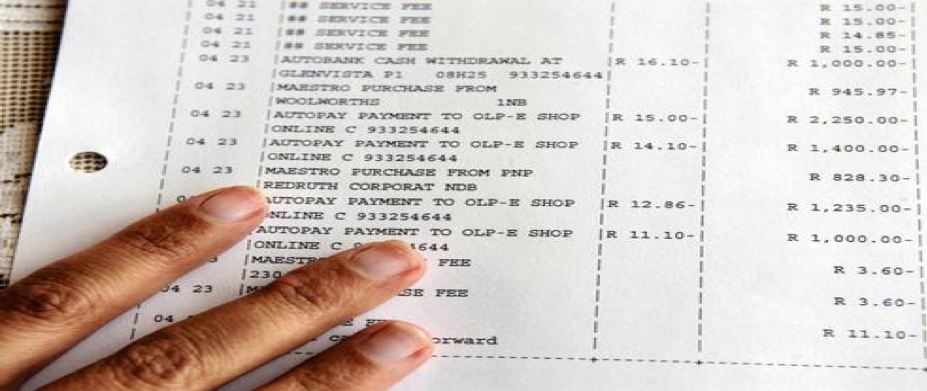

What the heck is that on my Bank statement?

We have all asked that question at one time or another, fretted and then called our Bank to see if it is fraud. Unfortunately, Banks know less than we do because the payment processors do not tell them what a transaction was for. The majority of these calls are about online purchases so friendly call center staff request that we check our email for a receipt.

For this reason I opened my pitch at EIE19 with the statement, With purchasing going on line, there are now 200x more email sent than there are Google searches’, grabbing the attention of the packed University of Edinburgh’s McEwan hall (my thanks to Danny Helson and the EIE team for an amazing event). It went down well, two days later I was pitching to a smart bunch of investors at ESM Investments.

The cost of not knowing

Finding an email receipt for the corresponding Bank transaction is almost impossible, email has become a dumping ground for spam, phishing and promotions. But it’s not just Fraud we worry about, we often want to find the receipt to return goods or use it to process a business expense. Banks also suffer, they field 6 million calls a year from customers concerned about online fraud (UK Finance.org reported that 78% (£393.4 million) of all fraud was online), at an average cost of £5 per enquiry, this costs the industry in excess of £30m a year. If Banks knew what was purchased they could make our customer experience better, for example, offering personalised Travel insurance to someone travelling abroad or putting an Uber button in their App to book the onward taxi and pushing the Uber receipt to the Expenses system to be automatically paid back.

Fixing the problem

As a Data Science business we wanted to find a solution to the problem, we decided to use Machine Learning to extract the data in email receipts and enrich the corresponding Banking transaction, we pursued this route for four reasons;

- Email was dead (email is dead – inc.com), it is becoming just another data source. It was plain that the world had moved on from Email and now prefers Whatsapp, etc for private communication but we all need an email address (and card) to buy things online.

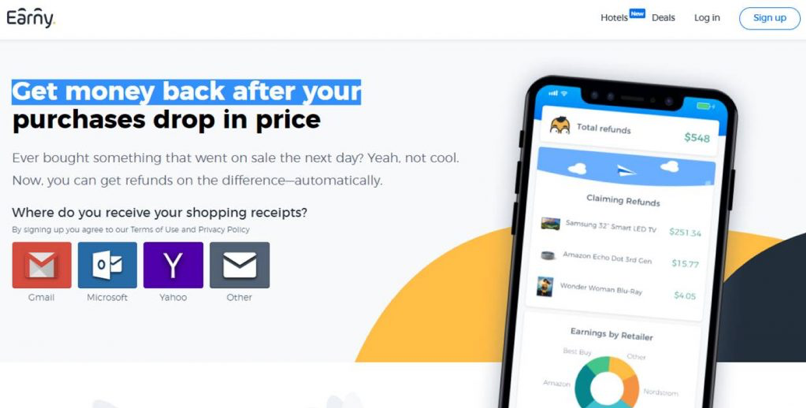

- US financial services were already doing similar stuff, companies like Capital One , Earny.co and Siftwallet.com had been at this for years – they read email receipts, obtained refunds and have amassed millions of users.

- Concerns about Privacy were not founded, especially in Millennials and Gen Zs, as this article Online value exchange by the Populus consultancy showed in The Drum.

- Apple and Google already use Machine Learning to auto add things to a Calendar (iOS 10 Siri auto adds events from email) or Wallet, Google now pulls Tickets and Loyalty data from Gmail and puts it in Google Pay (The Verge – April 16 2019).

Security and Application

Monily uses the same Machine Learning technology as Apple and Google to extract the data from the email receipt found on your Smartphone and populates the Bank transaction with the items you purchased, with no data going to the cloud. This makes it completely secure, safe and private. At first we developed our own App (Shoppa) but we came to realise the real benefits were for Retail and Business Banking, Personal Financial Management applications and Accounting solutions. Using our Splinter solution, we can help to reduce fraud enquiries by 50%, assist in selling personalised financial products and cut expense processing times down by 30%.

After years of development we are now actively selling the product and are pleased to be collaborating with Money Dashboard, pioneers in Personal Financial Management, and others to reduce fraud and improve expenses processing. If you would like to know more please email me on Adrian.James@moni.ly or visit Monily.co and I’ll get right back to you.

What is on this page:

Related content

Crypto firms fear being shut out of the UK market as operational readiness lags behind ambition

Why financial crime detection needs a new approach