Tech firm Exizent on why Bereavement processes are not fit for the 21st Century

Exizent, the Glasgow based technology firm recently launched its Probate Prospects survey which revealed why bereavement processes need a radical overhaul.

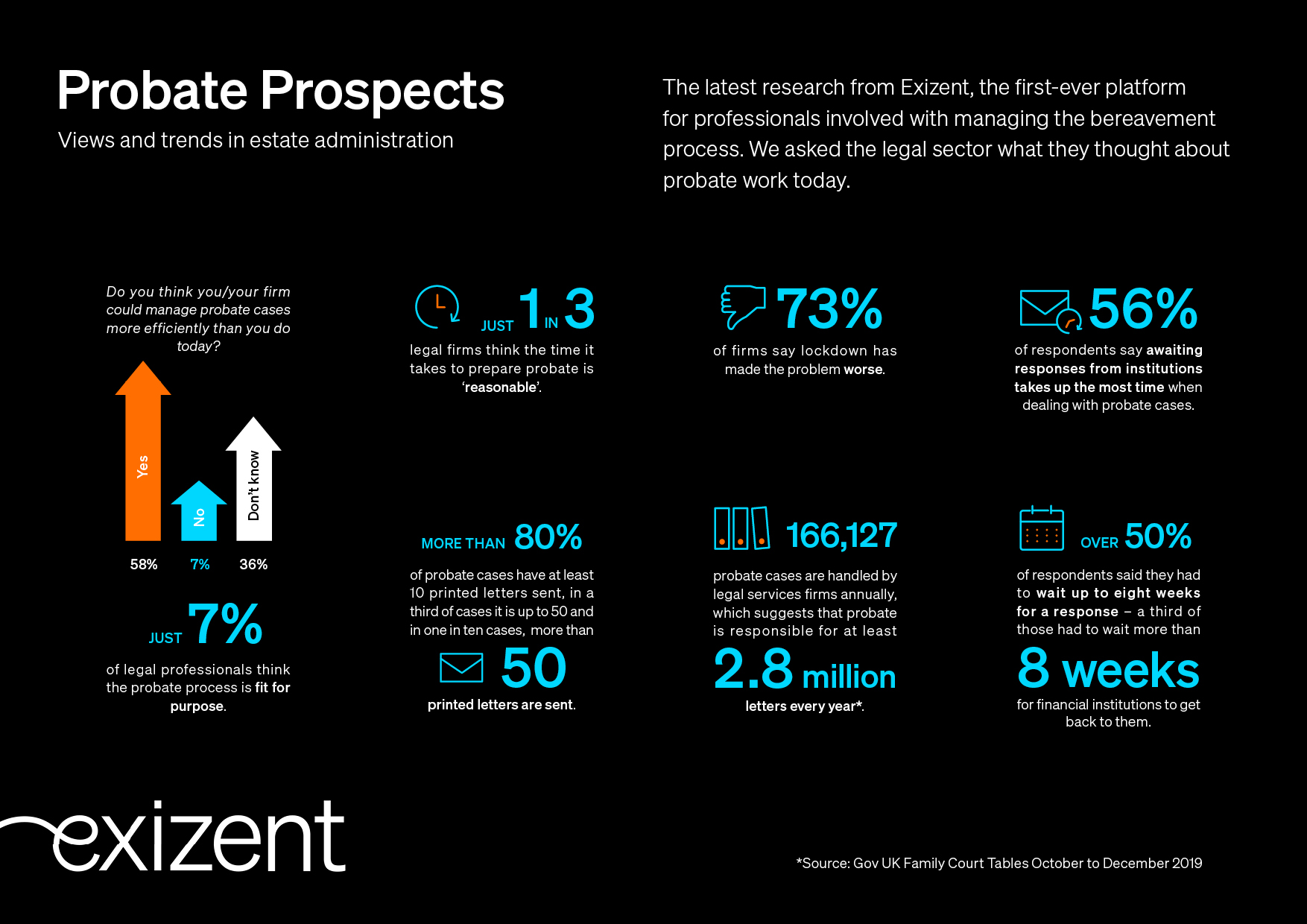

It surveyed the legal profession who handle probate, the process of dealing with the estate of someone who has died. It found that even though most law firms (64%) either have specialist probate teams or people who mainly work on probate cases, the vast majority feel the processes are inefficient and could be enhanced by technology.

The top reason respondents gave for why they think probate cases take so long was waiting for financial institutions to get back to them’, with more than half (56%) saying this was the main hold up. More than half of respondents also said they had to wait up to eight weeks for a response ”“ a third of those had to wait more than eight weeks.

After waiting on institutions’, respondents said administration’ was the next most time-consuming part of the probate process, with more than a quarter (27%) saying this causes the most delays.

Exizent’s research also revealed that Covid-19 has exacerbated the problem even further. Almost three quarters of those surveyed said the lockdown has impacted their executory work, citing financial institutions taking even longer to respond as a result of working from home.

Nick Cousins, founder and CEO of Exizent said:

“Our research shows that a significant majority of professionals think the time it takes to process probate cases is unreasonable, and that administration and waiting on institutions is taking up most of their time, yet most (85%) don’t have any technology dedicated to managing probate while 18% don’t use any software at all. “People’s lives are increasingly dispersed and varied. Performing executry work with a growing number of banks and institutions is more complex than ever. Without standardisation and the right tools available, too much time is wasted on administration. What this means for families is frustration, long delays and unnecessary anguish in trying to piece together what’s required to administer an estate and release assets to beneficiaries.

“However, with the right technology in place, we know professionals involved with estate administration could cut down the time and cost involved with managing probate cases exponentially and make the bereavement experience better for everyone involved.”

The Exizent online platform is specially designed for executry teams managing probate. Exizent is working with major banks, share registrars, and other institutions to build standardised requests and responses, making it easier for legal services firms and institutions to work together to sort out what is needed and making the process more efficient and easing the burden on executors and families.

Cousins’ and co-founder Aleks Tomczyk’s own experiences led them to establish Exizent. They felt that the administrative tasks facing families after the death of a loved one should be far easier.

They have spent the last 18 months carefully designing, developing, and testing the product with innovative partners, and, in September, successfully raised £3.6 million in funding from several investors including FNZ. It launched fully to legal professionals this month.

Photo by Andrew Neel from Pexels

New Chief Financial Officer for fintech Autorek

Kenny Bain will join Scottish fintech AutoRek, a leading software provider to global financial services, as Chief Financial Officer. He will play a key role in evolving and scaling the company.

Bain was previously Chief Executive Officer of Rant and Rave and is very experienced in financial leadership and operational management with a proven track record of delivering substantial growth in the software and technology sector, in the UK and internationally. Prior to this, Mr. Bain worked for 14-year at Graham Technology, as Chief Financial Officer, Chief Operating Officer and EMEA Managing Director, as the business expanded across the US, Europe and Asia.

“We are delighted to welcome Kenny onboard. He brings a wealth of invaluable experience from the software technology sector, which will no doubt make an enormous contribution as we continue to build on the success of AutoRek within the UK financial services sector and internationally.”

Gordon McHarg, CEO, AutoRek

“I am delighted to join AutoRek at this exciting time and look forward to working with Gordon and the team to deliver further growth. The business has a fantastic culture, a highly engaged team, a market leading product and is passionate about customer success – all positioning AutoRek perfectly to capture the significant opportunities that lie ahead.”

Kenny Bain, Chief Financial Officer, AutoRek, added,

£9m investment for Scottish fintech Modulr

Edinburgh based fintech, Modulr, just announced a £9 million investment from PayPal Ventures. This fresh investment will help the company develop new products, recruit and reach new clients.

Modulr let companies easily implement new payment products and services within their customer journey. The fintech provides a full stack Payments as a Service API, whilst taking care of the complexities and regulatory overhead. Modulr has a direct access to the

Modulr works with platforms that serve small and medium-sized businesses. This year has been rich in news for the company with the onboarding of new customers despite problems caused by COVID-19. Modulr connected to the Back scheme, the Faster Payments scheme, Visa and Mastercard.

“This investment marks an important milestone for Modulr’s modern payments infrastructure. Modulr lowers the barriers to bringing payments into a platform, creating endless new possibilities for our customers while allowing them to focus on their core competencies. The investment from PayPal Ventures enhances our ability to execute on that vision.”

Myles Stephenson, CEO of Modulr

“More digital businesses are looking to incorporate payments into their existing user experience but either don’t have the expertise or the resources. Modulr is well-positioned to be an enabler of this trend and will undoubtably expand end-users’ access to fast, reliable and secure financial services. We look forward to working with Modulr as it helps to powers the next generation of digital businesses.”

Anil Hansjee, partner at PayPal Ventures

In total, Modulr has raised £63.3 million including investment from PayPal Ventures, Highland Europe, Frog Capital, Blenheim Chalcot and a £10m grant from the Capability and Innovation Fund.

AutoRek to partner with iSoftware4Banks in the USA

It was announced today that Scottish fintech, AutoRek, would be partnering with iSoftware4Banks, a company based in the USA which provides solutions to support effective financial reporting and compliance.

With this partnership, AutoRek and iSoftware4Banks will offer their clients improved automation and better ROI. This will be achieved by bringing together highly experienced consultants and leading data management technologies.

Due to the current global epidemic, the financial sector, historically office-based, is moving towards different ays of working with many more people working from home. This change generates various operational issues across financial institutions. To adapt, those firms are reviewing their IT infrastructure, systems and outsourced services to future proof robust operational resilience strategies to ensure uninterrupted service. This is why this partnership was born, to help large financial companies achieve transformation whilst keeping on top of reporting and compliance requirement in a new and more efficient way.

“Our partnership with iSoftware4Banks comes at a crucial point of this year. As financial services firms consider their 2021 budgets after a turbulent year of operational risk, they will inevitably seek optimal value, which together we are confident in delivering.”

Head of Partnerships at AutoRek, Marc McCarthy

“We are delighted to be partnering with AutoRek to offer excellence in financial and operational controls to meet regulatory and compliance requirements. In-depth market research confirmed AutoRek’s solution is the best on the market, and we look forward to working together.”

Vincent Raniere, Chief Executive Office, iSoftware4Banks

Origo ”“ what are we working for?

Written by Anthony Rafferty, Managing Director, Origo

The other day a member of the team wrote this in an email to us all: “It’s so exciting how highly anticipated this service is ”“ we’re really doing the right thing for people in the industry.”

She was referring to a brand new service Origo had launched in the financial services (pensions, investment and savings) market, with which we had set out to tackle one of the most frustrating issues for the administrators, paraplanners (think para-legals for the financial planning market), financial advisers as well as the product providers and platforms in our industry. This is conveying the authorisation required from the client of the financial advice firms by the providers and platforms, stating that they are authorising the advice firm to act on and transact on their behalf; termed the Letter of Authority (LoA).

On the face of it you’d expect this to be a simple process and hardly an issue for an industry that transact billions of pounds every year. Right?

The actual situation is this: A myriad range of requirements and different pieces of information being required by providers and platforms; paper-based systems; pieces of paper having to be posted or faxed(!) to every individual provider/platform; no way of tracking the process, so no way of knowing if it is being dealt with or how long it will take. You can imagine the resource and cost implications all along the process chain.

Here’s a quote from someone on the front line:

“We offer an outsourced administration support, alongside our paraplanning services, and our administrators spend a lot of time finding out how a provider wants to receive the LoA (not everyone accepts emails and some still insist on seeing the wet signature, and these requirements seem to vary all the time), making sure the LoA actually got to the team which is supposed to be dealing with it and establishing current turnaround times, and finally chasing for information, often spending hours on hold each week only to be told there’s currently a backlog. Providers must also spend a lot of time answering these calls.”*

If you want to read further of the frustrations this is causing those dealing with this administrative burden, read this article on LinkedIn [ https://www.linkedin.com/pulse/sending-letters-authority-2020-debbie-condon/ ].

It’s written by Debbie Condon, founder of Intuitive Support Services, an outsourced administration firm for this market. She tells how she has had to put together a spreadsheet of 100 companies (there are many more in the industry) for her team of administrators laying out what each company needs and in what format and to which department the information should go. Needless to say, we asked Debbie to be one of the testers for our new service.

Hopefully, this gives a flavour of the issues and frustrations being experienced.

So, how have we tackled this. First, we did one of the things we do best, having identified the issue, we brought together a range of different industry participants to ascertain what they would need to create a common, efficient digital process that would meet the requirements of the industry and they would all be happy using.

From these working groups we developed the Unipass Letter of Authority service. Unipass is one of our brands ”“ 8 in 10 financial advisers use Unipass Identity for example to safely connect to the websites of the various providers and platforms they use on a daily basis.

In a nutshell, Unipass Letter of Authority enables the person in the financial advice firm to enter all the client’s details in a common format and for that information to be sent to all providers and platforms on the system. No laborious form filling for the advice firm and no postage cost.

Also, by securely digitising the process, Unipass Letter of Authority enables advice firms to know where they are in the onboarding process, so they can keep up-to-date with progress and keep the client informed, helping to improve their customer service.

This is a service that the industry tells us it has been crying out for and we are delighted to have been able to work collaboratively with participants in developing it. To accelerate the use of the service and the benefits it can bring to the industry, we are making it free to use until July 2021, allowing advice firms, providers and platforms to experience first-hand how the service will work for them.

I’m going to end with a quote from Debbie Condon: “What we need is for providers to sign up to this system as soon as possible. The more companies that are on board, the faster, easier and cheaper this process will become for the industry and the better the quality of service adviser businesses will be able to give to their clients.”*

Having this kind of impact on the efficiencies and for the people in our industry is what inspires everyone at Origo to be the best they can be in their jobs. The new Unipass Letter of Authority is just one of several innovative services we provide for our part of the industry and I am extremely proud of what we do as a FinTech to help address these issues.

An Edinburgh company doing its best to change the industry for the better.

Unipass Letter of Authority launches on 23 November 2020.

* Quotes from articles published by Professional Paraplanner magazine.

https://professionalparaplanner.co.uk/new-letter-of-authority-service-could-be-game-changer/

Obashi, first Scottish company to join the World Economic Forum’s Global Innovators Community

Scottish fintech Obashi has become the first Scottish business to join the World Economic Forum’s Global Innovators Community, an invitation-only group of the world’s most promising start-ups. It provides a tool to engage with public and private sector leaders and to contribute new solutions to overcome current crises and build future resiliency.

In their latest white paper, “A Roadmap for Cross-Border Data Flows: Future-Proofing Readiness and Cooperation in the New Data Economy”, the forum recently recognised that understanding dataflow is paramount when developing the Fourth Industrial Revolution.

“We are delighted to have Obashi join our Global Innovators Community,” says. We are excited to work with Obashi within the Data Policy Platform given their focus on data flows as a key to accessing the opportunities of the new global data economy”

Sheila Warren, Head of Blockchain, Digital Assets and Data Policy at the World Economic Forum.

Obashi provides a flexible dataflow governance model that enables any organisation to understand and unlock their dataflow potential.

“Dataflow underpins every industry on the planet, and it’s exciting and heartening to now see it being recognised as a vital global utility and a key component part of the Fourth Industrial Revolution. We’re delighted to be the first Scottish company to begin collaborating with the World Economic Forum and other technology leaders as part of the Global Innovator’s Community.”

Fergus Cloughley, CEO of Obashi

As part of the Global Innovators Community, Obashi will help define the global agenda on key issues with a particular focus on shaping the future of technology governance ”“ Artificial Intelligence and Machine Learning.

Ping Identity to acquire Scottish fintech Symphonic Software

It was announced today that identity solution Ping had acquired Scottish fintech Symphonic Software, who specialises in dynamic authorisation for protecting APIs, data, apps and resources through identity.

This acquisition comes after a couple of years of collaboration between the 2 companies during which they combined Symphonic’s authorisation platform with Ping’s data privacy and consent products. The combination of both solutions allows their clients to centralise administration and enforcement of critical resources and data for all types of users, applications and devices in a language that is easily understood.

“With increasing data privacy regulations, users are demanding that enterprises give them better digital experiences with more transparency and control. The acquisition of Symphonic accelerates our vision for enterprises to not only maintain security and compliance with confidence, but to easily deliver personalised, trustworthy experiences.”

Andre Durand, CEO and Founder of Ping Identity

The features offered by both companies help companies avoid costly bespoke integrations thanks to native services that are at the centre of identity platforms like users, groups, entitlements, consents, and risk.

“For the past two years Symphonic has worked alongside Ping to make policy management easy for enterprises. Ping Identity’s dedication to their customers aligns well with Symphonic’s values, and we are thrilled to continue our journey together as one.”

Derick James, CEO of Symphonic

Fintechs Worldline and BRIDGE announce partnership

Worldline and Scottish fintech Bridge announced today a technology partnership. BRIDGE will integrate its eCommerce payment consolidation and control features into Worldline’s UK rail eCommerce platform.

Worldline’s eCommerce platform is a very innovative customer-facing service adopted by major transport providers. It helps people along the full booking process from journey planning to payment.

Thanks to this partnership, Worldline’s customers will be able to take control of the end-to-end payments experience whilst connecting transactions with other business processes.

James Bain, CEO, Worldline UK & Ireland, said,

“We believe in collaboration for innovation, ensuring that, through our partnerships, we always have the most inventive technologies built into our solutions. Working with BRIDGE’s specialist strength in payments integration and control means that we will be quicker in bringing a more agile and resilient payment ecosystem offering to our customers. It aligns with the Worldline vision of payments for a trusted world.”

Mobility-as-a-service’ is a growing trend and with it appears the need for a on one-stop platforms to deliver convenience, comfort and flexibility. This partnership ensures that Worldline is equipped to deliver such a platform.

Brian Coburn, CEO at BRIDGE, said,

“For transport companies and their customers, the ticketing system is so much more than a permit to travel ”“ it’s a key part of the customer journey. Given its influence on trust and satisfaction, we see payments as an engine for opportunity and differentiation today and into the future. Through our partnership with Worldline, we look forward to seeing our innovation at work within a world-class transport eCommerce system and showcasing its impact on a frictionless customer experience.”

BRIDGE is a new payment orchestration service, offering a single horizontal integration layer across the retailer’s payment system that manages, consolidates and controls multiple payment offerings, as well as providing data reporting and analytics, and the ability to deploy and test new innovations at speed.

Scottish fintech Exizent secures £3.6 million funding

Exizent, just announced it had raised £3.6m investment to completely reinvent how the legal and financial services sector deals with bereavement making it less stressful for families.

The Scottish fintech is working on the first ever platform that will connect data, services and the network of people involved when someone passes away. Exizent’s objective is to make the process less uncertain and significantly faster and simpler.

Co-founders Nick Cousins and Aleks Tomczyk both have an impressive track records of building successful products and businesses. Aleks founded the very successful fintech Arum before selling the business at the end of 2017. Nick was previously Chief Product Owner of Barclays Wealth and Investments division.

The investment announced today involved several investors including FNZ, the global platform-as-a-service firm which reached unicorn status in 2018.

Nick Cousins, Founder and CEO of Exizent, said:

“Our personal experiences are what led to us to establish Exizent. We believe the administrative tasks facing families after the death of a loved one should be far easier, and that modern technology solutions and services can make this a reality. We have spent the last 18 months carefully designing, developing, and testing our product with innovative partners, and look forward to launching the platform to legal services professionals later this year.”

Adrian Durham, Group CEO of FNZ said:

“The Exizent team has already achieved an enormous amount and we are proud to support their vision of leveraging technology to make the bereavement process far easier for everyone involved. Exizent will also be joining the fast growing FNZ OpenPlatform App Store.”

In the next few months the company will focus on helping legal services firms, working for executors, efficiently manage the process of completing and submitting probate applications (confirmation in Scotland). It will also make the process of gathering information about an estate easier by connecting third parties to automatically discover assets the person may have had, reducing the reliance on an executor to find and send physical documents.

The company also plans to build digital connections with the various institutions that hold data and information about the person who has passed away to help them deal with queries from executors and legal services firms more efficiently.

Scottish fintech selected for fintech growth programme

Vistalworks just announced it has been selected for the UK’s fintech growth programme.

The company will be part of the Tech Nation’s Fintech 3.0 cohort, delivered as part of the UK Treasury’s fintech strategy.

The growth programme aim to provide coaching and networking to some of the best fintech firms in the UK so they can develop new solutions to support the UK economy.

Vistalworks’ solution allows financial institution to fight fraudulent transactions and reduce consumers detriment thanks to a state of the art software that creates risk profiles for sellers and products. The new technology also sends alerts to governments, police, specialist agencies, consumer protection bodies, and corporations such as banks.

Thanks to a browser add-on, consumers can also check products are licit before buying them.

Vicky Brock, chief executive and co-founder of Vistalworks, said:

“Our technology protects consumers and businesses from harmful online criminal sellers at every stage of the transaction, and we want to expand our reach.

“Our goal is to enable banks and payments providers to be more proactive in preventing high risk illicit transactions that lead to consumer harm and costly claims and refunds.

“Illicit trade is the biggest funding source of organised crime and directly harms economies, the environment, businesses, citizens and their communities.

“We want Scotland and the UK to be at the forefront of the fintech innovation that will help tackle this problem.”

Stephen Ingledew, chief executive of FinTech Scotland, said:

“The inclusion of Vistalworks on the Tech Nation programme is terrific recognition of Vicky Brock and the team’s exciting and innovative proposition in addressing consumer and business challenges of financial crime.

“The development of proactive tools to deal with high risks transactions handled by banks and payment providers has never been more important in the emerging digital economy and I am inspired by how the Vistalworks team are pioneering innovative approaches which will benefit consumers and businesses.”

Lynne Cadenhead, chair of Women’s Enterprise Scotland, said:

“We are delighted that Vistalworks has secured a place on the Tech Nation Fintech programme.

“Founder Vicky Brock is both a vocal supporter of women in STEM and an active Women’s Enterprise Scotland Ambassador.

“As a visible role model, she inspires other women and girls to pursue careers in STEM industries and we know that diversity is a key driver of innovation.

“This in turn fuels economic growth, making gender diversity a key component in rebuilding our economy after the impact of the COVID-19 pandemic.”