by FinTech Scotland last week, with presentations from Fintech leaders across the UK including Ron Kalifa, Regional bodies and Government Ministers.

FinTech Scotland used the conference to release a “Building a Global Fintech Cluster” prospectus (brochure) to further build on the momentum driving fintech innovation and collaboration.

Commenting, the Executive Chair of Fintech Scotland, Stephen Ingledew said

“The ongoing collaboration of inspiring FinTech leaders will enable us grasp the global innovation opportunities and the UK wide conference in Glasgow was an ideal opportunity to demonstrate this with colleagues and friends from all corners of our country”

Commenting on the FinTech Scotland Festival, CEO of FinTech Scotland Nicola Anderson said,

This year’s festival has reinforced the dynamism, breadth, and capability of fintech innovation in Scotland. We were privileged to be joined by so many fintech and industry leaders sharing experiences, knowledge and opportunities. We’re looking to more collaboration and to supporting the digital and green economy through continued fintech innovation.”

Lessons as the latest IPO window starts to close

In recent weeks, there has been a flurry of news articles about the bumper run of IPOs, observed as economies globally look to plot a post-COVID recovery. Those ongoing and ultra-lax monetary policies buoy this, though that may be coming to an end. Floats are being postponed or prices slashed by prospective issuers, suggesting that it is inevitable that the window is starting to close ”“ for now anyway.

However, is this such a bad thing? Increasingly IPOs have been looking somewhat disorganised. Whilst fervent day one ‘pops’ in the share prices of newly issued stock may be headline-grabbing, ultimately, it suggests that the advisers have miscalled the market. Founders and early-stage investors could have got a far better price had a more considered approach been taken. Indeed, academic thinking from a little over twenty years ago always suggested that involvement in IPOs was a risky proposition. With savings in transaction costs and taxes offset by the fact that the previous investor ought to be selling at the top of the market and the opportunity cost of having capital tied up during the pre-IPO period.

It is also worth bearing in mind that even if IPO deal flow does become somewhat more constrained, the option is not being removed indefinitely. This market has always been cyclical, so that it will return. Given that, what takeaways are there from the frantic levels of activity seen over the last twelve months?

Arguably the most important for many will be ensuring that your cap table reflects the needs of the business at the time of float. What will an IPO mean for key staff and early-stage investors who have likely played an instrumental role in getting you this far? And how can these valuable participants be convinced to stick around for the next phase of the journey?

Secondly, there’s that opportunity to ensure your business is IPO-ready. Regardless of the time horizon here, there’s a raft of best practices that you can deploy to make sure your company is in the right shape to facilitate a listing. After all, you may find that time is of the essence at a future date and such preparedness has longevity ”“ investments now will yield results in the future. That combines to create a situation where you’re getting closer to having liquidity within your privately held business ”“ something that CrowdX is assisting with already, helping bolster the company’s reputation, its brand perception, and the early stages of institutional engagement.

This all means that it should be easier for prospective professional advisers to make more accurate assessments of your company’s value. Those ‘day-one-pops’ in share prices can largely be a simple transfer of wealth from your company to the institutions that can participate at the very outset. Don’t give away wealth unnecessarily.

Looking forward to a month of events

Welcome to September! I’m excited to write this month’s blog post where we highlight the 2021 FinTech Scotland Festival.

September is always a month the FinTech Scotland team look forward! It’s a time to celebrate fintech, learn about developments, meet new people, and reconnect with old friends who are driving forward fintech innovation across Scotland and across the world.

This year we’re especially grateful to be able to welcome back more in person, and face to face events as we continue to emerge from the necessary restrictions over the last 18 months.

The festival kicks off on the 16th of September with the DIGIT FinTech Summit and concludes with the Times Scotland and Canongate Publishing event on actions and initiatives to drive global fintech leadership on the 14th of October.

For the first time in a long time, we’ll get to see people in person! We’ll experience the atmosphere and energy that comes from fintech innovation and specifically through the people that make fintech.

Fintech entrepreneurs and leaders will share their experiences and talk about the innovations shaping financial services and the future digital economy. We’ll hear from Nucleus, Sustainably and LendingCrowd on their thoughts about the opportunity fintech continues to present and about the fintech Cluster in Scotland. Soar, MoneyMatix and Exizent will give views on the opportunities for fintech to contribute to building back better post COVID. Fintechs such as Pour, Striver, Women’s Coin, Amiqus, Modulr and Gigged.ai also plan to share their experiences and ambitions for the future.

We’ll be hearing directly from fintech entrepreneurs on topics such as fast-tracking innovation, the future of crypto, how blockchain is transforming society, avoiding team burnout in fintech and how to scale a fintech! YES and YES!

The diverse mix of events and topics covered during the festival continue to demonstrate the breath of opportunity and significant range of contribution that makes fintech unique, inclusive and collaborative. It’s this support from a wide range of committed participants that allows fintech innovation in Scotland to thrive.

Like every year, our partners are also very much involved and we’re looking forward to attend events from RBS, Pinsent Masons, BT, PwC, Deloitte, The University of Edinburgh, The University of Strathclyde, IBM, Merkle, Checkpoint, SDI and no less than 6 events from the FCA.

We’re particularly excited to welcome colleagues from across the UK and the world as we continue to build national and international collaboration, share knowledge, and learn about fintech developments across regions and geographies.

We’re privileged and inspired to see the leadership, experience and expertise that plan to contribute across all the events, and I’d like to extend my thanks to everyone involved.

I’ll look forward to hearing your experiences and updates across the duration of the festival and I’m very much looking forward to seeing many of you in the coming weeks.

All the best

Nicola

The evolution of high-growth tech firms in Scotland

By Lynsey Walker, dispute resolution partner and tech specialist at Addleshaw Goddard

Technology and digital innovation have played an important role throughout the pandemic, which rapidly accelerated a global reliance on connected services.

Digital innovation has protected many businesses which, despite traditionally not being online operators, have been able to pivot through a technology-first approach, providing business continuity which previously would have been an expensive challenge.

As the wider economy opened as Scotland was moved to level 0, our continued ability to work from home while also remaining connected with friends, family and social groups underlines how vital technology and digital innovation is to the country’s economic recovery. It is clear that the loosening of restrictions is not going to result in a return to all of our pre-pandemic practices.

Central to this is the understanding that tech underpins all sectors, from education to manufacturing, rather than a standalone stream supplying businesses with IT or other more traditional machines.

In recognition of this, the Scottish Government has made more funding available to help businesses take advantage of digital technologies to improve their productivity, increase their resilience and create new market opportunities. An additional £11.8 million, announced in November 2020, will go towards helping businesses to adopt digital technologies and improve their digital capabilities.

Looking at the fintech sector specifically, Scotland already boasts one of Europe’s most successful offerings and is projected for notable growth in the years ahead. Innovators are looking to the future and are driving a collaborative agenda in a bid to make impactful change across the sector and for consumers alike.

The launch of the Kalifa Review earlier this year marked a significant milestone for the UK fintech sector, as it set out a strategy that will accelerate growth over the next three years – again enabling post-pandemic recovery.

Deservingly, Scotland was earmarked as a standout region thanks to the continued development of its Fintech Scotland Cluster model. With input from Fintech Scotland, the Kalifa Review sets out a five-point plan to leverage innovation through a positive regulatory environment, developing diverse skills, facilitating investment to scale enterprises and accelerating a targeted approach to inward investment. It will be fascinating to see how we gather momentum in enabling this through investment, innovation and job creation.

Just last week, UK Government ministers were given an exclusive glimpse into the evolving Scottish fintech community as part of an event hosted by FinTech Scotland. Secretary of State for Trade, Liz Truss, and Scotland Secretary, Alister Jack, paid a visit to the Bayes Centre to meet some of the companies driving the thriving fintech ecosystem.

Over the last five years, Addleshaw Goddard has developed its AG Elevate programme, designed to accelerate start-ups and guide fast-growing tech firms through the legal challenges they face. We’re proud to have supported more than 30 fintech and technology entrepreneurs’ innovative businesses, helping many go on to operate internationally.

Originally designed for fintech firms, this year Addleshaw Goddard welcomed all high-growth tech businesses to the scheme and has also placed a greater focus on businesses with an emphasis on sustainability.

Given Addleshaw Goddard’s experience and insight into the tech sector, this year we also launched the Aspiring Unicorns campaign to support high-growth tech firms. We are encouraging as many businesses and entrepreneurs as possible to get involved.

Aspiring Unicorns comprises seven critical lessons for high-growth technology firms to consider such as data, disputes, IP and investments, and we will be delivering relevant insights on these themes over the coming months.

We’ve developed our support programmes as we recognise the supportive infrastructure, innovation and opportunities that are all available within Scotland for high-growth tech and fintech firms. While the last year has been challenging collectively, tech and digital innovation’s positive influence throughout has reinforced why we are committed to championing its capabilities.

Collaborative leadership, entrepreneurial mindsets and support from government is required for Scotland to spearhead the fintech sector at a global level, and it’s evident that we have these tools to continue such drive.

For more information about the Aspiring Unicorns programme, visit: https://www.addleshawgoddard.com/en/insights/insights-briefings/2021/general/guide-aspiring-unicorns-supporting-high-growth-tech/

FinTech Scotland looking ahead and looking forward!

With August literally just around the corner we’re inching closer to the FinTech Scotland Festival which starts on the 16th of September with Digit’s FinTech Summit.

This year we’re hoping to see a return to some face-to-face events and are looking forward to catching up in person with so many of you working across Scotland and UK fintech clusters. We’re starting to see more opportunities for those in person meet ups, respecting the opportunity to start seeing people again in a safe way. Personally, I’m finding it invigorating and energy building talking face to face with those inspiring and committed to driving change through fintech innovation.

That energy was more than evident in a FinTech Scotland meeting with Liz Truss, the Secretary of State for International Trade earlier in July. Not only was it good to see everyone in a (large) meeting room, but it was also great to hear directly from the leaders in Trace Data, Direct ID, Float, EedenBull, Modulr, FreeAgent on their plans and views on international trade and how Scotland is leading and building world class data driven innovations. Key markets discussed included the US, Asia and Australia. Opportunities are growing and many of the events in the festival will focus on international trade opportunities helping to build local understanding of fintech markets in Australia and other countries. (Link to the FinTech Australia event).

We’ve also been working closely with the University of Edinburgh and Edinburgh Innovations on a Data Driven Entrepreneurial Programme that is focused on the application of PhD research into industry and in building businesses. All the enterprises are using technology and data and are building innovative solutions across a host of issues, including climate change, economic recovery and financial wellbeing. The team at Space Intelligence is focused on managing environmental risks using technology and space data analytics to monitor carbon reducing initiatives. I also met Iceni Earth this week, another climate fintech innovation, and providing leadership and practical applications that supports agriculture and better land use. I’m constantly reminded how privileged and lucky we are in FinTech Scotland with continuous connections to new innovations supporting future business developments.

Over the coming weeks and months, we’ll be doing more on climate and fintech. The FCA recently announced a range of planned innovation programmes for later in 2021 starting with a Tech Sprint in October on the topic of ESG data and helping build market confidence towards ESG credentials and the environmental impact of financial decisions. There is more information here, and it’s another opportunity for Scotland to showcase its strengths in innovation, driving purposeful change and building collaboration to achieve Net Zero ambitions.

The topic of fintech’s role to address climate change was also discussed on one of the FinTech Scotland podcasts in July, it’s a great listen!

How Platform Sourcing can help Fintechs win the War for Talent

Current State

The War for Talent had a ceasefire in early 2020 due to COVID-19 but is now back in full swing. The War for Talent is not new, the term was coined by McKinsey and Company way back in 1997. However, this war has evolved due to the increase in digital initiatives and the rise in remote work smashing down the usual geographical barriers. The most in-demand tech roles for companies across the UK are software developers, web designers and data analysts with AI skills quickly catching up. According to Adzuna in April 2021 there were nearly 10,000 vacancies for software developers, compared to 5,630 at the same time last year. Furthermore, the Gartner 2021 CFO survey found that 74% of CFO’s plan to permanently shift employees to remote work after the Covid-19 crisis ends. Many Fintechs including Revolut have rewrote policies to include fully remote work.

The old solution

Historically when skills are in demand there are a number of tactics large organisations deploy which include but not limited to:

- Post more (and more and more) jobs on Linked In

- Create a new Preferred Supplier List (PSL) of agencies

- Hire contractors from PSL when perm hiring stalls

- Referrals schemes

- Recruitment open days

- Host tech meet ups (obligatory beer and pizza post)

- Expensive PR Campaigns to hype up culture and opportunity

- Increase Salaries

Now these are all perfectly good solutions if you have lots of time and money. However, most digital initiatives have an end goal to generate revenue. With a lack of key talent then projects start to delay and so does the revenue. This is when most CEO’s and CFO’s start to get interested. This is usually when the big digital consultancies get brought in.

The new solution

There is another way. There is so much talk right now about the “future of work” and there are many debates of what that means. That is for another day, lets focus solely on the platform sourcing element of the future of work. There has been a rise in companies using talent platforms to complete projects using platforms such as Toptal, Freelancer, Innocentive and Upwork. Even NASA use platform sourcing for major software development projects. This has been largely in North America with the UK slow to this model.

A recent Harvard Business School report about building the on-demand workforce states:

“COVID-19 has only accelerated the move away from traditional, pre-digital-era talent models toward on-demand workforce models.”

Also, the well-regarded University of Oxford Report on Platform Sourcing stated there will be rapid growth in the next 5 years on how companies use Platform Sourcing including crowdsourcing and outsourcing platforms. The report focused on research around how Fortune 500 firms are adopting online platforms. The report author Greetje Corporaal found the following benefits:

- Providing easy access to a scalable source of manpower, skills and expertise

Platforms provide access to freelancers with highly specialized skills and expertise, making them an attractive option for organizations to quickly and flexibly complement the capabilities of their in-house employees on an on- demand basis.

- Reducing start-up and transaction costs

Compared to traditional outsourcing vendors and contracting agencies, platforms substantially lower the start-up and transaction costs of a contract. This allows enterprises to quickly hire freelancers to address project needs.

- Eliminating conventional hiring barriers

Platform technologies eliminate or at least reduce geographical, informational, and administrative barriers in the hiring process. This allows their use for projects of shorter length and scope. It facilitates the hiring of freelancers on a more flexible, on-demand basis, and allows managers to bring in new skills and knowledge to the organization that would otherwise have remained outside.

There are factors to be aware of when using platform sourcing:

- The work needs to be well defined with milestones and outcomes

- Time zones need to be factored in

- This does not replace your team but can enhance

In conclusion, the next time you are worrying about the impact that losing the war for talent will have on your projects and ultimately revenue then consider a platform approach. There are a number of UK platform companies including Distributed and the Gigged.AI (I am biased as the CEO). Start small and define your outcomes and this could be game-changer.

Candidate Engagement in Fintech Recruitment

I read recently that in the next four years, The Global Fintech Market is expected to grow at a rate of 23.58%. With news emerging that the Scottish Government has appointed an adviser to assist tech, with £7m earmarked for the project, Scottish Fintech has a great opportunity on its hands to grow.

But this growth will need great talent to sustain it. Talent that will sustain growth and drive innovation – not an easy feat considering the current shortages of candidates across all tech markets.

This shortage isn’t due to slow in the next few years either. In a recent study, The World Economic Forum pointed out that the global talent shortage in technology, media, and telecommunications alone is due to reach 4.3million workers by 2030.

What Does This Mean for Fintech Recruitment?

It means that it’s becoming more difficult to hire top talent and will continue to become harder. We already know that top tech talent hold most of the cards, shortages meaning they have their choice of employers and can command top salaries.

Businesses that want to continue to innovate and stay at the top of their game need the right people to do so. Which means being able to attract and engage the best candidates. But with many businesses in Scotland at the startup or ramping stage, recruitment often doesn’t come top of their list.

Getting the right people in place is a combination of being able to access alternative talent pools, and engaging them and your traditional pools.

How to Improve Candidate Engagement?

The type of people you’re looking for aren’t usually out of a job. Right now, it’s not just candidates who need to impress employers, employers need to impress candidates too. And that means working on your candidate engagement:

Working on Your Candidate Value Proposition

Salary and standard benefits are no longer enough to engage with top talent in the tech space. You need to do more. That means improving your candidate value proposition. What do you offer over and above the competition?

The easiest way to improve your candidate value proposition is to improve your employee value proposition. Use internal surveys to ask your current team what they like about working for you and what you could be doing better. The happier people are at work, the more likely they are to spread good word of mouth among friends and peers.

Changes could be more flexible hours, the ability to permanently work from home, better choice of benefits, company shares (particularly for start-ups), or better work culture. Many people are also looking for more social responsibility from their employers, both with charitable efforts or sustainability.

When you have identified what areas are important to your current team, ensure these are clear on your careers site, on your social media, and in any candidate collateral, you issue.

Put More Effort into Diversity and Inclusion

Currently, just 24% of people working in fintech in Scotland are women. Considering women makeup 51.5% of the population, that figure looks low. Just 1.4% of fintech workers are black and 6.2% Asian. (Solutions Driven 2021)

All of these are untapped, diverse markets that businesses should be engaging with to diversify their talent pools and find candidates their competitors can’t. But do you improve candidate engagement in these areas?

- Talk to the diverse people in your current teams – what could you be doing better to make them feel included? Is there anything you’re doing wrong?

- Set up diversity groups – is there scope for a women’s panel in the business? Could you set up a diversity workforce?

- Embed diversity into your KPIs – set targets for diversity and make them part of your recruitment team’s KPIs.

- Improve diversity branding – make diverse figures visible on your website, your social media, and your candidate content.

- Improve your language – masculine language using words like “ninja” and “rockstar” turn women off applying for roles. Look at making your language more inclusive.

Spend More Time Engaging Candidates

Candidates like to feel sold to. They want to feel as though joining your business will benefit them and you, and that they’d be a valuable member of the team.

If “candidate engagement” consists of sending a couple of messages or emails, that’s not going to cut it. Much like a sales process, great talent needs multiple touchpoints from your company to attract the candidate. After all, a 2019 survey by Indeed showed that 13% of job seekers have ghosted a business because there wasn’t enough engagement with the hiring manager or recruiter.

If your own team doesn’t have the time to carry out a longer process like this, you need to ensure your recruitment partner does. They must be well-versed in the complexities of tech talent and spend the time and energy showing them why your business is the right one for them.

At Solutions Driven, our candidate engagement works alongside our 6F Methodology, where we ensure someone is right for a role and a company by looking at their compatibility in Fit, Freedom, Family, Fulfilment, Fortune and Future. If someone matches with your business in these areas, they’re more likely to feel an affinity with the business, feel fulfilled, and become long-term employees.

Great candidate engagement has a multitude of benefits for your business. Not only are you more likely to find and attract the talent you need right now, you also build a pipeline of connected talent for the future. If people have a great experience, even if they don’t get the role, they’re more likely to re-apply or be open to an approach further down the line. Word of mouth is vital in smaller sectors and by ensuring your employees, prospects, and potential prospects all have a positive view of your business, you’re setting yourself up for future hiring success, as well as current.

To find out more about how to connect with alternative talent pools, engage candidates, and power your growth, get in touch with Nicki Paterson at Solutions Driven today on npaterson@solutionsdriven.com.