FinTech Research & Innovation for Climate Finance

The impact of climate change across the world is disrupting national economies and affecting lives. It requires urgent action from all to address the growing issue.

In its 2020 Global Risks report, the World Economic Forum highlights that the risk signals show the horizon for addressing climate risks has shortened. For the first time in the history of the report, the top five risks that it outlines are in a single category: climate environmental change’

In the Research & Innovation Roadmap, we use the term Climate Finance to describe the role that finance, technology and data can play in addressing the climate change crisis and powering a sustainable future.

The importance of Climate Finance

Enabling a more sustainable future was a prominent theme throughout the research for the development of the Roadmap. Throughout our analysis, the influence of finance together with the potential for exponential change through technologies was thought to be a powerful combination to help the necessary transition to a carbon neutral economy.

In the UK, financial regulators are aiming to influence positive climate outcomes through a series

of new expectations, rules and guidance. The Bank of England is working to encourage an early and orderly transition to a carbon neutral economy and to “play a leading role, through policies and operations, in ensuring the financial system, the macroeconomy, and the Bank are resilient to the risks from climate change and supportive of the transition to a net zero economy.”

The Financial Conduct Authority also has a sustainable finance strategy, aiming to build greater transparency and trust, developing guidance and tools to provide mutual support to address the challenges of climate change.

Climate Finance is a complex matter. Our research with FinTech Scotland showed that it connects many things, including:

- Investment

- Regulatory change

- Better data

- Advanced analytics

- A deeper understanding of consumer behaviours and consumer engagement

- A deeper understanding of new technologies, biodiversity, carbon, and carbon markets

The challenge ahead is huge. Nevertheless, the research behind the Roadmap pinpointed three priority areas where further FinTech research and innovation could advance progress by helping nations adapt to the impact of climate change, manage the risks of transition and lead to them becoming greener, more resilient and more inclusive. All three offer Scotland and the UK an opportunity to use strengths in research and innovation, and to build collaborative action across the FinTech and finance industry and the research community.

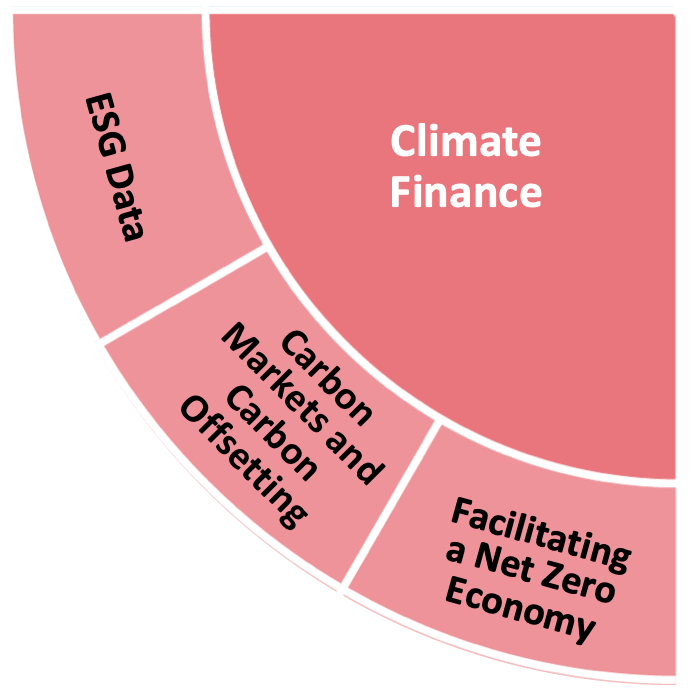

Priority areas in Climate Finance

Environment, Social, Corporate Governance (ESG) data.

Assessing the current situation and outlining the ambition for new data sources, clearer standards and advanced analytics to build greater trust and transparency in the sustainable claims made by finance and business.

- ESG reporting

- Investor confidence

- ESG data

- SME market

Carbon markets and carbon offsetting

Considering the role that each plays in realistically transitioning to a net zero low-carbon economy while exploring the technologies and innovation that could drive further progress.

- Voluntary carbon markets

- Carbon offsetting

Facilitating a net zero economy

Moving beyond finance-as-usual practices. Using innovation and technology to reinvent financial markets and stimulate the change needed to support a healthier planet.

- Investment decisions for net zero

- Circular economy

- Housing

- Insurance

- SME market

Roadmap next steps: Climate Finance

A range of proposed next steps are laid out in the published Roadmap, which specifically identifies 8 actions relating to Climate Finance, and categorises each into one of three phases over the next 10 years. These actions are illustrated in the graphic below. the report also references 25 different stakeholders who can support the implementation of these actions, which are broken down into research projects and innovation calls.

More information about FinTech Scotland’s Research & Innovation Roadmap can be found here, where the full Roadmap can also be downloaded.

Research & Innovation opportunity in Open Finance data

Article written by Julian Wells, Director at Whitecap Consulting

FinTech Scotland recently published its 10 year Research & Innovation Roadmap. Whitecap worked in partnership with the FinTech Scotland team to support the development of this roadmap, and is discussing the key outputs in a series of blogs. This blog focuses on Open Finance data, which is one of the four key strategic priority themes.

In the first blog in this series, we discussed the purpose, value and impact of a Research & Innovation Roadmap. In this blog, we discuss Open Finance data which is a strategic priority itself but also a facilitator of FinTech innovation in wider areas, and an enabler for the three other strategic priority themes in the Roadmap.

The other three themes are Climate Finance, Payments & Transactions, and Financial Regulation, each of which will be the subject of a subsequent blog in this series.

Open Finance data has the potential to significantly change consumers’ and businesses’ engagement with finance, and to deliver better outcomes. It spans the whole suite of financial products and services as we understand them today, including banking, savings, mortgages, pensions, investments, insurance, lending, and payments.

How can Research & Innovation support the development of Open Finance?

To help Open Finance achieve its potential, more leadership, actionable research, and innovation is required. FinTech Scotland’s Research & Innovation Roadmap sets out specific actions to help drive this opportunity ”“ through a collective approach that involves industry, innovators and researchers ”“ to create the future of finance.

Open Finance can create progressive change that will move the UK forward significantly, by moving beyond banking and asking other financial institutions (such as pension providers, asset managers and insurers) to enable customers to share their data with others.

This would open up a wider range of financial products and services to the transformative impact of third-party innovation through trusted data sharing. For consumers and businesses, it offers new ways to understand their finances, receive financial advice, and compare financial product features and prices.

Research and innovation are needed to facilitate the potential of Open Finance data, building economic growth and creating employment opportunities in high value sectors which in turn will make the UK an attractive destination for inward investment.

Furthermore, it will help us better understand, measure, and forecast the considerable impact that Open Finance could have on society and to shape future policy.

In the UK, one of the key enablers of research and innovation in Open Finance is the Smart Data Foundry (formerly The Global Open Finance Centre of Excellence), which has been established in Edinburgh to support the understanding and development of the capabilities of Open Finance. It has a leadership role in enabling the necessary research and innovation, and building confidence in Open Finance across the UK, and can encourage research and innovation by providing a highly secure environment that can host Open Finance data. The Open Finance data priority in FinTech Scotland’s Research & Innovation Roadmap supports and complements The Smart Data Foundry’s agenda.

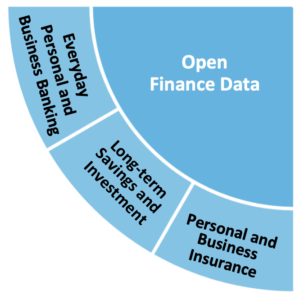

Priority areas in Open Finance data

When developing the Roadmap, analysis highlighted three industry priorities that will benefit from more focused research and innovation on this topic. They involve shaping the future of:

Everyday personal banking and business banking

- Insights through Open Banking data

- Future banking business models

Long-term savings and investment

- Financial resilience and wellbeing

- Future living & the ageing population

Personal and business insurance

- New data and insights for insurance

- Data privacy

- Data ethics and governance

Roadmap next steps: Open Finance data

A range of proposed next steps are laid out in the published report, which specifically identifies 22 actions relating to Open Finance, and categorises each into one of three phases over the next 10 years. These actions are illustrated in the graphic below. the report also references 23 different stakeholders who can support the implementation of these actions, which are broken down into research projects and innovation calls.

Why should tech companies care about double fetch vulnerabilities?

Fintech companies are facing an increasing need to focus on cybersecurity. Whilst cyber-attacks are on the rise and necessitate the constant evolution of cyber-security solutions, very often the issues arise from known vulnerabilities within existing systems.

In this blog we’re exploring double fetch vulnerabilities.

The phrase ‘double fetch bug’ was first used by Fermin J. Serna in a post on the Microsoft Security and Defense Blog in October 2008, although the bug type had been known about for some time before this.

Double fetch vulnerabilities in C and C++ have been known about for a number of years. However, they can appear in multiple forms and can have varying outcomes.

As much of this information is spread across various sources, the whitepaper, draws the knowledge together into a single place, in order to better describe the different types of the vulnerability, how each type occurs, and the appropriate fixes.

There are two broad general types of double fetch vulnerability: those resulting from coding practices and those introduced by compiler optimization, referred to as a ‘compiler introduced double fetch’ below and in the whitepaper.

The two types of double fetch bug both have the same result, whereby an invariant exists involving two or more variables and one or more of these variables is modified without the invariant being enforced.

Since double fetch bugs can have varying causes, we must consider different solutions for the two different subtypes of double fetch.

- Double fetch bugs caused from accessing shared memory may be fixed by adding a check against the second fetch, eliminating the second fetch (where practical), or performing the check in a different manner.

- For compiler-introduced double fetches, the use of volatile variables is one possible solution to the double fetch problem.

In conclusion, double fetch bugs can result in privilege escalation vulnerabilities that can allow an attacker with a low privilege account to execute code with elevated privileges, although the exploitable vulnerabilities are a relatively small subset of these bugs.

To understand how to best protect yourself against these vulnerabilities, click here to access the full whitepaper from NCC.

Why is the FinTech Research & Innovation Roadmap so important?

Article written by Julian Wells, Director at Whitecap Consulting

FinTech Scotland, the cluster management body, recently published its 10 year Research & Innovation Roadmap. Whitecap worked in partnership with the FinTech Scotland team to support the development of this roadmap, and in the first in a series of blogs we discuss the fundamentals behind this important document.

FinTech is driving change in one of the most important parts of our economy. It presents a significant disruptive force in financial services, and will shape the future of the digital economy. It has the potential to radically change the way people and businesses engage with money, and to create a new financial system that is more effective and resilient.

FinTech Scotland’s Research & Innovation Roadmap is a 10 year plan which has been developed as an industry-led and action-focused tool to increase the positive impact of FinTech innovation across Scotland and the UK. It creates a framework and an environment to drive greater collaboration, and to build the connections that will enable responsible innovation for the future of finance.

The roadmap builds on foundations that were already established through the FinTech Scotland cluster, and sets out the cross-sectoral strategic priorities that ”“ through collective and collaborative action ”“ will shape the future of financial services, and enable Scotland and the UK to further advance FinTech innovation. It was published on the anniversary of the HM Treasury commissioned Review of Fintech led by Ron Kalifa OBE which set out a number of recommendations, including the opportunity for research and innovation to accelerate the development of cluster excellence.

Why do we need a Research & Innovation Roadmap for FinTech?

The financial services industry contributes £132 billion to the UK economy ”“ almost 7% of total economic output. It is an essential part of the full UK economy that enables prosperous outcomes for businesses and people across the UK. Its significance was highlighted by the Chancellor of the Exchequer in the recent HM Treasury report A new chapter for Financial Services’. Working with others across the economy, his vision is for “an agile and dynamic approach, one which enables those in the financial services industry to evolve and thrive as they embrace the new opportunities of the future.”

Research and innovation play a key role in the vision for the future of financial services in the UK and beyond. However, financial services and FinTech have, compared to other industries, generally not been aligned with the academic research communities. Recent analysis highlighted that research funding into these fields is as low as 3% of total UK funding1 for research and innovation.

In addition, there is a general acknowledgement in financial services, FinTech, and the academic community that current engagement has had a relatively narrow focus. The result is limited exploration of research and innovation, which means an important part of the economy is not fulfilling its full potential.

There is an opportunity to close the gap between the economic productivity of UK financial services and the current scale of UKRI investment in FinTech and financial services R&I. This can be achieved via more strategic and systematic collaboration, which can help develop the necessary FinTech innovation between the range of stakeholders. Importantly, this should be driven by a true desire for effective change, and by an industry-first real-world’ approach to the challenges ahead.

This work also supports the strategic HM Treasury Review of UK Fintech led by Ron Kalifa OBE. It recognises the value of collaboration, and the leadership that is needed to create the right conditions for FinTech to innovate, accelerate and grow.

How will the Roadmap be implemented?

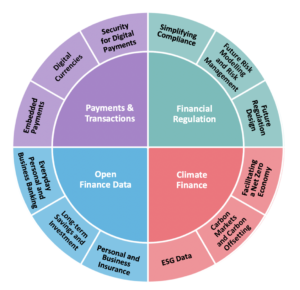

The priority themes form the building blocks of the Roadmap are: Open Finance data, Climate Finance, Payments and transactions, and Financial regulation. In subsequent blogs in this series we will focus on each of these four themes individually.

The roadmap will be led and facilitated by FinTech Scotland. However, wider stakeholder participation is required to implement the R&I actions set out in this Roadmap.

Actions will be progressed through two key types of activity:

Unleashing Innovation: A series of Open Innovation Calls, using technologies and data to develop new and improved financial products and models.

A rollout plan will be developed to implement a programme of innovation calls. This will include developing a sponsorship proposition to maintain the commitment for an industry-led programme.

The initial steps for the Roadmap innovation calls include:

- Work with the Smart Data Foundry to start the implementation of the priority innovation calls identified in the Roadmap.

- Continue the work with industry stakeholders to refine a series of problem statements for each theme, ensuring industry value in the future solutions.

- Market the innovation calls across UK and international FinTech clusters, raising the profile of FinTech innovation in Scotland.

Actionable Research: Research, using technologies and data to create actionable insights that can be applied commercially using FinTech.

FinTech Scotland will engage with academic community in respect of the research topics proposed. FinTech Scotland will also engage with research funding organisations such as UKRI / Innovate UK to ensure this roadmap is fed into future funding calls.

The initial steps for research topic actions include:

- Work with university leaders to generate research briefs that directly respond to the actions identified in the roadmap.

- Establish relevant steering groups demonstrating collaboration across industry and the research community.

- Monitor and review progression (including a KPI scorecard).

Twice a year, the FinTech Scotland Cluster Management Board will measure and review the Roadmap’s progress of the Roadmap. This will be reported publicly to stakeholders in Scotland and the UK.

What will the impact of the Roadmap be?

In this blog we have outlined the requirement and benefits to bringing industry-led approach to research and innovation, but describing the impact the Roadmap can have on the Scottish and UK economy is perhaps the most compelling way to explain why this is such a vital document.

The overarching economic ambition for the Roadmap is to do two things:

- Create up to 30,000 extra jobs in Scotland.

- Increase economic value (GVA) by more than 330% ”“ from £598 million to more than £2 billion ”“ over ten years.

Taking a broader perspective, the impact of the Roadmap will be:

- To tangibly help improve lives for citizens, by tackling inclusion and health- related issues.

- To further develop Scotland as part of the UK in being a global engine room’ for FinTech and a desirable location for international FinTech companies.

- To drive innovation, supported by a world-leading reputation in regulation and compliance.

- To use Scotland’s and the UK’s natural strengths, making them a global enabler of greener’ FinTech.

A blueprint for the future

FinTech Scotland’s Research & Innovation Roadmap outlines actionable research and innovation activities that can help develop economic, environmental, and societal value for Scotland and the UK through FinTech. Successful implementation will require the engagement and co-operation of key stakeholders within the FinTech Scotland cluster, and stakeholders from across the UK and internationally. The Roadmap is the first of its kind in the UK, but the aspiration is that it has created a framework that other countries, regions or indeed FinTech sectors can learn from and adapt.

More information about FinTech Scotland’s Research & Innovation Roadmap can be found here, where the full Roadmap can also be downloaded.

FinTech research and Innovation ”“ the future of finance

This month we published our FinTech Research and Innovation Roadmap. We know more research and innovation in financial services and fintech will set us on a course to shape the future of finance.

It’s been in the works over recent months, and it’s allowed us an opportunity to hear industry, consumer academic, and innovators views on what the future of finance and fintech could be. Leading the way!

It’s a genuine privilege to hear the ambition and determination across the fintech and finance industry for a future that means less friction in financial services, enables more inclusion using technology and data, and drives climate change enabling greener investments.

The tone from all was clear, fintech will drive better financial outcomes for people, businesses, our society, and the environment. The desire for change and energy for innovation and collaboration is truly inspiring.

The report gives us a framework for focused collaboration. It identifies 4 priority themes and outlines the primary actions that will enable us all to learn, advance, and most importantly, build the right collaborations to drive and lead future fintech innovation. It was published during the first anniversary of the Kalifa review of UK Fintech where more R&D was a specific recommendation.

The first of those priority themes in Open Finance Data ”“ already an area of strength in Scotland! FinTech businesses such as DirectID, Visible Capital, Inbest, AirFunders, and One Bank all use Open Finance Data in their businesses. This experience along with the investment in the Global Open Finance Centre of Excellence, now known as the Smart Data Foundry sets us on a course to explore how Open Finance Data can change the way we do finance in the UK and across the world.

Climate Finance is another key priority ”“ a growing area of strength and focus for Scotland. FinTech businesses such as Snugg, Coastr, Pulse, Iceni Earth, Trade in Space, and Space Intelligence are all focused on using data and technology to help people and businesses make the changes needed to achieve change in the interests of the planet. These businesses are enabling a different future. The same can be said for the research community in Scotland with centres such as The Centre for Sustainable Developmentand the Edinburgh Climate Change Institute leading research and providing deeper and focused insights on climate impact. From this place of understanding more will change.

Payments and transactions’, as well as Financial Regulation’ complete the 4 priority themes. Again, both assets for Scotland, where the depth of fintech innovation, skills and expertise stand Scotland’s FinTech Cluster in great stead. More on both these themes in the coming weeks and months.

For now, we’re gearing up for UK FinTech next week. There’s a host of events in plan where we’ll have an opportunity to share the wonderful work happening across FinTech Scotland.

I’m signing off with a note of thanks and a special note of thanks to everyone who contributed to the FinTech Research and Innovation Roadmap.

The Roadmap is a true demonstration of Scotland’s FinTech Cluster at its best. It highlights the breadth of contribution to the cluster that allows us to learn, collaborate and inspire each other for development and growth. It shows how our commitment to action for positive change, and it is ambitious, challenging us to think ten years ahead so we can lead the future of finance.

I’m looking forward to seeing this advance and working with the inspiring leaders, innovators, entrepreneurs, and educators as we build and teach the future!

Thank you

Nicola

How Scotland’s Fintechs plays a role in saving people and planet

The most recent IPCC report has shown us how much we need to change to keep the warming of our planet below 1.5º. Climate change is no longer in the future – it is now. Heatwaves, droughts and floods are already exceeding plants’ and animals’ tolerance levels and with 80% of people in the UK being concerned about the warming climate, the appetite for making changes that positively impact our futures is there.

All eyes have been on Scotland since COP26 was held in Glasgow last year, and the coverage and the attention made it clear that Scotland must do more to become a climate and social leader. While there have been changes it is clear that they are too incremental, that a radical overhaul is not yet here. The will for change is there though ”“ especially amongst Scottish people.

Scotland has a reputation as being socially and environmentally progressive ”“ they are ahead of the rest of the UK in the legally binding target to hit net zero, co2 emissions are already half of what they were 30 years ago. At the start of 2020, Scotland was already creating enough renewable energy to account for 97% of total gross energy use in the country. Socially, also, Scotland is setting an example ”“ with free university education, fantastic baby boxes for every newborn and the new young carer’s grant.

Scottish Fintech has been a fast-growing industry since the beginning of the pandemic; there were 119 in March 2020, and there are now almost 200. With the analysis of our cluster as being positive and vibrant’ in the Kalifa review, along with the fantastic collaboration between small and large companies in the Fintech sectors in Scotland, it is no wonder that Scotland has become a hub and a leader in the industry. This brings with it the responsibility to build environmental and social governance (ESG) into our organisations ”“ this is much easier than trying to retrofit later on.

Some Scottish Fintech organisations that are working to be changemakers in society include Iceni Earth (The Experian of Nature) – which help landowners assess their land and give them a biodiversity score, along with clear instructions on how to improve this score. A lot of Scottish Fintech is also focused on social inclusion, with HI55 helping people get access to their pay more frequently and when required. Inbest is using data capture and analysis for good, helping people who are entitled to benefits receiving them. These are just a few examples of fintech organisations that are using their skills to bring benefit to people and the environment, as well as helping people feel empowered to impact the biodiversity of their land, or simply their personal finances.

Fintech has the opportunity to help customers take control of aspects of their lives, using data to see and control their finances and investments. This has been shown to be vital in keeping eco-anxiety (the chronic fear of environmental cataclysm) at bay. This is vital if we are to keep activated, moving forward and not frozen in fear. With all eyes on Scotland, the time to prove they are the social and climate leaders we know they can be is now.

However, there is still plenty of work to be done and the changes that have been made so far could be described as modest. While it is possible to hit net-zero targets, it has been recognised that this will take a radical change in every part of Scottish lives and businesses. But there is the drive to make that change ”“ Scotland has a socially responsible culture, environmentally thoughtful perhaps because of the strong connection to the fantastic landscape.

Gihan Hyde is the award-winning communication specialist and founder of CommUnique, an ESG communication start-up.

She has been implementing ESG campaigns in eight sectors, across six countries over the past 20 years.

Her campaigns have positively impacted over 150,000 employees and 200,000 customers and have closed over £300m in investment deals. Some of the clients she has advised include The World Health Organisation (WHO), HSBC, Barclays, M&S, SUEZ, Grundfos, Philip Morris, USAID, and the Saudi Government.

Get in touch with Gihan through LinkedIn or Twitter @gehanam.

Interview with a fintech that pitched in the Den

Following her appearance on Dragons’ Den, Fintech Scotland member Sheila Hogan, founder and CEO of digital legacy vault, Biscuit Tin, shares her experience of her time in the Den and what it was like pitching to such a high profile and successful group of entrepreneurs

Sheila, well done for your appearance on Dragons’ Den. Can you tell us what drove you to apply for the show?

I had originally applied to take part in Dragons’ Den in 2020 and was approached about being in the show in 2021. The process for getting in front of the Dragons is a lengthy one, involving an application, video pitch and interviews with a researcher who then presents your case to the executive team. Just getting to be on the show felt like an enormous achievement.

I applied for the show because I wanted to propel awareness of Biscuit Tin, it’s purpose and mission to a global audience, whilst hopefully securing investment from one of the Dragons’. I had my hopes pinned on Deborah Meaden. Given her own personal experience I knew Biscuit Tin would resonate, and she holds a strong belief in businesses with purpose and as a force for good. I knew getting on Dragons’ Den would be the chance of a lifetime and would help me to achieve my vision of establishing Biscuit Tin as a leading global household brand for end-of-life planning and digital legacy within the next five years.

Despite a great pitch, you didn’t manage to get a dragon on board. What do you feel was the main reason?

At the time of filming, I was a pre-revenue tech company with a business profile that simply did not align with the Dragons’ individual investment strategies.

Is pitching in the den very different from pitching anywhere else?

Knowing my pitch was going to be aired to potentially millions of people on prime-time TV, meant that my Dragons’ Den experience was always going to be quite unlike any other pitch or speaking engagement that I’d ever had to do over my forty-year career in IT, change and project management. And so, it proved to be. Stepping out of the lift and into the studio where the Dragons were sat was one of the most nerve-wracking, but exhilarating times of my life. In the Den, there was an intensity to my pitch that I’d not experienced before. Knowing the pitch could be edited in any way the producers chose, which I had no control over, meant that I was more nervous on the night the episode aired than I was before the pitch! The one thing it did have in common with pitching to others, is that with any set of potential investors the key thing is to make a meaningful connection with them. In the Den I knew I had to give the performance a lifetime and I did everything within my control to be ready and prepared for filming on the day.

What learnings do you take away from your appearance on the BBC show? Would you do it again?

I would absolutely do it again. I wouldn’t want to miss such a golden opportunity. On my journey to the Den, I learnt so much. All the preparation was invaluable and has stood me in good stead for pitches to other investors. Since filming I have secured £330,000 investment from Velocity Capital, Scottish Enterprise, and a private investor. In fact, some of the feedback I received from the Dragons’ made me even more determined to succeed!

Whilst no money came from the dragons, you recently announced a successful £330,000 raise. What did you investors see that the dragons didn’t?

The investors we pitched to were specialist tech investors, who understand the financial profiles of tech startups. They saw the potential of Biscuit Tin and were not phased by the losses we experienced in the first couple of years of the business, as this is standard for a tech start-up. Biscuit Tin was simply better aligned to their experience and strategies.

What will this fresh investment allow you to do?

This investment will allow the business to gain significant traction through key hires and product development. I am more than equipped and determined to take the business to the next level. We are moving ever closer to achieving my dream of making Biscuit Tin a global household brand, to live in a world where planning for end of life is the norm, and where we all have virtual’ biscuit tins containing digital legacies to hand down the generations.

What are the next big milestones for Biscuit Tin?

The next big milestones are to engage with as many users as possible, coupled with valuable partnerships, so we can empower as many people as possible to get organised. We will be working to develop Biscuit Tin further, to provide product features that reflect the needs of our customers.

I am delighted to have been selected as part of the cohort of Scotland’s top twenty up and coming tech companies travelling to Silicon Valley with StartUp Grind in April. Funded by the Scottish Tech Ecosystem Fund, the trip will bring together Scotland’s top startups and scale ups with more than 3,000 of the world’s best.

Combatting CEOs cyber security concerns

By Fraser Wilson, Head of Financial Services at PwC Scotland and Colin Slater, Cyber Security Partner and Scotland Risk Leader.

For businesses with digital adoption high on their agenda, the arrival of the pandemic was undoubtedly a catalyst moment. Customers moved online in their droves benefitting subscription services from Spotify to Peloton. Retailers moved rapidly to refocus their operations to the web, and customer service channels and face to face’ services via video consultations, from high street banks to doctors surgeries, suddenly became normalised.

Scotland has a world leading FinTech ecosystem which has a key role in driving the innovations that allow businesses to transform customer experiences and adapt to a changing environment. However, the rapid pace of change has left many businesses feeling exposed to new risks.

Nearly two thirds (64%) of respondents to PwC’s 25th Annual CEO Survey said that they have significant concerns about cyber threats. In the UK, this outranked health risks, macroeconomic volatility and climate change as the threat to their business that CEOs are most concerned about, further cementing its elevation in business conscience.

And CEOs are right to worry. It’s an accepted fact that it’s not if but when a cyber attack will occur. CEOs’ main concern is around a catastrophic incident stunting business growth. As shown by the myriad of Ransomware cases, a successful cyber attack delivers more complex existential problems to solve. Associated issues we see, like not being able to pay salaries, deal with supply chains, place orders or give regulators the information they need; suddenly become pressing if you are in the midst of recovering your whole business.

Risk is a fundamental part of business. Companies are well practised at both mitigating risks and using them to take calculated business steps. Fintechs, in particular, have a role in both the defensive as well as proactive use of risk management. Being a good cyber citizen can be a huge market differentiator and demonstrating a good cyber posture and structure can also be hugely beneficial in any investment or deal situation. Being cyber aware and building a secure business are the foundational aspects for any fintech and will ultimately protect the valuable IP assets they are creating. While CEOs are right to be concerned, having an organisational approach to think cyber’ across all strategic and tactical decisions is key to success. Putting the right structures in place now ultimately will pay dividends in the market later.

Our recent announcement that we’re strengthening our financial services team in Scotland is part of our commitment to helping businesses embrace technology and improve resilience and agility. With our cyber security hub in Scotland we are expanding and delivering services around the world as well as on our doorstep. Our Managed Operations Centre of Excellence is located in Edinburgh, alongside our Threat Intelligence team, so our local footprint is something we are rightly proud of. We’re determined to help CEOs tackle their cyber concerns head on and drive the Fintech agenda in Scotland.

Increasing industry use of encrypted email to combat cybercrime

Recognition amongst financial services businesses of the need to safeguard emails is increasing in the face of financial cybercrime and they are taking action. Origo’s Unipass Mailock recently marked its one millionth email sent though the encrypted system.

Industry providers such as Aegon and Royal London are using military-grade encryption email services to protect their email exchanges with financial advice firms, and other providers are also realising email protection is now essential.

Cyber criminals hack vulnerable email systems and employ sniffer programs which identify valuable emails and take copies of them, which the criminals can then exploit. For example, in just one email in which a client sends their personal and asset details to their financial adviser, there would be enough detail to help criminals commit fraud.

Putting in place a secure, military-grade encrypted email system, one which protects emails in transit, and ensures that only the intended recipient can access the email, as well as providing an audit trail for compliance purposes, now needs to be thought of as base-level security for product providers and financial advice firms, and without a doubt where confidential and transactional data is being sent.

It is also another way for providers and firms to demonstrate value to their respective customers in the precautions they are taking to safeguard their data.

Origo’s Unipass Mailock system has now surpassed one million emails through the system. Looking at industry benefits, not only has this protected over a million communications between providers, advisers and their clients, but we calculate that this equates to £1.9m saved in print, packaging and postage costs, as well as climate related savings of 459 tonnes of CO2 and 154,000 tonnes of water.

The risk to businesses is not just potentially having to compensate clients for losses, and meeting fines imposed by the Information Commissioner’s Office (ICO), but the effect on client trust and the reputation of the business.

As we move to a more digital advice experience, we expect to see companies of all sizes look to protect this potential point of vulnerability and employ encrypted email as a matter of course.

Standard security protocols advice firms can follow

Some general basic actions businesses can take to help protect their businesses against cybercrime, include:

- Having in place standard items of internet hygiene including firewalls, anti-virus software and a virtual private network (VPN) for off-site working.

- Identifying where the risks to the business lie ”“ are they with providers or are they in unsecured communications with the end client?

- Implementing formal processes and procedures, and staff training, to raise awareness of the potential dangers, and how to protect the business against them.

- Having formal cybercrime processes written into a firm’s policy documents, including written instructions for staff to follow where, for example, fraud is detected.

- Having in place appropriate controls for inward and outward communications ”“ such as encrypted email.

- Letting your customers know the potential dangers and what you are doing to protect them.

Photo by Markus Spiske from Pexels

Why Origo is supporting the Research and Innovation Roadmap

Origo has been delivering technology solutions for the UK financial services market for over 30 years. We are proud of that history and also proud to be an Edinburgh-based company, contributing to the economies of both Scotland and the UK.

“With the technological innovations happening in the world today, and the opportunities they offer, this is probably the most exciting time in our history.

“Open Finance Data, which is one of the four themes of the Roadmap ”“ the others are climate finance; payments and transactions; and financial regulation ”“ is one example of the innovation taking place in financial services. Amongst other things, it will enable people and businesses to have more control over their finances by making it easier for them to access their financial information.

We see the value of this type of access every day at Origo. Our technology enables the industry providers to access pension and investment information and by evolving through Open Finance we can use this capability to enable individuals to directly access their information.

To this end, we are partnered with Capgemini to supply the central digital architecture for the Pensions Dashboards Programme, which will enable pension holders to easily access all their pension details in one place ”“ action that is vital for individuals planning for the future and for retirement.

But technological innovation is not restrained by geographical boundaries, so it is important that UK FinTech continues to innovate and push the boundaries, within the highly regulated environment in which we work.

This is about the future of finance, the way people engage with money, their savings and investments. The FinTech Scotland Research and Innovation Roadmap will help enable industry-led collaboration to provide a practical pathway to accelerate the development of FinTech and open up opportunities across the financial services industry as well as the broader economy in Scotland and the UK.

We are proud to be part of this forward-thinking and practical initiative.