Scotcoin announces the launch of its new ERC20 token

Scotcoin’s new token uses the Ethereum blockchain, the second largest distributed ledger network in the world by market capitalisation after Bitcoin. Adoption and use of the Ethereum blockchain assures that Scotcoin remains a bona fide distributed ledger cryptocurrency whose future sustainability is not in the hands of a few.

Temple Melville, CEO of The Scotcoin Project CIC said:

“I am delighted that we have finally reached this milestone in the evolution of Scotcoin. We have worked hard to meet the condition laid down by our stakeholders and funders that the durability and sustainability of the token would never be in the hands of the few. Use of the Ethereum blockchain assures that that objective is met”.

The Scotcoin Project is a not for profit community interest company that seeks to educate and inform the public on digital currencies and blockchain technology. It occupies the ethical space and is developing a program of initiatives designed to help improve the personal and financial prospects of those with the fewest opportunities afforded by the current economic landscape.

Moving to an ERC20 token means that our coin is basically acceptable on any exchange, and in fact we will be having an IEO (Initial Exchange Offer) over the next year. The move will enable us to engage with nearly everyone who has an interest in digital currencies. As an aside, digital currencies are most definitely now an asset class but are also a hedge against the massive quantitative easing that has taken place world-wiide during the Corvid-19 pandemic. We are already seeing inflation creeping into our daily lives in contrast to the mildly deflationary effect of digital and crypto currencies.

For further information please contact Temple Melville on temple@scotcoinproject.com

Why fintech Hubb Insure chose Glasgow

When we set about building our business one of the first questions we look at was the location, what was important to us?

Hubb firstly was a challenger to the commercial insurance space, built on modern management structures and a technology stack, built around flexibility and efficiency, our objectives where simple, cheaper more efficient solutions for our clients, happier more focused staff.

Homeworking was always going to be a major part of the mix, but we still needed a base for a head office and training, so we landed on London, Manchester or Glasgow.

London- The heart of the global insurance market, great public transport and connections all over the city, very expensive everything!

Manchester- Cheaper than London, two hours on the train from London, local public transport not so great.

Glasgow- Great flight links to London, good public transport, Scottish Enterprise are great to deal with.

When we had these discussions, it became clear that Glasgow was the perfect home for Hubb over and above the obvious, we have sourced local partners and found that the skill sets in sales, marketing and flexible office space in Glasgow a real positive.

DirectID Launch Collections & Recoveries Solution

Scotland based FinTech, DirectID just announced the launch of its Collections & Recoveries solution.

DirectID has built a solution to make the collections process easier and faster in collaboration with the UK’s leading banks, lenders and debt collections agencies,

Using Open Banking data, agents will be able to access accurate customer’s financial statement and an assessment on their disposable income, and how much they can afford to repay.

The new solution combines DirectID’s categorisation engine with the categories defined within the Standard Financial Statement.

For individuals who have built up large amounts of debt, it removes a lot of the stress and uncertainty. The use of bank data negates the need for them to supply lots of details around financial commitments with existing creditors.

Currently, collections agents can spend a large volume of time with a customer assessing how much income they have, and what their discretionary and non-discretionary spend looks like. This process is also prone to customer error, downplay spend, or deliberately mislead, in an attempt to keep repayments low.

DirectID’s product circumvents the often unpleasant collections process from a period of weeks to just minutes.

Collections & Recoveries uses an individual’s bank data to help lenders streamline the collections process. This supplies the lender with an up-to-date and accurate view of an individual’s debt commitments and subsequently their capacity to repay debt.

DirectID’s Collections & Recoveries solution identifies income streams; expenditure; insight into a customer’s profile; including discretionary and non-discretionary; and summarises payments to lenders.

James Varga, CEO of DirectID, said:

“I am immensely proud to be today launching our new Collections & Recoveries solution. This is an extremely important proposition which will help both collections agents and their customers, during which can be a difficult process.

“With the launch of this product, and because of the impact of bank data, DirectID now covers the whole customer lifecycle, from onboarding, portfolio management, and now Collections & Recoveries.

The launch of DirectID’s Collections & Recoveries product marks an important step for DirectID, as we not only launch our first product of this year, but the first of several that we have completed, or are near to completion. Now that we can cover the whole product lifecycle with bank data, we are in a position to work with businesses across industry, and differing needs and challenges.”

Why Scotland should harness its influence in the global fintech industry

Guest blog from Corporate Partner and Technology Lawyer at Addleshaw Goddard, David Anderson

In Scotland, we undoubtedly have one of the strongest fintech clusters in Europe. At the turn of the year, the Scottish fintech sector became the first in the UK, and only the third in Europe, to receive formal accreditation as a cluster of excellence from The European Secretariat for Cluster Analysis (ESCA).

The body looked at 36 economic factors before awarding Scotland this accolade, and our innovative, dynamic and collaborative ethos must, I believe, have had an important role to play in why we received this title.

Looking at growth from 2019 to 2020, the number of fintech SMEs based in Scotland increased by more than 60% from 72 to 119. This notable boost is something that we should continue to celebrate and use as a foundation to build upon to attract even more leading fintechs from across the globe to expand and invest in Scotland.

Most recently, it was announced that our fintech sector will receive a further £22.5 million of funding to establish a Global Open Finance Centre of Excellence (GOFCoE) in the Edinburgh and Central Belt region. Funded by the Strength in Places Fund, this is a remarkable opportunity for Scottish fintechs as the new research and development centre will explore how open banking and financial date can be used to deliver social and economic benefits.

We have world-class talent on our doorstep and as a Corporate Partner and Technology Lawyer at Addleshaw Goddard, I am fortunate to get the opportunity to work with a number of entrepreneurs, CEOs, advisors and customers in the fintech discipline every day.

As a firm, we recognise the importance and wealth of the fintech sector. That’s why in 2017 we launched our dedicated Addleshaw Goddard Elevate programme – a 10-month initiative for selected fintechs designed to accelerate them through legal challenges faced by start-up and fast growing businesses.

Year on year, we are enthused at the calibre of entrants to the programme and to date we have supported 22 fintechs with our expertise across financial services, regulation, IP and corporate and commercial transactions.

Successful applicants to Elevate programme receive advice covering funding, payments, financial regulation, investment and technology at no cost to them as well as ongoing mentoring and access to the firm’s resources. By combining our client-side experience with regulatory and legal expertise, gives us great insight into the concerns and priorities to help fast growing businesses become more productive and even more successful.

In 2019, we welcomed nine businesses to the cohort including Scottish businesses Amiqus , OBR-Open Banking Reporting and Trace, all of which are contributing to and bolstering the tech scene in Scotland. In the next few months, we will be launching the 2020/21 programme and are already looking forward to working with more forward-thinking technology firms with revolutionary ideas.

Whilst this paints an incredibly positive picture of the Scottish fintech sector, which is true, we must remember the Covid-19 cloud that currently hangs over our professional and personal lives. It is a challenging and sometimes worrying time, and the consequences of it will live on long past the ease of lockdown and other restrictions.

The last few months have, however, allowed many Scottish tech firms to adapt and highlight their invaluable contribution to society. I have been extremely encouraged at the response of Scottish technology businesses to the current situation as they adapt themselves or help to aid businesses, people and the economy with their agile approach.

For example, Airts, which uses AI tech to help people at large professional services firms plan projects, has reshaped its working pattern and working from home structure to ensure clients still receive an excellent service.

XDesign ”“ which plans, builds and develops digital products that solve your business challenges – has moved quickly to introduce new processes across the business to succeed throughout this challenging period. This has even resulted in the firm welcoming new clients and staff, which is incredibly encouraging for the industry.

A great local example of this came from Occupyd – which connects businesses to underused workspace ”“ who has used the time to support chefs and caterers access underused commercial kitchen space in closed pubs, cafes, churches and other locations. Occupyd also created a Secret Takeaways’ list which has helped diners in Edinburgh and London find their favourite local restaurant options which are not present on the main apps.

Tech has of course always been important, but through the covid-19 pandemic it is proving to be invaluable as we rely on it to communicate with family, friends, colleagues and in some cases, life-line services. From my perspective, I have seen an acceleration in strategictechnology projects which are driven by improving customer experience and developing the best possible customer proposition.

Looking to the immediate future, nobody can predict to what extent the pandemic will impact the tech ecosystem in Scotland. However, the agile, innovative and inclusive nature of the industry, particularly the fintech ecosystem gives me great confidence that we will come through this with the ability to continue our success and growth, but with new insights and perhaps a refreshed outlook.

Interested technology businesses can register their interest for the 2020/21 AG Elevate programme here.

Scotland is Tomorrow: Developing Responsible Investing in Scotland with rTech?

Scottish Fintech has been a key highlight of Scotland’s modern economic rotation. A more sustainable, inclusive and progressive ecosystem. It is helping to change the shape and face of Scottish e-commerce and finance but has it always been changing it to be more responsible?

Despite the COVID-19 lockdown, the delayed COP26 presents a unique opportunity to reinforce Scotland’s position as a global centre for responsible investing. In doing so Scotland competes with every other country to drive leadership and achieve United Nation Sustainable Development Goals (SDGs). Like Scottish Fintech and the formation of the Scottish National Investment Bank, developing and growing Scotland’s responsible investing landscape is a powerful way to move Scotland’s economy to something more purposeful. The key is collaboration, which stimulates innovation, which encourages inward investment, which produces change in Scotland and overseas.

May 2020 saw the launch of Ethical Finance Hub’s new report, Mapping the Responsible Investing Landscape in Scotland’, which examines the responsible investment market in Scotland, looking at:

- History: the history of responsible investing with a focus on Scotland;

- Ecosystem: the composition of the Scottish responsible investment market, and the linkages between different participants;

- Taxonomy: the terms used by Scottish fund managers to describe their approaches to responsible investment; and

- Market Size: The size of the responsible investing market in Scotland, and how it compares to Ireland and the rest of the UK.

The motivation behind the report was to raise awareness and support the growth of the responsible investing market in Scotland. Having engaged with a number of stakeholders, as well as undertaken internal desk-based research, it was apparent that, whilst data on the sector exists for the UK as a whole, there was little or nothing specific to Scotland available. A link to the report can be found here: https://www.ethicalfinancehub.org/investingscotland2020/.

The report sets out the following call to action:

“Across the globe individuals, organisations and governments are starting to move from talk to collective action as we strive to achieve inclusive economic growth without depleting natural resources. It is now widely recognised that the financial services sector has a fundamental role to play in delivering universally supported targets such as the Paris Agreement and the SDGs. However, despite its potential, the current financial system can be a cause of, rather than a solution to, some of the pressing challenges our planet and its people currently face. In trying to address this predicament Scotland is reflecting on its heritage and seeking to emerge as a leading centre for a new financial paradigm that looks beyond profit and shareholder value to deliver social, economic or environmental impact as well as financial returns.”

In parallel Scottish Fintech can now boast over 120 Fintechs, connected with 15 universities, 16 tech spaces, accelerators and incubators. The conditions are fertile for cross pollination between responsible investing initiatives and Fintech. Yet Scottish Fintech and Scottish Asset Management are, at best, acquaintances rather than partners driving true innovation in responsible investment. Only by linking the success and innovation of Scottish Fintech with the opportunity in responsible investing can Scotland truly compete and succeed as a global leader. Bluntly put, Scottish asset managers and asset owners are missing a step in utilising the talent within Scottish Fintech.

Indeed a key observation in the report was the lack of collaboration between Scottish Fintech and Scottish asset managers in creating new solutions to expand investment, improve data and clarify the taxonomy (the universe of terminology). This is totally in keeping with what I set out as a New Fund Order’, the enablement and transformation of asset management through Fintech.

Stephen Ingledew, Chief Executive at FinTech Scotland said:

“Fintech innovation in asset management and capital markets is a fast emerging trend with a growing number of fintechs in Scotland developing innovative propositions to help the sector be more efficient and deliver better outcomes to investors. THis is being boosted by Scotland attracting many international fintech firms for example Agrud from Singapore and Actelligent from Hong Kong, who are attracted to Scotland because of university research capabilities and highly qualified students and professionals.”

The Scottish Asset Management Market

With £8 trillion AUM (as at end of 2019) the UK is currently the second largest global centre for asset management after the United States. Within the UK, Scotland is the second largest financial services centre after London, and includes the headquarters of Aberdeen Standard Investments – the largest active manager in the UK with a total AUM of £525 billion as of June 2019. Scotland is also a growing centre for fund administration (also referred to as asset servicing’), with strong corporate links with firms based in London and overseas.

Today, asset managers in Scotland include: Aberdeen Standard Investments, Aberforth Partners, Amati Global Investors, Ardstone Capital, Baillie Gifford, Blue Planet Investment Management, Cadence Investment Partners, Cameron Hume, Castlebay Investment Partners, Circularity Capital, Cornelian Asset Managers, Dalmore Capital, Dundas Global Partners, Edinburgh Partners, Kames Capital, Martin Currie, Panoramic Growth Equity, Pentech, Revera Asset Management, RM funds, Saracen Fund Managers, Stewart Investors, SVM Asset Management, Walter Scott & Partners and Valu-Trac. The following are now subsidiaries of larger asset managers based elsewhere: Kames Capital (Aegon Asset Management), Martin Currie (Legg Mason/Franklin Templeton), Edinburgh Partners (Franklin Templeton) and Walter Scott & Partners (BNY Mellon). Firms originally founded in Scotland, like Newton (also part of BNY), still retain a Scottish presence.

In addition, a number of asset managers headquartered elsewhere have branch offices in Scotland including: Liontrust Asset Management, Investec, Janus Henderson Asset Management, Franklin Templeton, BlackRock and Barclays. Lastly there are a number of smaller boutique firms, many of which straddle fund management and financial advice such as; Alan Steel Asset Management, Balmoral Asset Management, Charlotte Square Investment Managers, KPW Investments, Murray Asset Management, Odysseus Capital Management, Par Equity, Rossie House Investment Management, Rutherford Asset Management, Social Investment Scotland, TCAM and Trafford. Together these asset managers manage a mixture of open-end, mandates and closed-end funds for domestic and overseas investors, across a broad gamut of asset classes. The vast majority noted above (if not all) are categorised as active managers’ (that is, they do not track an index). Currently there are no Exchange Traded Fund (ETF) or passive’ (index tracking) providers based in Scotland.

Fintech Innovation is Happening but not Everywhere

We see more innovation in the asset servicing part of the market but again could grow significantly from here. Currently Scotland does not have any investment exchanges upon which to trade assets. Currencies are traded without a centralised location, rather the FOREX market is an electronic network of banks, brokers, institutions, and individual traders (mostly trading through brokers or banks). Scotland has no central clearing companies; for asset managers, the main firms that serve the UK are Euroclear, Clearstream, LCH Clearnet and Calastone. All are based in London or overseas. Similarly all of the large global custodians like State Street, RBC, BNY and Blackrock (that control >90% of the market) centralise their custody operations outside of Scotland. Scottish stock brokers include Redmayne Bentley, Speirs and Jeffries (acquired by Rathbones in 2018) and StockTrade. However the majority of brokerage is controlled by large investment banks like Morgan Stanley, JP Morgan and Goldman Sachs outside of Scotland.

Meanwhile smaller providers like Valu-Trac, based in Inverness, and Multrees Investment Services, based in Edinburgh, offer a range of fund management, administration, custody and back office services. A number of asset managers (e.g. JP Morgan, Morgan Stanley, Blackrock) also base their asset servicing and technology operations in Edinburgh and Glasgow. Computershare is a global leader in financial services and data management, working with around 16,000 global clients and their 125 million customers and having an established operation in Scotland providing relationship management and registry services to around 150 listed companies in Scotland and beyond.

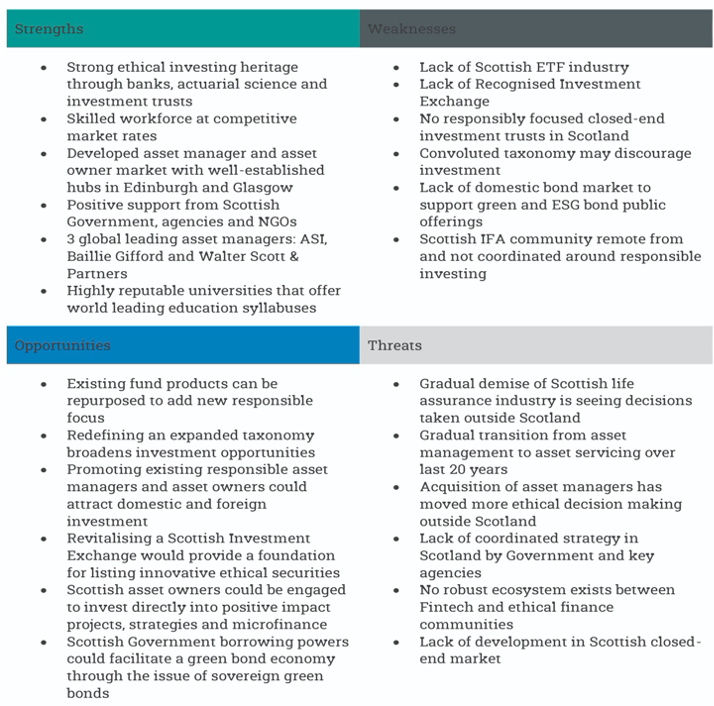

The analysis of the Scottish responsible investing market can be summarised in the following table of strengths, weaknesses, opportunities and threats.

Fig. Extract Mapping the Responsible Investing Landscape in Scotland’.

Page 55: SWOT Analysis’:

Conclusion: A Missed Opportunity

This innovation is not being replicated in the front and mid office of asset managers or asset owners and here the opportunity arises. Scotland lacks many of the traditional levers to stimulate responsible investment. This stymies the size the market could grow to. It also presents as a missed opportunity for Scottish Fintech. The goal is encouraging external investment into Scotland through asset management and asset owners. In doing so to become a global headquarters for responsible investment. Developing technology solutions and platforms to transplant these deficiencies calls on Fintech investment. The dawn of rTech’, responsible and sustainable Technology, with it the New Fund Order’ is set to becoming increasingly Green.

JB Beckett, Consultant, Ethical Finance Hub, Global Ethical Finance Initiative #GEFI #newfundorder #fintechscotland #scotlandisnow #scotlandistomorrow

Co-Author Mapping the Responsible Investing Landscape in Scotland’

Author New Fund Order 2.0 A Digital Resurrection’

Co-Author: The WealthTec Book’, AI Book’ and Paytech Book’

Photo by Karolina Grabowska from Pexels

LendingCrowd approved for accreditation under CBILS

Scottish fintech LendingCrowd, just announced it had been approved for accreditation by the British Business Bank as a new lender under the Coronavirus Business Interruption Loan Scheme (CBILS).

This accreditation will allow the fintech to distribute UK government-backed loans to SMEs impacted by the Covid-19 pandemic. LendingCrowd will provide loan product from £50,001 to £250,000 across either a three or a five-year term to SMEs who are experiencing lost or deferred revenues, leading to cashflow difficulties.

SMEs will have nothing to pay for the first 12 months so they can focus on bringing back their company to a healthier position.

Stuart Lunn, founder and CEO of LendingCrowd, said:

“We appreciate the stress and struggle that SMEs are going through and that time is of the essence in providing support. Our agile and flexible approach means that we can distribute funding responsibly to those who need it quickly. We have already spoken to every existing borrower, implemented repayment holidays for qualifying borrowers and changed repayment dates to better suit their cashflow patterns at no cost. In offering CBILS loans, LendingCrowd can play its part in supporting the survival and resurgence of as many SMEs as possible.”

If you’d like to apply for CBILS funding through LendingCrowd go to https://www.lendingcrowd.com/cbils

LendingCrowd will begin offering CBILS loans imminently and they will be available to new and existing borrowers, subject to eligibility.