Addressing stress in the tech industry

As we approach the summer season and holidays, it’s a good time to reflect on managing the work like balance.

Burnout is a significant concern in the tech industry, given its fast-paced and demanding nature; the constant pressure to meet deadlines and deliver results, to stay updated with the latest trends, acquire new skills, and outperform peers. Tight project timelines, high expectations, and a culture that values productivity all can lead to chronic stress and anxiety. Fear of falling behind or losing job security further exacerbates stress levels.

Post covid, working patterns have changed, more of us are continuing to work more at home, blurring the work-home, work-life distinction. Whilst this way of working has benefit from increased flexibility, the lack of boundaries can lead to increased stress, with remote work arrangements, global collaborations, and the expectation of always being accessible, adding to the difficulties in finding the time to disconnect and recharge.

We need to reconsider the work-life balance. Work ”“ life balance sounds like it is either/ or ”“ we work or we have a life ”“ we have no life at work. We are not one self at work and another self at home, we need a holistic approach, one integrated self at home and work. Work needs to be more life friendly, so feel comfortable taking breaks, recognise that we work better when we are relaxed and refreshed. Keeping continual pressure to perform will exhaust us.

The tech industry can be a double whammy with long hours of intense workloads leaving little time for relaxation and self-care and the sedentary nature of tech roles, with prolonged periods of sitting, limited physical activity, and poor ergonomic practices makes it harder to look after our physical health contributing to health issues such as musculoskeletal problems, obesity, and cardiovascular conditions.

So what can you do about it? Take advantage of flexible work arrangements, any wellness programmes or stress management resources. Make time for you. Recognise when you need a break and make and take time. Talk to colleagues about ways to better organise workloads, communication strategies to maximise your time. Pay particular attention to your home life, research shows that burnout is much more likely to occur if work and home are stressful. If this is the case ”“ do something about it now. Be proactive. Reach out to others to help you, it does not have to be a deep emotional heart to heart, just connecting with someone at work or socially, having a chat, doing something you like, can be restorative. Get outside, do something physical helps you see things differently and find other ways of doing things.

At the heart of our wellness is the ability to have autonomy, that is agency over ourselves, be in charge of ourselves, relatedness, that is connecting with others, and competency, that is recognising our skills. These all contribute to our purpose and meaning. This doesn’t have to be a huge life mission but can be a sense of what’s important to us today. Small acts of kindness, a smile, a compliment, all help build our connectedness to others and make us feel good too. And don’t forget to be kind to yourself as well. Lastly pay attention to your sleep, good sleep protects mental health ”“ but that’s another blog!

Dr Sheila Ross, health psychologist, co-founder Feeling good app ”“ proven audio programmes derived from sports training for recovering mental fitness and resilience. contact sheila@positiverewards.co.uk for more information about how your organisation could benefit from free app access. www.feelinggood.app

Photo by Oladimeji Ajegbile: https://www.pexels.com/photo/man-working-using-a-laptop-2696299/

High confidence in Glasgow’s regional tech sector

Startups and scaleups in the Glasgow City Region are experiencing remarkable growth in venture capital investments, surpassing many of Europe’s prominent and emerging ecosystems.

The Glasgow City Region Tech Ecosystem currently holds an enterprise value of £3.4 billion, marking an impressive 89% increase since 2018.

This positive economic performance has attracted a wave of enthusiastic investors and entrepreneurs. The encouraging news stems from a report published by Dealroom.co on behalf of Glasgow City Council’s Digital Economy team, released on Wednesday, May 24, 2023.

Leading the charge in this emerging ecosystem are regional clusters focusing on healthtech, precision medicine, net zero/climate technologies, space, fintech, advanced manufacturing, and the digital and creative economy.

Councillor Susan Aitken, Leader of Glasgow City Council, stated,

“Glasgow’s reputation for innovation, invention, and ambition continues to shape the city, and this report by Dealroom demonstrates that we are attracting new businesses and entrepreneurs throughout the region. This confidence in our city as a business hub is generating numerous specialised, high-value jobs across Glasgow.”

Dealroom.co, a global data platform, diligently tracks the performance of regional tech businesses, ranging from startups to high-growth companies and their associated investments.

Glasgow City Council announced its collaboration with Dealroom six months ago during the 24th State of the City Conference. At the conference, they unveiled the Glasgow City Region Tech Ecosystem Platform, the UK’s first standalone regional Dealroom platform designed to support local government, academia, and other public-private agencies.

This platform highlights the value of in-depth analysis of startups, scaleups, and innovation assets headquartered, founded, or significantly present in Glasgow. It provides reliable data crucial for entrepreneurs, potential investors, and facilitators operating in or considering entry into the Glasgow marketplace.

Additionally, the platform offers all startups and scaleups a valuable and free, open-source business platform and profile. Meanwhile, the data they contribute aids in shaping the overall growth landscape of Glasgow’s tech ecosystem.

Key findings from the recently published inaugural annual report include:

- Startups in the Glasgow metropolitan area continue to attract increasing levels of investment, showcasing an 8% growth over the past 12 months. This growth stands in contrast to many leading and emerging ecosystems across Europe.

- Startups in the Health, Energy, Real Estate, Fintech, and Semiconductors industries have secured nearly two-thirds of the total investment rounds in Glasgow over the past five years. Notable companies benefiting from these investments include EnteroBiotix, HVS, arbnco, AlbaCo, and M Squared Lasers.

- The first quarter of 2023 marked Glasgow City Region’s third-highest venture capital investment period on record. Noteworthy investments since the beginning of the year include companies such as Phlo Technologies, Causeway Therapeutics, DxCover, and IbisVision.

- Research conducted in city regional universities has led to the creation of over 100 spinout companies. Solasta Bio, Krucial, and Novosound are among the regional companies contributing to this achievement.

- This growth has generated more than 1,000 jobs and has inspired a new wave of entrepreneurial graduates to pursue careers in startups.

Anne McLister, Head of Digital Economy, commented,

“As Scotland’s largest city, Glasgow offers tremendous business appeal, boasting abundant talent and collaborative networks within our thriving tech and creative communities. Our emerging tech ecosystem benefits from the resources provided by renowned higher and further education institutions, including a highly educated pool of individuals with strong research and innovation capabilities.”

Glasgow’s three distinct university-anchored Innovation Districts underscore the region’s unparalleled allure as an attractive, high-quality, and cost-effective living environment for entrepreneurs and startups.

The Centre for Finance, Innovation and Technology recruits

The Centre for Finance, Innovation and Technology (CFIT) is delighted to reveal that it has teamed up with Recruit121, a worldwide expert in talent acquisition within the finance and technology industry, to locate its core senior leadership squad.

CFIT’s objective is to remove the obstacles to expansion in financial technology, and the achievement of this goal depends on creating a robust and efficient leadership unit.

The roles are:

Head of Talent, Engagement & Placements

Director of Coalitions & Research

Director of Ecosystem & Partnerships

Ezechi Britton, CEO of CFIT, commented,

“The Centre for Finance, Innovation and Technology (CFIT) is extremely pleased to announce that we have partnered with Recruit121 in order to source our core leadership team. These first few roles are critical to making CFIT a success and to carrying out our mission to unblock the barriers to growth for financial technology.”

New solution for Pensions Dashboards onboarding

A consortium of four leading technology providers has joined forces to offer a comprehensive end-to-end solution for pension providers seeking to integrate into the UK pensions dashboards ecosystem.

The collaboration between Target Professional Services, mypensionID, Bravura, and Delta Financial Systems is designed to simplify the complex processes and regulatory requirements that providers face when connecting to the ecosystem.

Each firm specialises in a particular area of expertise to ensure a seamless journey toward dashboard readiness before the staging deadline. Target Professional Services uses its leading tracing capabilities to screen and cleanse member data while mypensionID verifies and traces individual members using a verification app tailored to the pensions industry.

Bravura and Delta then provide a jointly developed cloud-hosted Integrated Service Provider (ISP) solution for providers’ data, with a focus on configurability and compliance with the Pensions Dashboards Programme’s (PDP) Code of Connection. The four firms’ technical expertise and market knowledge combine to create a unique solution capable of addressing pensions providers’ urgent and specific needs.

Jonathan Hawkins, Principal Consultant & Pensions Specialist at Bravura, said:

“Delta, mypensionID and Target’s deep expertise and technical know-how in the pensions and data sectors, combined with our ability to process huge volumes of assets and trades on our systems, brings a level of reliability and scalability that pensions providers require right now.

“Pensions dashboards are a crucial step towards modernising and digitising the UK’s pensions sector and, with the clock ticking, pensions providers up and down the country need tech partners with proven scale and expertise. This unique collaboration delivers that solution.”

Photo by Andrea Piacquadio: https://www.pexels.com/photo/young-woman-helping-senior-man-with-payment-on-internet-using-laptop-3823488/

New identity verification standards for new home sales

The Home Builders Federation (HBF) has announced the launch of new and updated customer identity verification (IDV) and anti-money laundering (AML) checks following a successful 3-month consultation period run by Etive. The new process aims to improve the customer experience and align with emerging Government legislation and standards.

The HBF’s new process aims to eliminate the need for customers to show their ID separately to different parties throughout the purchase journey, reducing frustrations, costs, delays, and errors in the process. Customers will only have to prove their ID once during the home buying process.

The HBF consulted with 84 HBF members who responded to the survey, and one-to-one in-depth interviews were conducted with a range of different sized builders across the membership groups. The consultation helped the HBF develop an industry-centered set of rules that reflect good practices amongst home builders and ensure alignment to planned Government legislation.

The consultation’s output has led to the development of two new standards that go over and above the standards set out by DSIT to facilitate the selling of a home. The new standards are compliant with the DIATF and the HM Land Registry ‘safe harbour’.

Steve Turner, Executive Director of the HBF, said, “The new procedures are a huge step forward that will benefit both businesses and our customers and reduce delays, costs, and the opportunity for errors.” Stuart Young of Etive said, “A standard for IDV and AML will drive the industry towards higher standards, reducing the likelihood of money laundering and ID/property fraud, which can only benefit the sector, buyers, and the UK economy.”

The HBF is holding an online industry briefing session on Wednesday the 22nd March at 3 pm to provide further information on the new process. Those interested in attending can email Stuart at s.young@etive.org to receive details.

Photo by Dom J: https://www.pexels.com/photo/uk-driving-license-45113/

FinTech and Space ”“ propelling Scotland forward

We all know that two heads are better than one so imagine the power of two of Scotland’s strongest and most innovative industries coming together to develop tools and capabilities to tackle large scale challenges.

“FinTech meets Space” event in January was the first in a series of joint activities between FinTech Scotland and Space Scotland to spark collaboration between the two clusters and harness the power of cross sector working.

The event brought together thought leaders, industry experts, academics, government agencies, innovators and corporates to start the process of understanding how two very different industries can utilise the capabilities of each other to face off to solve real time challenges.

“You don’t know what you don’t know, so be open to possibilities” was the provocation that started the day off, and it certainly worked. Conversations ranged from the strength of Scotland as a centre of excellence in both fields, to leading edge use of Spatial data to tackle unexpected issues in the health and social care sectors, to more focussed discussions on some live use cases within Financial Services.

These examples spanned a wide range of activities, including understanding insurance risks, building confidence in investments, supporting emerging regulatory requirements and a number of areas of ESG development.

Presentations from Global Surface Intelligence, D-CAT, AstroSat and Earthblox brought some of the possibilities to life, with a joint presentation from the FinTech and Space leads at the University of Strathclyde reinforced the potential for interconnection and collaboration.

The objective of this event was to introduce and to spark conversations between the sectors ahead of a broader Accelerator programme funded by the UK Space Agency.

The programme which will run over the course of a number of months will take the live problem statements and use cases which sparked such enthusiasm in the room and create the opportunity for us to all come together and start working on some tangible prototypes and solutions

We will build on the connections made in the room to form some long lasting relationships and potentially partnerships across our sectors. The potential is vast and the opportunity for Scotland to build on our strengths in both domains to become a world leader in this area is hugely exciting”¦”¦ watch this space!

A FinTech welcome to 2023!

January 2023 marks FinTech Scotland’s 5th birthday! Across that time we’ve seen fintech numbers grow, investment build, partnerships develop, international opportunities prosper and fintech adoption accelerate.

The occasion gives us an opportunity to reflect, consider the future and celebrate the fantastic progress of fintech firms in Scotland.

Over the years these fintech businesses have grown in number, collectively raised over £530m in investment and continue to build businesses with longevity and scale in mind, that deliver positive outcomes for people, businesses and society. It’s a resilient and inspiring group of innovators and leaders and I’m looking forward to the year ahead and the future opportunities to come.

The birthday celebrations were one reason to cheer, another was the news that Stephen Ingledew, our founding father and now our Executive Chair was honoured in the New Years honours list!

A further cause for celebration on two fronts.

Firstly, it’s a richly deserved mark of Stephen’s leadership and commitment, and secondly, it’s another indication of the value that’s placed on fintech innovation across the UK. We’ve always known the value that fintech will bring and it’s given us a further spring in our step as we welcome the possibilities for 2023.

We started those possibilities with an event connecting Space innovation and FinTech innovation. On a bright morning on the 11th of January, in a room full of space tech and fintech innovators, financial and professional service experts we gathered to discuss what we could achieve if we explored the connection between Finance and, Satellite data such as earth observational data or EO to those working in the Space sector.

The answer came when we joined the dots on sustainable finance, and ESG’. There are several pioneering companies, already innovating in this space.

Trade in Space, EarthBlox, Space Intelligence or Terrabotics are great examples of fintechs using earth observational data and technology. Their capabilities can help build confidence in green investing, will shape the future of infrastructure and real estate insurance, build clarity on the environmental impact of supply chains, and help businesses demonstrate regulatory compliance!

The day set the tone for more to come, watch this space!

Data Driven Innovation continues to inspire us, and while we might be at the beginning of our work with Space to drive Climate-FinTech possibilities, other data driven innovators are striving ahead.

January has seen an even stronger renewed focus on financial inclusion, with fintechs including Inicio.ai, Amiqus, DirectID, MoneyMatix, Soar and Inbest.ai continuing to grow and deliver change for citizens across Scotland and the UK.

More than ever, we’re confident that the purpose and intent from the Scotland’s fintech community will help drive the products and services needed to help address the challenges we continue to face.

The potential for 2023 continues, with partnerships and investment top priorities. Br-dge kicked off the year announcing its partnership with Visa and its growth plans for the year ahead! Gigged.ai kicked off investment news with a £1.6m raise to fuel next stage development.

And I’m looking forward to more! Welcome 2023, I’m looking forward to seeing business grow, fintechs scale, investment continue, and more collaboration develop.

On a personal note I’m looking forward to more daytime daylight and a stretch to the evening!

I’m also looking forward to seeing you in February! Please join us on Wednesday 15 February for our first in-person gathering of the year as we celebrate success and look forward to 2023.

New scheme to improve identity checks when buying and selling property

Etive Technologies (Etive) is working with the Home Builders Federation (HBF) to support homebuilders in complying with government regulation and make identity and anti-money laundering checks easier, faster, and more secure.

Throughout the home buying and selling process consumers must provide the same information to prove their identity and confirm details about themselves numerous times. This leads to a frustrating user experience and duplicated effort and costs across the industry, with organisations paying to carry out the same checks on the same consumers.

Etive has been working with the Home Builders Federation to develop a verification scheme to address the current challenges associated with the verification process, and support compliance with the Digital Identity and Attributes Trust Framework developed by the Department for Digital, Culture, Media and Sport (DCMS).

The MyIdentity® scheme enables consumers to carry out digital identity and anti-money laundering checks and share them with organisations as and when they need to. This means checks can be carried out at the beginning of the buying/selling process, reducing customer friction and duplication of effort.

As part of this work, Etive is developing additional identity verification standards that go beyond the framework’s rules, in a bid to better meet consumer and industry needs. It has been working with a cohort of representatives from Barratt Developments PLC, Bellway PLC, Berkeley Group, Miller Homes Ltd, Persimmon PLC, Telford Homes Ltd and the Vistry Group PLC to explore these additional standards and is now seeking views from the wider industry.

A Department for Levelling UP, Housing and Communities (DLUHC) spokesperson says: “As per our commitment in the Levelling Up White Paper, essential checks to verify identity should be as streamlined as possible so home buyers and sellers do not have to go through the process repeatedly, with all the delays and extra costs this can incur.

“We are pleased to see the sector is building on the identity trust framework to make the verification process more straightforward and less frustrating for consumers.’”

A HBF spokesperson says: “Homebuilders are committed to continually improving the experience of customers and this scheme is a further demonstration of this.

“As well as simplifying the identity verification process, the scheme supports homebuilders to comply with government requirements and reduce duplication of effort so our members can focus on building much needed homes.”

The MyIdentity.org.uk® scheme needs to ensure that that it can represent the views of all new home builders. If you would like to contribute and help influence the scheme requirements fill out the online survey by the 30th January 2023.

Fintech in Scotland – Connect, Collaborate, and Cultivate

Over the last few weeks, the FinTech Scotland team has had the pleasure of working with an intern from Portobello High School as part of a Career Ready programme. It provided us with an opportunity to support a young person think about the future of work, but more importantly it helped us see through a young learner’s eyes, the excitement and curiosity fintech generates. The power of those questions from a someone with no industry baggage or background yet, is striking.

His facial expressions and questions ranged from sheer surprise to genuine delight, and with a work focus on planning the FinTech Scotland Festival we were delighted to have another set of eyes, ears and thoughts help develop the plan.

Our new young colleague summarised his experience under four key themes. In his view FinTech enables communication, connection, and collaboration, and together these are helping to cultivate the future of finance. As we look towards the FinTech Scotland Festival these themes really set the tone.

The FinTech Scotland Festival

This year We will connect and reconnect with new and old colleagues across the UK and across the world. We will share, listen, learn and have the privilege of some key messages, communicating on the journey so far and the ambition for more.

We’ll celebrate the growing strength of the fintech community in Scotland, and the brilliant entrepreneurs cultivating the future of finance and achieving record levels of investment.

Across the festival we’ll hear more about their plans and ambitions including Snugg’s plans to enable us all to make our homes more energy efficient through fintech, DirectID’s global growth in helping people get fairer access to necessary lending, and Legado’s continued focus to help us get all of our financial lives more digitally organised as we move away from paper-based experiences to digital ones.

We’ll also see Know-it who are gearing up to help businesses manage credit, and Waracle who are helping so many larger Enterprises embrace the possibility of doing business through mobile. Amiqus, will share plans on driving fairer access to better services for people, while Float will show the future of financial management for businesses through a business unique financial command centre. The list goes on and we’re proud to show the advances and flourishing potential.

We’ll also explore emerging fintech innovations, be curious about next generation finance and discover the art of the possible as we collaborate across FinTech and Space innovation to help the climate agenda.

The Festival lift off is on the 15th of September with the FinTech Summit. As ever this event and the Digit team set the scene, tone and ambition for the following three weeks where we will explore the world of fintech. We will land on the 6th of October to celebrate the journey with the Scottish Financial Technology Awards.

I’m really looking forward to it all, meeting people, learning, sharing experience and celebrating success.

And a final note of thanks to Jack, our new intern colleague. While Jack will return to school in the next few weeks, he has left an lasting impression that we’ll not forget.

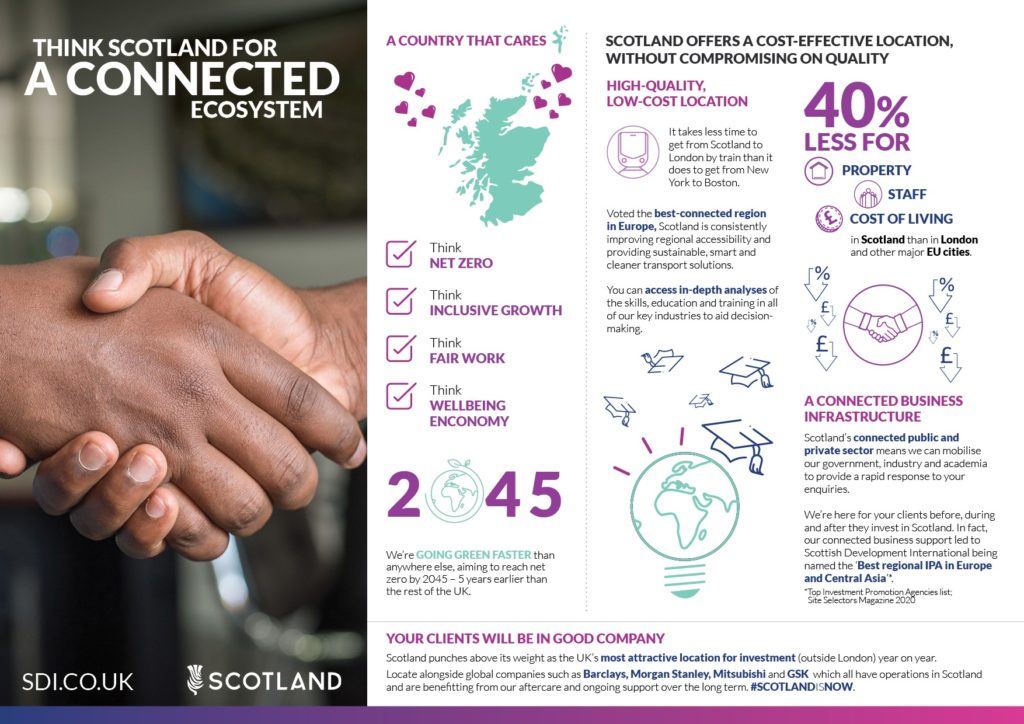

Fintech driving Scotland’s inward investment success

By Kevin Reynolds, Inward Investment Specialist at Scottish Development International

It has been an excellent past month or so for inward investment in Scotland.

As Scottish Government Business Minister Ivan McKee announced at the World Forum for FDI in Edinburgh in May, Scottish Development International (SDI) statistics revealed that more than 7,500 planned real living wage jobs had been generated by inward investment in FY21/22.

The figures showed that 113 investment projects were supported by SDI, Scottish Enterprise and its partner agencies Highlands and Islands Enterprise, South of Scotland Enterprise and Skills Development Scotland in the past financial year, 39 of which were investors locating in Scotland for the first time.

These excellent results were reinforced by the publication of EY’s latest Annual Attractiveness Survey, which confirmed that Scotland was again the most attractive location for inward investment in the UK outside of London.

EY’s figures showed that Scotland secured 14% more Foreign Direct Investment (FDI) projects in 2021 compared with 2020. This helped ensure that Scotland’s investment destination attractiveness was now at record levels.

EY’s figures showed that Scotland secured 14% more Foreign Direct Investment (FDI) projects in 2021 compared with 2020. This helped ensure that Scotland’s investment destination attractiveness was now at record levels.

And earlier this week, a new Department for International Trade report showed a substantial increase in both the number of projects and jobs created in Scotland due to inward investment in FY21/22, compared to the previous financial year.

So, these reports showed Scotland’s continued ability to attract inward investment is clear, with the country’s software, IT and digital sectors central to this success.

SDI’s results showed that one of the most predominant sectors for inward investment was Software and IT, while EY’s figures revealed that Digital projects in Scotland rose by 73.6% in 2021 compared to 2020.

In the past financial year, SDI supported many fintech firms choose Scotland for global growth. For example, Hong Kong cyber security company PolyDigi Tech continued to expand its presence in Edinburgh. PolyDigi Tech has been involved in several programmes designed to support innovative start-ups, including EIE (Engage Invest Exploit), and was chosen as one of the Rising Stars 4.0 Scotland regional winners, an early-stage tech scaleup competition organised by Tech Nation.

And the good news keeps coming. In May, Embark announced plans to hire more than 50 people in Dundee over the next few months as it continues to develop its presence in the city.

Meanwhile, digital finance company ClearScore recently announced that it intends to create an Open Banking Centre of Excellence in Edinburgh, creating up to 100 jobs over the next few years. SDI has been pleased to engage with both companies regarding their plans for growth in Scotland.

Looking ahead, our dedicated specialists based here and in more than 30 locations around the world – alongside our prestigious international networks such as GlobalScot – will continue to promote Scotland as a perfect place for companies to locate.

Using the Scottish Government’s Inward Investment Plan as our North Star, we will focus our activities on delivering projects in opportunity areas where Scotland is a genuine world leader. One of these sectors is undoubtedly Digital Financial Services.

Scottish Enterprise has developed a national programme on the digital economy, demonstrating our own commitment to digital scale-up. Scottish Enterprise also provides investment to the wider tech sector. For example, Scottish Enterprise last year invested more than £30m into companies in the sector via our co-investment funds, investing alongside local, national and international investors from seed through to series A and beyond.

But we know this will be a partnership effort. Our Team Scotland’ approach, which sees public bodies, academia and industry working together to promote the very best Scotland has to offer, makes us stand out from the crowd. Businesses have told us that this joined-up approach is a key reason why they choose Scotland.

But we know this will be a partnership effort. Our Team Scotland’ approach, which sees public bodies, academia and industry working together to promote the very best Scotland has to offer, makes us stand out from the crowd. Businesses have told us that this joined-up approach is a key reason why they choose Scotland.

For example, both Scottish Enterprise and the Scottish Government have endorsed FinTech Scotland’s recently published ten-year Research & Innovation roadmap, which outlines a bold and ambitious commitment to fintech innovation in Scotland, playing on our key strengths in regulation, payments, climate finance, etc.

By bringing together start-ups, entrepreneurs, businesses and universities, we can create, co-develop and share knowledge, leading to more innovation that will help unlock Scotland’s economic potential.

Scotland’s financial services sector is rightly regarded as one of the leading finance centres in Europe. Our universities are world-renowned and the innovative technology scene in our towns and cities is second to none. When you combine these factors with our skilled workforce, Scotland is an irresistible proposition for fintech growth and development.

Scottish Enterprise is fully focused on transforming Scotland’s economy, as well as our journey towards a net zero future. Crucial to achieving this will be innovative sectors such as fintech. We look forward to continuing to work with partners across the public and private sectors, including FinTech Scotland, to ensure all our communities and regions benefit from the economic opportunities arising from fintech.