7 Key trends in the P2P lending industry to prepare for

Photo by Maciej Pienczewski on Unsplash

Author: Vit Arnautov, Chief Product Officer, TurnKey Lender

According to Statista, by 2025 the P2P lending market is going to be worth 1 trillion dollars while just in 2015 it stood shy at 64 billion. The industry develops astonishingly fast and it’s not just hype (unlike Bitcoin in 2017). I believe the reasons for lenders and borrowers to switch to P2P are logical and pragmatic, which is exactly why the market will keep growing. As a Chief Product Officer at TurnKey Lender, a company that creates intelligent lending automation solutions, I have to stay alert to any new trends and developments and I’ll be happy to share what I foresee for the P2P lending industry in the near future.

1. More small to midsize lenders will enter the game

For many, the rise of the P2P model opened the doors into the world of financial services. Nowadays, it costs less than ever to get into the lending niche. No need for enormous investments and staff. Even the regulations aren’t as complex as the ones conventional banks go through.

This means that the old-school financial institutions now have a swarm of smaller and hungrier online competitors. But despite being small, the new P2P lenders often provide better service due to recent advances in lending technology and fully automated lending processes.

2. Banks don’t intend to give up

Large institutions have a harder time adjusting to the realities of the digital world and it takes them a ton of time to change their gears. But the boards of directors do see market trends and understand the need to go P2P. Slowly but surely banks worldwide start to introduce P2P functionality.

One of the pioneers in this regard was the N26 direct bank which struck a partnership with auxmoney, a German marketplace lender. Another example would be Monzo with their new peer-to-peer functionality. As of now, it’s mostly digital banks who are willing to start offering peer-to-peer lending. But the old-school banks also have to adjust as they go through their own digitalization. And it’s not just a theory. A prime example would be the Royal Bank of Scotland. All the way back in 2015 the company started to formally refer clients to Funding Circle and Assetz Capital for p2p loans. We can also look at two community banks, Titan Bank and Congressional Bank, who are buying loans through the Lending Club platform.

Traditional institutions often choose to develop their own solutions instead of using and customizing the existing and tested products that are already on the market. This route takes more time, the systems often turn out slow, clumsy, and not user-friendly. This means that only the banks with a more agile approach will adapt to the market to compete against the light-on-their-feet competitors.

Keep in mind, that for many people big banks still bring a sense of security and reliability. So in the nearest future small and midsize lenders will need to work a little harder and to market a little more aggressively to prove to the customers that they are every bit as good or even better. But P2P lenders are already doing really well and the big players in the field show that the success if very real to attain. Here are some growth stats of some of the leaders in the field:

- Lending Club – In Q4 of 2017 the company had issued $33.6bn in loans, while in Q4 of 2018 they were already at $44.5bn.

- RateSetter – The company announced that their 2017 to 2018 revenue growth reached 47%.

- Funding Circle – As of September 2018, Funding Circle has issued £6.3bn in loans. To reflect upon its growth the company has gone through an IPO.

3. Financial inclusion for underbanked areas

Take the two previous points into consideration and you’ll see that the market wins when a ton of smaller lenders compete with big banks. The loan prices go down and the businesses do their best to reach the previously underbanked areas and demographics. Global financial inclusion is the overarching goal of all the responsible members of the lending community and this competition serves this purpose perfectly.

The lending software providers create better solutions to process more of the right loans safer and faster and the lenders try to tap into new markets and demographics. For example, the AI-powered models used by Upstart (a p2p lending startup by ex-Googlers) result in 75% fewer defaults and 175% more approvals than those of traditional banks. The smart approval processes allow serving the people who were previously underserved in addition to providing a more flexible and fast online experience.

4. More markets and jurisdictions

The more governments see that P2P lending works, the more of them make it legal and start to work with it as they work with other financial instruments. Just last April the Central Bank of Brazil authorized P2P lending across the whole country and new governments join in all the time. For example, in Malaysia authorities introduced a P2P scheme for first time home buyers and in the US peer-to-peer lending is recognized and regulated by the SEC just as well as other financial instruments.

Some countries even go the route of Australia where financial startups can work without a license for a year which is called creating a FinTech sandbox. Jurisdictions that used similar mechanisms to stimulate the growth of the FinTech sector include UK, Switzerland, and Singapore.

5. Regulations

Don’t expect P2P lending to be the new “Wild West” where lenders can do whatever they want without any consequences. Governments have learned the lessons uncontrolled ICOs taught them.

In addition, authorities have seen China’s bitter experience of letting P2P function without sufficient control. There it led both to drastic growth and to dramatic fall of the industry. So in 2019 more governments won’t only allow and encourage P2P lending, but will also come up with specific ways to control the niche.

FinTech is still very young and governments often have troubles figuring out how to work with it and regulate it. But it’s safe to say that in 2019 the authorities will be far more focused on P2P lending. No one is really arguing that P2P lending is a good thing which should be allowed and encouraged. But at the same time, there are many influential voices who call for proper regulation, which is not necessarily a bad thing. As long as the rules are written to realistically reflect the state of the market and technology, any regulation should only do good in protecting both lenders and borrowers. Some examples that already apply come from the UK, with the ongoing updates from the Financial Conduct Authority to regulatory framework related to the P2P lending market. Also, in Canada, peer-to-peer lending is regulated under the same laws as securities. And in China, the government’s reaction to the meltdown of the industry was to tightly regulate the niche and weed out any wrongdoers before letting it grow any further.

6. The go-to choice for younger audiences

In Europe, over half of the P2P market is comprised of people aged 22-37. That’s no news that young people don’t want to deal with stuffy corporate organizations and choose the more user-friendly and up-to-date options when they can.

In addition to that young people often simply can’t get a loan on decent conditions from conventional lenders. Mostly since they simply don’t have the financial background baby boomers have. So the trend of young borrowers preferring the P2P lenders will continue.

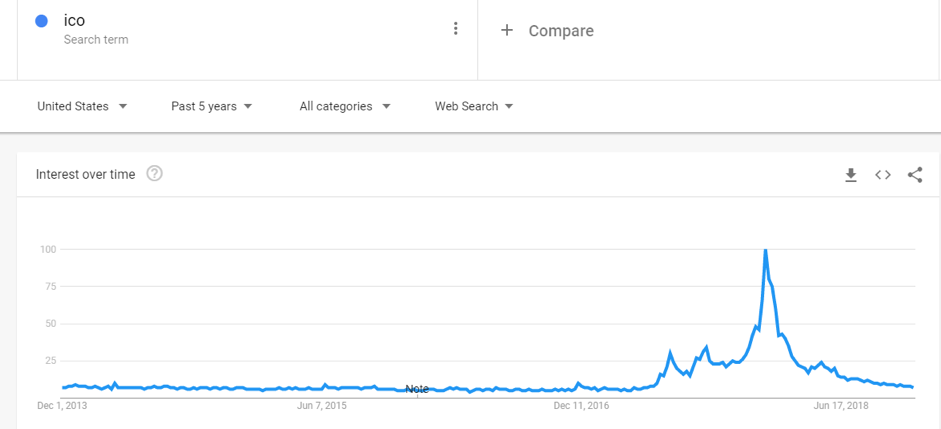

7. Fiat currencies prevail in 2019

For a while there it looked like every FinTech project needed to hold an ICO. P2P lending was no exception. But the trend is down for the best.

Either the public wasn’t ready for such a drastic shift of the paradigm or the technology and concept weren’t solid enough. Anyhow, it looks like we’re over ICOs for the time being. Even though projects may still effectively use blockchain as data storing and operating technology, there will be fewer crypto coins and more dollars and cents.

Final thoughts

It’s a great time to be in the P2P lending business. Not only are there still 3 billion unbanked people around the globe with no credit bureau score, but the technology we have makes it possible to get in the game without the huge investments. Now more than ever, all it takes is an entrepreneurial spirit and an idea.

What is on this page:

Related content

Building societies face growing “Digital Delivery Gap” as member expectations outpace communication infrastructure

University of Glasgow and Lloyds Banking Group announce groundbreaking agentic AI research programme