Are You Ready for Blockchain? Collaboration Could be Key

Photo by Hitesh Choudhary on Unsplash

It’s undeniable that blockchain is a complicated and, at times, daunting technological development. Having said this, the opportunities proposed are as exciting as they are complex. From reshaping business transactions to the secure and accurate exchange of data – blockchain has the potential to improve nearly every financial service industry.

This poses an issue of great internal debate for businesses in markets which could truly benefit from the traceability, security and wider potential presented by blockchain.

As a business, should you invest in tech that could ultimately revolutionise your capabilities at the risk of encountering stumbling blocks? Or, do you sit back and watch while others in your sector pick up the early adopter mantel?

Collaboration could be the answer.

Here, we delve deeper into this dilemma faced by businesses considering incorporating blockchain technology into their wider strategy, and help answer the question; is your business ready for blockchain?

What is the impact of blockchain?

Blockchain is far more than just a channel for cryptocurrency and can offer far reaching business applications. Here are some of the key impacts blockchain could have on your business:

- Automation

- Transparency

- Autonomy

- Security

- Reduced error handling

- Member accountability

How can blockchain help businesses?

When considering whether blockchain is a worthy investment for your business, it’s important to consider what its wider applications could be. This technology can provide clear solutions to challenges in wide-ranging sectors. However, as a business owner, you need to be sure that the investment will benefit your company.

Here are just a few ways blockchain could benefit your business:

- Shared data across several participants or external parties

- Access to edit or update information needed by multiple participants

- Recorded verification and security of participants and users

- Reduction of cost through decentralised record keeping

- Time sensitive information sharing and updates

- Instant, interactive transactions between different participants

- Improved capital optimisation

Should you consider blockchain for your business?

No one is disputing that blockchain is going to become increasingly influential over time. Having said this, it simply isn’t needed by everyone at this stage. If you’re sitting on the fence, there are many points to consider.

Blockchain shouldn’t be considered as an aspiration to achieve for your company. It’s an enabler to aid in the efficiency or cost reduction of your existing processes. Don’t position this technology as a capability which validates your business’ proposition. Instead, it’s a tool to improve your business models and dealings with other companies. If it’s not addressing a current issue or opportunity, it simply isn’t for you at this stage.

Finding your opportunity

Monitoring the way distributed ledger or blockchain technology is used in similar industries is a great place to start when seeking potential opportunities. It’s important to be aware of any competitors who attempt to leverage this tech before you as it may leave you at a serious disadvantage later on.

Consider whether your business could work smarter’ using blockchain and whether you can leverage enough influence to truly benefit from doing so.

What Can EEN Offer Your Business in Terms of Collaboration?

Enterprise Europe Network (EEN) provides a network of specialist support to help companies do business in Europe and beyond. From helping with access to funding to finding trusted partners, EEN can help your business grow internationally.

Here’s how EEN can help:

- Improve the way you manage innovation

- Track down long-term finance from public and private sectors

- Provide a network of world-wide advisers

- Help you find trusted partnerships

- Help you expand into new markets and countries with help from local experts

- Expand and scale-up your business

With hundreds of collaborative partnership opportunities available, EEN allows you to search for SME and academic business partners to develop your products, ideas and services.

Current Opportunities with EEN

Here are some examples of live opportunities available through EEN:

- A UK business is offering a blockchain based employee background checking toolkit to make employee checks more efficient.

- They are looking for organisations that are seeking improvements using automation, candidate experience, candidate privacy and modernising employment checks.

- A London company has developed a next generation private, permissioned blockchain development platform. The platform enables businesses to take advantage of the benefits of the blockchain and apply them to business solutions and applications.

- They are seeking partners to sign commercial agency and license agreements across a wide range of industries to pilot test their built platform.

- A London based start-up is seeking a software developer with relevant technical skills in AI, ML and Blockchain to develop a professional social media and communication cost centre management platform.

- The business wishes to develop service agreements with businesses possessing the technical expertise that will help the company to realise its vision of disrupting technology in the healthcare industry.

- A Portuguese SME specialising in software as a service (SaaS) solutions for fintech and business communication is looking for partners to cooperate under a commercial agency agreement.

- This SME is interested in commercial agency agreements with international partners to pursue their scale-up strategy in European and non-European markets.

How to ensure you’re ready for the implementation of blockchain

Is your business ready to begin blockchain implementation?

There are several factors to consider;

- Commercial gain – is there a value to be taken from this technology?

- Compliance – will this technology comply with the regulations your business is required to meet?

- Execution – do you have the right skills and resources to actually make this work?

- Technical capabilities – can the technology be seamlessly integrated?

- Transparent operations – have you planned a fair and transparent way of governing the wider operational aspects of integrating this technology?

Partnership Opportunities in Blockchain

Enterprise Europe Network (EEN) helps businesses to find global partnership opportunities with SMEs or academia to help manufacture, develop and supply their products, ideas and services. If you’re considering implementing this technology into your business, explore EEN’s blockchain partnership opportunities.

Fortnightly FinTech Fuse ”“ Exhilarating FinTech Energy!

The fintech energy across Scotland is just so exhilarating in so many ways!

It is an energy that is driving the rapid growth of the fintech community and this has been wonderful to experience again at first hand over this last few weeks.

Innovative Energy

For example, innovative energy has been very much in evident at a variety of meetings such as with Stephen Henry of the exciting Asura Financial as well as with Laura Bosworth and Mel Alexander from the awesome Amiqus team.

Then there were the engaging discussions with Chris Herd of Nexves and Kevin Hollister and Keith Harrison of Guiide at the Scottish FinTech meet up. Big thanks again to Scottish Fintech stalwarts Sergei Miller Pomphrey and Bobby King for being at forefront of community energy.

Last week it was a fascinating catch up with Garry Williams of Phoebus to talk about his innovative future plans and potential for expansion in Edinburgh.

Earlier in the week it was another wonderful meet up, this time with the very special Fife Fintech community to catch up with old and new friends.

Thank you to Iain Shirlaw for the celebratory cake and organizing a valuable discussion in the Adam Smith Theatre in Kirkcaldy.

I get a lot of my energy in seeing the fintech community come together, such as at the University of Edinburgh Futures Institute meeting on Wednesday evening.

Wonderful to see energetic entrepreneurs Helene Rodger of MoneyMatix, Christian Burgin of Visible Capital, George Kelsey and, very new to the community, Nanik Ramchandani of Trade Phi.

It was a great mixer’ event organized by Gbenga GB’ Ibikunle from the University of Edinburgh to share the developments of the fintech cluster being led by the University of Edinburgh

On top of all this engagement there have been some magnificent news from a range of innovative enterprises.

Modulr raising £14m capital to grow, LendingCrowd raising nearly £20m to support SME growth, Money Dashboard hugely successful crowd funding of £2m in 24 hours and then Soar receiving a major financial injection to take their innovation to the next level. Wow!!

These examples of the vibrant fintech community in Scotland is something I find myself sharing with global innovators and entrepreneurs on almost a daily basis on phone calls and in meetings.

For example, it was great to catch up recently with Ambreen and Sophie from Monese to hear about their exciting journey and the potential of being in Scotland.

Then it is spectacular to see all this come alive on line and in print through the Scotsman Fintech supplement this week.

Huge thanks to the brilliant David Lee for leading on such a comprehensive supplement and to the Scotsman team for bringing Scotland’s fintech progress alive.

Collaborative Energy

The innovation across the fintech community really comes alive when combined with the collaborative energy from a range of participants.

This is a theme I shared at the awesome Fintech North conference in Leeds on Thursday.

Building on the success of the Manchester conference, this was another wonderful occasion and it was a privilege to be part of the event with a really buzzing atmosphere.

It was an opportunity to meet a diverse range of people from the Leeds community including David Hoghton-Carter, Glynn Robinson, chairman of BJSS, Daniel de Wolf of Flybits and Andy Thompson (again) of Sandstone. All I hope to see in Scotland soon.

As well as people from the broader fintech ecosystem, David Beer of Fintech Alliance and Peter Cunnane and Clare Black of Innovate Finance. Clare led on terrific session on Fintech and diversity in the afternoon sessions.

Over lunch it was great to catch up with the engaging founder Kyle MacDonald and non exec director Mark Spink of Scottish fintech Financial Cloud to talk through collaboration opportunities in Glasgow especially in the credit union sector.

Also, terrific to meet up with international guests Muhamed Farooque of Excelledia and Kyoungrok Lee and Min Sungjun from Samsung Life, all of whom I look forward to welcoming to Scotland next month.

Thank you once again to inspiring FinTech North leaders Julian Wells and Chris Sier as well as the fabulous Fintech North and Whitecap Consulting and White Label Crowdfunding teams. Magical

Very much looking forward to hosting the FinTech National Network meeting in Edinburgh in June and the collaboration conference in the Autumn in Glasgow.

One area of collaboration I highlighted to people was between fintech and the public sector. For example, the work to develop a new payments platform with the Scottish Government is a hugely exciting collaboration opportunity for fintechs.

It is a real pleasure to be working with inspiring leaders Trish Quinn and Hugh Wallace along with the impressive team Clare, Martin, Alex and Carron at the Scottish Government.

Very much looking forward to the buzzing energy at the collaboration event in June to share more with the fintech community and wider stakeholders.

On the subject of large scale collaborative energy, fantastic to see the news about Lloyds Bank major tech job expansion in Edinburgh.

Last week I was delighted to be invited to the Lloyds Bank pre AGM dinner to talk with Chair Norman Blackwell and give examples of Lloyds Bank energetic support of the fintech community in Scotland.

The collaboration energy was very much part of the discussion with the CYBG Innovation Team a week ago as well.

Great to have such an engaged and imaginative audience looking to develop even closer working relationship with the fintech community.

Many thanks to the inspiring Sam Bedford, Gary McLellan and Jack Mckenna, looking forward to progressing the opportunities.

Also very much encouraged by the meetings with the Barclays team, Ben Davey and old colleague Steven Roberts, especially with the exciting build of the new Barclays campus in Glasgow.

Thanks also to Colin Carmichael and the Sopra Team for a terrific working session with Mark Daisley and the BNP Paribas team

I am very encouraged by the large financial services institutions who are looking to work with us to bring the fintech community in to a closer working relationship to support innovation.

Many thanks to Ali Law of Royal London and David Skinn of Aviva for valuable conversations over the last week or so.

A completely different area where the collaboration energy is beginning to be so powerful is our fabulous engagement with the Money Advice Scotland team

It was very much a huge privilege for me to present at their annual conference in Dunblane on Friday as a double act with my colleague Nicola Anderson.

Infact, it was really quite emotional, as the work of the front line money advisers is something I have recognised as hugely valuable since my childhood.

Just magical to be there with real experts who are focused in supporting people when faced with the most difficult of financial circumstances.

Very much appreciate Yvonne McDermid and David Hilferty giving me us the opportunity to share the role of fintech in supporting their work.

Expert Energy

This expert energy is crucial to the thriving fintech ecosystem and the universities play a crucial role.

This also was a key theme at the Fintech North conference, and it was great to be on the stage to discuss this with Chelsea Hardy, Andrew Maeer, Iain Clacher, George Lodorfos and expertly chaired by Eve Roodhouse of Leeds Council. Very much a shared agenda of inclusive growth.

I am thoroughly enjoying working with the brilliant expert team at University of Strathclyde, Daniel Broby, Devraj Basu, Martin Hughes and James Bowden in developing the plans for the fintech cluster in Glasgow.

Their expertise in bringing together the academic intellect with entrepreneurial new enterprises in the magnificent Technology and Innovation Centre in Glasgow is certainly fueling fintech energy and enterprise.

Bringing together the consortium of stakeholder expertise across the central belt in Scotland is a huge strength in developing the Global Open Finance Centre of Excellence.

My meetings this last few weeks with a cross section of key players such as Simon Pink and Mairi Cairney of IBM, Anneli Ritari-Stewart and Richard Gill of Dentsu Aegis as well the brilliant team at Edinburgh Chamber of Commerce, Liz Mcareavey and Alex Haramis very much reinforce this.

Broadening the potential range of experts contributing and supporting fintech is key and it was valuable to discuss this with Graham Burns, John and Nia from FWB Park Brown team. Very much looking forward to working with the Aberdeen community on this

Earlier this week I delighted to have the opportunity to share progress on the Global Centre of Excellence with Government Minister Ivan McKee.

Damien McGarrigle and Kevin Collins are doing an excellent job on leading the initiative along with the awesome Gavin Littlejohn driving the amazing global engagement.

The open banking and finance opportunity was highlighted recently by Caroline Stevenson of Womble Bond Dickinson in a great article in the Scotsman.

I had the opportunity to learn about Caroline expert work as part of a six mile running meeting’ around Arthurs Seat one very early morning this week.

What could be better than combining my two passions of running and fintech!

Running Energy

I am going to need all the running energy I can muster this weekend with the Edinburgh marathon on Sunday!

Being only six weeks back from an eight week injury lay off, I know I will need to take it steady over the 26.2 miles, so the pressure is off in many ways when it comes to how fast I go.

This will be the first of three marathon this year and I’ve been helped back to running fitness with a couple really enjoyable races in Coatbridge and Balerno over the last couple of weeks.

The latter made all the more enjoyable on a lovely Monday evening by running most of route with Carron Macnab of Scottish Government when we ended up talking as much about fintech as running!!

Maybe talking fintech is the secret for the marathon this weekend but who will I find to chat with!! Until next time.

Scotsman fintech event: what has fintech ever done for us?

Fintech has made a huge impact on the financial services sector and the wider economy of Scotland ”“ but what did it ever do for us?

That’s the subject of a quick-fire panel discussion at Strathclyde Business School in Glasgow on Wednesday, 5 June, with experts from across the fintech field, including Nicola Anderson of Fintech Scotland, Professor Eleanor Shaw of the University of Strathclyde and Louise Smith, Head of Intelligent Automation at RBS.

The panel is completed by young entrepreneur Daniel Sloan of BankPal, Chris Brown of Deloitte and Callum Sinclair of Burness Paull.

If you are a member of the fintech community, or interested in the sector in any way, we would love to see you there for the rapid-fire discussion around seven key topics, each representing a letter of fintech:

FINANCIAL INCLUSION

Last year’s discussion asked if fintech could be an agent of positive social change. How are we doing in terms of financial inclusion and does fintech in Scotland still have that social purpose?

INNOVATION

How is the sector coming together in a collaborative way to deliver genuine innovation, through initiatives like the Glasgow City Innovation District? Are we seeing any tangible outputs?

NEXT GENERATION ENTREPRENEURS

How is Scotland doing at creating a generation of fintech entrepreneurs who can provide the economic powerhouses of tomorrow?

TRUST AND TRANSPARENCY

What are Scottish fintech businesses doing to build customer trust ”“ and are they being fully transparent about their use of data? Can Scotland use trust and transparency as its fintech USP?

EMPLOYMENT

Last year, Fintech Scotland’s company map had 40 businesses on it. This has now doubled to 80-plus. Scotland is also attracting fintech jobs in large financial institutions. Is fintech starting to drive significant employment growth?

CONSUMER DATA

As consumers become more aware of the importance of their data to large tech companies, how can fintech help them to realise value from that data?

HOME-BUYING JOURNEY

How can fintech have a positive impact on the way we buy and sell homes? Does it have the power to bring together the whole home-buying journey in a simpler, more seamless way? And can this approach be rolled over into other aspects of our lives, such as travel and tourism?

To book your free place to this event click here: https://www.scotsmanconferences.com/

Helping to build Scotland’s digital expertise

Blog written by Anthony Rafferty, Managing Director at Origo

This week Origo was delighted to welcome Kate Forbes, Minister for Public Finance and Digital Economy to our Edinburgh headquarters to talk about the critical tech-based services Origo delivers for the financial services sector, as well as our commitment to the future generations through our apprenticeship scheme.

We wanted Ms Forbes to see the important work being developed in Scotland and how we as a company invest in our digital skills, including development of relevant apprenticeships, to enable us to deliver industry critical services to the rest of the UK.

Origo is committed to developing digital skills both within the Scottish FinTech sector and within the company, and as well as being introduced to staff generally, we were pleased to be able to introduce Ms Forbes specifically to our apprentices and Cyber Security graduate apprentice, Taylor McAuley.

As Cyber Resilience is important to Scotland’s digital economy, Ms Forbes was also briefed on Origo’s digital ID service, called Unipass, that is used by 8 out 10 financial advisers in the UK to securely access digital services from financial providers and platforms.

We were also proud to provide a demonstration of Origo’s world-leading Pension Finder Service for the Government’s Pensions Dashboard project. The role of Pensions Dashboards is to find and display an individual’s pension savings on one screen and is intended to encourage people to engage with and, where appropriate, take action on their retirement income planning.

Origo has been heavily involved in the Pensions Dashboard project from the outset in 2014 and we are excited by the potential for Pensions Dashboard to not only benefit millions of individuals and potentially improve their financial outcomes, but also help to drive further innovation by facilitating an open pensions environment.

Commenting on her visit to our Edinburgh headquarters, Ms Forbes said:

“Origo looks set to reinforce Scotland’s reputation for high quality and innovative digital skills and services. The FinTech is investing in our youth through development and support of apprentices and a graduate apprentice as well as recruiting from a specialist digital academy, Code Clan.

“Origo’s innovative Pension Finder Service will be critical to the Pensions Dashboard project and will also enable other and different FinTechs to get involved in delivering technology such as user interfaces and integration services.

“Scotland is a highly competitive business location, with investment built around the quality of innovation and the digital skills of our workforce. Companies such as Origo can play a big part in making Scotland a centre of digital excellence.”

Alastair Ross, Head of Public Policy (Scotland, Wales & Northern Ireland) for the Association of British Insurers, also attended the Minister’s visit. He added:

“Millions of savers stand to benefit from a pensions dashboard system ”“ an initiative with cross-party support and the backing of consumer groups ”“ which will give everyone much easier access to information about their own retirement prospects. The ABI, having led a cross-industry group of pension providers, pension schemes and FinTech companies, has already delivered a great deal of the work needed to make Dashboards a reality and we look forward to continuing this collaboration with Government.”

Origo was formed 30 years ago in Edinburgh, making us one of the UK’s longest established FinTechs and we are proud of our long history at the forefront of innovation in Scotland’s and the UK’s financial services industries.

We are dedicated to improving the financial services industry’s operating efficiencies, lowering costs for market participants and improving outcomes for consumers. We work collaboratively with government, other industry bodies as well as product providers, platforms, financial advisers, portals and software suppliers, to find new ways to cut costs and make processes more efficient.

Fortnightly FinTech Fuse ”“ The Energy Fueling FinTech!

There has been a frenzy of energetic fintech activity over the last few weeks even with the interruption of a sunny Easter break.

I’ve seen this energy fuel innovation and collaboration across a diverse range of engaged fintech participants and it is really exciting to be in amongst the activity.

For example, a couple of weeks ago I had the privilege to judge to the fintech innovation pitches by the University of Edinburgh entrepreneurship students along with David McLeay from Scottish Widows.

I was blown away by the students creative and imaginative new business models to reinvent financial services, many of which could complement propositions being developed by Scottish fintech firms.

Congratulations to Ben Spigel, the Chancellor’s Fellow at the Business School, for leading such a talented group of students. Many of whom I am sure we will hear about in the fintech community in the future.

Energetic Talent

Another example of this energetic fintech talent was catching up with Elisabetta Trasatti and Andrea, the very inspiring President and Vice President of the University of Glasgow Student FinTech Society

Absolutely fantastic to hear about their plans for the year for the Society, recognized as one of the largest student fintech student groups in Europe, and how they are engaging with the fintech sector.

Excited about working with the team, especially looking forward to an energy charged evening with Jazz band and more at the Society’s pitch final competition later this year!

My meetings with the brilliant team at University of Strathclyde have further demonstrated how much terrific energy is going in to develop the fintech talent for the future.

I am very excited to be working with the fabulous Martin Hughes, Daniel Broby, Devraj Basu and Tim Bedford in shaping the emerging fintech cluster in Glasgow and connecting with the financial services sector.

Similarly, working with Ksenia Siedlecka and the University of Edinburgh team on the development of the newly launched European FinTech Digital Office focused on new research areas and investing in new enterprises.

There’s a huge amount of interest in the fintech collaboration event being planned for June and it is great to be working with our European colleagues and fintech firms such as on this initiative.

On Tuesday it was great to catch up with the fabulous Michael Young whose energetic MBN Solutions team do so much in supporting development of talent for the sector.

Michael and the team bring a huge amount of energy to the collaboration initiatives across Scotland, especially through their very successful meet up programme.

Energetic City Collaboration

Later that evening on Tuesday, Michael as well as Elisabetta joined me at the Glasgow Economic Leadership meeting where skills development and collaboration were a key part of the discussion.

I very much appreciated the engagement of the group on how we further develop fintech collaboration across the City and thank you to Mark Napier, and JP Morgan for hosting the session.

This energetic city collaboration was also very much in evident when I was invited to present at the FinTech North conference in Manchester a couple of weeks ago.

A wonderful atmosphere generated by a diverse audience and terrific fintech entrepreneurs sharing their innovative propositions to a very engaged audience.

For me it was also special to meet up with some great entrepreneurs such as Adam Bickell of Jamtoday and David Smith a wonderful colleague from 20 years ago, who gave an awesome presentation explaining the Uinsure proposition

The FinTech North conference captured everything that is so special and energetic about the fintech movement and it was a real privilege to be part of it.

Huge thanks to the inspiring leaders Chris Sier and Julian Wells along with the whole FinTech North and Whitecap Consulting team for delivering such an innovative community driven occasion.

I was given the opportunity in Manchester to share the stage as well as catch up with the terrific Charlotte Crosswell, chief executive of Innovate Finance

It was a recognition of our shared values for the ambition for the fintech movement and the mutual opportunities that prompted us to agree to more formally collaborate going forward.

Hence the announcement on Monday this week of a new Fintech National Network to provide collective support for FinTech Scotland, FinTech North and Innovate Finance fintech communities.

Our aim is to see our collaboration activities and engagements provide more support and we are looking forward also to FinTech Wales and FinTech Wales joining with us in the coming months.

The new Network was announced at the Innovate Finance Global Summit in London which a number of the Scottish fintech community attended.

Including Professor Jane Lewis from Womens Coin, a newer member of the Scottish community, who was invited to share how the exciting developments were taking shape in Scotland. Big thanks to Jane.

The week before was another global event, EIE 2019, with many Scottish fintech firms taking centre stage to share their propositions to an international investor audience. A huge accolade must go to Steve Ewing and the team for a fabulous occasion

Big congratulations to everyone who participated, and a special mention to Callum Murray of Amiqus for winning pitch presentation of the day.

Global Energy

Scotland’s fintech activity is certainly attracting global energy, for example it was terrific to welcome the delegation of Hong King and Singapore fintech innovators to Edinburgh on Thursday.

It was great to share the Scottish fintech developments with a diverse range of firms in the morning with Graham Hatton from Scottish Development International.

Then in the afternoon, to have an engaging session in the afternoon with our friends from the Far East with a fantastic mix of people from Scotland’s fintech community, considering collaboration opportunities.

Great to meet Bettina Wong and Charles Lam of Cybersport and Avere Hill of Cynopsis, Ivy Tse of FreightAmigo as well see Joel Ko, again who has exciting fintech plans for Edinburgh

All brilliantly hosted by the fabulous Kent Mackenzie, Chris Brown and the Deloitte team who are doing so much to develop the global fintech collaboration and energy.

The event with a global diversity was wonderful to be part and embodies everything that Scotland’s fintech is all about. All fantastically organized by Karen Craib and Mandy Cooper from Scottish Enterprise.

Sandwiched in between the two events I was given the opportunity to talk about embracing diversity through fintech at the Women in Banking and Finance conference on Thursday.

An absolute privilege to be on the stage in front of a big audience with the inspiring Sue Liburd, Wincie Wong of RBS and Maggie Craig of FCA.

All expertly hosted by the fabulous Andy Nicol, chief executive of Abstract, who do terrific people leadership work in this space.

Many thanks to Niamh Sims and Nomi Puri for inviting me to join you and for a terrific event and energetic atmosphere.

Scotland is certainly contributing to the positive global energy, for example, it was great to catch up with Chris Tait and Omar Shaikh to discuss the fintech participation in their Global Ethical Finance conference

Delighted we are working together on this global exciting event in October which very much reinforces Scotland’s leadership role in sustainable finance as well as fintech.

Also, on the global energy theme it was a pleasure to catch up this week with Gurjit Singh Lalli, the curator of TEDx for Glasgow, about the amazing event planned for June and future role for the fintech community.

I am hugely excited about the global energy being generated by the planned fintech festival for Scotland in September which Mickael is working hard on.

Excellent strategy meeting with the terrific Rory Archibald of Visit Scotland and Karen Craib of Scottish Enterprise who are doing such fantastic work to help us prepare for the festival later this year.

Talking about how we build on this global energy with developing the strategic international opportunities for Scottish fintechs was the key part of the valuable discussion with Lorraine Mallon and Andrea McLeish from SDI this week.

Strategic Energy

Sharing the strategic energy behind the fintech developments in Scotland is always a key role and there have been so many interactions over this last few weeks to do this

For example, we very much valued the opportunity to present to the team at the Financial Conduct Authority and great to meet the teams shaping the regulatory landscape for future fintech progress and good consumer outcomes.

Thank you to Ed Smith and the team for arranging with Nicola for this. We followed this up with a great conversation with Tom Kegode and the innovation team at Lloyds Bank who are leading some terrific strategic fintech collaboration initiatives

Over this last few weeks I have also had the opportunity to discuss the strategic developments with other major financial groups

For example, very enjoyable and constructive conversations with Ali Law of Royal London, Peter Bole of CYBG and Bob Hair of Cazenove.

Along with exploring strategic fintech collaboration opportunities with Jim McCumesty of SAS, Neil Delany of Contis and Kirsty Irvine of JCCA. Brilliant to have their engagement win working with the Scottish fintech community.

On Monday, I had the opportunity to share FinTech Scotland future plans with a broader engaged audience at the FiSAB (Financial Services Advisory Board) quarterly meeting chaired by the First Minister and Jim Pettigrew of CYBG.

It was great to have fintech on the agenda along with the terrific work being led by Barry Connolly of RBS on skills and Helen Page of CYBG on the social impact of financial services.

Both significant pieces of work align with the fintech developments on skills and inclusion and it was great to continue the conversation on these at the Scottish Financial Enterprise AGM on Thursday evening all expertly organized by the magnificent SFE team.

Thank you, Graeme Jones for the FinTech Scotland progress shout out great to be there with the SFE members. Many congratulations to the awesome Sue Dawe for being elected to the SFE Board

Energetic Running

After an eight week injury lay off, I am back out running energetically and what a really amazing feeling in so many ways.

This included a return to the race circuit with the Stirling half marathon last Sunday which was just wonderful.

Coming up are races in Coatbridge, Dalkeith and Balerno as well as a few Saturday morning Park Runs, all before the Edinburgh marathon at the end of May.

Although I’m having to control my running energy at the moment, so I don’t pick up another injury but despite this I have fallen in love with running event more!! Until next time

How AI helped Interactive Investor with Customer engagement

Photo by Markus Spiske on Unsplash

Blog by Michael Mauchline, Industry Leader, Marketing Automation & Personalisation at Watson Marketing

Very often when AI and investment are mentioned together it is about Robo Advice or high frequency trading. However, in the case of Interactive Investor AI proved useful for customer engagement.

IBM Watson Marketing works with Fintech clients to improve customer engagement as well as boost digital revenues. Interactive Investor deployed the technology in 2018 and have since been able to inspire thousands of customers to actively engage in their portfolios:

- increased newsletter open rates by over 80% through personalising content based on a customer’s segment

- improved clickthrough rates more than 70% by sending emails to customers at optimal times based on an individual’s behavior

Those results were achieved by the personalization of investment content based on customers’ segments. Going beyond segment, personalization was achieved for each individual.

Personalisation isn’t all to do with the content itself but also about send time. By learning about people’s habits IBM Watson was able to send email at the most appropriate time for each individual.

Head of CRM at Interactive Investor, Phil Ireland explains how this happened:

“IBM Watson has been an integral tool over the last six months in helping my team achieve specific objectives set by our business. The platform has allowed us to dynamically target our customers with personalised information. For example, the platform has allowed us to target customers who hold any of the top 20 stocks within our business dynamically with news relating to that stock and provide updates on the performance of each stock.”

“The platform has allowed us to automate our new customer welcome journeys and provide trigger based campaigns dependent upon customer behavioural actions. We’ve seen considerable uplifts in our KPI’s due to the impact of the IBM Watson platform.”

Read the full story at:

https://www.ibm.com/case-studies/interactive-investor

About Watson Campaign Automation

Watson Campaign Automation is a SaaS-based digital marketing automation platform that puts the power of data insights in the hands of the marketer to design smarter campaigns that exceed your customer expectations. Use behavioural data from any source to create consistent campaigns across email, web, mobile push, SMS, social, group messaging and more. Marketers can work smarter with an AI powered Watson Assistant for Marketing’.

- Improve Customer Engagement

- Boost customer engagement and conversion with personalised experiences and offers that connect with your customers, when and where they expect it.

- Increase Customer Loyalty

- Leverage AI-powered insights and capabilities to deliver the right message and offer at the right time in the right channel to grow customer loyalty and, ultimately, revenue.

Any questions? Contact Michael Mauchline 07764 666 813 mauchline@uk.ibm.com

What the heck is that on my Bank statement?

We have all asked that question at one time or another, fretted and then called our Bank to see if it is fraud. Unfortunately, Banks know less than we do because the payment processors do not tell them what a transaction was for. The majority of these calls are about online purchases so friendly call center staff request that we check our email for a receipt.

For this reason I opened my pitch at EIE19 with the statement, With purchasing going on line, there are now 200x more email sent than there are Google searches’, grabbing the attention of the packed University of Edinburgh’s McEwan hall (my thanks to Danny Helson and the EIE team for an amazing event). It went down well, two days later I was pitching to a smart bunch of investors at ESM Investments.

The cost of not knowing

Finding an email receipt for the corresponding Bank transaction is almost impossible, email has become a dumping ground for spam, phishing and promotions. But it’s not just Fraud we worry about, we often want to find the receipt to return goods or use it to process a business expense. Banks also suffer, they field 6 million calls a year from customers concerned about online fraud (UK Finance.org reported that 78% (£393.4 million) of all fraud was online), at an average cost of £5 per enquiry, this costs the industry in excess of £30m a year. If Banks knew what was purchased they could make our customer experience better, for example, offering personalised Travel insurance to someone travelling abroad or putting an Uber button in their App to book the onward taxi and pushing the Uber receipt to the Expenses system to be automatically paid back.

Fixing the problem

As a Data Science business we wanted to find a solution to the problem, we decided to use Machine Learning to extract the data in email receipts and enrich the corresponding Banking transaction, we pursued this route for four reasons;

- Email was dead (email is dead – inc.com), it is becoming just another data source. It was plain that the world had moved on from Email and now prefers Whatsapp, etc for private communication but we all need an email address (and card) to buy things online.

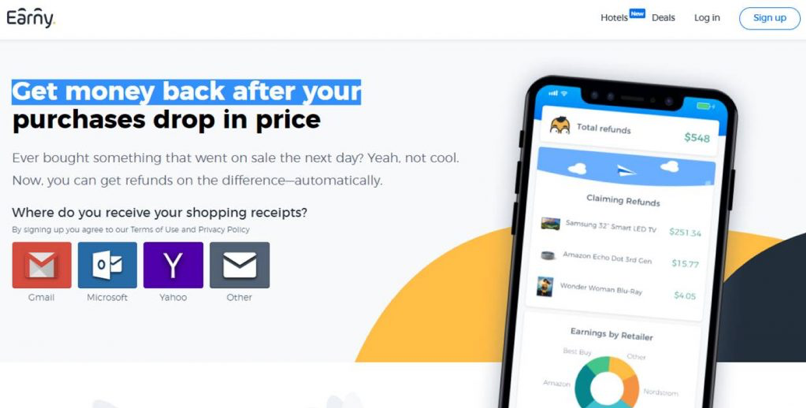

- US financial services were already doing similar stuff, companies like Capital One , Earny.co and Siftwallet.com had been at this for years – they read email receipts, obtained refunds and have amassed millions of users.

- Concerns about Privacy were not founded, especially in Millennials and Gen Zs, as this article Online value exchange by the Populus consultancy showed in The Drum.

- Apple and Google already use Machine Learning to auto add things to a Calendar (iOS 10 Siri auto adds events from email) or Wallet, Google now pulls Tickets and Loyalty data from Gmail and puts it in Google Pay (The Verge – April 16 2019).

Security and Application

Monily uses the same Machine Learning technology as Apple and Google to extract the data from the email receipt found on your Smartphone and populates the Bank transaction with the items you purchased, with no data going to the cloud. This makes it completely secure, safe and private. At first we developed our own App (Shoppa) but we came to realise the real benefits were for Retail and Business Banking, Personal Financial Management applications and Accounting solutions. Using our Splinter solution, we can help to reduce fraud enquiries by 50%, assist in selling personalised financial products and cut expense processing times down by 30%.

After years of development we are now actively selling the product and are pleased to be collaborating with Money Dashboard, pioneers in Personal Financial Management, and others to reduce fraud and improve expenses processing. If you would like to know more please email me on Adrian.James@moni.ly or visit Monily.co and I’ll get right back to you.

Can technology help the crucial impartial debt advice sector?

Photo by Alice Pasqual on Unsplash

The first blog in a series connected to FinTech Scotland’s consumer inclusion work. Nicola Anderson shares her reflections on work we’ve been doing with the impartial and independent debt advice sector. There is no doubt technology and fintech can play a role in the future of this crucial sector and we’re keen to support more collaboration and finding ways to build needed solutions.

Recent research and studies have found that 51% of consumers run out of money before payday; 23% report they are finding it difficult to manage; one in five consumers have no savings and almost 16% of the population can be described as over-indebted.

Recognising demand for debt advice services is rising, we invited representatives from a range of debt advice agencies and Scottish Government to discuss the current problems facing the sector and the potential for seeking technology-based solutions to practically improve the experience for those both providing and receiving debt advice.

Working collaboratively and across sectors the aim of the initiative was to identify priority issues that, if addressed through technological developments, would benefit the debt advice sector, building efficiencies and putting users at its heart.

The input from these experts has shaped three main problems and we’re pleased to share details of these in this blog. Of course, the next stage is to find solutions for these issues! Ever the optimist I’m hopeful that collectively we can do that, starting with sharing what this vital sector thinks its main problem are!

Unanimously, the experts agreed that the problem top of their list was the sectors limited ability to access available data efficiently or to its fullest extent. They shared examples where it can often take weeks to have a fully verified understanding of a clients circumstances, due to time consuming nature of the range of data and documentation checks needed to verify the position. Understandably this can exasperate the stress for people but in addition there can be circumstances where it also can limit the appropriate options for debt advice solutions.

Second problem held by the experts in the room was that current debt solutions and repayment plans are inflexible and do not reflect the reality of people’s lives – which exacerbates problem debt. Current solutions, more often than not, seem to force people into a set date repayment plan with little of no flexibility to reflect the fact that income could be variable or paid at different points each month. The view in the room was that there seemed to be little room for flexibility once a plan was in place and there was a general desire to see all creditors think about the benefits of greater flexibility in repayment plans not just when someone enters a problem debt scenario.

The third problem centered on the lack of pre-emptive engagement options to enable earlier intervention in a developing debt scenario. Experience shows that general recognition of the tipping point’ into problem debt is poor, increasing in the numbers of people moving from debt to problem’ debt scenarios. The inability to recognise the tipping point’ happens across a range of vested stakeholders including, Consumers/Citizens, Financial Organisations and Statutory bodies.

Money Advice Scotland in particular, are hopeful that technology solutions plays a key role in the debt advice sector of the future and have plans to work with FinTech Scotland and the fintech community to help develop and raise further awareness on financial inclusion issues impacting today’s society.

The insights coming directly from the experts who work with people at the heart of this issue are invaluable. Are there any quick wins available to any of these issues ”“ we’d love to know!

In the meantime, thank you to all those who shared their views, its good to know the debt advice sector will continue the focus on this initiative.

Income Verification: The Next Stage in Open Banking

As I’ve iterated more times than I can remember over the last two years, the implementation of Open Banking has changed the face of finance for ever.

To my eye, most financial institutions have now reached base camp’ with Open Banking, that is to say, the development of account aggregation within mobile apps. This is nice, and I’m sure consumers are enjoying having access to all their accounts in one place.

The next stage will be for banks and financial institutions to begin deriving value from its use. Within the next year I fully expect to see new services being launched by banks and FinTech’s that will allow financial institutions as well as consumers to reap the rewards from Open Banking.

To that end, we here at The ID Co. have been working with banks and lenders over the last year to bring a new proposition to market.

The ID Co.’s Income Verification solution offers banks and lenders the opportunity to capitalise on the Open Banking opportunity.

We work with numerous banks and lenders. On top of that we’ve spoken to many more over the course of the last year, both in the UK and Europe, and across the globe.

As such, I have a fairly good idea in my head of some of the challenges that are witnessed in the banking sector. One of the biggest that we’ve witnessed is the need to cut operating costs in order to stay competitive.

It’s no secret that the sector is far more crowded than it was just 10 years ago. And some of the Challenger banks now boast healthy customer acquisition, impressive UX across their apps and the web, and innovative new services.

Banks and lenders therefore have the dual pressures of bringing to market new services that will make their core offerings stickier’, while also attempting to streamline back office solutions.

It’s for this reason that I’d suggest exploring an income verification solution.

Verifying income is vitally important for banks and lenders, ensuring they have an accurate view of applicant’s financial income prior to awarding credit in order to ensure they are lending responsibly and offsetting any future risk of bad debt.

Operational Costs

Having an applicant’s income calculated within seconds of them making an application for a loan or credit totally negates the need for paper-based bank statements. The savings in time and resource here are enormous. It could take a few weeks for an applicant to submit their bank statements. And in that time, there’s plenty of opportunity for them to decide not to proceed, or to find an alternative.

We’re sympathetic to the hurdles that banks and lenders need to jump through in order to grant a loan. As well as AML and KYC checks, there are new rules on affordability to consider. For these reasons and more, it is vital that a sound lending decision is made, and not only that, be able to demonstrate why it was a sound decision.

Income verification allows you to do just that. With a solution such as ours, banks and lenders can know an applicant’s income exactly and can then calculate their monthly disposable income accordingly.

Thin Credit Files

Many of us will have friends and colleagues who are not British by birth. It feels a long time since I made the long journey from Canada to Scotland, but it is one that I remember well.

With individuals moving homes and countries with such frequency why is it that when beginning life in a new country, you also start with a blank credit file? Those with a thin credit file, perhaps because they’ve just moved into the country, can now illustrate their earnings and therefore capacity for credit through income verification.

Credit Risk

It’s a difficult challenge because most people aren’t paid monthly, or consistently. With the gig economy, students, retired, and others, those that get paid monthly are in the minority. To make a decision around credit risk, Underwriters or others need some context on which to base a lending decision. We need to understand what kind of income applicant have ”“ frequency, recency and more are all critical factors.

And this works both ways. While those with thin credit files can demonstrate why they might be right for a loan, it also gives the creditor more protection as they can protect themselves from applicants unable to practically make repayments or those that pose a bad credit risk.

Fraudulent Applications

When we were conducting research into loan applications and how Open Banking could support banks and lenders, I was struck by the volume of fraudulent activity that financial institutions needed to filter out in order to service genuine applications. Open Banking removes any opportunity for fraud as through APIs, direct access is made with an applicant’s bank account. Our Income Verification solution then looks back over many months to calculate income, not just the last one or two.

Conclusion

Income verification is the first of the services that will allow banks and lenders to derive value from Open Banking. The savings in time, cost and resource through its use are enormous and as its such reception from those who have trialled it use has been universally positive.

Reducing fraud, servicing customers with a thin credit file, widening prospect pools of potential customers, and illustrating good governance are all vitally important to lenders in 2019. We think that the introduction of our Income Verification solution will give financial institutions the answers to these questions.

Pensions Dashboards ”“ a positive step forward for the nation’s financial wellbeing

By Anthony Rafferty, MD of Edinburgh-based Fintech, Origo

Improving the overall wellbeing of citizens is becoming and ever more important focus of government, an important element of which is financial wellbeing ”“ the vision being a society where people make the most of their money and pensions through being more financially aware and equipped.

Technology has an important part to play in this, notably in respect of the implementation of the Pensions Dashboards. Primarily, dashboards are about enabling individuals to find and view all their pensions in one place, thereby increasing engagement with their long term savings and retirement planning.

Last week the DWP published its Pensions Dashboards paper, which is the Government’s response to the consultation that ended in December 2018. It sets out the practical steps necessary to implement Dashboards, starting with the establishment of an industry delivery group by the end of the summer under the new Money and Pensions Service (MPAS).

Some initial commentator reaction to the paper suggested the project wasn’t being moved on fast enough, but the paper is what we expected at this stage in the project and we see it as a positive step forward. In the paper, government clearly stated its intention to introduce Dashboards as quickly as possible’.

The four key elements necessary to make the Pensions Dashboards a reality are governance, compulsion to provide data, state pension and digital architecture. Next steps for all of these elements have been addressed in the paper, which we see as good news.

What’s more, through the consultation, government was able to test its proposals with the industry, consumer groups and other interested parties. Some 125 organisations gave feedback and the paper says the vast majority’ of them agreed with the suggested approach.

This approach includes establishing a single Pension Finder Service ”“ the core architecture that orchestrates an individual’s search for their pension data across all pensions companies and which displays their data on the dashboard they have chosen to use.

Origo has taken a leading role in the project from the start, quickly demonstrating how the technology could meet the government’s policy intent and objectives. We have built and scale-tested the central components to more than handle the 15 million and more potential requests the service could receive. Furthermore, we believe that the digital architecture can be deployed quickly to meet the stated timescales.

Through the DWP paper, government has given dashboards the green light. The task now is for the industry to help MAPS and the delivery group take the project forward to launch. It is a most exciting challenge and one that can have a significant positive effect on the wellbeing of this nation’s retirement savers.