HR for Fast Growing Fintechs: Investing in a People Strategy for Success

The rise of the FinTech sector in Scotland continues at an impressive rate despite the challenges of this year, with a number of innovative new start-ups contributing to this exciting growth.

Setting up any new business is challenging but especially so in technology where getting access to and retaining the best talent is crucial to success. HR strategies and framework must address this reality in order to build a strong team and culture for sustained growth and competitive advantage. Setting up the company’s values and mission early on lays the foundations for a strong and successful workplace culture ”“ ultimately the driving force of HR.

Supporting Scottish FinTech

As HR specialists with a niche focus in the technology sector, we have supported Scottish Fintech Exizent since early 2020.

An innovative, Glasgow-based technology firm, Exizent have a strong purpose – to improve the bereavement experience for everyone involved.

The Founders had launched the company, both having previous experience of building successful businesses. They had plans to scale rapidly and knew the value of early investment in strong HR practice. Having secured funding to support their ambitious growth plans, they needed to build a strong team and culture and implement HR framework and infrastructure.

Establishing HR & people strategy

Having engaged us to support their growth journey, we conducted a full review of Exizent’s existing HR setup and processes, held scoping 1:1’s with the Founders and conducted a needs analysis, planning and prioritisation session aligned to their business and growth plans. This allowed us to gain a real understanding of the company’s ambitions, culture, people plans and future HR support needs.

We then identified the key short and medium term strategic and operational HR requirements which would enable the business to achieve its aims linked to rapid expansions and rollout, as well as being able to support the company values and culture.

Key requirements included contracts and documentation, onboarding processes, compliance, a HR management system, an employee handbook and the ongoing development of strong organisational culture.

The outcome was a tailored and prioritised HR plan with indicative timeline to support the business to scale rapidly over a 24-month period.

Our approach was designed to provide an effective and fit for purpose HR strategy, putting in place solid foundations to allow Exizent to grow and scale sustainably from a people management perspective.

A regular bank’ of HR support time was agreed, allowing Exizent a full hands-on HR service and access to expert HR support when needed to help them develop, implement and maintain their people strategy. This would also ensure that ongoing guidance and manager support was available to their team from a very early stage in their organisational development.

Exizent now have in place robust, fit for purpose, effective and compliant HR and people management systems and documentation, optimising their organisational effectiveness by aligning strategy, people, resources and processes. Team development sessions led by Purpose HR support effective business relationships, collaborative working practices across the organisation, and a strong and positive culture.

Exizent continues to grow rapidly, confident in the knowledge that they have a trusted and flexible HR partner embedded in their business.

“We engaged Purpose HR for their recognised expertise with growing technology-led businesses. They are a trusted extension of our management team and we value their depth of knowledge and professionalism. Purpose HR are very well aligned with our business, share our values and are a great cultural fit. Their flexible support is responsive, cost-effective and saves us valuable time. I would highly recommend Purpose HR for their cutting-edge, hands-on and people-centric approach – perfect for scaling businesses.”

Aleks Tomczyk, Founder & COO

The importance of investing in HR

It can be easy to overlook HR in a startup business and it is an area of expertise which many technical startups lack.Many entrepreneurs get their businesses off to a flying start, charging forward at speed, but struggle with people management further down the line. As a business grows, leaders often find there just isn’t time to deal with day-to-day people management and recruitment, and the focus on people can easily get lost. This is a costly mistake and can affect employee engagement, culture and long-term success.

Investing early in strong HR practice at the beginning, as Exizent have done, is critical for sustained growth. For startups, outsourcing this to a HR partner who understands the market, the company’s values, culture and strategic aims, and who adds value to the business is an investment in the future success of the organisation.

Lisa Thomson is the Managing Director of Purpose HR and is experienced in establishing HR functions and people management and development frameworks within growing businesses and is a trusted advisor at board level.

Purpose HR are a trusted HR partner to some of the most exciting, investor backed, high growth businesses in the Technology, Engineering and Life Science sectors in Scotland and offer hands-on flexible support to enable scale and growth through attraction, retention and development of key talent.

If you’d like to find out more about cost-effective and tailored HR support for fast growing, technology-led startups and scaleups, contact Lisa Thomson at lisa@purposehr.co.uk

Is artificial intelligence the key to better access to funding for business and consumers alike?

Although the UK ranks third in the world for numbers of new business start-ups, it sits at a less impressive 13th place in the number of successful business scale ups[1]. Access to finance is widely argued to be a contributing factor with traditional banks having become more risk averse in recent years, and focussed heavily on security rather than a borrower’s ability to pay. Consumers, too, know first-hand how frustrating this can be, especially those held back by the seemingly inflexible approach taken by credit ratings agencies.

Change, however, is coming

Financial disintermediation, or more direct links between providers of capital and borrowers, has been a major feature of the financial landscape for the past two decades. Digital advances have seen this trend accelerate and the proliferation of non-bank lenders continues to increase. In fact, according to recapitalnews.com, 18 of Europe’s 40 largest real estate lenders are non longer banks.

And whilst some might argue that it really doesn’t matter where borrowers gain access to the funding they need to grow, there are increasing signs that both sides of the lending equation are benefitting significantly from new, highly advanced, technology solutions being deployed in the sector.

Elsewhere, comparison websites, taxi or ride-hailing apps and online supermarkets have all helped to show us the convenience of going digital. We feel more in control of our choices, and have the information we need at our fingertips. We have become used to instant gratification, and processes that are simple to use (even if they are massively complex to run). So too, we are starting to see this in the world of FinTech – where finance and technology collide to produce new and innovative activities in the sector.

Houston we Have is one such company that has developed an innovative solution that produces the strangely non-binary, or win-win, situation where a lender risk and operating costs are reduced and borrower convenience and access to funding is actually enhanced.

Based on the company’s proprietary prescriptive intelligence software platform, Houston we Have developed a credit risk assessment model for a Sydney-based SME lending platform that combines leading automation, the best of human expertise (without bias) and more than 70 information variables to produce an online application tool that’s easy to use, and fast to run.

Prior to the implementation of Houston we Have’s solution, the credit risk decision support system in place at the business was manual, resource intensive, reliant on third party providers and exposed to flawed systems. Typically a fast decision would take several hours. Today, the business can produce a decision within seconds.

Risk has also been reduced with a far better understanding of a borrower’s ability to pay and the removal of human bias in the decision making. Delinquent loans have been an astonishing zero since the system was introduced. And as for changes in legislation, lending frameworks or appetite for risk; these can be easily factored into system updates, as can revised versions for the regulatory environments in different countries and jurisdictions.

All this points to a more efficient industry that benefits lenders and borrowers alike.

Houston we Have is a boutique technology business that combines data science, software and artificial intelligence to deliver the kind of information that allows their clients to make better decisions and thrive. Their proprietary software was initially developed for military intelligence agencies, an environment where it is still very much in use. Gartner has identified the company as a Cool Vendor describing the value proposition as “unlike that of any vendor we have seen.”

[1] www.smallbusiness.co.uk, June, 2018

Photo by Markus Spiske from Pexels

Creating a Culture of Support in the Financial Services Industry

Pinsent Masons recently published a report Creating a Culture of Support in the Financial Services Industry’, produced in collaboration with a number of key stakeholders in the financial services industry, including financial institutions, fintechs and third sector organisations, to explore this important topic in more detail.

As part of the report, Pinsent Masons commissioned a consumer survey to obtain insight into the role individuals see their bank playing in helping to support them if they are affected by a mental health condition. Their findings show that consumers are very much in favour of banks taking a proactive approach in helping consumers to manage their money, for example by implementing spending controls or notifying the consumer if an abnormal spending pattern is identified.

One of the key areas of focus for the FCA is ensuring that consumers with mental health issues are treated fairly and the report looks at the FCA’s approach, the legal issues associated with banks and other financial services institutions being proactively involved in supporting consumers, what the industry is doing to support consumers with mental health issues and how the COVID-19 pandemic has increased the need for additional support to be offered to consumers.

Creating a Culture of Support in the Financial Services Industry’ highlights the positive steps already taken by the financial services industry to ensure that consumers with metal health issues have access to the support they need and shows that that there is a huge opportunity for collaboration between industry players to offer even better solutions for consumers in the future.

A copy of the report is available here.

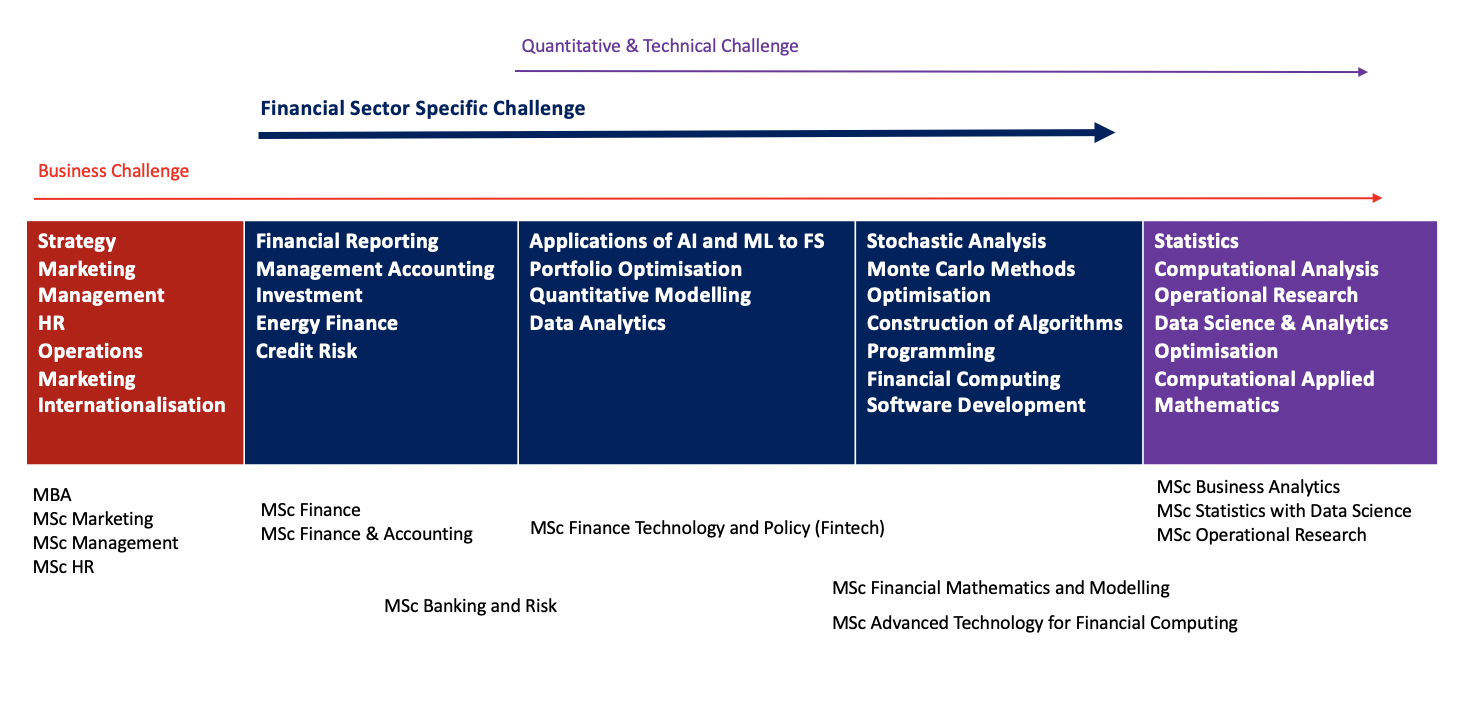

In-depth fintech research and analysis with specialist MSc students

Article written by Ksenia Siedlecka, Financial Services and Fintech Sector Engagement Manager at Edinburgh Innovation

We are currently looking for projects for a variety of MSc programmes with finance and fintech focus (MSc Fintech ”“ Finance, Technology, Policy, MSc Banking and Risk, and MSc Finance, MSc Financial Mathematics). We also have a number of business and data science MSc programmes which are popular with Financial Services and Fintech companies looking to propose projects (e.g. Business Administration, Business Analytics, Statistics). With such a fantastic selection of programmes, we are able to tackle a variety of business challenges. Our students are among the best in their field and combine their specialist subject knowledge and management skills with the refinement offered through our 12-month, intensive programmes. Projects are delivered free of charge and supported by our world-leading academics at The University of Edinburgh. We offer different types of projects and will match you with an individual postgraduate student with the specialised skill set suited to your business challenge and research needs.

Our Business School students can help tackle questions related to corporate strategy, marketing, finance, internationalisation, product development, HR, operations management, change management and many others. The MSc in Finance programme covers all aspects of investment, corporate and energy finance. MSc Accounting and Finance could help with topics on financial reporting and management accounting. MSc Banking & Risk projects could cover such topics as analysis of corporate financial information, credit risk management, econometrics applications and many others. We can consider almost any topic that has a finance, accounting, investment, energy market, banking or risk focus. Successful projects tend to have an empirical element, which has practical relevance. Our students are keen to work with practitioners on projects which will be of real value to them, helping them find solutions to strategic financial issues such as validity forecasting, forecast asset market returns, risk modelling, dynamic lifecycle strategies etc.

MSc Financial Mathematics students will work on a real mathematical finance problem and can utilize specialist techniques such as stochastic analysis, Monte Carlo methods, statistics and optimisation, construction of algorithms and programming skills. Projects often require the design and implementation of computational analysis to a specific area, and can involve the application and implementation of existing mathematical models, or development of new approaches to solution methods. Quantitative modeling, data analytics, financial computing and software development projects can be tackled by our computer science students from MSc Advanced Technology for Financial Computing.

The MSc Finance, Technology and Policy (Fintech) prepares students with technical skills and knowledge of programming, artificial intelligence and machine learning who also understand financial markets and regulations so they are ready to develop technological solutions fit for the financial sector. We are particularly interested in dissertation topics in applications of artificial intelligence and machine learning, data analytics, and portfolio optimisation. Example topics include: building robo-advise algorithms using ML; pattern recognition in big data (including alternative data) using ML; optimal execution strategy with particular emphasis on trading securities in ratio, and many others. Can you help?

If so, we’re looking for companies to submit project ideas by approx. 25 January 2021. In return, you’ll benefit from the insight of one of our high-calibre postgraduate students, including a substantial report featuring extensive research, rigorous analysis and practical conclusions.

To discuss further, contact Ksenia Siedlecka, Financial Services and Fintech Sector Engagement Manager, ksenia.siedlecka@ei.ed.ac.uk

Origo ”“ what are we working for?

Written by Anthony Rafferty, Managing Director, Origo

The other day a member of the team wrote this in an email to us all: “It’s so exciting how highly anticipated this service is ”“ we’re really doing the right thing for people in the industry.”

She was referring to a brand new service Origo had launched in the financial services (pensions, investment and savings) market, with which we had set out to tackle one of the most frustrating issues for the administrators, paraplanners (think para-legals for the financial planning market), financial advisers as well as the product providers and platforms in our industry. This is conveying the authorisation required from the client of the financial advice firms by the providers and platforms, stating that they are authorising the advice firm to act on and transact on their behalf; termed the Letter of Authority (LoA).

On the face of it you’d expect this to be a simple process and hardly an issue for an industry that transact billions of pounds every year. Right?

The actual situation is this: A myriad range of requirements and different pieces of information being required by providers and platforms; paper-based systems; pieces of paper having to be posted or faxed(!) to every individual provider/platform; no way of tracking the process, so no way of knowing if it is being dealt with or how long it will take. You can imagine the resource and cost implications all along the process chain.

Here’s a quote from someone on the front line:

“We offer an outsourced administration support, alongside our paraplanning services, and our administrators spend a lot of time finding out how a provider wants to receive the LoA (not everyone accepts emails and some still insist on seeing the wet signature, and these requirements seem to vary all the time), making sure the LoA actually got to the team which is supposed to be dealing with it and establishing current turnaround times, and finally chasing for information, often spending hours on hold each week only to be told there’s currently a backlog. Providers must also spend a lot of time answering these calls.”*

If you want to read further of the frustrations this is causing those dealing with this administrative burden, read this article on LinkedIn [ https://www.linkedin.com/pulse/sending-letters-authority-2020-debbie-condon/ ].

It’s written by Debbie Condon, founder of Intuitive Support Services, an outsourced administration firm for this market. She tells how she has had to put together a spreadsheet of 100 companies (there are many more in the industry) for her team of administrators laying out what each company needs and in what format and to which department the information should go. Needless to say, we asked Debbie to be one of the testers for our new service.

Hopefully, this gives a flavour of the issues and frustrations being experienced.

So, how have we tackled this. First, we did one of the things we do best, having identified the issue, we brought together a range of different industry participants to ascertain what they would need to create a common, efficient digital process that would meet the requirements of the industry and they would all be happy using.

From these working groups we developed the Unipass Letter of Authority service. Unipass is one of our brands ”“ 8 in 10 financial advisers use Unipass Identity for example to safely connect to the websites of the various providers and platforms they use on a daily basis.

In a nutshell, Unipass Letter of Authority enables the person in the financial advice firm to enter all the client’s details in a common format and for that information to be sent to all providers and platforms on the system. No laborious form filling for the advice firm and no postage cost.

Also, by securely digitising the process, Unipass Letter of Authority enables advice firms to know where they are in the onboarding process, so they can keep up-to-date with progress and keep the client informed, helping to improve their customer service.

This is a service that the industry tells us it has been crying out for and we are delighted to have been able to work collaboratively with participants in developing it. To accelerate the use of the service and the benefits it can bring to the industry, we are making it free to use until July 2021, allowing advice firms, providers and platforms to experience first-hand how the service will work for them.

I’m going to end with a quote from Debbie Condon: “What we need is for providers to sign up to this system as soon as possible. The more companies that are on board, the faster, easier and cheaper this process will become for the industry and the better the quality of service adviser businesses will be able to give to their clients.”*

Having this kind of impact on the efficiencies and for the people in our industry is what inspires everyone at Origo to be the best they can be in their jobs. The new Unipass Letter of Authority is just one of several innovative services we provide for our part of the industry and I am extremely proud of what we do as a FinTech to help address these issues.

An Edinburgh company doing its best to change the industry for the better.

Unipass Letter of Authority launches on 23 November 2020.

* Quotes from articles published by Professional Paraplanner magazine.

https://professionalparaplanner.co.uk/new-letter-of-authority-service-could-be-game-changer/

Inclusion, fintech and future talent

Inclusion drives fintech innovation

This has been an action-packed time for everyone involved in the FinTech Scotland Cluster. With COVID-19 continuing to have an impact on our lives both at work and at home the energy across the cluster continues to inspire us.

In particular there has been an even stronger focus on inclusion. Since I’ve known it, this topic has always been front of mind for all involved in the FinTech Scotland Cluster. The work over the recent weeks has continued to demonstrate the drive to build an inclusive environment that enables diversity to win, innovative environments to advance future opportunities for all and build business success.

Inclusion driving future talent

We’re continuing to learn about the full range of organisations across Scotland that are working in practical ways to build skills, experience and communities to help people from different backgrounds explore opportunities in FinTech and Tech. It’s always a pleasure to learn about the practical approaches being taken to support and enable inclusion.

Code your Future is strengthening its focus in Scotland. It works with people who have had limited access to education, offering practical tech training to anyone that’s experience problems in getting meaningful work. There are ten graduates on course to graduate in November, who will be looking for opportunities. Previous graduates are working at BBC Scotland and STV, and code your future has plans to support another class of 30 students next year.

We’ve also been working directly with the team Inlcusion Scotland over the past few weeks as we look to expand the FinTech Scotland team through an internship. Inclusion Scotland work to ensure the full inclusion of disabled people into all aspects of Scottish society can be achieved. All of us a FinTech Scotland very much looking forward to adding to the team.

Inclusion drives business development

It’s been great to see the hard work from the team Lloyds Banking Group pay off so successfully as they launched the Launch innovation lab. The innovation themes of digital services and ESG are another example of the conscious focus being given to the topic of inclusion. Congratulations to Inbest and Legado who are both participating in the programme.

Obashi also shared an exciting development this week as it joins the World Economic Forum’s innovators community. An inclusive first for this forum, for Obashi and for Scotland. Obashi’s work is another great example of inclusion driving business development, moving from the oil industry to share its experiences of dataflow frameworks to bring clarity to new sector.

Inclusion drives financial inclusion

Over the last few weeks we have continued to see the efforts of many across the FinTech Scotland Cluster continue their unwavering focus on financial inclusion.

Amiqus continues its work with proxy address and launched a new trial to test the proposition. It works to provide those in danger of losing their home and subsequently their address with a proxy address and the innovation has the potential to ensure people continue to get access to vital services including access to the benefits they need.

FinTech focus on financial inclusion has also been supporting the UK’s Money and Pension Service (MAPS) who has recently launched a UK Financial Wellbeing Strategy. Thank you to, Nude Visible Capital Soar Directid FastPAYE and Money Dashboard for sharing your views. We know there will be more on this over 2021 and that COVID-19 has brought the topic of financial inclusion into sharper view.

Pinsent Masons recent research on Creating a Culture of Support in Financial Services has focused on the topic of Money and Mental health. It draws on a range of perspectives from a wide and diverse group of industry participants and explores a range of initiatives being built to offer inclusive support for those that want it.

And on a final related note, this week has been Talk Money week, another initiative to encourage people to engage in money and to get us all talking about it. Experience shows that money continues to be a taboo subject and research has highlighted that often people find the subject to daunting and complex. FinTech’s such as Sonik pocket and Moneymatix are working to help children engage with money and financial decisions at an early age. A bit like those why’ questions our children are so good at asking, innovations like this might go some way to helping us all talk about money.

Hoping you all stay safe and well.

Nicola

FinTech and Translation Industries; Interesting Bedfellows

When one looks at the business challenges and technological advancements, shared by both FinTech and Translation Industries, alike, quite a few interesting synergies emerge, including:

- Both being enablers of global online client interactions

- Both enjoying unlimited client reach

- Both disrupting traditional workflows, via technological advancement

- Shared concerns regarding data security

Enablers

FinTech is one of the most rapidly expanding sectors in the world, revolutionising personal & business finance, via online banking and applications. FinTech has changed the finance game, forever, and has rendered traditional banking methods, extinct.

Whether it is, the exchange of foreign currency, the ability to trade in cryptocurrency, the ease of access to the world of investment, or making payments via mobile, the sheer scale of opportunity is remarkable.

The translation industry, of course, performs the translation & localisation of banking apps, websites, and communications that all enable global trade. New advances & developments in translation technology, have played their part in changing the entire client experience. This could be through automated translation as opposed to human translations, secure portals for the transfer of client files, API technology to connect client and supplier systems, or Online Editor facilities.

Unlimited Client and Workforce Reach

Online workflows & operations mean that, in both industries, there are no geographical barriers to having a global workforce or client base. Translation & localisation also ensure no limitations in the launching of new products to international audiences.

Accredited translation agencies have invested and incorporated the latest technologies within their workflows. Their skillset in managing complex localisation projects, ensures that the FinTech industry can quickly & effectively market their services globally.

Although FinTech communications can be handled seamlessly, accreditation is an altogether different story. One principal issue that FinTech faces when expanding, is navigating the relevant local regulation. With codices differing between, and even within, countries, the legal side of FinTech growth is far from simple.

Technology: Disrupting Traditional Ways of Working

FinTech and Translation companies can successfully operate without necessarily needing brick & mortar facilities. Of course, there are both advantages & disadvantages to fully-online-based organisations; for those with global operations, however, the advantages are manifold. For example, lower operational costs allow SMEs and Start-Ups to invest in personnel and the business itself, rather than being burdened with the heavy cost of facilities.

Although, being location-independent does present its own set of challenges. The puzzles of how to best: manage, motivate, or support staff effectively, for instance.

Data Security

Data security is essential in all industries and sectors; this is especially acute with respect to financial transactions and the security of client translation documents. Unfortunately, we are all too frequently confronted with news of ransomware cyber-attacks, against companies such as North Hydro and Travelex. That said, this threat is perennial to all industries and companies.

Most translation agencies enable clients to order & transfer files online, via a secure Client Portal’. For the most technologically advanced translation companies, the client files are not issued directly to external translators, as was done in the past.

This new workflow facilitates the translation of files directly within the online translation platform, accessed via the unique & secure portal. Maximum security for client IP, is thus, guaranteed.

A Conclusion

As little as five years ago, it was unimaginable to foresee such a rapid shift to mobile apps & online-only operations; it is fascinating to contemplate where we will be in five years’ time.

These technological developments are not only advancing services & capabilities within the industries themselves, but also other, more indirect, business benefits. These include: a global unlimited client base; online-only operations; physical office facilities becoming no longer necessary; or flexible working options.

All of this significantly lowers the barriers to entry for entrepreneurs in all industries internationally. It will be enthralling to see this continued evolution, and what lies ahead for all of us.

This blog was written by Fiona Feldermann McCrae, Managing Partner, at McFelder Translations.

McFelder Translations, an ISO accredited powerhouse with almost two decades of technical experience, is your passport to building a global brand.

If you’d like to find out more about localising your FinTech communications, email: fiona@mcfelder.com.

Website

LinkedIn

Twitter

Instagram

Image created using Canva

Making FinTech more diverse and representative

Rise, Barclays’ FinTech ecosystem, is spearheading diversity and inclusion in the sector. This wide-ranging topic is the subject of the latest edition of Rise FinTech Insights, a regular publication from the bank.

This blog was written by Clare Whitehead, FinTech Platform Lead, Rise London

Building a more diverse future for FinTech

Working towards a more equitable future starts with addressing the wealth gap created by unequal access to resources by underepresented communities. Bridging the gap starts in the very early years from focusing on STEM eduction to the later years by providing FinTech resources for the baby boomer population.

The next generation is very evidently making great strides in FinTech when you watch Stemettes in action. Dr Anne-Marie Imafidon MBE and her remarkable organisation allows girls and young women to get creative with technology and see the opportunities available to them in joining one of the fastest-growing (but still male dominated) UK sectors.Pre-lockdown, Stemettes, their siblings and their parents would regularly take over our Rise London building to work on Future of FinTech’ hackathons. Based on the energy and enthusiasm of that crowd, we should be seeing more women in our sector in the years to come.

Rise community leading the way

We call the Rise ecosystem the #HomeofFinTech because it fosters such great technology and talent. The latter includes several diverse pioneers, and they deserve a shout-out. To name just three from our sites around the world:

- Kevin Barrow is a Black founder in our community and CEO of Mark Labs, a London-based FinTech company that shows how money can be used as an instrument for creating positive social and environmental change at scale.

- Nadia Sood is the female founder and CEO of CreditEnable, a Mumbai-based credit insights and technology company that applies proprietary data analytics, and AI to build solutions to the world’s biggest financial challenges.

- David Beatty is a co-founder of Gaingels, a New York-based company focusing on co-investing with leading venture funds in companies that embrace LGBT leadership.

Building and maintaining a diverse and inclusive environment are at the heart of Barclays’ values: Respect, Integrity, Service, Excellence and Stewardship. The global corporate and investment bank is a better, stronger and more successful organisation as a result of it.

As Jes Staley, Group Chief Executive Officer, Barclays said recently: “We are deeply committed to empowering the next generation of leaders, providing access to enterprise, employability and financial skills.”

A call to action

Personal empowerment is perhaps the main driving force in any diversity initiative, and these leaders demonstrate how effective it can be. Empowerment of a different kind can come when underrepresented communities come together to effect change in a system ”“ like the Latinx community in banking. Ramona Ortega, Founder of My Money My Future, argues the case with a FinTech call to action to create a more diverse FinTech sector. Speaking for that community, she calls on us to:

- Help more FinTech founders of colour get funded. Get to know them and open up your network to them.

- Partner, support or even acquire small diverse companies and, as a result, add value by reaching new markets (because existing products doesn’t fit the market for people of colour).

- Give Black and Latinx folks a seat at the table. If you’re launching a diversity campaign or coalition, make sure to have them involved.

And, if you’re a FinTech VC, take the time to research the opportunity and make a pledge to fund a Black or Latinx founder.

In case you were wondering, supporting the Black and Latinx community in these ways makes great business sense because the future will be even more diverse than it is now, with 2020 being the year when more than half of all Americans under seventeen years old are from a minority background[1] and with Latinos making up 35% of Gen Z[2].

AI ”“ the part diversity plays

Does technology have a part to play in making FinTech more diverse and representative of our societies? It certainly does. A great example is how we can use technology to design out bias in the many AI algorithms at the heart of so much data analysis and business decision-making. The way that financial decisions the algos make can be intrinsically unfair, and this bias is now seen as the biggest risk in data-driven technology[3]. Bias can creep in at any point in the development process, but technology and regulation both play a part in mitigating it. But a number of tools can measure bias and the trustworthiness of algorithms. Some are open source, some commercial. Furthermore, there are considerable efforts across academia to enhance these tools and provide improved algorithmic transparency and explainability’.

However, technology alone is not enough. As Ana Perales, AI Horizontal and Conception X Lead at Barclays Ventures, explains in the Rise FinTech Insights report, other factors are key to minimising bias. These include design and regulation. Designing ethics into algorithms requires, among other things, the very teams (of data scientists and developers) that create the code to be diverse. Additionally, developing a culture of frequent testing to collect data in an unbiased and systematic way should be part of any design.

Tracking changes to government regulation is key. Regulatory consultations and frameworks for AI highlight the close link between fairness and bias, on the one hand, and transparency and explainability on the other. For example, the European Commission, the Monetary Authority of Singapore, the Financial Conduct Authority and the Information Commissioner’s Office have all issued guidance that includes principles of fairness, bias, explainability and accountability. Check out Rise FinTech Insights for examples of how bias can creep into AI and of startups that specialise in analysing and reducing bias.

The distribution of AI companies across the Rise ecosystem

Download all editions of Rise FinTech Insights here.

[1] https://tribecamarketinggroup.com/tribecatrending/get-to-know-hispanic-generation-z/

[1] Report: AI Barometer by the Centre of Data Ethics and Innovation

Europe’s Fintech Startup Environment – And How The Current Crisis Drives Its Further Development

Europe is great in many ways, and a favorable environment for many economic sectors to flourish – and the fintech startup industry is definitely among them. While the Silicone Valley is booming, and Atlanta is following as a close second, the regional players, such as Estonia, are emerging to challenge the world’s most prominent fintech hubs.

European fintech environment today: an overview

One can easily see the benefits available to the fintech entrepreneurs that choose to base their companies in Europe. Among the most prominent ones is the European regulatory environment, which is both start-ups oriented and tailored in a way that fits the specifics of each of the states in the region and the European market as a whole.

Having said that, we should also note that there are a number of challenges that are preventing Europe from making a strong standing among those with the most attractive start-up environments in the world.

Firstly, unlike the US start-ups, ones based in Europe need to rethink their line of development. While the former is more focused on market penetration and a marketing boom that will make them widely known, the European start-ups need to secure the revenue first, before thinking of what the next step should be like.

And, secondly, despite London and Berlin – the current fintech startup hubs of Europe – entrepreneurs based elsewhere can sometimes struggle to have access to funding opportunities. The lucky few manage to get initial funding outside the region – in the USA or Asia, however, once that is secured, the start-up is also likely to abandon Europe for a more favorable environment.

Despite the challenges listed above, Europe remains to be the birthplace of the fintech unicorns, such as the Swedish payment system Klarna, the UK’s bank for entrepreneurs OakNorth, N26, and the Revolut, that we will examine in a bit more detail later.

Amidst the outbreak of the COVID-19 pandemic, the European fintech sector is likely to flourish even further. With the digitalization of most of the products and services, the demand for fintech solutions is growing – and European start-ups are all too happy to cater to it. The main sectors that the regions’ fintech entrepreneurs are targeting are blockchain, banking, and financial trading, and we will discuss them in more detail below.

Blockchain – The Newest Solutions To The New Trends

Ever since the blockchain solutions were first introduced, their popularity did not cease to stop growing. The current estimate is that the world blockchain spending will increase to more than 15 billion in 2023.

However, with such a rapid expansion, it became apparent that some sort of regulatory mechanism is imperative to ensuring the safety of all the parties involved. But how does one control something so strongly based on anonymity?

The solution was once offered by Ethereum (which, coincidentally, was co-founded by a programmer of Eastern European descent – Vitaliy Buterin). Smart contracts that the company came up with are now widely used to document the details of transactions, and can even be used as a legal confirmation in court disputes. The technology is especially popular with the individual lenders in Europe, as they act as an additional layer of security for both the lender and the borrower alike.

Financial Trading ”” Innovation With Benefits For All

Financial trading is one of the rare few of the markets that was always glad to welcome new technological solutions and incorporate that into the traditional way of functioning. It is, therefore, unsurprising that European start-ups are often trying to tailor their services in a way that best caters to the needs of this market niche.

A good example of that would be the UK-based fintech company Revolut. In an attempt to both expand their customer base and penetrate the financial trading market, Revolut came up with an idea of integrating their services with the brokerage offering, and it worked out very well for them both. Revolut did expand their client base and made themselves even more recognizable, trading service providers obtained an efficient payment system to offer, and the traders benefited from a mechanism that significantly reduced the hassle involved with depositing or withdrawing funds.

After proving to be both efficient and profitable, the integration of services with financial trading was soon picked up by the European fintech start-ups and continues to be done so today. There are only a few downsides to this development, and the most prominent among them is the lack of accessibility to the full services that either a trading company or the Revolut (and other fintech companies of a similar nature) has to provide. The client of a fintech service provider would still have to join a trading company separately, and, similarly, the trader will have to get in touch with the fintech to get access to the full variety of their services.

Other than that, functional integration goes a long way to show that there is definitely potential for the Europe-based fintech start-ups to come up with breakthrough technologies and reclaim the title of being listed among the world’s top largest technological hubs.

Banking – A Means Of Achieving The Ultimate Goal

Although the banking segment is strong in Europe, there is one struggle that it is yet to win – namely, the desire to achieve 100% of the inhabitants of the region being banked. While the numbers are sufficiently high in Western Europe, the situation is very different in the Eastern part of the region.

With that in mind, European fintech start-ups have stepped in to try to solve the issue of unbanked citizens. Russian Tinkoff online banking, recently valued at over 5 billion USD, is a shining example of how financial technology can offer a working solution. Tinkoff is completely digitized, and, in that, reduces the hassle of having to physically visit one’s bank to virtually non-existent. With such convenience combined with the efficiency and trustworthiness of the service provider, Russia saw a significant increase in the coverage of the previously unbanked population.

The opportunities for fintech start-ups in Europe are widely known and actively used, and on top of the prominent regional fintech centers, such as Berlin and London, Europe is currently seeing a rise of the new players, such as Estonia, Bulgaria, and Lithuania. The niches to occupy are plentiful, and the outbreak of COVID-19 is generally favoring technological advancement, however, there are still a number of aspects of the industry that need to be refined – with the lack of accessible funding among the most obvious ones.

If the current crisis and the fintech boom associated with it will lead to those challenges being successfully resolved, Europe can easily become a strong competitor to the United States and Asia in the development of modern fintech solutions.

Photo by Jonas Leupe on Unsplash

Ambition Can Attract the Right Talent

A few months ago, Mark Logan produced his long-awaited, government-commissioned report on the Scottish tech ecosystem, of which FinTech is now a key component.”¯

There were many positives. We have established a thriving, well-connected community. However, Mark was quite clear; things need to change.”¯

We need to think bigger; we need to push boundaries and reach further than many think is possible, capitalising on the global opportunities that will take us beyond the tipping point.

One of the pillars at the heart of Mark’s vision for a larger, more robust Scottish Tech ecosystem was, of course, people.”¯

But how do we attract this critical talent?”¯

Growing our own talent, working with schools and universities to prepare future captains of industry is vital. Making sure the technical skills taught are combined with commercial acumen is critical. However, this is a generation away.”¯

To realise some more immediate returns and to capitalise on the global opportunities, tech companies in Scotland need to attract the sort of investment required to be an international player and employ the talent with the experience and knowledge to succeed.

Embrace Your Ambition

With COVID19 banishing most traces of presenteeism and reassuring business leaders that it is possible to operate remote teams without impacting on productivity, this has opened up access to a far more significant, global labour market.”¯

However, while the talent exists, encouraging them to join your team instead of sticking with the FinTech operating out of London isn’t easy.”¯ ”¯ ”¯ ”¯ ”¯”¯

What was clear from listening to Shane Kehoe, Co-Founder at SVK Crypto, who was a keynote speaker at EIE20, is the acknowledgement from London that there is an incredibly exciting scene here in Scotland. However, for whatever reason, the investment and to a certain degree the talent isn’t making its way north at quite the speed we would hope.”¯

Something both Shane said at EIE20, and Hector Mason, Investor at Episode 1, mentioned when we interviewed him for the TalentSpark podcast last year, was that the level of ambition shown by the companies in London and America is exceptionally high.”¯”¯

Our inbuilt Scottish apprehension prevents many from showing the global ambition we harbour, and from taking the risks that perhaps our counterparts in Silicon Valley, and to a certain degree those down in London, take for granted.”¯

These founders are shooting for the star’s fuelled by mind-blowing ambition, and many eventually fail. However, the lessons they learned along the way, will be invaluable to an emerging FinTech and the experience will help attract more significant levels of investment.”¯

This faster turnaround of experienced talent was, in fact, one of the potential solutions suggested by Mark Logan in his report.

Define Your Market

Another key aspect of attracting the right talent for your business is defining your ‘why’.”¯

Whether you are trying to attract the COO from a FinTech that has just exited to a global institution, or you have your sights set on securing the services of the most inspiring CTO, you need to sell a vision of a business that does more than it says on the tin.”¯”¯

This concept became abundantly clear when we worked with one of Scotland’s most exciting new FinTechs‘, Nude.”¯

Lots of company leaders and advisors talk about creating the right culture, but Nude have worked hard to define their culture and make it a key component of their hiring process.”¯”¯

Nude has now raised £5.7m, and their most recent raise was to help them deliver on the government-backed Lifetime ISA (LISA), created to help first-time buyers get onto the property ladder.”¯ ”¯

However, there was a time pressure on getting the LISA product to market, and it required the recruitment of up to ten staff. It was an exciting project for our team to get stuck into but daunting none the less.”¯

Nude’s Why

Their one goal is to:”¯

“Help you reach life’s most important life goals, starting with buying a home”.”¯

So, the ‘why’ was clear, and after meeting with Stephen Doherty, COO, it was apparent their culture was laser-focused on customer-focused delivery.”¯

Having this made the process that we went through very clear. It helped us define the type of person we were recruiting for making shortlisting far more effective. The vision and values also helped sell the opportunity to an already engaged audience which meant the candidates we put forward had a higher chance of success, reducing the time to hire considerably.”¯ ”¯

So, while defining the vision and culture of the company certainly helped us, it created a very attractive proposition in an incredibly competitive marketplace.”¯

Diversity and Inclusion

Living and breathing an inclusive culture from the very top is not only the right thing to do, but it makes financial sense too.”¯

While no one should have to be convinced of the benefits of a more diverse mindset throughout your business, based on the potential financial upside, it does seem to be rolled out as part of the argument.”¯

Jacqueline De Rojas, Chair of Tech UK, has highlighted the imbalance of female representation in the tech sector, and the potential impact this can have on everyday lives.”¯

The retention rate of Black, Asian and Minority Ethnic is far shorter than that of their white counterparts. This could be in part down to the, on average 13% lower salaries compared with their white workmates.”¯

However, it is almost certainly also the result of a lack of buy-in from senior-level executives to embody change, making the role of Chief Diversity Officer (CDO) incredibly frustrating.”¯

It is incumbent on senior leaders, founders and CEO’s to take ownership of the diversity throughout their organisation. They need to embody the culture and take action to stamp out any perceived bias. Only when the policy is taken seriously at the top level will change genuinely take place, and companies will see the financial benefits of having a diverse workforce.”¯

So, if the many fantastic companies that make the FinTech sector here in Scotland are to achieve the growth they all grave, they need to be brave and embrace their real ambitions. They need to define their vision and culture and embody a diverse and inclusive hiring approach.”¯”¯

Author

- Peter Dunn

- Associate Director (Tech and Digital)

- Eden Scott

- 07795 553 835