Being a woman entrepreneur in the fintech industry

To celebrate International Women’s Day 2022, we met with Lynne Darcey Quigley, founder and CEO at Scottish fintech Know-it.

Lynne, when did you decide to become an entrepreneur and why?

From a young age I knew I wanted to run my own business.

I’ve always been hardworking and was a skilled credit management consultant so understood that I could build something great by helping businesses in need of recovering unpaid invoices and increasing their cashflow.

I founded Darcey Quigley & Co in 2007 offering commercial debt recovery and sales ledger management that has grown to be one of the UK’s leading commercial debt recovery specialists.

What led you to launch Know-it?

Working in the credit industry for over 25 years and running one of the UK’s leading commercial debt recovery specialists for 15 years I seen businesses make the same credit management mistakes time and time again.

The businesses I help day to day could avoid the need to use a debt recovery partner if they had implemented a robust credit control process. However, there’s a perceived barrier to this, mainly time and cost.

But the problem of late payments is massive, SMEs in the UK are currently chasing £61 billion in late payments, an increase of 22% since 2020!

Realising the size of the issue with late payments I founded Know-it to give business owners a complete automated end-to-end credit management process that is cost effective. Our automation will save businesses valuable time and help them get paid quicker and boost their cashflow.

How will Know-it help businesses avoid problems associated with late payments and improve their cashflow?”

Know-it provides businesses with all the tools and intelligence needed for a watertight credit control process all in one easy to use platform. Know-it brings together the 3 key elements of the credit control process, we like to call the 3 C’s, Check- it, Chase-it, Collect-it.

Check-it gives businesses the facility to credit check and automatically monitor companies from across the UK with real-time data from independent and reliable sources in just one click. This intelligence will allow businesses to make more informed credit decisions and mitigate credit risk.

Chase-it automatically chases unpaid invoices when they’re due through email, letter and SMS. Our smart integration with leading accountancy packages means Chase-it knows which invoices are due when and how much is owed.

Collect-it offers a much needed safety net by providing the services of leading commercial debt recovery specialists Darcey Quigley & Co to Know-it users with problematic late payers.

What is it like to be a woman entrepreneur in the fintech industry?

It’s been fantastic so far! The Scottish fintech community is so vibrant I feel women are very well represented.

I feel very supported in the Scottish fintech space. Schemes such as AccelerateHER and Business Women Scotland are helping female entrepreneurs thrive.

Do you feel like investors, potential clients or other stakeholders approach female entrepreneurs differently?

No, it’s never been something I’ve experienced during my fintech journey so far, certainly not with potential clients, partners or other stakeholders.

We’re just getting started with our big push for investment but so far I haven’t experienced any feelings of being treated differently so far.

According to you, what should be done to ensure more gender diversity in tech?

I believe there’s a lack of awareness of the variety of careers available to women within the IT industry.

It’s not just about coding. There are so many other exciting jobs in the tech sector such as Project Management, Business Analysis, Solutions Architects, as well as a myriad of roles in supporting business functions. We are in tech and big advocates for our industry, so we need to educate girls and women to the variety of careers now available to them.

What does the future look like for Know-it? Any exciting developments you can share with us?

Having launched our beta late last year we have aggressive growth plans for 2022.

We’re actively seeking investment now to help us fund these plans.

Our goal is to make Know-it the best credit management platform possible so we’re taking feedback from our users onboard and are always developing our product to meet the needs of our users.

The Talent Solution Most Enterprises Are Missing Out On

The societal and digital disruption brought about by COVID-19 has changed the way we work. Enterprises are having to reassess how they can develop, hire and invest in talent in their workforce as we move into 2022.

At the same time, employees’ views on career success, mobility and even the meaning of work itself have undergone a seismic change.

In fact, data shows that in the UK alone, the number of job vacancies is at an all-time high, reaching 1,219,000 in November 2021 ”” an increase of 434,500 from pre-pandemic levels.

Against the backdrop of the so-called war for talent’, businesses that want to maintain a competitive advantage over others need to find new and innovative ways of not only attracting top talent, but retaining it as well.

The traditional model

Traditional human resource management relies on a number of accepted ideas about how organisations work. Namely, a person is hired to do a particular job, and answers to a manager, who is in turn managed by someone else ”” all the way up to the top of the traditional hierarchical structure.

On the traditional career path, employees may eventually be promoted and climb the ladder within their chosen profession. A marketing assistant might eventually work their way up to becoming a marketing manager ”” but not an accountant.

And herein lies the problem: an employee is not just a CV. Placing someone in a box based on their job title alone ”” not on their actual skills, experience and personality ”” isn’t useful to anyone.

And while agile talent mobility might be relatively common within a job function (HR, marketing or sales professionals may jump from project to project fairly frequently), it’s rare for people to cross those boundaries and work on a project under a different discipline entirely ”” even when the skills and competencies needed for the role massively overlap.

For example, a data analyst working within a company’s IT department might make a fantastic addition to the team working on marketing analytics ”” but this is rarely the way it works.

The invisible talent problem

When companies need to staff a new project or build a new team, they’ll usually look to bring new talent on board ”” despite the fact they may well already have the skills they need in house.

As Gigged.AI’s CEO Rich Wilson explains: “Because of remote working and a largely distributed workforce, a lot of enterprises have no idea what talent they have internally. There’s so much money wasted by hiring new employees when actually, they’ve got that talent in house”.

Essentially, because of the silos the traditional company structure inevitably creates, enterprises have always found it difficult to understand exactly what skills and talent they’re sitting on.

The internal talent marketplace and the future of work

There are signs, though, that this mindset is beginning to change. Coca-Cola is just one big enterprise that’s starting to do things differently, and actually analysing the skills they have in-house.

These are skills that might not appear on a CV, that might have been picked up in a previous job ”” or a previous career ”” and that might otherwise have remained invisible. By bringing these skills to the surface, Coca-Cola hopes to identify opportunities for employees to have new experiences at work.

More importantly from the company’s perspective, this can help to retain talent as well. As Rich says, “There’s this sense right now that if somebody can make more money elsewhere, they’re going to leave. But people don’t just leave jobs for money ”” they leave because the project they’re working on’s not exciting, or because they’re not utilising certain skills.”

And it’s true: The Work Institute’s 2020 Retention Report found that compensation and benefits was only the sixth most common reason employees gave for leaving their jobs in 2019 ”” the first was career development.

By identifying their workforce’s core skills ”” and linking these with opportunities for employee development and the chance to work on new projects ”” companies can lower not only their staffing costs but their attrition rates as well.

And there are other big benefits to be had from implementing an internal talent marketplace too.

A broadened perspective for managers and employees

Coming into contact with different members of an organisation, either on a short-term basis or through a permanent job move, can broaden perspectives and help employees and management alike to develop positive traits such as empathy. An increase in empathy was the key theme of LinkedIn’s Global Talent Trends 2020 report, which also suggested that employees stay at companies with high levels of internal hiring 41% longer than at those with low levels.

Elimination of bias and increased DEI

In the current model, when projects are staffed internally, this is often done on a who-you-know basis ”” according to the LinkedIn report above, 50% of internal recruitment happens because a manager reaches out to an employer they already know.

Naturally, unconscious bias plays a role here, as people are much more likely to refer people who resemble themselves. It can also leave out talented employees who don’t have a strong network ”” but whose skill sets might be a good match for the project. By using an internal talent platform based on a comprehensive skill classification system, you can eliminate that bias and focus on the best person for the role.

Access to a broader talent pool

One of the biggest advantages of using an internal talent marketplace is that it can bring talent that might otherwise have been overlooked to the forefront. Like in the case of Coca-Cola above, enterprises can access skills that their employees may have picked up in previous roles, or transferable skills that could make a person a great fit for a role they might otherwise have been dismissed for due to lack of job-specific experience. As an added bonus, companies can also see a reduction in onboarding and training costs when new hires are already familiar with the business.

Drawbacks and pitfalls

Of course, there are problems with this approach too ”” most notably that it requires significant buy-in from management, employee engagement and a sizeable investment in tech.

Management buy-in

Surprisingly, according to Deloitte’s 2019 Global Human Capital Trends report, 46% of managers resist internal mobility, which can create a talent-hoarding culture ”” a big problem when it comes to implementing a successful internal talent solution.

Companies that want to adopt this approach to talent management, therefore, need to help managers understand that it effectively removes the need to jealously hang on to their top performers because it provides real-time transparency into the skills available within their organisation ”” and the opportunity to build and develop their team’s skills.

Hiring managers need to move away from the traditional talent acquisition model, which simply involves recruiting a candidate to do a particular job, and instead focus on fractionalising’: thinking in terms of projects and the knowledge and skills they require ”” knowledge and skills which may well be present within the organisation already.

Staff buy-in

The second problem is employee engagement, as employees (plus freelancers and contractors) usually need to manually input their details into their organisation’s internal talent platform to appear in searches. Although this might only take a few minutes, there needs to be some encouragement to motivate them to put themselves forward.

Team leaders can start by leading by example and entering their own skills and experience into the system. There should also be some education around the opportunities that the short process of filling in a profile could lead to ”” after all, only 28% of millennials surveyed in 2015 felt that their employer was making full use of their skills.

Tech investment

The last and perhaps most notable problem with implementing an internal talent marketplace at the enterprise level is the tech side. Building a platform in house will almost certainly be a time-consuming, complex, and ”” yes ”” astronomically expensive undertaking.

Thankfully, there is a solution available.

Introducing the Gigged.AI internal talent marketplace

Fresh from a successful pilot with The Data Lab, the Gigged.AI internal talent marketplace launches officially in the summer of 2022 ”” and can help large enterprises, universities and public sector harness the power of internal talent sourcing problems at the enterprise level.

Designed to meet the evolving business needs of companies in the post-COVID world, our white-labelled, data-driven solution allows managers at large enterprises to create a detailed and accurate statement of work using our innovative conversational AI chatbot. Our unique skills-matching algorithm will then use this to find the best people for the job from within your organisation.

You can run a quick check to see what talent you have internally within about 22 seconds ”” 22 seconds that could save your enterprise the thousands of pounds and months of lost time that typically comes with sourcing talent externally.

Gartner predicts that by 2025, 20% of large enterprises will have deployed internal talent marketplaces to optimise their utilisation and agility of talent.

Drivers for Growth? People, Technology and Regulations- a collaborative approach

Driven by digitalisation, fintech is one of the most important innovations embedded in everyday transactions, supported by emerging technologies including automation, cloud computing, artificial intelligence, blockchain, smart contracts, and machine learning.

While fintechs are here to stay, the image of the future is a little uncertain. Challenges such as the modernisation of financial architecture and changing consumer perceptions, the disruption of existing service models, incumbent employers and regulatory frameworks posing double edge implications for the overall ecosystem, and to access human capital, a discussion initiated by the University of Dundee Business School inviting FinTechs, regulators and Academics.

Regulators’ concerns have become increasingly complex because of technological integration and at times, fintechs exist in an environment with limited guidance. This challenge is underscored by regulatory regimes that multiply across countries, states, and even regions, a point emphasised by Professor Hisham, Birmingham University Business School, added how the terms around fintechs are not”¯comprehensive or standardised, which needs to be addressed in order to enable the”¯ecosystem to”¯grow.

Quicker responses from financial markets are crucial in terms of developing new instruments to battle the challenges about security and reliability of data and in terms of developing the regulatory framework, fostering relational and behavioral trust with consumers.

We must understand that regulations can be a barrier too, another point emphasised by industry experts, emphasising the need for a more balanced approach that allows flexibility and innovations. Najia ( Securities Exchange Commission of Pakistan) shared a regulatory perspective by adding that attitudes are shifting as a result of regulatory sandbox initiatives, providing a safe environment for early-stage development for fintech start-ups to test their innovations without the need for full license, thereby, playing another critical role in the development of fintech, ultimately breaking down the current regionalism of the sectors.

Nonetheless, different countries are at different stages of fintechs growth, for developing countries like Pakistan, a bigger issue is contract enforceability, suggesting that the biggest challenges are from the other side of the table, hence being mindful of the fact of how”¯the investors are and can be protected. This signifies the emergence of new developments and technological innovations that can help to develop a global friendly fintech ecosystem, breaking down the current regionalism of the sector.

“”¦.Fintech innovations will only become more pervasive in everyday transactions as their adoption increases and more inclusive and open regulatory frameworks allow them to grow.” [Stephen Ingledew, CEO at FinTech Scotland]

Opportunities abound for fintechs to engage in dialogue with regulators and raise awareness of rapidly emerging technologies and consequences they may have for market integrity, stability, and sustainability. Knowledge shared between regulators and fintech companies can enhance regulators’ awareness of consumer habits, behaviours and desires.

The technology supports the human understanding, where the growth opportunities are, but it will never replace a human in making those decisions, a point emphasised by Clive representing ACCA and Morris, Dean of Dundee Business School, adding that Digital transformation requires a transformation of people, technology, and processes, with people being the most important factor.

The key challenge organisations are facing globally, is the right talent. Despite searching for it, businesses are not getting the right people to assist them in this particular transformation. You can’t really have one without the other, Marijus (NCR) and James (Zudu), Tayseer (SadaPay) and Hazel (Candocollective) continuing the debate, suggested that people are extremely important, especially development of human capital, we need to put more emphasis on people’s learning, not only in their own skill set and knowledge, and also for their cross-functional flexibility.

After all, everything connects and technology, human capital, and businesses are dependent on each other now maybe more than ever before. The importance of educators was emphasised by most participants in reducing the gap between the needs of FinTechs and the offer of the current human capital market.

Overall, the promises offered by fintech certainly far outweigh the risks, at least in the medium to long term! However, we need to act now and get the regulatory environment and the human capital market “fintech ready”.

Participant organisations:

University of Dundee Business School ; SadaPay; Sehatkahani; Fintechscotland; Securities Exchange Commission of Pakistan; Candocollective; Birmingham University Business School; Zudu; NCR; ACCA; Tez Financial Services

Fraud Academy ”“ Cryptocurrency: Opportunity vs Threat

Fraud Academy ”“ Cryptocurrency: Opportunity vs Threat.

Are you familiar with the legislation and rules that pertain to cryptocurrencies in the United Kingdom? What can be done to prevent crime involving cryptocurrency, where could fraudsters go from here, and how do we begin to investigate this?

PwC are hosting a highly informative virtual event and will explore these questions, and more.

Date: Wednesday 9th February 2022

Time: 13:00 – 14:15 (GMT)

Location: Virtual / Webcast

Within the first nine months of 2021, cryptocurrency related fraud is estimated to have cost the UK over £146 million; a figure already 30% higher than that noted for the whole of 2020. Over 7,100 reports of fraud involving cryptocurrency have been made to the UK’s national reporting centre for fraud. More than half of victims were aged between 18 ”“ 45.

Cryptocurrency will only become a bigger part of how we do business, presenting both an opportunity and a threat; yet how ready are we to make the most of the opportunity and to deal with the threat?

Are you aware of the legislation and rules which exist in relation to cryptocurrencies in the UK? What can be done to prevent crime using cryptocurrency, where could fraudsters go from here and how do we start to investigate it?

At this highly informative virtual event, we will explore these questions, and more with a panel of deep subject matter experts.

We are delighted to be joined by Jim Robertson (DCI, Police Scotland), who will give an overview of the current lay of the land’ from a policing perspective in relation to cryptocurrency and discuss how law enforcement is dealing with the challenges of an increase in this crime type.

Jim will be joined by Craig Kennedy (Partner, Dentons), who will discuss the legal powers available in relation to cryptocurrency in the UK and the potential risks and benefits of using cryptocurrency.

We will also be joined by Haydn Jones (Senior Blockchain Market Specialist – PwC) who will share his own opinions and thoughts on the opportunities and threats presented by the rise in cryptocurrencies from his own experiences investigating and providing expert witness testimony on cases involving cryptocurrency.

Attendees will also have the opportunity to put questions to our speakers during a Q&A session.

We look forward to welcoming you to our event on Wednesday 9 February 2022 at 1:00pm.

If you have any questions about this event, or have any issues registering for this event, please contact the team via uk_fraud_academy_scotland@pwc.com or uk_ni_fraud_academy@pwc.com.

Global climate tech investment more than triples, but could be better targeted to cut emissions

In December 2021, PwC Global released the State of Climate Tech report. The analysis examines how investors are improving both climate impact and commercial returns through the emerging asset class of climate technology, helping to keep the Paris Agreement’s goal of limiting global warming to 1.5 degrees Celsius within reach.

This represents an increase of 210% from the US$28.4bn invested the year prior, with 14¢ of every dollar of venture capital investment now going to climate technology. PwC’s State of Climate Tech 2021 reports that where the investment is lacking is in addressing the largest contributors to global emissions. From the 15 technologies investigated, the top five technologies, which represent more than 80% of emissions reduction potential by 2050, received only 25% of the climate techinvestment between 2013 and H1 2021.

Emma Cox, Global Climate Leader, PwC UK, said: “The world has 10 years to halve global greenhouse emissions if we are to have hope of achieving net zero by 2050. Innovation is critical to meeting the challenge and the good news is that climate tech investment is up significantly across the board. However, our research has found there is potential to better channel and incentivise investment in technology areas that have the greatest future emissions reduction potential. This raises the question of why these sectors are missing out ”“ are investors missing a value opportunity or is there an incentive problem that needs the attention of policy makers?”

To find out more about PwC’s Climate Tech report, please contact Jason Higgs, Partner, PwC jason.c.higgs@pwc.com

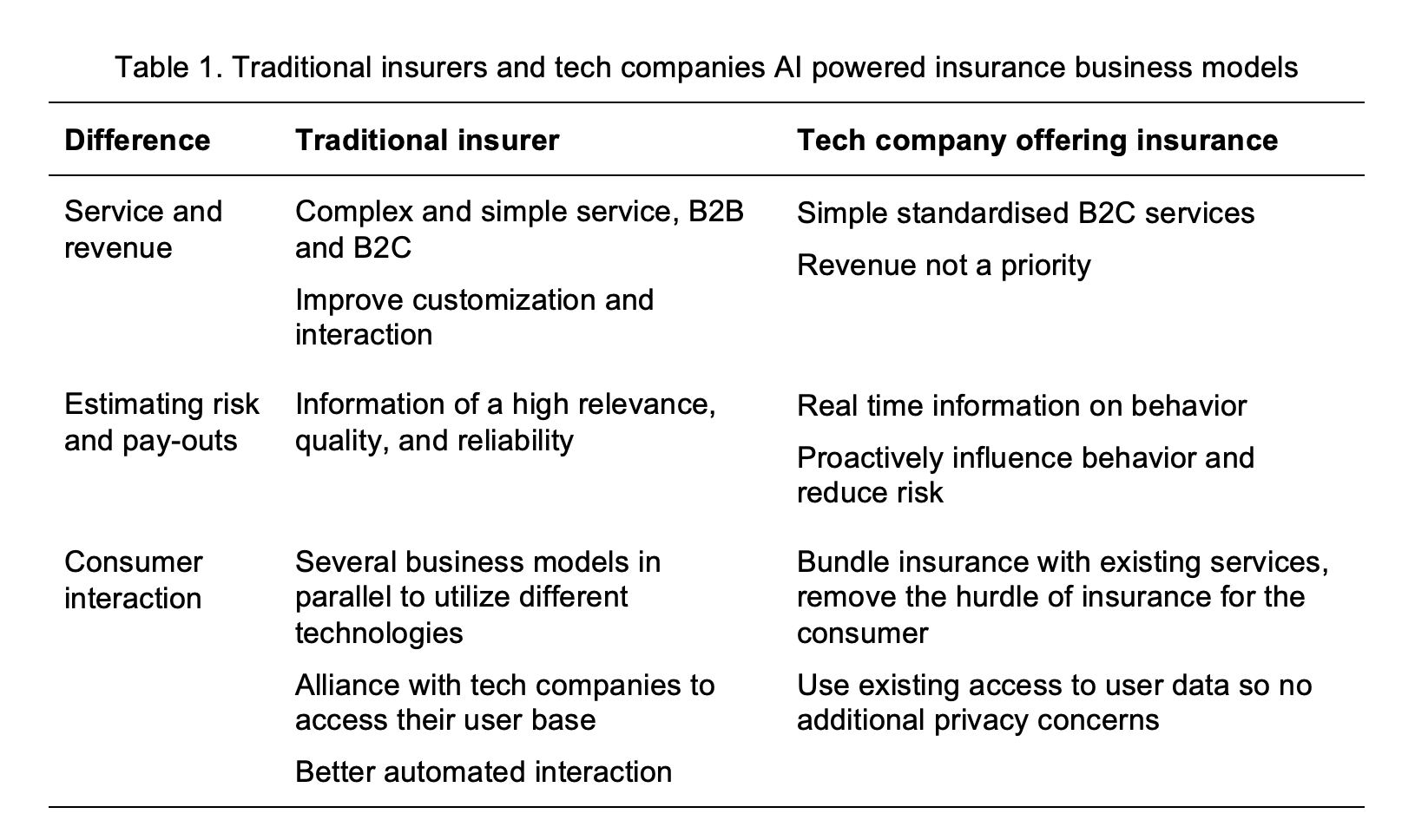

Existing insurers and disruptors are utilizing Artificial Intelligence to create new business models

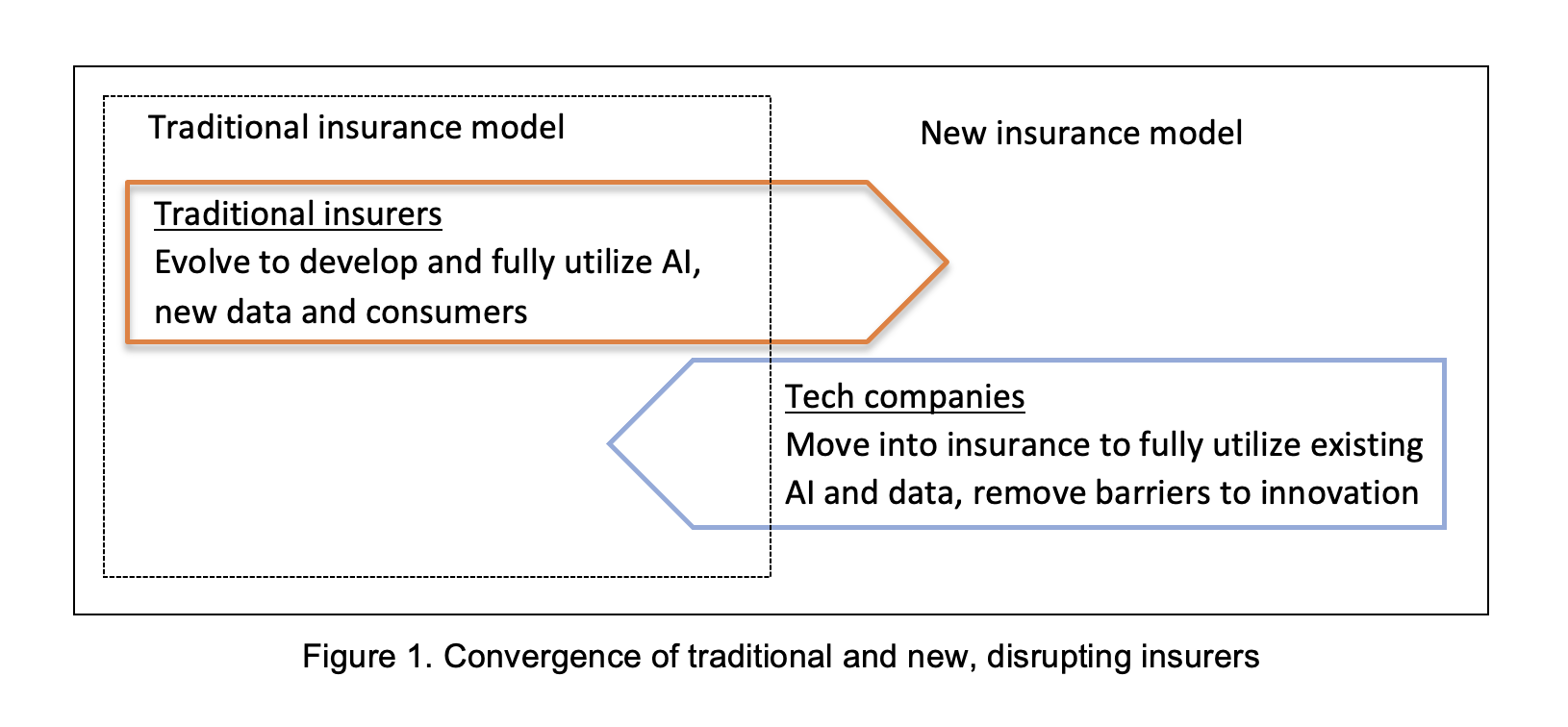

We can see that Artificial Intelligence (AI) is transforming many parts of our lives, but do we know where this journey is taking us? Insurers need some certainty on what their future will looks like. Some new insurers are trying new business models enthusiastically and then changing direction sharply, like a speedboat swerving to avoid a collision. The larger insurers, however, are like large cruise ships; they need to be able to see far ahead before they plot their course, and they don’t want to keep changing direction.

This research tried to identify the viable AI driven business models to help give some clarity. Some traditional insurers are just trying to be more effective with AI, while others reinvent themselves to fully utilize the new capabilities available. Tech-savvy companies from outside the sector like Tesla, are entering and disrupting it. Would these diverging paths continue, or would they converge in the future towards one, ideal, business model? This research focused on one example of a traditional insurer and one new tech-savvy disruptor and evaluated whether their models are converging.

AI is changing the insurance value chain, as illustrated in figure 1. Most new insurers, like Tesla, offer fully automated simple services. The traditional insurers offer some of their simpler services in this way. The more complex services are supported with AI, but a human makes the final decision. An example of this are audits for fraud, where the AI identifies unusual patters and cases for an expert to evaluate.

There are signs of convergence between the models of traditional and new insurers. First, there is convergence in technologies, such as the use of chatbots utilizing AI. Second, there is a convergence in processes, for example, the interaction with the consumer. Third, there is convergence in the strategy on costs and pricing.

However, there are two areas where there seems to be a limit on convergence, which seems to suggest the business models of the incumbent and the disruptor will remain distinct. These are: (1) evaluating risk and (2) the cost of attracting the user and profitability.

Despite some convergence, certain differences are likely to remain even after this transitionary period. This is because the two models have distinct competitive advantages. Traditional insurers no longer monopolize the capability of providing insurance, but they still have the existing user base and utilize it to evaluate risk. Technology-savvy companies that now offer insurance, have their own forms of engagement with their consumers, use different methods to evaluate risk due to their access to real time data, and do not prioritize generating revenue but instead utilize insurance to increase their user base, overcome barriers, and reduce the overall cost of their products and services.

Therefore, when insurers are thinking about how to utilize AI and plot their course through the turbulent, unpredictable times ahead, they should stay true to what they are. This is their comparative advantage.

Dr Alex Zarifis is a lecturer at the University of Nicosia in Cyprus.

This article is adapted from his paper, “Evaluating the New AI and Data Driven Insurance Business Models for Incumbents and Disruptors: Is there Convergence?” available from https://doi.org/10.52825/bis.v1i.58.

PRESS RELEASE: Automation the key to growth and data management for banking and payments sector, finds new report

A new report from leaders in reconciliation and finance automation software, AutoRek, has found widespread concerns around the ability of businesses to grow amidst scalability and regulatory pressures over the next three years, affecting 92% of professionals surveyed.

The report ”“ Banking and Payments in 2022: Digital transformation and trends in financial technology ”“ was designed to provide an insightful view of the key challenges and solutions that will face the financial industry as it enters 2022.

AutoRek gathered insights from senior professionals across the banking and payments industry on the barriers they face surrounding the handling of payments data, compliance and growth, and new technologies in use or consideration.

Automation was found to be a key source of hope for enabling growth and regaining competitive advantage. Other key findings include:

- Manual processes form the biggest roadblock to achieving automation, cited by 46% of firms, followed by legacy systems (42%), poor interoperability (40%) and regulatory requirements (38%).

- In-house IT solutions are the most common for data handling across payment operations, used by 44% of firms ”“ a higher reliance on in-house systems than in most other sectors.

- Almost one-third of firms consider their jurisdiction’s regulatory body audit and control around regulatory reporting infrastructure somewhat or far too strict, while 22% consider it somewhat or far too lax. Just under half consider it appropriate. Financial institutions in central and south America were considerably more likely to view their regulators as lax than their European and Asia-Pacific counterparts.

- When selecting a solution to handle payments data, almost 80% of respondents consider its ability to integrate easily with existing infrastructure a key factor.

- Over half of respondents (56%) either already have or are in the process of deploying modern technologies such as artificial intelligence (AI), machine learning (ML) and application programming interfaces (APIs) to help monitor and streamline their data management processes. One-third had onboarding planned in the next 12-24 months. Only 12% reported having no plans to apply technology to improve data management processes.

Firms slow to adopt emerging technologies should be aware that they are now falling behind in an increasingly automated and competitive landscape, according to Nick Botha, Banking Lead at AutoRek.

Commenting on the findings of the report, Nick Botha continued: “While automating data flow has been a priority for some years now, this survey makes clear how many inefficiencies continue to plague firm’s day-to-day operations when it comes to data processing and reconciliation. Legacy banks in particular are grappling with often more than 20 disparate systems written in varying generations of software, none of which are designed to interact with one another.”

“While a decade ago that might have flown under the radar, the last few years have seen control of the payments space shift from banks into the hands of Payment Service Providers (PSPs), whose ability to deliver totally user-native customer service is forcing the whole industry to step up.”

“Beyond competing for market share, it’s a question of compliance. The costs associated with non-compliance are substantial both from a financial and reputational perspective, and regulators are increasingly less forgiving, as we have witnessed in the last few months with significant fines incurred by some of the world’s largest banks.”

“New technologies like AI, ML and APIs can be used to create greater interoperability and remove or significantly reduce manual interventions and use of spreadsheets. Investing in these capabilities today will enable firms to address evolving customer preferences, mitigate risk and achieve regulatory compliance down the road ”“ essential elements for remaining competitive in the payments landscape of today.”

The future of automation for UK asset managers

The last 18 months have been amongst the most disruptive that the financial services industry has ever experienced, forcing many sectors to reconsider business models.

Asset managers in particular have undergone a substantial transition as video conferencing has replaced client-facing interactions. To better understand how these firms have responded to market disruption, we surveyed 100 Heads of Operations across UK asset management firms to learn about their operational challenges, automation objectives and plans for regulatory compliance in 2022.

From this study, three lessons stood out for their relevance to the wider fintech industry:

1. Operational challenges and tech improvements are company-specific

We asked asset managers what does and doesn’t present a challenge to their daily operational processes.

While the availability of automated systems and adequately skilled staff were highlighted by two-thirds of respondents as the most significant challenge, firms also pointed to many others including the functionality of manual resources, process complexity and a changing regulatory burden.

Although nearly 8 in 10 acknowledge that the capabilities of current systems are hindering operational growth, firms have identified a range of priorities to improve these systems from seamless data flow, AI-assisted dashboards and dynamic data management through to enhanced risk management and talent acquisition.

The variety of responses tells us that no two firms face the same operational challenges and, consequently, that technology infrastructure improvements for 2022 will be equally varied in their application to the asset management industry.

2. Manual reconciliations continue to challenge asset managers

Reconciliation is an essential process for keeping accounts and financial records accurate. In recent years, more firms have been automating reconciliation procedures to eliminate risk of error and improve accuracy.

Despite this, our survey reveals that:

- 60% of asset managers worry that manual reconciliations are the greatest risk to their organisation

- 75% say that the number and volume of manual processes is an immediate operational challenge

- Only 7% say that manual processes present no challenge to their firm

Data preparation was also highlighted amongst the most time-consuming tasks for businesses, which further highlights how the complexity of data management continues to grow year on year. This is consistent with our work across other sectors, where we find that manual processing is really the core issue underlying poor reconciliation disciplines.

With half of UK asset management firms allocating budgets between £0.5 and £10m to address manual inefficiencies, we can expect automation to become more deeply embedded in the industry throughout this year.

3. Regulation is accelerating the trend towards automation

Although manual processing has been steadily declining for years in favour of automation, our findings show that a growing regulatory burden is definitely a factor in this transition.

Just 2% of asset management firms in the UK have no plans to invest in automation to achieve regulatory compliance. For the majority that did, top focus areas include operational resilience, prudential regulation, MiFID II and CASS. A further 7 in 10 felt that automation will be instrumental in achieving compliance with the IFPR regulation, which came into effect on 1st Jan 2022.

These findings tell us that UK firms are actively pursuing automation as a convenient and cost-effective way to fortify against regulatory breaches. Nevertheless, with 42% still pointing to new or changing requirements as the biggest threat to their company, such solutions need to be flexible as requirements continue to grow in scope and complexity.

What does this mean for software providers?

The results of our survey clearly demonstrate that automation in finance will become ubiquitous in the medium to long-term. However, the variety of responses and priorities outlined also shows that firms do not want an off-the-shelf solution; instead, they want a reconciliation platform which:

- Is configurable to specific operational needs

- Eliminates manual intervention through end-to-end automation

- Is purpose-built around specific regulatory requirements

- Is flexible to accommodate for multiple iterations of regulations

Of course, these are welcome findings at AutoRek, where we have spent over two decades working with financial firms to build bespoke solutions for unique reconciliation, operational and regulatory requirements.

In the short-term, it is clear that asset managers recognise how automated reconciliation disciplines do and will continue to form the cornerstone of an effective business model in today’s post-pandemic environment. It will be interesting to see how this plays out across the wider financial industry over the next 12 months.

Photo by George Morina from Pexels

Origo – Four of our proudest achievements in 2021

Antony Rafferty, CEO of Origo, reflects on four of the Edinburgh-based FinTech’s key achievements over the past year.

While 2021 has been another year that most people are probably glad to see the back of, as this time of year is traditional a period when we take a step back and reflect, I feel as a company we should take the time to consider what we have achieved.

Origo has a 30-year history of delivering technology solutions that make a difference to the financial services industry and to the consumers buying its products and services. Our expertise is in identifying the pain points for the providers, platforms, software companies, and financial advisers in the market and delivering a utility solution that solves the issue and whicheveryone can buy into.

We are proudly based in Edinburgh, but we work collaboratively with companies from the UK and overseas in delivering our industry solutions.

This year there are four areas I would like to highlight where, despite the pandemic, we have been able to help the industry become more efficient, more cost effective and as a result, help deliver better outcomes for consumers.

1. Being selected to build and run the core architecture of the UK Pensions Dashboards.

This year Origo was delighted to be able to announce that Capgemini and Origo had been appointed to supply the central digital architecture for the Pensions Dashboards Programme (PDP).

Pensions Dashboards will enable pension holders to identify and see displayed their pension policy data, which will help them make more informed decisions around their retirement planning.

This is a project we feel particularly passionate about and Origo was fully committed to progressing pensions dashboards from the day the project was announced. We see it as a major milestone in helping UK citizens to prepare for their futures.

PDP stated that the Capgemini/Origo bid was successful “due to its quality and value for money, plus the credibility and expertise of both parties to deliver the contract.”

2. Driving integration between systems and software.

One of the bugbears of our industry is that systems and software needed to run financial services businesses do not talk to one another and so force the re-keying or manual transfer of data and information between them. Not only does that increase risk to businesses but it makes for inefficient, overly time consuming and so costly operations. The solution is to integrate between companies and systems. In the past that has meant point-to-point integration between individual companies, which is expensive, resource heavy and requires ongoing maintenance and updating as rules, regulation and legislation changes.

As an industry solution, we launched the Origo Integration Hub, which enables participants to integrate once with the Hub and then operate with any other user. Currently, these arefor key operations, such as valuations, account opening, remuneration, transfer tracking and bulk transaction history, and further developments are in hand.

The Hub also helps drive competition and innovation, by levelling the playing field for all players, no matter how deep their pockets.

In 2021 signings to the Hub doubled and we now have over 40 companies integrated, from large providers to innovative new joiners to the market.

3. Doing away with inefficient paper-based systems.

Given we are in the 21st century, it is surprising that paper is still used to the extent that it is in our industry. While tackling operational inefficiencies has not been top of the priority list for financial services firms during the pandemic, for obvious reasons, this is now beginning to receive renewed focus amongst providers as they see it as a means to reduce costs and create operational differentiation in the market.

The Letter of Authority process, which is the way financial advisers notify providers that they are authorised to work with new clients, is a case in point. Currently, advisers have to manually fill in forms and have them signed by the client and then email, or in some cases fax them, to providers. Origo is making a dent in this with our Unipass Letter of Authorityservice, a way for providers to help simplify the current ad hoc way Letters of Authority are processed, creating a utility that delivers greater efficiencies for providers and adviser firms alike.

4. Keeping communications secure.

Cyber security has definitely risen up the priority list for financial services firms in 2021. As an industry we are handling huge amounts of personal and confidential information about individuals, which, if it falls into the hands of criminals, can be used to scam them or steal their identities. This can lead to devastating consequences for individuals as well as fines and reputational damage for the companies involved.

One of the most commonly used ways to communicate, i.e. email, is often the most vulnerable. This vulnerability is why we launched Unipass Mailock as a centralised industry utility to help businesses of all sizes secure their communications.

It encrypts email to keep the contents safe, combined with dual factor authentication, so the sender knows only the intended recipient can open it, and an audit trail is created for compliance purposes.

Two of the industry’s larger providers ”“ Aegon and Royal London ”“ started using Unipass Mailock in the past year to protect their communications with intermediaries and their clients and other companies are in the pipeline to go live.

These are four of our achievements over the past year. We arenot a large company and all that we have achieved is because of the dedication and expertise of our people, who, working together, physically and virtually, have done great things despite the pandemic.

If you haven’t done it already, I highly recommend taking a step back and contemplating your achievements this year. 2021 may not have provided the best environment for success but I will bet you will find you’ve achieved more than you think you have.

An end of year “Thank You” message from our CEO

As we come to the end of 2021 and look forward to 2022, we’re reflecting on the year and are hugely proud of what’s been happening across Scotland’s FinTech Cluster. Despite the continuing challenges from the COVID-19 pandemic we’ve seen fintech SME Growth, both in number of businesses and in terms of scale, we’ve seen record levels of investment in Scottish fintech SME’s, a true testament to the calibre of the businesses and leaders who continue to inspire us day on day.

The past twelve months have also seen more international growth with up to 50% of Scotland’s fintech SME’s building plans for international trade and more global businesses locating to Scotland as they establish a UK base.

We’ve also had the Kalifa review of UK fintech acknowledge the established progress of Scotland’s FinTech Cluster, and we’re looking forward to supporting the implementation of the Scottish Technology Ecosystem Review led by Mark Logan and building a plan to enable Scotland’s future digital economy.

The FinTech Scotland festival provided us all with an opportunity to meet again face to face and if we needed it, it reinforced the energy, optimism, diversity of contribution and breadth of collaboration that contribute to our fintech successes. A highlight for all of us in the FinTech Scotland team were the hybrid and in person events, kicking off with the DIGIT FinTech summit and ending with the Times and Futurescot event where we welcomed the UK regional fintech clusters to Scotland in the Accelerating UK FinTech conference.

During 2021 we have seen a growth in climate fintech, with new fintech SME’s starting to develop businesses to help address the impact of climate change and support the journey to net-zero, as well as established fintech SME’s expanding their existing capabilities to tackle this important issue. I have no doubt we’ll see more of this in 2022 and we’re looking forward to doing more to stimulate and accelerate climate fintech in Scotland.

With the establishment of the Scotland fintech SME advisory Board we have a clear plan on fintech SME priorities for 2022, and it is a privilege to work with these dedicated leaders who have come together aligned behind the vision of economic, social, and sustainable growth across the FinTech Scotland Cluster.

Looking forward to 2022 we’re focused on supporting fintech SME’s to scale and grow, strengthening international connections, building more impactful fintech collaborations and deliberately driving more fintech Research and Innovation (R&I) in Scotland and across the UK. We plan to launch the FinTech Scotland R&I roadmap early in 2022. It’s a plan that pulls together industry R&I priorities as we ask ourselves, what should finance look like in 10 years-time, and it provides us with a framework to lead the answers to that important question.

In drawing to a close, I’d like to say thank you to everyone that’s supported the FinTech Scotland Cluster across 2021. I’m continually reminded of the privilege it is, to know you and work with you in our collective efforts to lead and achieve our ambitions for fintech in Scotland. I’d also like to say a special word of thanks to the brilliant team at FinTech Scotland. I see their energy, commitment and drive everyday and it’s a pleasure to work them.

My final note is to wish you all a happy and healthy 2022 and we’ll look forward to seeing you all next year as we continue to build on our plans and drive the FinTech Scotland Cluster.