Global climate tech investment more than triples, but could be better targeted to cut emissions

In December 2021, PwC Global released the State of Climate Tech report. The analysis examines how investors are improving both climate impact and commercial returns through the emerging asset class of climate technology, helping to keep the Paris Agreement’s goal of limiting global warming to 1.5 degrees Celsius within reach.

This represents an increase of 210% from the US$28.4bn invested the year prior, with 14¢ of every dollar of venture capital investment now going to climate technology. PwC’s State of Climate Tech 2021 reports that where the investment is lacking is in addressing the largest contributors to global emissions. From the 15 technologies investigated, the top five technologies, which represent more than 80% of emissions reduction potential by 2050, received only 25% of the climate techinvestment between 2013 and H1 2021.

Emma Cox, Global Climate Leader, PwC UK, said: “The world has 10 years to halve global greenhouse emissions if we are to have hope of achieving net zero by 2050. Innovation is critical to meeting the challenge and the good news is that climate tech investment is up significantly across the board. However, our research has found there is potential to better channel and incentivise investment in technology areas that have the greatest future emissions reduction potential. This raises the question of why these sectors are missing out ”“ are investors missing a value opportunity or is there an incentive problem that needs the attention of policy makers?”

To find out more about PwC’s Climate Tech report, please contact Jason Higgs, Partner, PwC jason.c.higgs@pwc.com

Introducing mnAI to the fintech ecosystem

mnAI is a multi-award winning data, insight and analytics platform that provides information on all unlisted companies in the UK. It is the UK’s largest and most comprehensive source of data – a single, unified source that holds 10bn+ data points on 8m+ UK companies. We apply a wide variety of machine learning algorithms and filters so users can access targeted, customised information and insight across industries, sectors, and geographies far more rapidly than is currently possible.

The platform is used by, amongst others, investors, advisors, corporates, professional services, government and educational establishments to improve their insight and efficiency, to enhance and support their operations across several departments, while at the same time reducing their costs.

Ricky, our Managing director in Scotland, tasked with growing the business in Scotland and beyond said:

“With Edinburgh being named as one of the UK’s leading tech cities we are delighted to have become part of the Fintech Scotland ecosystem. Stephen Ingledew and Nicola Anderson have done and continue to do a remarkable job and the whole team at mnAI look forward to developing a very long-standing and close relationship with the Fintech teams across the UK. The power of data is now more valuable than ever and we believe the mnAI platform will only add value to strategic partners across the UK.”

To find out more about our platform and technology please visit us at mnai.tech

Flock selects Scottish fintech AutoRek

Scottish fintech AutoRek, just announced that Flock had joined their now extensive list of clients.

Flock is an innovative firm all about reinventing business models around insurance. They are looking to build a global, fully digital insurance company for connected commercial vehicles to mitigates risk, rather than just paying claims.

AutoRek was chosen by Flock because of its flexibility.

Flock will be using AutoRek to:

- Automate bordereau, bank and payment reconciliation requirements

- Calculate broker payments to generate statements to brokers and paid bordereau

- Take various external data sources from other insurance organisations, as well as from the general ledger

- Underpin Flock’s Insurance Broker Accounting (IBA) operations

Gordon McHarg, CEO at AutoRek, added,

“It is excellent to have Flock come on board as a new client. We are delighted to be seen as a flexible and adaptable tool to help fast-growing companies like Flock scale their business. We look forward to continuing this partnership over the coming years.”

Piers Williams, Insurance Lead at AutoRek, added,

“We are excited to work with Flock, they are disrupting the insurance industry with innovative new products. Behind their exciting business is a foundation of leading software solutions that are enabling the business to achieve its objectives. Flock will be deploying AutoRek’s bordereau reconciliation and financial control solution to deliver end-to-end automation.”

Fintech DirectID Raises $3m in Bridge Round

Scottish fintech DirectID just completed a $3 million (£2.2m) bridge round led by Hong Kong based venture capital firm QBN Capital. The firm grew its team and revenue by over 100% in the last year and this investment will help them pursue their ambitious growth plans and expand internationally.

DirectID has developed a market leading credit & risk platform that powers some of the world’s largest brands through the use of Open Banking data.

DirectID provides unique insights into customers’ financial situation, enabling financial institutions to have a more realistic view of credit risk and to make faster, more accurate and personalised decisions.

Based in the UK, DirectID is connected to over 13,000+ bank which represents 1.5bn users in over 45 countries.

James Varga, founder, and CEO of DirectID, said:

“We are very excited to have QBN being our lead investor. This funding step will help us grow into more markets and sectors as open banking adoption grows across the world. We are addressing a global pain with our product, redefining credit risk for consumers and businesses alike.”

Philea Chim at QBN Capital said:

“We look forward to helping DirectID expand their business to Asia. Their credit risk platform will make SME financing fairer and more accessible. We see synergies between DirectID and a number of our portfolio companies and QBN’s own initiatives, for example, in supply chain trade finance.”

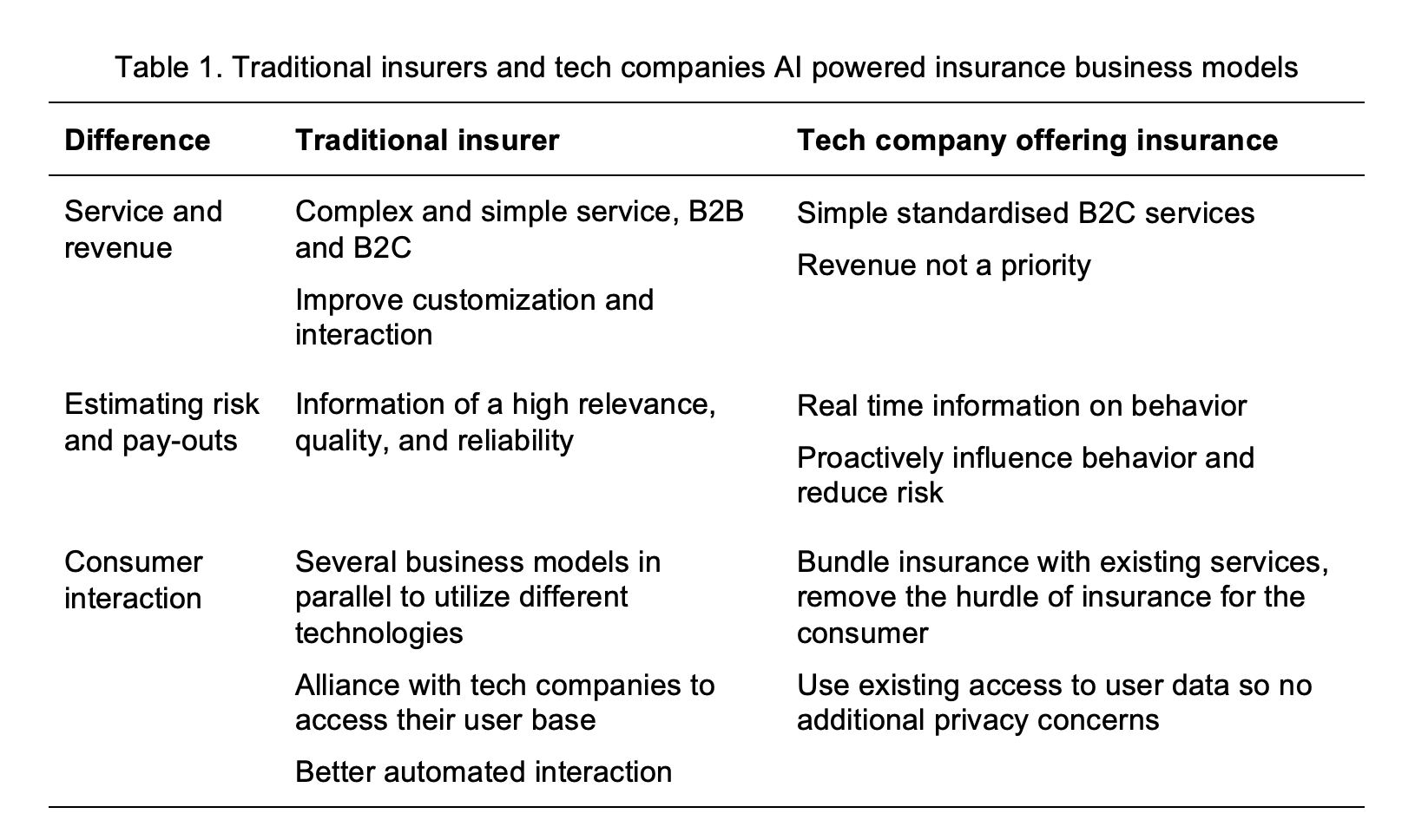

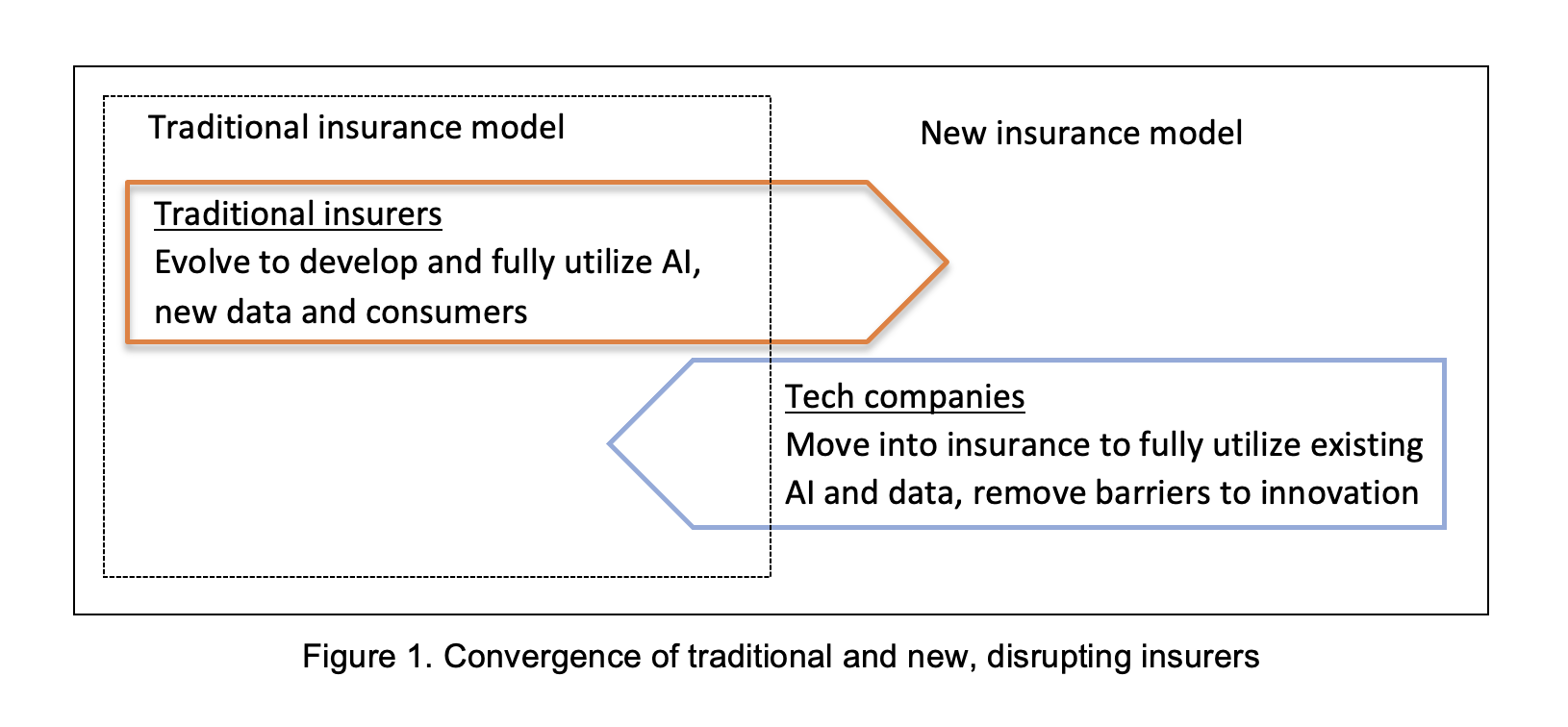

Existing insurers and disruptors are utilizing Artificial Intelligence to create new business models

We can see that Artificial Intelligence (AI) is transforming many parts of our lives, but do we know where this journey is taking us? Insurers need some certainty on what their future will looks like. Some new insurers are trying new business models enthusiastically and then changing direction sharply, like a speedboat swerving to avoid a collision. The larger insurers, however, are like large cruise ships; they need to be able to see far ahead before they plot their course, and they don’t want to keep changing direction.

This research tried to identify the viable AI driven business models to help give some clarity. Some traditional insurers are just trying to be more effective with AI, while others reinvent themselves to fully utilize the new capabilities available. Tech-savvy companies from outside the sector like Tesla, are entering and disrupting it. Would these diverging paths continue, or would they converge in the future towards one, ideal, business model? This research focused on one example of a traditional insurer and one new tech-savvy disruptor and evaluated whether their models are converging.

AI is changing the insurance value chain, as illustrated in figure 1. Most new insurers, like Tesla, offer fully automated simple services. The traditional insurers offer some of their simpler services in this way. The more complex services are supported with AI, but a human makes the final decision. An example of this are audits for fraud, where the AI identifies unusual patters and cases for an expert to evaluate.

There are signs of convergence between the models of traditional and new insurers. First, there is convergence in technologies, such as the use of chatbots utilizing AI. Second, there is a convergence in processes, for example, the interaction with the consumer. Third, there is convergence in the strategy on costs and pricing.

However, there are two areas where there seems to be a limit on convergence, which seems to suggest the business models of the incumbent and the disruptor will remain distinct. These are: (1) evaluating risk and (2) the cost of attracting the user and profitability.

Despite some convergence, certain differences are likely to remain even after this transitionary period. This is because the two models have distinct competitive advantages. Traditional insurers no longer monopolize the capability of providing insurance, but they still have the existing user base and utilize it to evaluate risk. Technology-savvy companies that now offer insurance, have their own forms of engagement with their consumers, use different methods to evaluate risk due to their access to real time data, and do not prioritize generating revenue but instead utilize insurance to increase their user base, overcome barriers, and reduce the overall cost of their products and services.

Therefore, when insurers are thinking about how to utilize AI and plot their course through the turbulent, unpredictable times ahead, they should stay true to what they are. This is their comparative advantage.

Dr Alex Zarifis is a lecturer at the University of Nicosia in Cyprus.

This article is adapted from his paper, “Evaluating the New AI and Data Driven Insurance Business Models for Incumbents and Disruptors: Is there Convergence?” available from https://doi.org/10.52825/bis.v1i.58.

PRESS RELEASE: Automation the key to growth and data management for banking and payments sector, finds new report

A new report from leaders in reconciliation and finance automation software, AutoRek, has found widespread concerns around the ability of businesses to grow amidst scalability and regulatory pressures over the next three years, affecting 92% of professionals surveyed.

The report ”“ Banking and Payments in 2022: Digital transformation and trends in financial technology ”“ was designed to provide an insightful view of the key challenges and solutions that will face the financial industry as it enters 2022.

AutoRek gathered insights from senior professionals across the banking and payments industry on the barriers they face surrounding the handling of payments data, compliance and growth, and new technologies in use or consideration.

Automation was found to be a key source of hope for enabling growth and regaining competitive advantage. Other key findings include:

- Manual processes form the biggest roadblock to achieving automation, cited by 46% of firms, followed by legacy systems (42%), poor interoperability (40%) and regulatory requirements (38%).

- In-house IT solutions are the most common for data handling across payment operations, used by 44% of firms ”“ a higher reliance on in-house systems than in most other sectors.

- Almost one-third of firms consider their jurisdiction’s regulatory body audit and control around regulatory reporting infrastructure somewhat or far too strict, while 22% consider it somewhat or far too lax. Just under half consider it appropriate. Financial institutions in central and south America were considerably more likely to view their regulators as lax than their European and Asia-Pacific counterparts.

- When selecting a solution to handle payments data, almost 80% of respondents consider its ability to integrate easily with existing infrastructure a key factor.

- Over half of respondents (56%) either already have or are in the process of deploying modern technologies such as artificial intelligence (AI), machine learning (ML) and application programming interfaces (APIs) to help monitor and streamline their data management processes. One-third had onboarding planned in the next 12-24 months. Only 12% reported having no plans to apply technology to improve data management processes.

Firms slow to adopt emerging technologies should be aware that they are now falling behind in an increasingly automated and competitive landscape, according to Nick Botha, Banking Lead at AutoRek.

Commenting on the findings of the report, Nick Botha continued: “While automating data flow has been a priority for some years now, this survey makes clear how many inefficiencies continue to plague firm’s day-to-day operations when it comes to data processing and reconciliation. Legacy banks in particular are grappling with often more than 20 disparate systems written in varying generations of software, none of which are designed to interact with one another.”

“While a decade ago that might have flown under the radar, the last few years have seen control of the payments space shift from banks into the hands of Payment Service Providers (PSPs), whose ability to deliver totally user-native customer service is forcing the whole industry to step up.”

“Beyond competing for market share, it’s a question of compliance. The costs associated with non-compliance are substantial both from a financial and reputational perspective, and regulators are increasingly less forgiving, as we have witnessed in the last few months with significant fines incurred by some of the world’s largest banks.”

“New technologies like AI, ML and APIs can be used to create greater interoperability and remove or significantly reduce manual interventions and use of spreadsheets. Investing in these capabilities today will enable firms to address evolving customer preferences, mitigate risk and achieve regulatory compliance down the road ”“ essential elements for remaining competitive in the payments landscape of today.”

UK-wide Investment Series announced by FinTech Alliance

FinTech Alliance, the Government-backed digital ecosystem for UK FinTech, has launched its third annual Investment Series, announcing FinTech Scottland as a key partner.

The series aims to bring FinTechs from around the UK together to learn about all aspects of a successful funding round and meet high-profile investors.

FinTechs can:

– Use the FinTech alliance platform for the duration, including the regulated Investment Hub.

– Build their pitch deck with advice from FinTech leaders.

– Network with high profile investors.

– Learn from a series of hybrid workshops on pitching, negotiating deals and more.

Signups are now open for the series, and the process will see a number of regional events across the UK to find the most innovative Seed and Series A FinTechs – including an event in Scotland.

The signup deadline is 30 March, after which there will be a launch party during UK FinTech Week, with workshops running through May and a pitch day in June.

Not ready to raise funds just yet? No problem! You can still take part in all workshops and build your network.

We’re delighted to partner with FinTech Alliance on the series.

For more information, email info@fintech-alliance.com

The future of automation for UK asset managers

The last 18 months have been amongst the most disruptive that the financial services industry has ever experienced, forcing many sectors to reconsider business models.

Asset managers in particular have undergone a substantial transition as video conferencing has replaced client-facing interactions. To better understand how these firms have responded to market disruption, we surveyed 100 Heads of Operations across UK asset management firms to learn about their operational challenges, automation objectives and plans for regulatory compliance in 2022.

From this study, three lessons stood out for their relevance to the wider fintech industry:

1. Operational challenges and tech improvements are company-specific

We asked asset managers what does and doesn’t present a challenge to their daily operational processes.

While the availability of automated systems and adequately skilled staff were highlighted by two-thirds of respondents as the most significant challenge, firms also pointed to many others including the functionality of manual resources, process complexity and a changing regulatory burden.

Although nearly 8 in 10 acknowledge that the capabilities of current systems are hindering operational growth, firms have identified a range of priorities to improve these systems from seamless data flow, AI-assisted dashboards and dynamic data management through to enhanced risk management and talent acquisition.

The variety of responses tells us that no two firms face the same operational challenges and, consequently, that technology infrastructure improvements for 2022 will be equally varied in their application to the asset management industry.

2. Manual reconciliations continue to challenge asset managers

Reconciliation is an essential process for keeping accounts and financial records accurate. In recent years, more firms have been automating reconciliation procedures to eliminate risk of error and improve accuracy.

Despite this, our survey reveals that:

- 60% of asset managers worry that manual reconciliations are the greatest risk to their organisation

- 75% say that the number and volume of manual processes is an immediate operational challenge

- Only 7% say that manual processes present no challenge to their firm

Data preparation was also highlighted amongst the most time-consuming tasks for businesses, which further highlights how the complexity of data management continues to grow year on year. This is consistent with our work across other sectors, where we find that manual processing is really the core issue underlying poor reconciliation disciplines.

With half of UK asset management firms allocating budgets between £0.5 and £10m to address manual inefficiencies, we can expect automation to become more deeply embedded in the industry throughout this year.

3. Regulation is accelerating the trend towards automation

Although manual processing has been steadily declining for years in favour of automation, our findings show that a growing regulatory burden is definitely a factor in this transition.

Just 2% of asset management firms in the UK have no plans to invest in automation to achieve regulatory compliance. For the majority that did, top focus areas include operational resilience, prudential regulation, MiFID II and CASS. A further 7 in 10 felt that automation will be instrumental in achieving compliance with the IFPR regulation, which came into effect on 1st Jan 2022.

These findings tell us that UK firms are actively pursuing automation as a convenient and cost-effective way to fortify against regulatory breaches. Nevertheless, with 42% still pointing to new or changing requirements as the biggest threat to their company, such solutions need to be flexible as requirements continue to grow in scope and complexity.

What does this mean for software providers?

The results of our survey clearly demonstrate that automation in finance will become ubiquitous in the medium to long-term. However, the variety of responses and priorities outlined also shows that firms do not want an off-the-shelf solution; instead, they want a reconciliation platform which:

- Is configurable to specific operational needs

- Eliminates manual intervention through end-to-end automation

- Is purpose-built around specific regulatory requirements

- Is flexible to accommodate for multiple iterations of regulations

Of course, these are welcome findings at AutoRek, where we have spent over two decades working with financial firms to build bespoke solutions for unique reconciliation, operational and regulatory requirements.

In the short-term, it is clear that asset managers recognise how automated reconciliation disciplines do and will continue to form the cornerstone of an effective business model in today’s post-pandemic environment. It will be interesting to see how this plays out across the wider financial industry over the next 12 months.

Photo by George Morina from Pexels

New Chief Commercial Officer at Legado

Scottish fintech firm Legado announced it had appointed Colin McKay as its first Chief Commercial Officer.

Colin McKay has over 25 years of experience in senior roles in the UK and global banking sector.

McKay was a partner in several firms, including K Legal/KPMG Law, Eversheds, and Shepherd & Wedderburn and he also held a variety of management roles and responsibility for various key institutional accounts.

More recently, Colin spent over 5 years as CCO of Almis International a growing financial technology company in the UK banking market, with responsibilities including both sales and account management.

Josif Grace, CEO & founder of Legado said:

“Colin understands the potential ”“ and increasing need ”“ for personal data storage within the digital experience offered by financial institutions, having worked in both the finance and technology sectors both domestically and internationally. We are delighted Colin has decided to take up this role and help us scale the business, laying the groundwork for continued success.”

Colin McKay said:

“The team has already demonstrated an ability to develop a scalable product and close early enterprise deals, and the market’s clearly starting to open up. So it’s a very exciting time to be coming on board….”